|

市場調查報告書

商品編碼

2063694

AI資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)AI Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

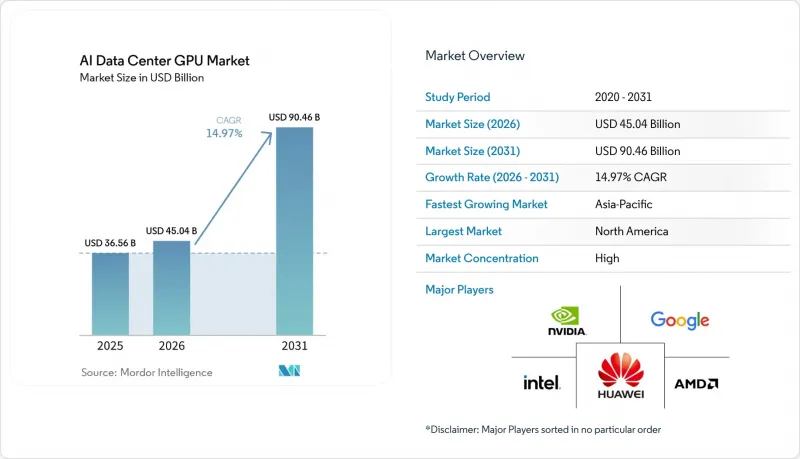

根據 Mordor Intelligence 預測,人工智慧資料中心 GPU 市場規模將從 2025 年的 365.6 億美元成長到 2026 年的 450.4 億美元,到 2031 年將達到 904.6 億美元,2026 年至 2031 年的複合年成長率為 14.97%。

本報告按部署類型(雲端資料中心、企業和私人資料中心等)、GPU 類型(訓練 GPU、推理 GPU)、互連方式(基於 PCIe 的 GPU、高頻寬互連 GPU)、最終用戶(超大規模資料中心業者中心和雲端服務供應商、企業、政府和研究機構)以及地區進行細分。市場預測以美元 (USD) 為單位。

全球人工智慧資料中心GPU市場趨勢與洞察

生成式人工智慧模型規模的爆炸性成長

大規模語言和多模態模型如今的參數量已超過兆,而諸如強化學習結合人類反饋、合成數據增強和長文本上下文推理等訓練後擴展過程,其計算資源消耗量高達原始預訓練運行的30倍。因此,營運商優先考慮封裝記憶體容量龐大的GPU。 AMD的MI325X配備了288GB的HBM3e顯存,使得單一伺服器即可運行兆參數模型,並消除了跨節點分剪切機造成的延遲。 NVIDIA的Blackwell架構將每百萬代幣的成本降低了15倍,降至約0.02美元。這使得計量收費API在企業級規模下更具經濟效益。超大規模資料中心超大規模資料中心業者正以創紀錄的資本投入積極響應,預付合約也確保了晶圓生產和先進封裝的供應。這正在推動市場需求,並鞏固人工智慧資料中心GPU市場的成長動能。

GPU加速雲端服務的快速普及

將生成式人工智慧直接整合到生產力軟體中已被證明高效且獲利,促使雲端服務供應商以前所未有的規模採購GPU。微軟在短短四個月內售出了超過800萬份付費Gemini Enterprise許可證,而Google雲端在2025年第四季的營收年增48%,這主要得益於Gemini在2800家企業客戶中的部署。這些工作負載推動了積極的採購,因為GPU叢集的投資可以在兩年內收回成本。諸如微軟向Nscale訂購3萬塊GPU用於其位於挪威的230兆瓦資料中心等多年期並行供應協議,凸顯了市場對人工智慧資料中心GPU市場現金流的信心。

先進封裝技術的供需失衡問題依然存在。

高頻寬記憶體 (HBM) 堆疊和 CoWoS 中介層持續面臨長期供不應求。 HBM 晶片面積約為傳統 DRAM 的 2.5 倍,而 TSV 的複雜性導致缺陷率上升,迫使供應商預留晶圓面積以應對較低的良率。美光 2026 年的 HBM 產能已售罄,儘管三星的 HBM 銷量成長了兩倍,但仍以接近 10% 的價格漲價。台積電 9.5 升產能限制的延長在 2027 年之前不會顯著提高 CoWoS 的產能。供不應求正在減緩 Rubin 和 MI400 的量產速度,迫使供應商將首批產品分配給高利潤買家,這可能會延遲中小規模雲端服務和企業用戶的供貨。

細分市場分析

到2025年,雲端設施將佔總收入的66.38%。這主要得益於千兆瓦級園區整合了水冷機架式資料中心,每個資料中心可容納超過10萬個GPU。雖然企業正在利用這種集中式容量將運算成本分攤到數千個租戶,但不斷上漲的出站資料通訊費用和日益嚴格的隱私法規正促使部分工作負載回歸企業內部或國內資料中心。邊緣資料中心目前仍是一個小眾市場,但預計到2031年將以15.57%的複合年成長率成長,這主要得益於自動駕駛汽車、機器人單元和即時工業檢測等領域對低於10毫秒往返延遲的需求。

為了實現不同環境間的無縫模型遷移,供應商正在加速軟體重構。例如,NVIDIA 的 BlueField-4 資料處理單元 (DPU) 層發揮著至關重要的作用,它將鍵值快取從核心傳輸到邊緣。這種方法顯著減少了冗餘的 GPU 記憶體分配,並最佳化了資源利用率。這些進步共同推動了 AI 資料中心 GPU 市場的雙管齊下式成長。超大規模資料中心正在經歷顯著成長,而聯邦微型站點也在擴張,儘管它們的架構水平截然不同。這些趨勢凸顯了為滿足不斷變化的 AI 工作負載需求而採用的各種策略。

預計到2025年,推理加速器將佔總收入的54.23%,並以15.37%的複合年成長率成長,超過訓練GPU,這得益於其穩健的憑證式的盈利模式。微調、檢索增強生成和即時個人化正在推動持續的推理週期,預計到2026年,這些應用將佔計算支出的三分之二左右。訓練GPU對於創建最先進的模型至關重要,但隨著效能提升速度的放緩(即使參數略有增加),它們的佔有率正在下降。

硬體廠商正透過混合精度管線來解決這個問題;NVIDIA Rubin 搭載了第三代 Transformer Engine,而 AMD MI325X 則將其 HBM 容量翻倍,從而在單塊電路板上整合了一個兆參數的解譯器。所有這些創新都進一步推動了推理成本的上升。因此,超大規模資料中心業者正日益將其 GPU 叢集進行二分:最新的高互連 GPU 用於大規模批量訓練,而推理叢集則配備針對每個令牌成本最佳化的高記憶體密度顯示卡。

區域分析

預計到2025年,北美將佔總收入的37.50%,這得益於其接近性主要雲端服務供應商總部,以及德克薩斯州、中西部和太平洋西北地區充足的電力供給能力。美國政策繼續優先考慮國內分配,2026年1月生效的出口管制修正案對某些高階GPU出口徵收25%的關稅,並有效保障了國內供應。 Applied Digital在Delta Forge 1專案簽訂的300兆瓦租賃合約等大型租賃協議,凸顯了美國建築業的長期成長潛力。歐洲則呈現集中但戰略性的成長態勢。微軟在挪威納爾維克簽訂的3萬塊Rubin GPU契約,凸顯了寒冷地區對可再生能源供電園區的需求,以應對不斷上漲的碳排放稅。英國正在向其「主權人工智慧部門」投資 5 億英鎊(6.3 億美元),承諾為每個新創公司提供 100 萬 GPU 小時的津貼,並直接投資於基礎設施編配公司。

預計到2031年,亞太地區將成為成長最快的地區,複合年成長率(CAGR)將達到15.97%。日本政府斥資120億美元在鹿兒島建設的GMI雲端主權資料中心,目標是1吉瓦的裝置容量,並試圖將其打造成為日本國內機器人、自動駕駛汽車和重工業人工智慧工作負載的製造地。中國正面臨美國日益嚴格的出口限制和進口NVIDIA H200晶片的關稅壁壘,因此正積極推動華為、寒武紀和維倫等國產加速器產品的採購。然而,由於良率和軟體成熟度的差異,短期內效能可能會出現滯後。同時,印度正在加速核准兆瓦級園區項目,而韓國的三星和SK海力士正在擴大其HBM4生產線,以期在GPU價值鏈的上游獲取價值。

儘管南美、中東和非洲的市場佔有率較小,但它們在低成本可再生能源領域扮演著「快速追隨者」的角色。 2025年5月,沙烏地阿拉伯和阿拉伯聯合大公國政策發生轉變,取消了「檢驗的最終用戶」框架下先進GPU的進口限制,並利用其豐富的天然氣和太陽能資源,達成了具有競爭力的購電協議。雖然這些地區的市場規模無法與北美或亞太地區相提並論,但它們為進入人工智慧資料中心GPU市場的供應商提供了更大的成長潛力和地理風險分散的機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 生成式人工智慧模型規模的爆炸性成長

- GPU加速雲端服務的快速普及

- 資料中心級 GPU叢集突破 10 萬個 GPU 大關。

- 採購中 MLPerf 基準的標準化

- 小規模經濟體中國家主導的人工智慧舉措的興起

- 水冷系統的改造升級正在推動產品更新換代。

- 市場限制因素

- 先進封裝領域持續存在的供需失衡

- 風冷機架總擁有成本增加

- 高階GPU出口限制

- 人們越來越傾向於選擇客製化的AI加速器而不是GPU。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 雲端資料中心

- 企業和私人資料中心

- 邊緣資料中心

- 按GPU類型

- 訓練 GPU

- 用於推理的GPU

- 依類型互連

- 基於 PCIe 的 GPU

- 高頻寬互連GPU

- 最終用戶

- 超大規模資料中心業者和雲端服務供應商

- 公司

- 政府和研究機構

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Google LLC

- Amazon Web Services, Inc.

- Microsoft Corporation

- Alibaba Group Holding Limited

- Baidu, Inc.

- Huawei Technologies Co., Ltd.

- Graphcore Ltd.

- SambaNova Systems, Inc.

- Cerebras Systems Inc.

- Tenstorrent Inc.

- Qualcomm Technologies, Inc.

- IBM Corporation

- Giga Computing Technology Co., Ltd.

- Super Micro Computer, Inc.

- ASUStek Computer Inc.

- Dell Technologies Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the aI data center GPU market size is expected to grow from USD 36.56 billion in 2025 to USD 45.04 billion in 2026 and is forecast to reach USD 90.46 billion by 2031 at a 14.97% CAGR over 2026-2031.

This report is Segmented by Deployment Mode (Cloud Data Centers, Enterprise and Private Data Centers, and More), GPU Type (Training GPUs, and Inference GPUs), Interconnect (PCIe-Based GPUs, and High-Bandwidth Interconnect GPUs), End-User (Hyperscalers and Cloud Service Providers, Enterprises, and Government and Research Institutions), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI Data Center GPU Market Trends and Insights

Explosive Growth in Generative AI Model Size

Large language and multimodal models are ballooning past the trillion-parameter mark, and post-training scaling steps such as reinforcement learning from human feedback, synthetic data expansion, and long-context reasoning now consume up to 30 times the compute of the original pre-training run. Operators therefore prioritize GPUs with enormous on-package memory; AMD's MI325X offers 288 GB of HBM3e, enabling a single server to host a 1-trillion-parameter model and eliminating cross-node sharding delays. NVIDIA's Blackwell architecture improves cost per million tokens by 15-fold, down to roughly USD 0.02 per million tokens, making pay-as-you-go API economics viable at enterprise scale. Hyperscalers are responding with record capex, and prepayment contracts are locking in both wafer starts and advanced packaging slots, effectively pulling demand forward and solidifying the AI data center GPU market's growth trajectory.

Rapid Adoption of GPU-Accelerated Cloud Services

Embedding generative AI directly into productivity software is proving sticky and high-margin, prompting cloud providers to reserve unprecedented quantities of GPUs. Microsoft sold more than 8 million paid Gemini Enterprise seats within four months, while Google Cloud revenue surged 48% year-over-year in Q4 2025 on the back of Gemini roll-outs across 2,800 corporate customers. These workloads amortize GPU fleets in under two years, reinforcing aggressive procurement. Parallel multiyear supply contracts, such as Microsoft's 30,000-GPU order from Nscale for a 230-megawatt site in Norway, highlight the cash-flow confidence underpinning the AI data center GPU market.

Persistent Supply-Demand Imbalance for Advanced Packaging

High-bandwidth memory (HBM) stacks and CoWoS interposers remain in chronic shortage. HBM die areas are roughly 2.5 times those of conventional DRAM, and TSV complexity raises defect rates, forcing suppliers to reserve wafer area for yield loss. Micron's 2026 HBM output is already presold, Samsung is tripling HBM revenue yet still hiking prices by high-teens percentages, and TSMC's 9.5-reticle-limit expansion will not meaningfully lift CoWoS capacity until 2027. Scarcity slows Rubin and MI400 volume ramps and may compel vendors to allocate early lots to the highest-margin buyers, delaying access for smaller cloud and enterprise users.

Other drivers and restraints analyzed in the detailed report include:

- Data-Center-Scale GPU Clusters Crossing the 100 K-GPU Threshold

- Rise of Sovereign AI Initiatives in Smaller Economies

- Growing Preference for Custom AI Accelerators Over GPUs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud facilities accounted for 66.38% revenue in 2025, anchored by multi-gigawatt campuses that integrate liquid-cooled rack pods housing more than 100,000 GPUs each. Enterprises rely on this centralized capacity to amortize compute across thousands of tenants, but rising outbound data fees and privacy mandates are nudging some workloads back on-prem or toward sovereign centers. Edge data centers, though still niche, are forecast to expand at a 15.57% CAGR through 2031 as autonomous vehicles, robotic cells, and real-time industrial inspection demand sub-10-millisecond round-trip latency.

Vendors are increasingly re-architecting software to facilitate seamless model migration across different environments. For instance, NVIDIA's BlueField-4 Data Processing Unit (DPU) layer plays a pivotal role by tunneling key-value caches from the core to the edge. This approach significantly reduces redundant GPU memory allocations, thereby optimizing resource utilization. Collectively, these advancements are driving the AI data center GPU market along a dual-track scaling trajectory. On one hand, hyperscale hubs are witnessing substantial growth, while on the other, federated micro-sites are also expanding, albeit starting from vastly different foundational levels. These developments highlight the diverse strategies being adopted to meet the evolving demands of AI workloads.

Inference accelerators accounted for 54.23% of 2025 revenue and will grow faster than training GPUs, with a 15.37% CAGR, thanks to steady, token-based monetization models. Fine-tuning, retrieval-augmented generation, and real-time personalization drive continuous inference cycles that now represent roughly two-thirds of 2026 compute spend. Training GPUs remain indispensable for frontier model creation, but their share erodes as marginal parameter increases yield diminishing performance gains.

Hardware vendors are responding with mixed-precision pipelines, NVIDIA Rubin packs a third-generation Transformer Engine, and AMD MI325X doubles HBM capacity to squeeze trillion-parameter interpreters onto a single board, both innovations that tilt economics further toward inference. As a result, hyperscalers increasingly bifurcate their fleets, reserving the newest interconnect-rich GPUs for large-batch training while backfilling inference clusters with memory-dense cards optimized for cost per token.

Geography Analysis

North America retained 37.50% of 2025 revenue, buoyed by the proximity of top cloud providers' headquarters and abundant power capacity in Texas, the Midwest, and the Pacific Northwest. U.S. policy continues to favor domestic allocation: January 2026 export-control revisions imposed a 25% tariff on certain high-end GPUs shipped abroad, effectively preserving local supply. Mega-leases such as Applied Digital's 300-megawatt deal at Delta Forge 1 underscore the long-term runway for U.S.-based construction. Europe follows with concentrated but strategic growth; Microsoft's 30,000-Rubin-GPU contract in Narvik, Norway, reveals appetite for cold-climate, renewable-powered campuses that mitigate rising carbon taxes. The United Kingdom is channeling GBP 500 million (USD 630 million) into its Sovereign AI Unit, pledging one-million-GPU-hour grants per startup and direct equity stakes in infrastructure orchestration firms.

Asia-Pacific is projected to log the fastest regional expansion at a 15.97% CAGR through 2031. Japan's USD 12 billion GMI Cloud sovereign site in Kagoshima aims for 1 gigawatt of capacity, positioning the country as a domestic manufacturing hub for robotics, autonomous vehicles, and heavy-industry AI workloads. China, facing tightened U.S. export rules and customs hurdles on imports of NVIDIA H200 chips, is pivoting toward homegrown accelerators from Huawei, Cambricon, and Biren, even though yield and software maturity gaps suggest short-term performance lags. Elsewhere, India accelerates approvals for multi-megawatt campuses, while Samsung and SK Hynix in South Korea ramp HBM4 lines to capture value upstream in the GPU supply chain.

South America, the Middle East, and Africa hold smaller shares but serve as fast-follower destinations for low-cost renewable energy. Policy shifts in May 2025 opened Saudi Arabia and the UAE to advanced GPU imports under a Validated End User framework, leveraging their vast natural gas and solar assets to deliver competitive power purchase agreements. Although these regions will not challenge the scale of North America or Asia-Pacific in absolute dollars, they offer incremental upside and geographic risk diversification for vendors marketing into the AI data center GPU market.

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Google LLC

- Amazon Web Services, Inc.

- Microsoft Corporation

- Alibaba Group Holding Limited

- Baidu, Inc.

- Huawei Technologies Co., Ltd.

- Graphcore Ltd.

- SambaNova Systems, Inc.

- Cerebras Systems Inc.

- Tenstorrent Inc.

- Qualcomm Technologies, Inc.

- IBM Corporation

- Giga Computing Technology Co., Ltd.

- Super Micro Computer, Inc.

- ASUStek Computer Inc.

- Dell Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive Growth in Generative AI Model Size

- 4.2.2 Rapid Adoption of GPU-Accelerated Cloud Services

- 4.2.3 Data-Center-Scale GPU Clusters Crossing the 100K-GPU Threshold

- 4.2.4 Standardization of MLPerf Benchmarks in Procurement

- 4.2.5 Rise of Sovereign AI Initiatives in Smaller Economies

- 4.2.6 Liquid-Cooling Retrofits Driving Refresh Sales

- 4.3 Market Restraints

- 4.3.1 Persistent Supply-Demand Imbalance for Advanced Packaging

- 4.3.2 Escalating Total Cost of Ownership for Air-Cooled Racks

- 4.3.3 Export Control Restrictions on High-End GPUs

- 4.3.4 Growing Preference for Custom AI Accelerators Over GPUs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise and Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By End-User

- 5.4.1 Hyperscalers and Cloud Service Providers

- 5.4.2 Enterprises

- 5.4.3 Government and Research Institutions

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Google LLC

- 6.4.5 Amazon Web Services, Inc.

- 6.4.6 Microsoft Corporation

- 6.4.7 Alibaba Group Holding Limited

- 6.4.8 Baidu, Inc.

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 Graphcore Ltd.

- 6.4.11 SambaNova Systems, Inc.

- 6.4.12 Cerebras Systems Inc.

- 6.4.13 Tenstorrent Inc.

- 6.4.14 Qualcomm Technologies, Inc.

- 6.4.15 IBM Corporation

- 6.4.16 Giga Computing Technology Co., Ltd.

- 6.4.17 Super Micro Computer, Inc.

- 6.4.18 ASUStek Computer Inc.

- 6.4.19 Dell Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)英國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)英國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 資料中心圖形處理器 (GPU) 市場預測至 2034 年:按部署模式、功能、最終用戶和地區分類的全球分析

資料中心圖形處理器 (GPU) 市場預測至 2034 年:按部署模式、功能、最終用戶和地區分類的全球分析 資料中心GPU市場:2026年至2032年全球市場預測,依產品、記憶體容量、伺服器密度、功耗範圍、應用、部署模式及最終用戶分類

資料中心GPU市場:2026年至2032年全球市場預測,依產品、記憶體容量、伺服器密度、功耗範圍、應用、部署模式及最終用戶分類