|

市場調查報告書

商品編碼

2063362

中東食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Middle East Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

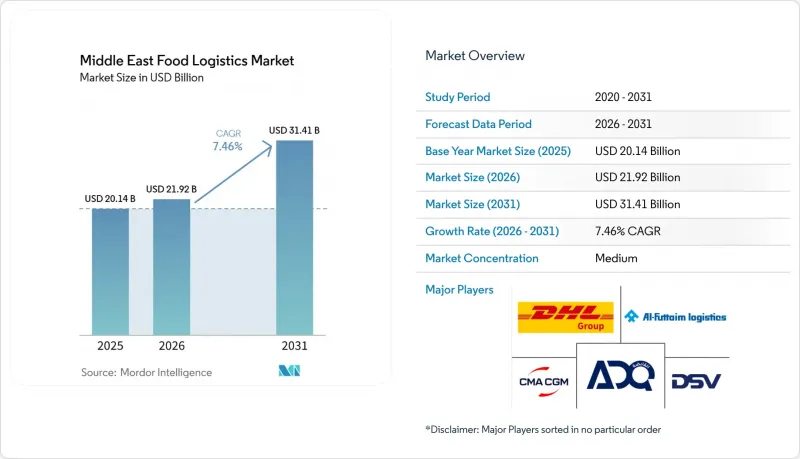

根據 Mordor Intelligence 預測,中東食品物流市場規模將從 2025 年的 201.4 億美元和 2026 年的 219.2 億美元成長到 2031 年的 314.1 億美元,2026 年至 2031 年的複合年成長率為 7.46%。

隨著政府主導的糧食安全法規不斷加強,戰略儲備計畫正轉向建設以倉庫為主要資產的模式,同時海灣合作理事會(GCC)各國海關業務的數位轉型正在消除曾經阻礙生鮮食品貿易的傳統邊境摩擦。本報告按服務類型(運輸、倉儲和儲存、附加價值服務)、溫度控制(低溫運輸、非低溫運輸)、最終產品類別(肉類、魚貝類和家禽、乳製品及其他)以及國家/地區(沙烏地阿拉伯、阿拉伯聯合大公國、卡達、科威特、阿曼、巴林、埃及及其他中東國家)進行細分。市場預測以美元計價。

中東食品物流市場趨勢與洞察

戰略性糧食安全儲備計畫擴大了區域倉庫容量。

世界各國政府正將糧食安全的言論轉化為興建多溫區倉庫的具體計畫。例如,沙烏地阿拉伯要求儲備相當於12個月消費量的糧食,而阿拉伯聯合大公國的目標是實現85%的糧食自給率。長期合約能夠為企業提供穩定且類似退休金的收入,但實施先進的存貨周轉系統對於防止庫存積壓至關重要。倉儲設施擴大採用即時物聯網監控技術,以可視化庫存貨物的保鮮度並減少廢棄物。這些項目正在加速中東食品物流市場的專業化進程,將無法滿足政府審計標準的小規模企業拒於門外。從長遠來看,公共部門的剩餘產能預計將流入商業租賃市場,進一步加劇價格競爭。

海灣合作理事會的海關數位化和統一關稅表將加速生鮮食品的跨境貿易。

海灣合作理事會(GCC)的《通用海關法》和基於區塊鏈的海關平台已將邊境等待時間從數天縮短至數小時,顯著降低了貨物變質風險和每公斤運輸成本。統一的電子植物檢疫證明和清真證書規範了文件流程,使第三方物流(3PL)營運商能夠在跨跨國樞紐共享庫存的同時,保證交貨時間。物流速度的提升使中東食品物流市場成為一條無縫銜接的大型通道,可與歐洲和北美成熟的貿易路線相媲美。該系統進一步促進了多模態解決方案的發展,從傑貝阿里到利雅德和Muscat的卡車運輸如今在速度和成本方面都與沿海運輸直接競爭。然而,營運商仍需承擔將現有運輸管理系統(TMS)平台與新的政府應用程式介面(API)整合的初始成本。

都市區冷藏倉庫的發展受到地價高昂和資本密集度高的限制。

傑貝阿里和哈立德國王機場附近的工業用地價格比周邊其他地段高出30%至50%,導致投資回收期超過七年,對中小企業構成了一大障礙。此外,節能型自然冷凍系統推高了初期成本,而成本節約只有在長期才能顯現,這進一步降低了企業透過貸款資金籌措的意願。開發商試圖引入多層倉庫和自動化托盤穿梭車,但結構維修導致設計複雜化和保險費用增加。因此,在齋戒月和朝覲高峰期會出現供不應求,導致現貨運費飆升,並對整個中東食品物流市場產生連鎖反應。隨著資金雄厚的機構投資者以低價收購不良資產,產業整合正在推進。

細分市場分析

到2025年,運輸業將佔中東食品物流市場佔有率的54.84%,這主要基於連接進口樞紐和消費區的陸路和沿海運輸路線。然而,附加價值服務正以10.03%的複合年成長率呈現顯著成長,反映出托運人正從簡單的運輸轉向整合快速冷凍、貼標和報關單準備等服務的包裝服務。隨著日常消費品(FMCG)客戶追求更豐富的產品種類和多元化的銷售管道,能夠將生產計劃與電商限時搶購同步,並將訂單交付週期縮短至24小時以內的第三方物流(3PL)供應商的重要性日益凸顯。

隨著燃油效率的提高和遠端資訊處理技術在路線最佳化方面的進步,商品化幹線運輸的利潤率持續下降,迫使現有業者轉向輔助收入來源。將先進的倉庫管理系統 (WMS) 與預測分析相結合的供應商,如今正透過保存期限管理和退貨處理來創造收入。因此,在增值功能的驅動下,中東食品物流市場規模預計到 2031 年將比 2025 年加倍,這將進一步增強技術型營運商的競爭優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 透過政府主導的糧食安全儲備計劃,擴大區域倉儲能力。

- 海灣合作理事會成員國海關的數位化和統一關稅制度正在加速生鮮食品的跨國流通。

- 清真旅遊和酒店項目的激增對高品質的食品服務物流提出了更高的要求。

- 由外國直接投資 (FDI) 資助的大型農業叢集,如沙漠地區的酪農和溫室農場,需要端到端的低溫運輸。

- 引進太陽能冷藏庫:將農村生產者融入現代供應鏈

- 一項智慧城市試點項目,旨在引入自主溫控配送車輛,用於最後一公里配送。

- 市場限制因素

- 都市區冷藏倉庫的發展受到地價飆漲和資本密集度高的限制。

- 各國不同的食品安全法規導致多個國家的合規成本上升。

- 隨著高全球暖化潛勢冷媒即將被淘汰,冷藏貨櫃船的二氧化碳級轉換套件的供應變得越來越緊張。

- 針對物聯網連接倉庫的網路攻擊日益增多,正在擾亂溫度監控系統。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按服務

- 運輸

- 路

- 鐵路

- 海運和內河航運

- 航空

- 倉庫/存儲

- 附加價值服務(快速冷凍、貼標籤、庫存管理等)

- 運輸

- 溫度控制方法

- 低溫運輸

- 室溫(15-25 度C)

- 冷藏(2-8 度C)

- 冷凍(低於0°C)

- 非低溫運輸

- 低溫運輸

- 按最終產品類別

- 肉類、魚貝類、家禽

- 乳製品和冷凍甜點(牛奶、冰淇淋、奶油等)

- 園藝(新鮮水果和蔬菜)

- 加工食品

- 寵物食品

- 其他產品(抹醬、調味品、沙拉醬、特色食品及機能性食品等)

- 國家

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 阿曼

- 巴林

- 埃及

- 其他中東國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Al-Futtaim Logistics

- GAC Group

- DHL Group

- DSV

- NAQEL Express

- Wared Logistics

- RSA Global

- Total Freight International

- Al Talib Shipping Co. LLC

- System8Group

- CUBES International Logistics

- TLM International Freight Services LLC

- EPx Logistics

- ILS Egypt

- PIL Logistics

- Clarion Shipping Services LLC

- Four Winds

- Noatum Logistics

- CMA CGM

- ADQ

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east food logistics market size is projected to expand from USD 20.14 billion in 2025 and USD 21.92 billion in 2026 to USD 31.41 billion by 2031, registering a CAGR of 7.46% between 2026 to 2031.

Intensifying sovereign-backed food-security mandates are converting strategic stockpiling ambitions into hard-asset warehouse construction, while GCC-wide customs digitalization dismantles legacy border friction that once slowed perishable trade. This report is Segmented by Service Type (Transportation, Warehousing and Storage, Value-Added Services), by Temperature-Control (Cold Chain, Non Cold Chain), by End-Product Category (Meat/Seafood/Poultry, Dairy Products, and More), and by Country (Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain, Egypt, Rest of Middle East). The Market Forecasts are Provided in Terms of Value (USD).

Middle East Food Logistics Market Trends and Insights

Strategic Food-Security Stockpiling Programs Expanding Regional Warehouse Capacity

Governments are translating food-security rhetoric into multi-temperature storage construction, illustrated by Saudi Arabia's grain reserve requirements that hold 12-months consumption equivalent and the UAE's 85% self-sufficiency ambition. Long-term offtake agreements guarantee annuity-style revenues for operators but oblige sophisticated inventory-rotation systems to limit obsolescence. Stockpiling facilities increasingly integrate real-time IoT monitoring, ensuring visibility into reserve freshness and reducing waste. The programs accelerate professionalization of the Middle East food logistics market, crowding out smaller entrants unable to meet government audit thresholds. Over the long term, excess public-sector capacity is expected to bleed into commercial leasing, further tightening competitive pricing.

GCC Customs Digitalization and Unified Tariff Schedules Accelerating Cross-Border Perishable Flows

The GCC Common Customs Law and blockchain-enabled clearance platforms now shrink border dwell time from days to hours, materially lowering spoilage risk and freight cost per kilogram. Unified electronic phytosanitary and halal certificates standardize paperwork, empowering 3PLs to guarantee delivery windows while pooling inventory across multi-country hubs. Enhanced velocity positions the Middle East food logistics market as a seamless mega-corridor that rivals mature trade lanes in Europe and North America. The system further stimulates multimodal solutions, trucking from Jebel Ali to Riyadh or Muscat, now competes directly with short-sea transits on both speed and cost. However, operators face upfront integration costs to interface legacy TMS platforms with new government APIs.

Urban Cold-Storage Development Hampered by High Land Prices and Capital Intensity

Industrial plots near Jebel Ali or King Khalid Airport are priced 30-50% above ambient alternatives, translating into payback periods that exceed seven years, a hurdle for smaller firms. Debt-funding appetite tightens further because energy-efficient natural-refrigerant systems raise up-front costs while delivering savings only over time. Developers are experimenting with multilevel warehouses and automated pallet shuttles, but structural retrofits increase engineering complexity and insurance premiums. Consequently, capacity shortfalls manifest during Ramadan and Hajj peaks, forcing spot-rate spikes that ripple across the Middle East food logistics market. Consolidation ensues as well-capitalized institutional investors purchase distressed assets at discounts.

Other drivers and restraints analyzed in the detailed report include:

- Halal Tourism and Hospitality Projects Demanding Premium Food-Service Logistics

- FDI-Backed Mega-Agri Clusters Requiring End-to-End Cold Chains

- Fragmented National Food-Safety Regulations Raising Multi-Country Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 54.84% of the Middle East food logistics market share in 2025, anchored by road and short-sea corridors connecting import hubs with consumption centers. However, value-added services are on track for a blistering 10.03% CAGR, reflecting shippers' pivot from pure haulage to bundled offerings that integrate blast-freezing, labeling, and customs documentation. As FMCG customers pursue SKU proliferation and channel diversification, they prize 3PLs capable of synchronizing production runs with e-commerce flash-sales, compressing order-to-delivery cycles to under 24 hours.

Margins in commoditized line-haul continue to tighten amid fuel-efficiency gains and telematics-driven route optimization, pushing incumbents toward ancillary revenue streams. Providers that meld advanced WMS with predictive analytics now monetize shelf-life management and returns processing. Consequently, the Middle East food logistics market size attributable to value-added functions is forecast to double its 2025 base by 2031, fortifying competitive moats for tech-savvy operators.

List of Companies Covered in this Report:

- Al-Futtaim Logistics

- GAC Group

- DHL Group

- DSV

- NAQEL Express

- Wared Logistics

- RSA Global

- Total Freight International

- Al Talib Shipping Co. LLC

- System8Group

- CUBES International Logistics

- TLM International Freight Services LLC

- EPx Logistics

- ILS Egypt

- PIL Logistics

- Clarion Shipping Services L.L.C

- Four Winds

- Noatum Logistics

- CMA CGM

- ADQ

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-Led Food-Security Stockpiling Programs Expanding Regional Warehouse Capacity

- 4.2.2 GCC-Wide Customs Digitalization and Unified Tariff Schedules Accelerating Cross-Border Perishables Flows

- 4.2.3 Surge in Halal Tourism and Hospitality Projects Demanding Premium Food-Service Logistics

- 4.2.4 FDI-Backed Mega-Agri Clusters (E.G., Desert Dairies & Greenhouse Farms) Requiring End-To-End Cold Chains

- 4.2.5 Roll-Out of Solar-Powered Micro-Cold Rooms Integrating Rural Producers into Modern Supply Chains

- 4.2.6 Smart-City Pilots Deploying Autonomous Temperature-Controlled Delivery Vehicles for Last-Mile Fulfilment

- 4.3 Market Restraints

- 4.3.1 Urban Cold-Storage Development Hampered by High Land Prices and Capital Intensity

- 4.3.2 Fragmented National Food-Safety Regulations Raising Multi-Country Compliance Costs

- 4.3.3 Impending Phase-Out of High-GWP Refrigerants Crimping Availability of CO2-Grade Retrofits for Reefers

- 4.3.4 Rising Cyber-Attacks on IoT-Linked Warehouses Disrupting Temperature Monitoring Systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea and Inland Water

- 5.1.1.4 Air

- 5.1.2 Warehousing and Storage

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-Product Category

- 5.3.1 Meat, Seafood, and Poultry

- 5.3.2 Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Horticulture (Fresh Fruits and Vegetables)

- 5.3.4 Processed Food Products

- 5.3.5 Pet Food

- 5.3.6 Others (Spreads, Seasoning, dressing, Specialty and Functional Foods, etc.)

- 5.4 By Country

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Kuwait

- 5.4.5 Oman

- 5.4.6 Bahrain

- 5.4.7 Egypt

- 5.4.8 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Al-Futtaim Logistics

- 6.4.2 GAC Group

- 6.4.3 DHL Group

- 6.4.4 DSV

- 6.4.5 NAQEL Express

- 6.4.6 Wared Logistics

- 6.4.7 RSA Global

- 6.4.8 Total Freight International

- 6.4.9 Al Talib Shipping Co. LLC

- 6.4.10 System8Group

- 6.4.11 CUBES International Logistics

- 6.4.12 TLM International Freight Services LLC

- 6.4.13 EPx Logistics

- 6.4.14 ILS Egypt

- 6.4.15 PIL Logistics

- 6.4.16 Clarion Shipping Services L.L.C

- 6.4.17 Four Winds

- 6.4.18 Noatum Logistics

- 6.4.19 CMA CGM

- 6.4.20 ADQ

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

食品低溫運輸市場報告:趨勢、預測與競爭分析(至2035年)

食品低溫運輸市場報告:趨勢、預測與競爭分析(至2035年) 食品物流市場:2026-2032年全球市場預測(依溫度分類、運輸方式、服務類型、食品類型及最終用戶分類)

食品物流市場:2026-2032年全球市場預測(依溫度分類、運輸方式、服務類型、食品類型及最終用戶分類) 食品低溫運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

食品低溫運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 食品物流市場機會、成長要素、產業趨勢分析及2026-2035年預測。英國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

食品物流市場機會、成長要素、產業趨勢分析及2026-2035年預測。英國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)