|

市場調查報告書

商品編碼

2063358

日本食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Japan Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

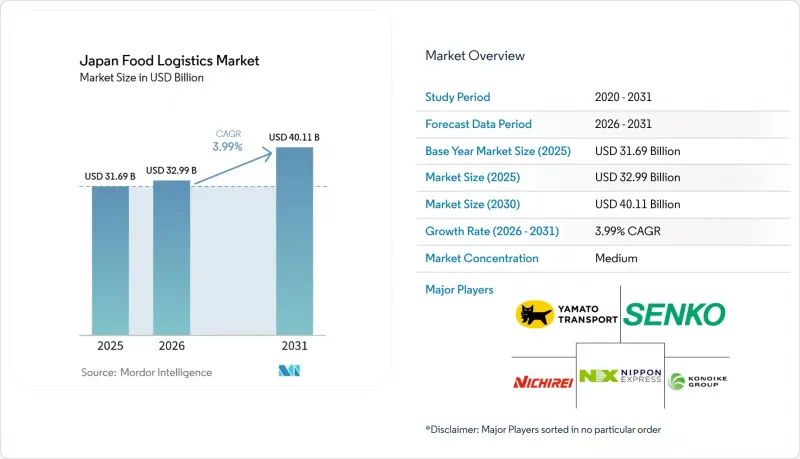

根據 Mordor Intelligence 預測,日本食品物流市場規模預計將在 2025 年達到 316.9 億美元,2026 年達到 329.9 億美元,到 2031 年達到 401.1 億美元,2026 年至 2031 年的複合年成長率為 3.99%。

這種看似溫和的成長率背後,隱藏著顯著的結構性變化。本報告按服務(運輸(公路、鐵路、海運和內河航運、航空)、倉儲和儲存、附加價值服務)、溫控類型(低溫運輸(常溫、冷藏、冷凍)、非低溫運輸)和最終產品類別(肉類、魚貝類和家禽、乳製品、園藝作物、加工食品、寵物食品及其他)進行細分。市場預測以美元計價。

日本食品物流市場的趨勢與洞察

藥品低溫運輸。

這種混合運輸網路將冷藏車從早晨的藥品配送轉向下午的生鮮食品配送,並透過統一兩種貨物的溫度要求(2-8°C),使食品運輸量佔藥品運輸車輛運力的15-22%。更嚴格的溫度控制減少了廢棄物,延長了保存期限,並為挪威鮭魚和澳洲冷藏牛肉等進口產品提供了更高的定價空間。由於營運商無需大量資本投入即可獲得新的收入來源,混合運輸服務將持續擴張,直到完全由食品專用車輛組成的運輸車隊失去成本競爭力。

企業範圍 3 的排放審核鼓勵供應商整合。

雀巢日本、聯合利華和其他公司已將貨運合作夥伴數量從15-20家減少到僅5家戰略合作夥伴,從而實現了每噸公里碳排放強度降低12-18%。提供即時二氧化碳排放儀錶板、電動卡車和液化天然氣牽引車的貨運公司正在簽訂多年協議,以確保基準貨運量並共同投資脫碳試點計畫。這一趨勢為缺乏測量能力的小規模本地貨運公司設定了准入門檻,並隨著大型第三方物流公司收購更密集的路線網路,加速了產業整合。

涵蓋溫度偏差的保險費正在飆升。

預計2024年至2025年間,低溫運輸貨物的保險費將飆升35%至50%,保險公司強烈要求持續的物聯網監控以及提交書面緊急時應對計畫。目前,平均保險索賠金額高達18萬美元,迫使小規模承運商在承擔利潤空間被壓縮的高額保費和承擔無保險營運的風險之間做出選擇。大型第三方物流公司正透過實施預測性維護和引入雙壓縮機拖車來應對這項挑戰,以滿足保險公司的要求並獲得更低的保費。

細分市場分析

預計到2025年,運輸業將維持在日本食品物流市場45.72%的佔有率。這得歸功於日本四通八達的公路網路,該網路保障了數千家便利商店的日常補貨。然而,附加價值服務顯然才是推動市場成長的主要動力,其複合年成長率(CAGR)高達6.55%。製造商將生產後的環節轉移到消費環節,並將快速冷凍、貼標和包裝等工序外包給物流專家。與倉儲相關的日本食品物流市場規模也不斷擴大。這主要歸功於集存儲和加工於一體的自動化多溫區物流中心,這些中心能夠實現大都會圈電商食品的次日達配送。

北海道與本州之間鐵路貨運走廊的復興,使冷凍散裝的單位成本比公路運輸降低了15%至25%。同時,海運覆蓋了島際航線和大宗進口貨物。空運仍然是高階生鮮食品(例如海膽和太平洋藍鰭鮪魚)的主要運輸管道,因為這些產品的保存期限經濟效益足以支撐包機運費。透過結合這些多模態方案,托運人可以在不影響低溫運輸完整性的前提下,靈活調整運輸速度、成本和碳排放目標。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 醫藥低溫運輸在其他領域的應用迅速增加。

- 企業範圍 3 的排放審核鼓勵供應商整合。

- 人口老化推動了頻繁的小批量冷藏配送需求的成長。

- 國家糧食安全儲備冷凍庫計劃

- 港口數位化顯著縮短了冷藏貨櫃的停留時間。

- 都市區對自動化垂直冷藏倉庫的稅收優惠

- 市場限制因素

- 因溫度波動而導致的保險費上漲。

- 高功率冷凍設備併網的限制

- 因夜間送貨噪音法規而受到的限制

- 無氫氟碳化物冷卻系統認證審核延誤

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按服務

- 運輸

- 路

- 鐵路

- 海運和內河航運

- 航空

- 倉庫/存儲

- 附加價值服務(快速冷凍、貼標籤、庫存管理等)

- 運輸

- 溫度控制方法

- 低溫運輸

- 室溫(15-25 度C)

- 冷藏(2-8 度C)

- 冷凍(低於0°C)

- 非低溫運輸

- 低溫運輸

- 按最終產品類別

- 肉類、魚貝類、家禽

- 乳製品和冷凍甜點(牛奶、冰淇淋、奶油等)

- 園藝(新鮮水果和蔬菜)

- 加工食品

- 寵物食品

- 其他(抹醬、調味料、沙拉醬、特色食品、機能性食品等)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Yamato Transport Co., Ltd.

- Nippon Express Holdings Inc.

- Nichirei Logistics Group Inc.

- Konoike Transport Co., Ltd.

- Senko Co., Ltd.

- Mitsubishi Logistics Corporation

- NYK Line(Including Yusen Logistics Co., Ltd.)

- Itochu Logistics Corp.

- Suzuyo Logistics Japan

- Sankyu Inc.

- Kintetsu World Express

- DHL Group

- CMA CGM Group(Including CEVA Logistics)

- JWD InfoLogistics

- SEKO Logistics

- SF Express(Kex-SF)

- GEODIS

- C&F Logistics Holdings Co., Ltd.

- Sagawa Express Co., Ltd.

- Toll Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan food logistics market size is projected to be USD 31.69 billion in 2025, USD 32.99 billion in 2026, and reach USD 40.11 billion by 2031, growing at a CAGR of 3.99% from 2026 to 2031.

A measured headline growth rate conceals big structural change. This report is Segmented by Services (Transportation (Road, Rail, Sea and Inland Water, Air), Warehousing and Storage, Value-Added Services), by Temperature-Control Type (Cold Chain (Ambient, Chilled, Frozen), Non-Cold Chain), by End-Product Category (Meat/Seafood/Poultry, Dairy Products, Horticulture, Processed Foods, Pet Food, Others). The Market Forecasts are Provided in Terms of Value (USD).

Japan Food Logistics Market Trends and Insights

Surge in Pharmaceutical Cold-Chain Cross-Utilization

Hybrid networks now shift refrigerated trucks from morning drug deliveries to afternoon fresh-food runs, aligning 2-8 °C requirements across both cargo types and lifting food volumes to 15-22% of pharmaceutical fleet capacity. Higher specification control trims waste, extends shelf life, and supports premium pricing for imports such as Norwegian salmon and Australian chilled beef. Operators capture new revenue without major capital outlay, so hybrid services should keep widening until dedicated food-only fleets lose cost competitiveness.

Corporate Scope-3 Emission Audits Prompting Supplier Consolidation

Nestle Japan, Unilever, and peer producers have cut carrier counts from 15-20 to as few as five strategic partners, achieving 12-18% carbon-intensity improvement per ton-kilometer. Carriers offering real-time CO2 dashboards, electric trucks, and LNG tractors win multi-year contracts that guarantee baseline volumes and co-fund decarbonization pilots. The trend erects entry barriers for small regional haulers lacking measurement capacity and accelerates roll-up activity as larger 3PLs buy route density.

Escalating Insurance Premiums Covering Temperature Excursions

Premiums for cold-chain cargo jumped 35-50% between 2024 and 2025, with underwriters insisting on continuous IoT monitoring and documented contingency plans. Claims now average USD 180,000 per incident, prompting small fleets either to absorb margin-sapping policy costs or risk operating uninsured. Large 3PLs respond with predictive maintenance and dual-compressor trailers that satisfy insurer checklists and wave through at lower rates.

Other drivers and restraints analyzed in the detailed report include:

- Ageing Population Driving High-Frequency Small-Lot Chilled Runs

- National Food-Security Stock Freezer Initiatives

- Constrained Grid Connections for High-Power Refrigeration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation retained 45.72% of the Japan food logistics market share in 2025, anchored by the country's intricate road network that supports the daily replenishment of thousands of convenience stores. Yet value-added services are the clear pace-setter, growing at 6.55% CAGR as manufacturers push postponement to the edge of consumption and outsource blast freezing, labeling, and kitting to logistics specialists. The Japan food logistics market size tied to warehousing also rises as automated multi-temperature DCs blend storage with light processing, enabling next-day ecommerce grocery fulfillment in megacities.

Rail freight's renaissance on the Hokkaido-Honshu corridor now shaves 15-25% off unit cost versus trucking for bulk frozen cargo, while sea transport covers inter-island lanes and bulk imports. Air remains a boutique channel for premium perishables such as uni and Pacific bluefin tuna, where shelf-life economics justify charter rates. Together, multimodal options give shippers flexibility to match speed, cost, and carbon objectives without compromising cold-chain integrity.

List of Companies Covered in this Report:

- Yamato Transport Co., Ltd.

- Nippon Express Holdings Inc.

- Nichirei Logistics Group Inc.

- Konoike Transport Co., Ltd.

- Senko Co., Ltd.

- Mitsubishi Logistics Corporation

- NYK Line (Including Yusen Logistics Co., Ltd.)

- Itochu Logistics Corp.

- Suzuyo Logistics Japan

- Sankyu Inc.

- Kintetsu World Express

- DHL Group

- CMA CGM Group (Including CEVA Logistics)

- JWD InfoLogistics

- SEKO Logistics

- SF Express (Kex-SF)

- GEODIS

- C&F Logistics Holdings Co., Ltd.

- Sagawa Express Co., Ltd.

- Toll Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Pharmaceutical Cold-Chain Cross-Utilization

- 4.2.2 Corporate Scope-3 Emission Audits Prompting Supplier Consolidation

- 4.2.3 Ageing Population Driving High-Frequency Small-Lot Chilled Runs

- 4.2.4 National Food-Security Stock Freezer Initiatives

- 4.2.5 Port Digitalization Slashing Reefer Dwell Times

- 4.2.6 Urban Tax Breaks for Automated Vertical Cold-Storage Sites

- 4.3 Market Restraints

- 4.3.1 Escalating Insurance Premiums Covering Temperature Excursions

- 4.3.2 Constrained Grid Connections for High-Power Refrigeration

- 4.3.3 Night-Time Delivery Noise Ordinance Constraints

- 4.3.4 Delayed Certification Pipeline for HFC-Free Cooling Systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea and Inland Water

- 5.1.1.4 Air

- 5.1.2 Warehousing and Storage

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-Product Category

- 5.3.1 Meat, Seafood, and Poultry

- 5.3.2 Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Horticulture (Fresh Fruits and Vegetables)

- 5.3.4 Processed Food Products

- 5.3.5 Pet Food

- 5.3.6 Others (Spreads, Seasoning, Dressing, Specialty and Functional Foods, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, Recent Developments)

- 6.4.1 Yamato Transport Co., Ltd.

- 6.4.2 Nippon Express Holdings Inc.

- 6.4.3 Nichirei Logistics Group Inc.

- 6.4.4 Konoike Transport Co., Ltd.

- 6.4.5 Senko Co., Ltd.

- 6.4.6 Mitsubishi Logistics Corporation

- 6.4.7 NYK Line (Including Yusen Logistics Co., Ltd.)

- 6.4.8 Itochu Logistics Corp.

- 6.4.9 Suzuyo Logistics Japan

- 6.4.10 Sankyu Inc.

- 6.4.11 Kintetsu World Express

- 6.4.12 DHL Group

- 6.4.13 CMA CGM Group (Including CEVA Logistics)

- 6.4.14 JWD InfoLogistics

- 6.4.15 SEKO Logistics

- 6.4.16 SF Express (Kex-SF)

- 6.4.17 GEODIS

- 6.4.18 C&F Logistics Holdings Co., Ltd.

- 6.4.19 Sagawa Express Co., Ltd.

- 6.4.20 Toll Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

食品低溫運輸市場報告:趨勢、預測與競爭分析(至2035年)

食品低溫運輸市場報告:趨勢、預測與競爭分析(至2035年) 食品物流市場:2026-2032年全球市場預測(依溫度分類、運輸方式、服務類型、食品類型及最終用戶分類)

食品物流市場:2026-2032年全球市場預測(依溫度分類、運輸方式、服務類型、食品類型及最終用戶分類) 食品低溫運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

食品低溫運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 食品物流市場機會、成長要素、產業趨勢分析及2026-2035年預測。中東食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)英國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

食品物流市場機會、成長要素、產業趨勢分析及2026-2035年預測。中東食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)英國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)