|

市場調查報告書

商品編碼

2063744

零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)HCM Software In Retail - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

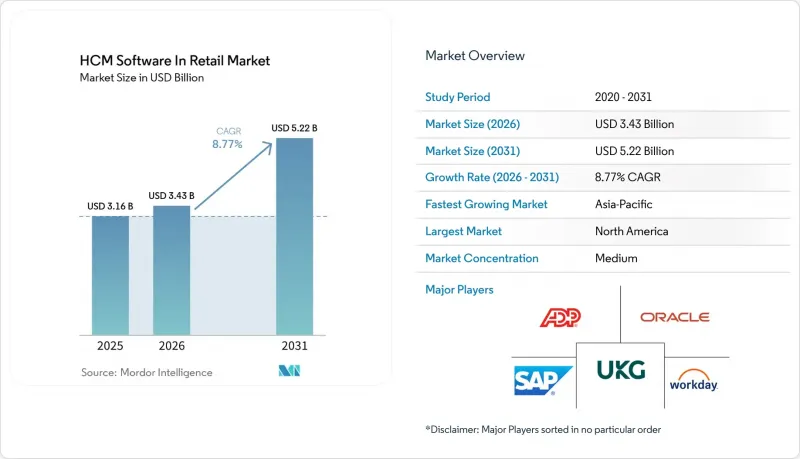

根據 Mordor Intelligence 預測,零售業 HCM 軟體的市場規模預計將從 2025 年的 31.6 億美元成長到 2026 年的 34.3 億美元,到 2031 年將達到 52.2 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 8.77%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、職能(薪資管理、勞動力管理、人才管理、核心人力資源、學習與發展以及其他職能)和地區進行細分。市場預測以美元計價。

全球零售業人力資本管理軟體市場趨勢與洞察

擴大雲端HCM套件的採用

零售商正從資本密集的本地部署系統轉向基於訂閱的雲端套件,以利用季度功能更新、嵌入式分析和自動化監管更新。在2026年1月的一份說明中,Workday指出零售業的合約制定週期正在加速,並引用連鎖店對行動時間追蹤和合規儀表板的需求作為推動因素,前提是這些需求無需承擔現場IT營運成本。 Dayforce被私募股權以123億美元收購,進一步鞏固了投資者對多租戶SaaS模式經濟效益優於永久授權模式的信念。像Belk這樣的中型企業在遷移到Workday後,已實現了300家門市的薪資核算、福利和工作安排的集中管理,從而避免了升級舊有系統帶來的延誤。此外,雲端供應商也承擔了有關加班費和資料居住的監管責任,這在香港「468」加班制度和歐盟《工資透明度指令》將於2026年生效之際,是一項顯著優勢。

人們對行動優先、自助式人力資源應用程式的興趣日益濃厚。

智慧型手機應用程式可讓員工隨時交換班次、更新空閒時間並查看薪資單,從而減輕了管理人員的工作量。 Sona 預計在 2025 年實施該系統後,總人事費用將降低 0.8% 至 4.0%,並節省先前用於手動更改排班的 40 小時行政時間。 Legion 的現場員工每週活躍使用率已達到 88%,即時透明度使離職率降低了三分之一。 isolved 和 Darwinbox 應用程式中的地理圍欄和生物識別可有效防止時間欺詐,並支援可審計的考勤記錄。該技術的應用主要集中在亞太地區,CARSOME 計劃在 2026 年 2 月前在四個國家的 3000 名員工中部署 Darwinbox 的行動工資系統。

員工資訊系統中的資料隱私和網路安全風險

員工記錄包括社會安全號碼、工資數據和健康信息,所有這些都是網路犯罪分子的目標。 2025年8月發生的Workday資料外洩事件迫使零售客戶緊急修補漏洞,並提醒經營團隊,人力資本管理(HCM)平台處理著一些最敏感的個人資料。由於GDPR罰款可能高達全球銷售額的4%,在歐洲營運的零售商現在正敦促供應商將資料儲存在歐盟境內,並記錄所有傳輸。美國律師協會警告說,人工智慧篩檢機器人可能被惡意輸入資料操縱,一次事件可能使公司面臨駭客攻擊和民權訴訟的雙重風險。

細分市場分析

預計到2031年,服務市場將以11.01%的複合年成長率成長,超過軟體市場佔有率(2025年軟體市佔率將達66.42%)。零售業人力資本管理(HCM)軟體服務市場的規模反映出,平台訂閱合約只是起點,在地化、測試和持續的監管合規才是推動支出成長的真正動力。Accenture、德勤和普華永道等領先的顧問公司正在將HCM部署整合到更廣泛的數位轉型中,而一些精品整合商則專注於印尼和墨西哥等市場的法定薪資核算管理。儘管由於薪資核算系統作為記錄系統,對軟體的依賴性仍然很高,但功能融合正在加速,價值創造正轉向諮詢和最佳化層面。 Rolling Arrays在2026年4月發布的說明強調,東南亞客戶在評估供應商時,不再以功能等效性為標準,而是以運作後的營運能力為標準。

對於業務遍及十多個國家的零售商而言,服務合作夥伴需要協調區域稅率表、工會規則和語言包,並且該模式正朝著外包薪資核算結算和合規性審計的管理服務模式發展。 IDC 的數據顯示,亞太地區 60% 的企業每次監管機構調整勞動法時都會面臨營運中斷,因此基於服務等級協定 (SLA) 的支援至關重要。因此,能夠將技術與區域服務架構相結合的供應商在零售業人力資本管理 (HCM) 軟體市場中的重要性日益凸顯,隨著歐盟薪資差距報告和美國公平工作週法案的實施,這一趨勢預計將會加劇。

混合部署預計將以 10.67% 的複合年成長率成長,透過將現代人才管理工具與現有薪資資料庫整合,有望超越早期純雲端解決方案的吸引力。許多連鎖店在本地部署 SAP 或 Lawson 薪資系統,並在其上疊加 Oracle Recruiting、SuccessFactors Learning 或 Workday Skills Cloud 等系統,並透過整合中心路由數據,這需要進行嚴格的端到端測試。截至 2025 年,基於雲端的 HCM 軟體仍以 54.11% 的市佔率在零售業中佔據主導地位。這是因為 SaaS 無需打補丁,並簡化了門市部署。然而,如果需要在標準 SaaS 架構上重建高度客製化的加班邏輯,則投資報酬率可能會降低。

正在考慮系統遷移的零售企業正在評估勞動力管理究竟是競爭優勢還是只是一項實用功能。如果是前者,他們會接受實施一套最佳組合方案所帶來的成本。如果只是一項實用功能,他們會選擇類似 SAP H4S4 這樣的核心-混合橋樑方案,該方案在保留薪資核算基礎架構的同時,增添了現代化的使用者體驗。Accenture指出,混合方案會使測試工作量翻倍,因為每次薪資核算週期,工作流程都會跨越系統邊界。儘管如此,這種方案允許風險規避型的財務長逐步減少支出,逐步提升人力資源團隊的技能,並在不承擔薪資核算失敗帶來的負面影響的情況下保持業務成長勢頭。

區域分析

北美擁有先進的勞動法和人工智慧的早期應用,預計到2025年將佔全球銷售額的38.22%。美國零售商必須遵守全美50個州的工資法規,並在城市層級實施預測性排班,這使得自動化合規性成為董事會層級的重要議題。供應商正透過地理感知規則引擎和工資盜竊警報等功能來應對這項挑戰,這些功能如今已成為零售市場人力資本管理(HCM)軟體的標配。同時,有關演算法偏見的訴訟也開始出現,這催生了對可解釋人工智慧和公平性儀表板的需求。

亞太地區是成長最快的地區,複合年成長率達10.45%。在東南亞行動優先的勞動力推動下,印度有組織的零售業蓬勃發展;而中國的連鎖商店則將人力資本管理(HCM)直接整合到社交電商和即時配送應用程式中。根據ETHRWorld的數據,該地區65%的人力資源經理計劃在2026年增加人工智慧預算,但只有11%的人認為已做好充分準備,這為服務合作夥伴創造了龐大的商機。政府主導的數位化舉措,例如新加坡的「數位勞動力」舉措,正在進一步加速雲端HCM的普及應用。

歐洲的成長並非源自於門市數量的增加,而是監管政策的改變。歐盟的《工資透明指令》(將於2026年6月生效)將要求所有擁有100名以上員工的零售商揭露其工資結構並解釋性別薪資差距。這將起到催化劑的作用,隨著企業加強其報告機制,零售市場對人力資本管理(HCM)軟體的需求將會提升。 GDPR的資料居住要求將縮小供應商的選擇範圍,使資料中心位於歐盟境內的平台更具優勢。雖然南美、中東和非洲的市場佔有率較小,但都市區正在經歷局部高速成長,國際特許經營公司正在效仿北美的合規做法。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大雲端HCM套件的採用

- 人們對行動優先的自助式人力資源應用程式越來越感興趣。

- 擴大人工智慧驅動的人才分析的應用

- 跨州零售管轄區的合規性日益複雜。

- 微型倉配零售模式的快速成長需要靈活的勞動力排班。

- 透過整合HCM和POS平台來提高門市生產力

- 市場限制因素

- 員工資訊系統中的資料隱私和網路安全風險

- 遷移舊式人力資源系統高成本且複雜。

- 零售業人工智慧招募工具中與演算法偏見相關的訴訟風險

- 季節性勞動力波動正在削弱對全套人力資本管理系統的投資報酬率。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 按部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按功能

- 薪資管理

- 勞動力管理

- 人才管理

- 核心人力資源

- 學習與發展

- 其他功能

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Automatic Data Processing, Inc.

- Workday, Inc.

- SAP SE

- Oracle Corporation

- UKG Inc.

- Ceridian HCM Holding Inc.

- Paycom Software, Inc.

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Ramco Systems Limited

- PeopleFluent, Inc.

- Cegid Group SA

- The Sage Group plc

- Gusto, Inc.

- Rippling People Center Inc.

- HiBob Ltd.

- Darwinbox Digital Solutions Private Limited

- Paycor, Inc.

- Deel Inc.

- TriNet Zenefits, Inc.

- SumTotal Systems, LLC

- Paychex, Inc.

- Namely, Inc.

- SmartRecruiters, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the hCM software in retail market size is expected to increase from USD 3.16 billion in 2025 to USD 3.43 billion in 2026 and reach USD 5.22 billion by 2031, growing at a CAGR of 8.77% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Function (Payroll Management, Workforce Management, Talent Management, Core HR, Learning and Development, and Other Functions), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HCM Software In Retail Market Trends and Insights

Rising Adoption of Cloud-Based HCM Suites

Retailers are shifting capex-heavy on-premises systems to subscription-based cloud suites to access quarterly feature drops, embedded analytics and automatic legislative updates. Workday cited faster retail deal cycles in its January 2026 commentary, attributing momentum to chains seeking mobile time tracking and compliance dashboards without onsite IT overhead. Private equity's USD 12.3 billion Dayforce take-private underscores investor conviction that multi-tenant SaaS economics outperform perpetual-license models. Mid-market adopters such as Belk unified payroll, benefits and scheduling across 300 stores after moving to Workday, eliminating legacy upgrade backlogs. Cloud vendors also shoulder liability for overtime and data-residency rules, an advantage as Hong Kong's "468" overtime regime and the EU Pay Transparency Directive come online in 2026.

Growing Focus on Mobile-First Self-Service HR Applications

Smartphone apps are shrinking manager-mediated workflows by letting associates swap shifts, update availability and view pay slips on demand. Sona's 2025 rollouts saved between 0.8%-4.0% of total payroll and returned 40 manager hours per week previously lost to manual schedule changes. Legion recorded 88% weekly active usage among frontline staff, cutting attrition by one-third thanks to real-time transparency. Geofenced clock-ins and biometric validation in isolved and Darwinbox apps curb time theft and support audit-ready attendance logs. Adoption trends skew toward Asia-Pacific, where CARSOME deployed Darwinbox's mobile payroll across 3,000 staff in four countries by February 2026.

Data Privacy and Cybersecurity Risks in Employee Information Systems

Employee records house social security numbers, pay data and health details prized by cybercriminals. Workday's August 2025 breach forced emergency patches across retail clients and reminded boards that HCM platforms sit on some of the most regulated personal data. GDPR fines can reach 4% of global turnover, so retailers operating in Europe now require vendors to store data within EU borders and document every transfer. The American Bar Association warns that adversarial inputs can manipulate AI screening bots, exposing companies to both hacking events and civil-rights suits in one incident.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Use of AI-Driven Workforce Analytics

- Escalating Compliance Complexity Across Multi-State Retail Jurisdictions

- High Cost and Complexity of Migrating Legacy HR Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are expanding at an 11.01% CAGR through 2031, outpacing software's dominant 66.42% share in 2025. The HCM software in retail market size for services reflects the reality that platform subscriptions only launch the journey; localization, testing and ongoing regulatory tuning now drive spend. Consulting majors such as Accenture, Deloitte and PwC integrate HCM rollouts into wider digital transformations, while boutique integrators specialize in statutory payroll for markets like Indonesia and Mexico. Software remains sticky because payroll engines are the system of record, yet functionality converges fast, pushing value creation into advisory and optimization layers. Rolling Arrays' April 2026 commentary stressed that Southeast Asian clients judge providers on post-go-live discipline, not feature parity.

For retailers spanning 10-plus countries, services partners juggle localized tax tables, union rules and language packs, evolving into managed-service models that outsource payroll closing and compliance audits. IDC data show 60% of Asia-Pacific enterprises face operational disruption whenever regulators tweak labor codes, making SLA-backed support indispensable. Consequently, the HCM software in retail market increasingly values vendors able to package technology with regional service benches, a trend expected to deepen as EU pay-equity reports and U.S. fair-workweek laws proliferate.

Hybrid deployments are projected to grow at a 10.67% CAGR, eclipsing pure-cloud's early glamour by reconciling modern talent tools with entrenched payroll databases. Many chains keep SAP or Lawson payroll on-prem but layer Oracle Recruiting, SuccessFactors Learning or Workday Skills Cloud on top, routing data via integration hubs that demand rigorous end-to-end testing. The HCM software in retail market share for cloud still leads at 54.11% in 2025 because SaaS eliminates patching and eases store roll-outs, yet ROI can erode when deeply customized overtime logic must be rebuilt on a vanilla SaaS stack.

Retailers weighing their journey assess whether workforce management is a differentiator or utility. If differentiator, they accept change costs for best-of-breed suites. If utility, they opt for core-hybrid bridges like SAP's H4S4 that preserve payroll DNA while adding modern UX. Accenture cautions that hybrids require twice the test effort, as workflows cross system boundaries in every pay cycle. Still, this path lets risk-averse CFOs stage spend and upskill HR teams gradually, sustaining momentum without payroll failure headlines.

Geography Analysis

North America retained 38.22% of global revenue in 2025 due to sophisticated labor codes and early AI adoption. U.S. retailers grapple with 50 state wage laws plus city-level predictive scheduling, making compliance automation a board concern. Vendors respond with geo-coded rules engines and wage-theft alerts, features now standard in the HCM software in retail market. Algorithmic bias lawsuits also germinate here, injecting demand for explainable AI and fairness dashboards.

Asia-Pacific is the fastest riser at a 10.45% CAGR. India's organized retail booms alongside Southeast Asia's mobile-first workforce, while Chinese chains weave HCM directly into social-commerce and instant-delivery apps. ETHRWorld data show 65% of HR leaders in the region will boost AI budgets in 2026, yet only 11% feel fully prepared, opening doors for services partners. Government digitization pushes, such as Singapore's Digital Workforce initiative, further accelerate cloud HCM uptake.

Europe's growth rides on rule changes instead of store count expansion. The EU Pay Transparency Directive effective June 2026 forces every retailer above 100 employees to publish wage structures and justify gender pay gaps, a catalyst pushing the HCM software in retail market size upward as firms upgrade reporting pipelines. GDPR's data-residency demands splinter vendor choices, favoring platforms with EU-hosted data centers. South America, the Middle East and Africa contribute smaller shares but show spotty high growth in urban corridors where international franchises replicate North American compliance playbooks.

- Automatic Data Processing, Inc.

- Workday, Inc.

- SAP SE

- Oracle Corporation

- UKG Inc.

- Ceridian HCM Holding Inc.

- Paycom Software, Inc.

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Ramco Systems Limited

- PeopleFluent, Inc.

- Cegid Group SA

- The Sage Group plc

- Gusto, Inc.

- Rippling People Center Inc.

- HiBob Ltd.

- Darwinbox Digital Solutions Private Limited

- Paycor, Inc.

- Deel Inc.

- TriNet Zenefits, Inc.

- SumTotal Systems, LLC

- Paychex, Inc.

- Namely, Inc.

- SmartRecruiters, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Cloud-Based HCM Suites

- 4.2.2 Growing Focus on Mobile-First Self-Service HR Applications

- 4.2.3 Increasing Use of AI-Driven Workforce Analytics

- 4.2.4 Escalating Compliance Complexity Across Multi-State Retail Jurisdictions

- 4.2.5 Surge in Micro-Fulfillment Retail Formats Requiring Agile Labor Scheduling

- 4.2.6 Integration of HCM with Point-of-Sale Platforms Enhancing Store Productivity

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Risks in Employee Information Systems

- 4.3.2 High Cost and Complexity of Migrating Legacy HR Systems

- 4.3.3 Algorithmic Bias Litigation Risk in AI Recruiting Tools for Retail

- 4.3.4 Seasonal Workforce Volatility Undermining ROI on Full-Suite HCM Investments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Function

- 5.4.1 Payroll Management

- 5.4.2 Workforce Management

- 5.4.3 Talent Management

- 5.4.4 Core HR

- 5.4.5 Learning and Development

- 5.4.6 Other Functions

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 Workday, Inc.

- 6.4.3 SAP SE

- 6.4.4 Oracle Corporation

- 6.4.5 UKG Inc.

- 6.4.6 Ceridian HCM Holding Inc.

- 6.4.7 Paycom Software, Inc.

- 6.4.8 Cornerstone OnDemand, Inc.

- 6.4.9 BambooHR LLC

- 6.4.10 Ramco Systems Limited

- 6.4.11 PeopleFluent, Inc.

- 6.4.12 Cegid Group SA

- 6.4.13 The Sage Group plc

- 6.4.14 Gusto, Inc.

- 6.4.15 Rippling People Center Inc.

- 6.4.16 HiBob Ltd.

- 6.4.17 Darwinbox Digital Solutions Private Limited

- 6.4.18 Paycor, Inc.

- 6.4.19 Deel Inc.

- 6.4.20 TriNet Zenefits, Inc.

- 6.4.21 SumTotal Systems, LLC

- 6.4.22 Paychex, Inc.

- 6.4.23 Namely, Inc.

- 6.4.24 SmartRecruiters, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年) 中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測

中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測