|

市場調查報告書

商品編碼

2063359

英國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United Kingdom Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

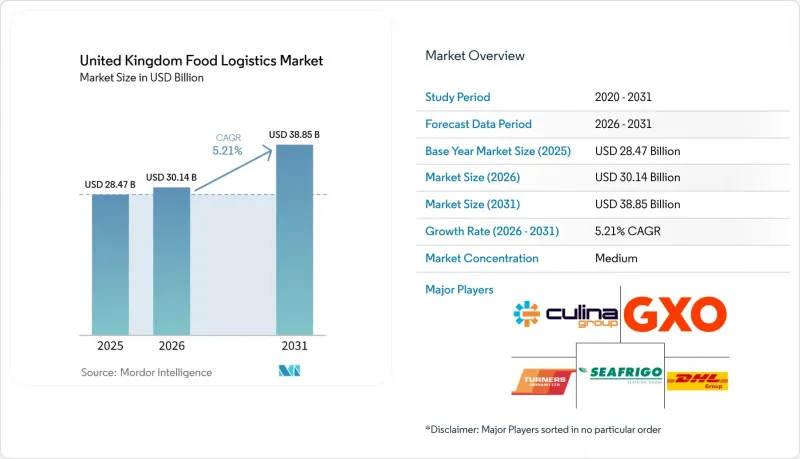

據 Mordor Intelligence 稱,2025 年英國食品物流市場價值為 284.7 億美元,預計到 2031 年將達到 388.5 億美元,而 2026 年為 301.4 億美元,預測期(2026-2031 年)的複合年成長率為 5.21%。

費利克斯托-米德蘭走廊的綜合冷藏運輸、強制性的廢棄物數位化追蹤以及政府「升級計畫」(Level Up)資助的區域處理中心是推動這一成長的基礎。本報告按服務(運輸、倉儲和儲存、附加價值服務)、溫度控制類型(低溫運輸(常溫、冷藏、冷凍)、非低溫運輸)和最終產品類別(肉類、水產品和家禽、乳製品和冷凍甜點、園藝作物、加工食品、寵物食品及其他)進行細分。市場預測以美元(USD)為單位。

英國食品物流市場趨勢與洞察

出口型冷藏食品需求的激增,擴大了多式聯運的需求。

預計到2025年,乳製品出口將創歷史新高,銷往亞太市場的中溫肉品和即食產品的出貨量也呈現兩位數成長,進一步推動了對溫控貨櫃和鐵路深水港運輸的需求。由於中溫產品對溫度的要求更為嚴格(2-8°C),且運輸時間比冷凍貨物更短,因此托運人擴大選擇公路和鐵路一體化解決方案,以將全程運輸時間縮短多達12小時。 GB Railfreight在費利克斯托和米德蘭之間這條關鍵線路上提供的專用冷藏集裝箱運輸服務表明,一旦碳排放減少和燃料節省得到量化,鐵路運輸就能滿足長途運輸的需求。運輸方式的轉變可減少76%的相關排放,使出口商能夠展示其在永續發展方面所做的努力。然而,要使這項舉措得到廣泛應用,增加冷藏貨車的數量以及實現貨櫃追蹤系統的自動化以防止溫度偏差至關重要。

強制性的廢棄物數位化追蹤正在擴大逆向物流的趨勢。

強制性食物廢棄物報告系統將於2025年4月生效,正式確立所有大型食品零售商和餐飲服務企業的逆向物流要求。 2026年3月,強制性家庭食物廢棄物分類收集計畫將增加與前向配送路線重疊的收集路線,從而提高車輛運轉率。像Tesco這樣的零售商現在將最後一公里配送與剩餘食物回收結合,利用QR碼資料追蹤將貨物運送至再分配非政府組織。擁有混合裝載冷藏車和整合API的調度工具的企業可以將以往空載的返程轉化為創收服務,從而減少排放並獲得監管積分。隨著端到端數位化視覺性在合規審計中變得越來越重要,先行者正在享受開拓優勢。

對氟化氣體和氨氣的更嚴格監管推高了冷庫維修的成本。

到2030年,氫氟碳化合物(HFC)的配額將削減79%,屆時,英國三分之二仍在使用過時冷媒的冷藏倉庫將被迫維修或更換系統,每個設施的成本在60萬至250萬美元之間。使用氨或二氧化碳冷媒的設計方案可以顯著降低能源成本,但需要安裝洩漏檢測裝置、升級通風系統並聘請熟練的技術人員。對於融資不佳的獨立營運商而言,這些資本投資過於昂貴,因此他們傾向於與房地產投資信託基金(REITs)進行售後回租交易,例如Lineage 物流 ,這些公司提供資金籌措、建設和長期營運合約等一攬子服務。

細分市場分析

就服務類型而言,預計到2025年,運輸將佔英國食品物流市場佔有率的46.77%。雖然道路運輸仍然是最後一公里配送的關鍵,但人手不足和柴油成本上漲正在擠壓利潤空間,促使營運商轉向盈利更高的輔助服務。快速冷凍、庫存管理、聯合包裝和有組織的逆向物流等附加價值服務正以7.78%的複合年成長率成長,比英國食品物流市場的整體複合年成長率高出近2個百分點。客戶高度重視具備原生WMS和TMS整合、SKU等級視覺性以及跨多個溫區組裝訂單能力的供應商。雖然海運和內河運輸與以港口為中心的冷庫密切相關,但隨著運輸能力瓶頸的緩解,鐵路將在多式聯運走廊中逐步擴大其佔有率。

自動化是提升績效的統一動力。在NewCold位於韋克菲爾德的自動化AS/RS倉庫中,每平方公尺的托盤處理速度比人工操作快40%,每個處理單元的能耗降低,並符合近乎非接觸式的安全規程。隨著超級市場更新物流競標,整合運輸、倉儲和合規報告的綜合合約比各部門的單獨提案更具優勢。 DFDS物流正是這項轉變的體現。其交叉轉運設施的重新設計,如今融合了速凍冷凍庫、訂單組裝機器人和支援RFID技術的廢棄物收集閘門。在整個預測期內,收入成長將主要流向那些將其傳統的「運輸和倉儲」模式轉型為數據豐富、合規驅動的服務平台的承運商。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 出口冷藏食品的激增擴大了對多式聯運的需求。

- 強制性廢棄物數位化追蹤和逆向物流的擴展

- 根據「均衡發展」政策建立的區域處理中心將振興中距離冷藏運輸路線。

- 透過引入製冷設備的預測性維護來減少停機時間。

- 費利克斯托-米德蘭走廊冷藏鐵路運輸服務的擴建

- 保險公司主導溫度控制的要求正在催生一個加值服務層級。

- 市場限制因素

- 對氟氯化碳和氨的更嚴格監管推高了冷庫維修的成本。

- 冷藏鐵路貨車短缺限制了接受模式轉換的能力。

- 外匯波動導致燃料和設備的進口成本上升。

- 與海關清關相關的現金流壓力正在增加中小型食品運輸公司破產的風險。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按服務

- 運輸

- 路

- 鐵路

- 海運和內河航運

- 航空

- 倉庫/存儲

- 附加價值服務(快速冷凍、貼標籤、庫存管理等)

- 運輸

- 溫度控制方法

- 低溫運輸

- 室溫(15-25 度C)

- 冷藏(2-8 度C)

- 冷凍(低於 0 度C)

- 非低溫運輸

- 低溫運輸

- 按最終產品類別

- 肉類、魚貝類、家禽

- 乳製品和冷凍甜點(牛奶、冰淇淋、奶油等)

- 園藝(新鮮水果和蔬菜)

- 加工食品

- 寵物食品

- 其他產品(抹醬、調味品、沙拉醬、特色食品及機能性食品等)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- GXO Logistics

- Culina Group

- Seafrigo Group

- Turners(Soham)Ltd

- Kuehne+Nagel

- DFDS Logistics

- XPO Logistics

- DACHSER

- Lineage, Inc.

- NewCold

- La Poste Group(Including DPD UK)

- DSV A/S

- Hellmann Worldwide Logistics

- Constellation Cold Logistics

- Kammac

- McCulla Refrigerated Transport

- Rhenus Logistics

- Certa Logistics

- Supply Chain Solution Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom food logistics market size was valued at USD 28.47 billion in 2025 and estimated to grow from USD 30.14 billion in 2026 to reach USD 38.85 billion by 2031, at a CAGR of 5.21% during the forecast period (2026-2031).

Intermodal refrigerated transport along the Felixstowe-Midlands corridor, mandatory digital waste-tracking, and regional processing hubs funded by the government's levelling-up program anchor this growth. This report is Segmented by Services (Transportation, Warehousing and Storage, Value-Added Services), by Temperature-Control Type (Cold Chain (Ambient, Chilled, Frozen), Non-Cold Chain), by End-Product Category (Meat/Seafood/Poultry, Dairy Products/Frozen Desserts, Horticulture, Processed Food Products, Pet Food, Others). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Food Logistics Market Trends and Insights

Export-Oriented Chilled-Food Surge Amplifying Intermodal Demand

Record dairy export volumes in 2025 accompanied a double-digit rise in chilled meat and ready-to-eat products moving to Asia-Pacific markets, driving incremental demand for temperature-controlled containers and rail access to deep-water ports. Chilled items require tighter 2-8 °C windows and shorter transit times than frozen cargo, which pushes shippers toward integrated road-rail solutions that cut end-to-end journeys by up to 12 hours. GB Railfreight's dedicated reefer services on the Felixstowe-Midlands spine illustrate how rail captures long-haul volumes once carbon abatements and fuel savings are quantified. Exporters gain sustainability credentials as modal shift cuts 76% of associated emissions. However, widespread take-up relies on a larger refrigerated wagon fleet and automated container-tracking to pre-empt temperature excursions.

Mandatory Digital Waste-Tracking Expanding Reverse-Logistics Flows

Compulsory food-waste reporting from April 2025 has formalized reverse-logistics requirements for every major grocer and food-service player. Separate household food-waste collection mandated by March 2026 is adding collection routes that mirror forward distribution lanes, boosting fleet utilization. Retailers such as Tesco now pair last-mile deliveries with surplus pick-ups, routing them to redistribution NGOs aided by QR-coded data trails. Operators with mixed-load refrigerated vans and API-linked scheduling tools can turn what was once empty back-haul into a revenue-generating service, trimming emissions and securing regulatory credits. Early adopters enjoy first-mover advantage as compliance audits increasingly demand end-to-end digital visibility.

Tightening F-Gas and Ammonia Regulations Inflating Cold-Store Retrofit Costs

HFC quotas fall 79% by 2030, forcing two-thirds of the United Kingdom cold stores still running legacy refrigerants to retrofit or replace systems at USD 0.6-2.5 million per site. Ammonia and CO2 designs slash energy bills but require leak-detection, ventilation upgrades, and skilled engineers. For cash-constrained independents the capex outlay is prohibitive, incentivizing sale-and-leaseback deals with REITs such as Lineage Logistics that bundle financing, build, and long-term operating contracts.

Other drivers and restraints analyzed in the detailed report include:

- Regional Processing Hubs under Levelling-Up Agenda Boosting Mid-Mile Reefer Routes

- Predictive-Maintenance Deployment for Refrigerated Assets Cutting Downtime

- Shortage of Refrigerated Rail Wagons Constraining Modal-Shift Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In service type, transportation commanded 46.77% of the United Kingdom food logistics market share in 2025. Road remains indispensable for last-mile coverage, but labor shortages and diesel costs compress margins, steering operators toward higher-yield ancillary work. Value-added services such as blast freezing, inventory management, co-packing, and organised reverse-logistics are on track for a 7.78% CAGR, almost 2 percentage points above the overall United Kingdom food logistics market CAGR. Clients reward providers capable of native WMS-TMS integration, SKU-level visibility, and multi-temperature order assembly. Sea and inland-water moves tie closely to port-centric chill-tunnel storage, while rail's share inches forward on intermodal corridors once capacity bottlenecks ease.

Automation is the performance equalizer. NewCold's automated AS/RS facility in Wakefield lifts pallet-throughput per square meter 40% above manual designs, compressing energy per unit handled and meeting near-zero-touch safety protocols. As supermarkets renew logistics tenders, bundled contracts that fuse transport, warehousing, and compliance reporting beat siloed offerings. DFDS Logistics illustrates the pivot: cross-dock redesigns now include blast-freezers, order-assembly robots, and RFID-enabled waste-capture gates. Over the forecast horizon, earnings growth will be skewed toward fleets that convert traditional "haul and store" models into data-rich, compliance-embedded service platforms.

List of Companies Covered in this Report:

- DHL Group

- GXO Logistics

- Culina Group

- Seafrigo Group

- Turners (Soham) Ltd

- Kuehne+Nagel

- DFDS Logistics

- XPO Logistics

- DACHSER

- Lineage, Inc.

- NewCold

- La Poste Group (Including DPD UK)

- DSV A/S

- Hellmann Worldwide Logistics

- Constellation Cold Logistics

- Kammac

- McCulla Refrigerated Transport

- Rhenus Logistics

- Certa Logistics

- Supply Chain Solution Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Export-Oriented Chilled-Food Surge Amplifying Intermodal Demand

- 4.2.2 Mandatory Digital Waste-Tracking Expanding Reverse-Logistics Flows

- 4.2.3 Regional Processing Hubs Under "Levelling-Up" Agenda Boosting Mid-Mile Reefer Routes

- 4.2.4 Predictive-Maintenance Deployment for Refrigerated Assets Cutting Downtime

- 4.2.5 Expansion of Rail-Based Refrigeration Services on Felixstowe-Midlands Corridor

- 4.2.6 Insurer-Led Temperature-Compliance Requirements Creating Premium Service Tiers

- 4.3 Market Restraints

- 4.3.1 Tightening F-Gas and Ammonia Regulations Inflating Cold-Store Retrofit Costs

- 4.3.2 Shortage of Refrigerated Rail Wagons Constraining Modal Shift Capacity

- 4.3.3 Currency Volatility Elevating Fuel and Equipment Import Costs

- 4.3.4 Rising Insolvency Risk Among SME Food Hauliers Due to Customs-Linked Cash-Flow Stress

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea and Inland Water

- 5.1.1.4 Air

- 5.1.2 Warehousing and Storage

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-Product Category

- 5.3.1 Meat, Seafood, and Poultry

- 5.3.2 Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Horticulture (Fresh Fruits and Vegetables)

- 5.3.4 Processed Food Products

- 5.3.5 Pet Food

- 5.3.6 Others (Spreads, Seasoning, Dressing, Specialty and Functional Foods, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 GXO Logistics

- 6.4.3 Culina Group

- 6.4.4 Seafrigo Group

- 6.4.5 Turners (Soham) Ltd

- 6.4.6 Kuehne+Nagel

- 6.4.7 DFDS Logistics

- 6.4.8 XPO Logistics

- 6.4.9 DACHSER

- 6.4.10 Lineage, Inc.

- 6.4.11 NewCold

- 6.4.12 La Poste Group (Including DPD UK)

- 6.4.13 DSV A/S

- 6.4.14 Hellmann Worldwide Logistics

- 6.4.15 Constellation Cold Logistics

- 6.4.16 Kammac

- 6.4.17 McCulla Refrigerated Transport

- 6.4.18 Rhenus Logistics

- 6.4.19 Certa Logistics

- 6.4.20 Supply Chain Solution Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

食品低溫運輸市場報告:趨勢、預測與競爭分析(至2035年)

食品低溫運輸市場報告:趨勢、預測與競爭分析(至2035年) 食品物流市場:2026-2032年全球市場預測(依溫度分類、運輸方式、服務類型、食品類型及最終用戶分類)

食品物流市場:2026-2032年全球市場預測(依溫度分類、運輸方式、服務類型、食品類型及最終用戶分類) 食品低溫運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

食品低溫運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 食品物流市場機會、成長要素、產業趨勢分析及2026-2035年預測。中東食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

食品物流市場機會、成長要素、產業趨勢分析及2026-2035年預測。中東食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)