|

市場調查報告書

商品編碼

2063745

IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)HCM Software In IT And Telecom - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

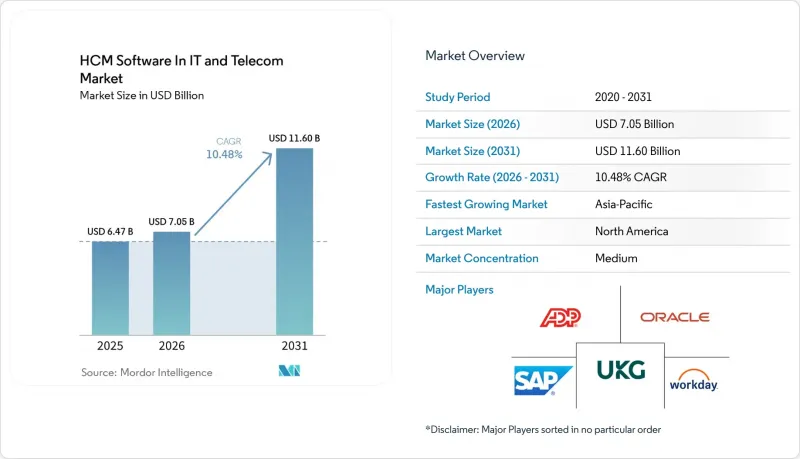

根據 Mordor Intelligence 預測,IT 和電信業 HCM 軟體的市場規模預計將從 2025 年的 64.7 億美元成長到 2026 年的 70.5 億美元,到 2031 年將達到 116 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 10.48%。

本報告按元件(軟體和服務)、部署模式(本地部署、雲端部署、混合部署)、應用程式(核心人力資源、人才管理、人力資源管理、薪資核算等)、企業規模(中小企業和大型企業)、最終用戶產業(IT服務等)和地區進行細分。市場預測以美元計價。

全球IT及電信HCM軟體市場趨勢及洞察

在IT技術棧中擴大雲端原生技術的應用

IT服務供應商和通訊業者正在將人力資源工作負載重構為容器化的微服務,以實現亞秒級的 API 回應時間,從而實現即時勞動力分配。 Workday 的歐盟主權雲將於 2025 年 11 月發布,使歐洲通訊業者能夠在不影響功能且符合 GDPR 要求的前提下,將資料保留在區域內。 SAP SuccessFactors 於 2026 年新增了 400 多項雲端原生增強功能,其中包含可處理 47 個國家/地區稅務調整的薪資核算機器人。與本地環境相比,這種架構遷移可將基礎架構開銷降低高達 35%,並將 MSP 的上線週期從數週縮短至數天。

人工智慧驅動的技能映射,協助通訊網路演進

亞太地區的通訊業者正在部署人工智慧引擎,透過分析資格和培訓記錄來預測哪些技術人員已準備好從銅線維護過渡到5G小型基地台建設。 Eightfold AI透過識別離職風險較高的工程師並觸發留任激勵措施,成功將離職率降低了22%。 SkillPanel等平台則透過提案個人化的技能提昇路徑,協助通訊業者將現有員工重新部署到開放式無線存取網(Open RAN)專案中,從而在90天內彌補技能差距。

對資料居住和主權的擔憂

遵守歐洲GDPR、中國CSL和印度DPDP法案的公司必須維護多個HCM(人力資源管理)系統。目前,供應商對自主雲端SKU收取15%至20%的附加費,這給已在5G部署方面投入大量資金的通訊業者的IT預算帶來了壓力。這種分散的情況導致實施週期延長至多六個月,並迫使增加額外的審計環節,加重了人力資源團隊的負擔。

細分市場分析

2025年,服務收入佔總收入的31.86%,但該年度的複合年成長率(CAGR)為13.76%,預計到2031年,IT和電信業人力資本管理(HCM)軟體市場中服務收入的佔有率將進一步擴大。系統整合商正在建立人工智慧驅動的排班引擎,並從本地部署的ERP系統中提取數十年的薪資歷史記錄——這些任務客戶往往不願自行完成。隨著軟體供應商引入能夠自動產生職位說明和薪酬方案的生成式輔助工具,軟體在IT和電信行業HCM軟體市場中的佔有率將保持顯著。然而,隨著授權續訂週期的成熟,訂閱成長正在趨於平緩。

大型託管服務供應商(MSP) 透過在其所有客戶中標準化 Dayforce、Oracle HCM Cloud 或 UKG,並簡化合約員工的入職流程,從而獲得持續的諮詢費收入。供應商也積極回應,提供包含資料提取和 90 天超前支援的固定價格遷移套餐,將原本一次性的授權交易轉變為多年的服務收入來源。

儘管預計到2025年雲端運算仍將保持56.88%的市場佔有率,但混合雲12.91%的複合年成長率表明,在預測期內,它將成為IT和通訊領域人力資本管理(HCM)軟體市場中成長最快的細分市場。企業在全球GPU容量可用的地區運行人才分析,同時將核心薪資核算資料儲存在獨立環境中,以符合GDPR和印度資料保護與資料保護(DPDP)法規的要求。這種配置也滿足了人工智慧工作負載的延遲要求。

混合部署的成長凸顯了雲端運算經濟與資料主權之間的矛盾。像Oracle這樣的供應商現在允許管理員對單一表格進行地理圍欄,確保薪資資料永遠不會離開本國,同時將員工敬業度調查的回覆同步到區域叢集進行情緒分析。預計本地部署將繼續萎縮,但一些受工會協議約束的通訊業者可能仍會繼續在本地託管系統,以滿足集體談判的要求。

區域分析

北美地區憑藉高雲端滲透率、充裕的創業投資資金和深厚的薪資核算專業知識,仍然是收入支柱,預計到2025年將佔37.12%的市場佔有率。 Workday、ADP和UKG的許多初始部署都始於北美,續約率也維持在90%左右。然而,儘管穩定的法規環境為人工智慧模組的提升銷售提供了空間,但預計未來的成長將是漸進的。

預計亞太地區將實現最快成長,到2031年複合年成長率將達到11.78%。這主要歸功於印度、印尼和菲律賓的通訊業者正在推動藍領員工的數位轉型,以最佳化其基地台的能源成本。印度和印尼的通訊業者也在推動其勞動力管理計畫的數位化,例如,du Telecom在2025年實施TCS的HCM平台後,效率提升了50%。各國的資料保護法迫使供應商建立國內資料區,這為本地系統整合商提供了立足點,並提升了HCM軟體在IT和電信領域的區域市場佔有率。通訊業特有的功能,例如自動危險津貼和生物識別考勤管理,正在推動通訊業者採用這些功能來管理分散的現場員工。

在歐洲,關於勞工委員會參與的嚴格規定以及工資平等指令顯著擴大了採用率。 GDPR帶來的數據主權投資推動了混合雲的普及,但宏觀經濟逆風和漫長的ERP系統替換過程減緩了許可證總數的成長。儘管如此,SAP和Workday推出的主權雲端產品仍保持了成長勢頭,並防止了市場佔有率的下滑。

由於需要即時儀錶板來展示國有化計畫中平民勞動力的比例,中東和非洲市場正在擴張。該地區對主權雲的需求與歐洲類似,但由於舊有系統負擔較輕,可以完全繞過本地環境,直接部署待開發區的SaaS解決方案。南美洲面臨貨幣波動,但巴西一個自動化eSocial報告的合規平台正在推動雲端遷移,並保持中等個位數的市場佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在IT技術棧中擴大雲端原生技術的應用

- 整合分析功能,助力投資報酬率視覺化

- 遷移到整合式員工體驗平台

- 分散式勞動力合規要求

- 專注於胡志明思維管理(HCM)的獨立軟體開發商(ISV)併購活動活性化

- 人工智慧驅動的技能映射,協助通訊網路演進

- 市場限制因素

- 對資料居住和主權的擔憂

- 傳統ERP系統的更新周期越來越長。

- 特定領域HCM整合商短缺

- 面臨利潤率壓力的通訊業者正在凍結資本投資。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 現場

- 雲

- 混合

- 透過使用

- 核心人力資源

- 人才管理

- 人力資源管理

- 薪資核算

- 其他用途

- 按組織規模

- 中小企業

- 大公司

- 按最終用戶行業分類

- IT服務

- 通訊業者

- 資料中心

- 託管服務供應商

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday Inc.

- SAP SE

- Oracle Corporation

- UKG Inc.

- ADP LLC

- Ceridian HCM Holding Inc.

- Cornerstone OnDemand Inc.

- Paycom Software Inc.

- Paylocity Holding Corporation

- The Sage Group plc

- Infor Inc.

- YourPeople Inc.(Zenefits)

- BambooHR LLC

- Gusto Inc.

- PeopleFluent Inc.

- Ceridian Dayforce, Inc.

- Ramco Systems Limited

- Kronos Systems Incorporated

- Rippling People Center Inc.

- Namely Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the hCM software in IT and telecom market size is expected to increase from USD 6.47 billion in 2025 to USD 7.05 billion in 2026 and reach USD 11.60 billion by 2031, growing at a CAGR of 10.48% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (On-Premises, Cloud, and Hybrid), Application (Core HR, Talent Management, Workforce Management, Payroll, and More), Organization Size (Small and Medium Enterprises, and Large Enterprises), End User Industry (IT Services, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HCM Software In IT And Telecom Market Trends and Insights

Growing Cloud-Native Adoption in IT Stacks

IT service providers and telecom operators are re-platforming HR workloads onto containerized microservices to gain sub-second API response times for real-time labor allocation. Workday's EU Sovereign Cloud release in November 2025 lets European carriers keep data in-region without losing functionality, aligning with GDPR demands. SAP SuccessFactors added more than 400 cloud-native enhancements in 2026, including payroll bots that reconcile taxes across 47 countries. The architecture shift cuts infrastructure overhead by up to 35% compared with on-premises estates and accelerates MSP onboarding cycles from weeks to days.

AI-Enabled Skill Mapping for Telecom Network Evolution

Asia-Pacific telecom operators deploy AI engines that parse certifications and training records to forecast which technicians can shift from copper maintenance to 5G small-cell builds. Eightfold AI identifies flight-risk engineers and triggers retention offers, lowering attrition by 22%. Platforms such as SkillPanel now propose personalized upskilling paths that close gaps within 90 days, helping carriers repurpose legacy staff for Open RAN projects.

Data Residency and Sovereignty Concerns

Enterprises juggling GDPR in Europe, China's CSL, and India's DPDP Act must maintain multiple HCM instances. Vendors now charge 15%-20% premiums for sovereign-cloud SKUs, squeezing IT budgets at carriers already funding 5G rollouts. The fragmented landscape prolongs implementation timelines by up to six months and forces additional audit layers that strain HR teams.

Other drivers and restraints analyzed in the detailed report include:

- Integrated Analytics Driving ROI Visibility

- Compliance Mandates for Distributed Workforces

- Prolonged Legacy ERP Replacement Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services accounted for 31.86% of 2025 revenue, but their 13.76% CAGR means this slice of the HCM software in IT and telecom market size will widen by 2031. Systems integrators configure AI shift-scheduling engines and extract decades of payroll history from on-premises ERPs, workloads that customers are reluctant to tackle alone. The HCM software in IT and telecom market share held by software will remain substantial because vendors embed generative copilots that auto-draft job descriptions and compensation offers, yet subscription growth is leveling as license renewal cycles mature.

Large MSPs standardize Dayforce, Oracle HCM Cloud, or UKG across client portfolios to streamline contractor onboarding, driving recurring advisory fees. Vendors respond with fixed-price migration bundles that include data extraction and 90-day hypercare, turning what was a one-time license transaction into a multiyear services annuity.

Cloud remained dominant at 56.88% in 2025, but hybrid's 12.91% CAGR positions it as the fastest-rising slice of the HCM software in IT and telecom market size over the forecast horizon. Enterprises store core payroll in sovereign environments to respect GDPR or India's DPDP rules while running talent analytics in global regions where GPU capacity sits, a configuration that still meets latency targets for AI workloads.

Hybrid growth underscores the tension between cloud economics and data sovereignty. Vendors such as Oracle now allow administrators to geofence individual tables so salary data never leaves the country, while engagement-survey responses sync to regional clusters for sentiment analysis. On-premises footprints will keep shrinking, though certain carriers bound by union accords continue to host systems locally to satisfy collective agreements.

Geography Analysis

North America remained the revenue anchor with 37.12% share in 2025, supported by high cloud penetration, abundant venture funding, and deep payroll domain expertise. Most early Workday, ADP, and UKG deployments originated here, and renewal rates stay near 90%. Yet regulatory stability means future growth moderates, even as upsell potential persists for AI modules.

Asia-Pacific delivers the fastest growth at an 11.78% CAGR through 2031 as carriers in India, Indonesia, and the Philippines digitize blue-collar labor to optimize tower energy spend. Carriers in India and Indonesia digitize labor management programs, du Telecom cited 50% efficiency gains after a 2025 deployment of TCS's HCM platform. Domestic data-protection laws push vendors to open in-country zones, creating a springboard for local integrators and boosting the region's slice of the HCM software in IT and telecom market size. Telecom-specific functionality, such as hazard-pay automation and biometric attendance, drives take-up among operators managing dispersed field crews.

Europe holds significant installed bases thanks to stringent works-council engagement rules and wage-equalization directives. GDPR-driven data-sovereignty spending lifts hybrid adoption, though macro headwinds and protracted ERP replacement slow total license growth. Still, sovereign-cloud releases from SAP and Workday preserve momentum, preventing share erosion.

The Middle East and Africa market expands because nationalization programs require real-time dashboards to prove citizen workforce ratios. Sovereign-cloud demand here mirrors Europe, yet limited legacy burden enables greenfield SaaS rollouts that skip on-premises entirely. South America faces currency volatility, but compliance platforms that automate Brazil's eSocial reporting keep cloud conversions moving, sustaining a mid-single-digit share.

- Workday Inc.

- SAP SE

- Oracle Corporation

- UKG Inc.

- ADP LLC

- Ceridian HCM Holding Inc.

- Cornerstone OnDemand Inc.

- Paycom Software Inc.

- Paylocity Holding Corporation

- The Sage Group plc

- Infor Inc.

- YourPeople Inc. (Zenefits)

- BambooHR LLC

- Gusto Inc.

- PeopleFluent Inc.

- Ceridian Dayforce, Inc.

- Ramco Systems Limited

- Kronos Systems Incorporated

- Rippling People Center Inc.

- Namely Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Cloud-Native Adoption in IT Stacks

- 4.2.2 Integrated Analytics Driving ROI Visibility

- 4.2.3 Shift Toward Unified Employee Experience Platforms

- 4.2.4 Compliance Mandates for Distributed Workforces

- 4.2.5 Rising M&A Activity Among Pure-Play HCM ISVs

- 4.2.6 AI-Enabled Skill Mapping for Telecom Network Evolution

- 4.3 Market Restraints

- 4.3.1 Data Residency and Sovereignty Concerns

- 4.3.2 Prolonged Legacy ERP Replacement Cycles

- 4.3.3 Shortage of Domain-Specific HCM Integrators

- 4.3.4 Capital-Expenditure Freeze in Telcos Under Margin Pressure

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Core HR

- 5.3.2 Talent Management

- 5.3.3 Workforce Management

- 5.3.4 Payroll

- 5.3.5 Other Applications

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By End User Industry

- 5.5.1 IT Services

- 5.5.2 Telecom Operators

- 5.5.3 Data Centers

- 5.5.4 Managed Service Providers

- 5.5.5 Other End User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 UKG Inc.

- 6.4.5 ADP LLC

- 6.4.6 Ceridian HCM Holding Inc.

- 6.4.7 Cornerstone OnDemand Inc.

- 6.4.8 Paycom Software Inc.

- 6.4.9 Paylocity Holding Corporation

- 6.4.10 The Sage Group plc

- 6.4.11 Infor Inc.

- 6.4.12 YourPeople Inc. (Zenefits)

- 6.4.13 BambooHR LLC

- 6.4.14 Gusto Inc.

- 6.4.15 PeopleFluent Inc.

- 6.4.16 Ceridian Dayforce, Inc.

- 6.4.17 Ramco Systems Limited

- 6.4.18 Kronos Systems Incorporated

- 6.4.19 Rippling People Center Inc.

- 6.4.20 Namely Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測

中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測