|

市場調查報告書

商品編碼

2063357

法國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)France Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

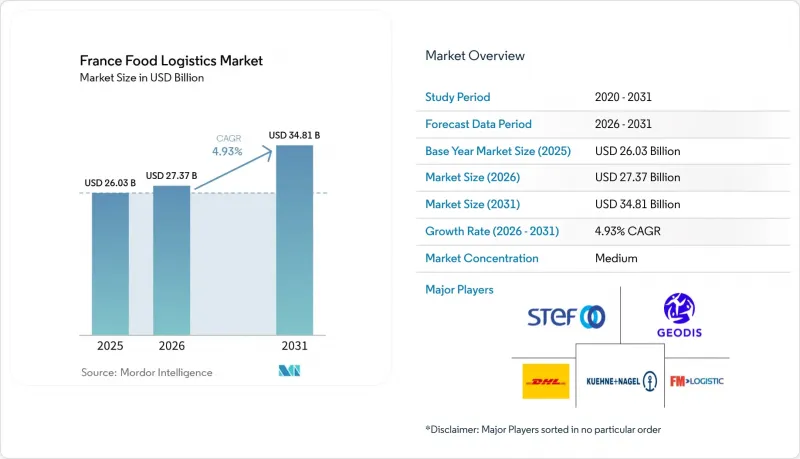

根據 Mordor Intelligence 預測,法國食品物流市場規模預計將從 2025 年的 260.3 億美元成長到 2026 年的 273.7 億美元,到 2031 年達到 348.1 億美元,2026 年至 2031 年的複合年成長率為 4.93%。

對經認證的有機產品的強勁需求、更嚴格的HACCP和ISO 22000審核,以及在通用農業政策(CAP)資助下農場冷藏設施的現代化改造,正在重塑設施標準和分銷路線設計。本報告按服務(運輸、倉儲和儲存、附加價值服務)、溫度控制類型(低溫運輸、非低溫運輸)和最終產品類別(肉類、水產品和家禽、乳製品、園藝作物、加工食品、寵物食品及其他)進行細分。市場預測以美元計價。

法國食品物流市場的趨勢與洞察

有機認證食品數量激增,需要專門的冷鏈物流。

物流業者正在對倉庫進行隔離,以消除交叉污染,並引入配備Ecocert認證衛生管理系統的雙溫運輸車輛,這導致固定成本增加,但合約利潤也隨之提高。有機乳製品的周轉速度比傳統產品更快,需要更頻繁的配送路線,而30%至50%的高溢價也推動了對基於區塊鏈的批次追蹤技術的投資。專注於有機食品的利基承運商正從尋求符合審核清單供應商的全國性零售商那裡獲得業務。因此,在奧克西塔尼等高成長地區,對認證運輸能力的需求超過了供應,給專用低溫運輸貨運價格帶來了越來越大的上漲壓力。

HACCP/ISO 22000 審核的日益嚴格,推動了對符合這些標準的第三方物流倉庫的需求不斷成長。

家樂福、Ocean 和其他大型公司現在只接受已獲得 ISO 22000 認證的倉庫的競標,這縮小了未認證營運商的市場。認證需要有文件記錄的關鍵控制點協議和持續的員工培訓,但小規模承運商難以獲得資金籌措,這加速了法國食品物流市場的整合。高階嬰幼兒配方奶粉和機能性食品的托運人正在將製藥業的 GDP 標準應用於進口,推動了對冗餘冷藏和遠端溫度遙測系統的投資。因此,符合標準的第三方物流公司可以收取 8-12% 的運費溢價,從而抵消認證成本並提高獲利能力。

自然冷凍設備短缺導致車輛和倉庫的更換工作延期。

適用於-25°C冷凍運輸路線的運輸設備全球僅有三家OEM廠商提供,導致採購價格高出35-45%。法國運輸商面臨兩難:要麼支付自2022年以來飆升180%的氫氟碳化合物(HFC)冷媒充填成本,要麼支付自2022年以來飆升180%的氫氟碳化合物(HFC)冷媒充填成本,要麼等待缺貨的天然冷媒設備,但這樣可能導致服務中斷。熟練人員短缺加劇了這一瓶頸。到2027年,還需要額外2,500名認證技術人員來安裝和維護天然冷媒系統。由於大型第三方物流公司領先預訂工廠的生產檔期,小規模運輸商被迫繼續使用過時的設備,拖慢了法國食品物流市場的整體現代化進程。

細分市場分析

到2025年,運輸業將佔法國食品物流市場佔有率的46.24%,但由於司機短缺和柴油價格波動,其成長速度正在放緩。同時,附加價值服務正以7.49%的複合年成長率快速成長。這一轉變表明,托運人更傾向於選擇能夠透過單一食品安全管理系統處理快速冷凍、包裝和批次追蹤等環節的「批量計費」合作夥伴。隨著零售商推出需要在低溫環境下進行份量調整和組裝的已調理食品套裝,與代工包裝(合約包裝)相關的法國食品物流市場規模正在擴大。在增值設施中引入機器人,可將快速冷凍循環的精度提高到±0.5°C,從而減少高水分SKU的細胞損傷,並強化合約關鍵績效指標(KPI)。

由於2024年至2025年間現貨卡車運費預計將下降8%至12%,純貨運公司被迫考慮提供多式聯運服務,否則將市場佔有率拱手讓給綜合性第三方物流公司。鐵路擴建雖然提供了一定的補貼,增強了運輸韌性,但由於其調度柔軟性有限,目前冷藏貨運量佔比仍不足8%。因此,多家第三方物流公司開始提供公路和鐵路聯運服務,確保貨物隔天送達巴黎,同時將每個托盤二氧化碳排放減少70%。在整個法國食品物流產業,服務多元化正成為應對投入價格波動和運輸能力過剩的主要手段。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 經認證的有機食品處理量的激增需要專門的冷藏物流。

- HACCP 和 ISO 22000 審核的日益嚴格推動了對符合標準的第三方物流倉庫的需求。

- 布列塔尼和諾曼第近水產品運輸增加了冷凍食品在德國境內的運輸距離。

- 通用農業政策 (CAP)津貼正在推動農場冷藏設施的現代化。

- 佩皮尼昂-隆吉冷藏鐵路走廊的重新開放擴大了多模態的選擇範圍。

- 採用可再生能源供電的氨製冷樞紐可降低農村地區的物流成本。

- 市場限制因素

- 自然冷凍設備短缺導致車輛和倉庫的更換工作延期。

- 地方政府對二級公路實施的軸荷限制,限制了大容量冷藏卡車的運作。

- 與氣溫波動相關的責任險保費正在飆升。

- 中小企業資料碎片化阻礙了端到端低溫運輸的可視性。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按服務

- 運輸

- 路

- 鐵路

- 海運和內河航運

- 航空

- 倉庫/存儲

- 附加價值服務(快速冷凍、貼標籤、庫存管理等)

- 運輸

- 溫度控制方法

- 低溫運輸

- 室溫(15-25 度C)

- 冷藏(2-8 度C)

- 冷凍(低於 0 度C)

- 非低溫運輸

- 低溫運輸

- 按最終產品類別

- 肉類、魚貝類、家禽

- 乳製品和冷凍甜點(牛奶、冰淇淋、奶油等)

- 園藝(新鮮水果和蔬菜)

- 加工食品

- 寵物食品

- 其他(抹醬、調味料、沙拉醬、特殊/機能性食品等)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- STEF

- GEODIS

- DHL Group

- Kuehne+Nagel

- Denjean Logistique

- Groupe Olano

- XPO

- FM Logistic

- DSV(Incl. DB Schenker)

- Dachser

- Transgourmet France

- Ceva Logistics(CMA CGM)

- Constellation Cold Logistics

- Rhenus Logistics

- Lacroix Logistics

- Delanchy Group

- Le Roy Logistique

- DGS Transports

- Yusen Logistics

- AIT Worldwide Logistics, Inc

第7章 市場機會與未來展望

According to Mordor Intelligence, the france food logistics market size is expected to increase from USD 26.03 billion in 2025 to USD 27.37 billion in 2026 and reach USD 34.81 billion by 2031, growing at a CAGR of 4.93% over 2026-2031.

Strong demand for certified-organic products, stricter HACCP and ISO 22000 audits, and on-farm cold-storage modernization funded under the Common Agricultural Policy are reshaping facility standards and route design. This report is Segmented by Services (Transportation, Warehousing and Storage, Value-Added Services), by Temperature-Control Type (Cold Chain, Non Cold Chain), and by End-Product Category (Meat/Seafood/Poultry, Dairy Products, Horticulture, Processed Food, Pet Food, and Others). The Market Forecasts are Provided in Terms of Value (USD).

France Food Logistics Market Trends and Insights

Surge in Certified-Organic Food Volumes Requiring Dedicated Cold Logistics

Logistics providers are segmenting warehouses to eliminate cross-contamination and deploying dual-temperature vehicles with Ecocert-approved sanitation regimes, raising fixed costs but unlocking premium contractual yields. Organic dairy lines move faster than conventional SKUs, forcing more frequent route turns, while premium price points 30-50% above conventional support investment in blockchain lot traceability. Niche carriers specializing in organics are capturing business from national retailers who want suppliers that already satisfy audit checklists. Consequently, demand for certified capacity is outstripping supply in high-growth regions such as Occitanie, reinforcing upward pressure on dedicated cold-chain rates.

Tightening HACCP / ISO 22000 Audits Raising Demand for Compliant 3PL Warehouses

Carrefour, Auchan, and other majors now restrict tenders to ISO 22000-accredited depots, compressing the addressable market for non-certified operators. Certification requires documented critical-control protocols and continuous employee training that smaller fleets struggle to finance, accelerating consolidation within the France food logistics market. High-end infant-formula and functional-food shippers are importing GDP standards from pharma, spurring investment in redundant refrigeration and remote-temperature telemetry. As a result, compliant 3PLs can command 8-12% rate premiums, offsetting certification expenses and improving margin resilience.

Scarcity of Natural-Refrigerant Equipment Delaying Fleet & Warehouse Upgrades

Transport units suitable for -25 °C frozen lanes come from only three global OEMs, adding 35-45% to purchase prices. French carriers face a dilemma: pay burgeoning HFC refill costs up 180% since 2022 or wait for back-ordered natural-refrigerant gear and risk service gaps. The talent deficit compounds the bottleneck; an extra 2,500 certified technicians are required by 2027 to install and maintain natural systems. As large 3PLs pre-book factory slots, smaller fleets are left to operate aging kit, tempering modernization across the France food logistics market.

Other drivers and restraints analyzed in the detailed report include:

- Seafood Nearshoring to Brittany & Normandy Boosting Domestic Reefer Mileage

- Common Agricultural Policy Grants Driving On-Farm Cold-Storage Modernization

- Escalating Insurance Premiums Linked to Temperature-Excursion Liability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation retained a 46.24% grip on France food logistics market share in 2025, yet its growth is muted by driver shortages and volatile diesel prices, whereas value-added services are climbing at 7.49% CAGR. This shift shows that shippers prefer single-invoice partners who can handle blast freezing, kitting, and lot-traceability under one food-safety umbrella. The France food logistics market size attached to co-packing lines is rising as retailers launch ready-meal bundles that require synchronized portioning and cold assembly. Robotics adoption inside value-added facilities improves accuracy to +-0.5 °C in blast-freeze cycles, reducing cell damage in high-moisture SKUs and strengthening contractual KPIs.

Spot trucking rates fell 8-12% in 2024-2025, forcing pure haulers to explore intermodal offerings or cede share to integrated 3PLs. Rail's subsidy-backed advance adds resilience, yet scheduling rigidity still caps its share below 8% of cold volumes. Several 3PLs are therefore bundling road-rail packages that guarantee next-day Paris arrival while cutting CO2 per pallet by 70%. Across the France food logistics industry, service diversification is the main hedge against input-price swings and capacity overhangs.

List of Companies Covered in this Report:

- STEF

- GEODIS

- DHL Group

- Kuehne + Nagel

- Denjean Logistique

- Groupe Olano

- XPO

- FM Logistic

- DSV (Incl. DB Schenker)

- Dachser

- Transgourmet France

- Ceva Logistics (CMA CGM)

- Constellation Cold Logistics

- Rhenus Logistics

- Lacroix Logistics

- Delanchy Group

- Le Roy Logistique

- DGS Transports

- Yusen Logistics

- AIT Worldwide Logistics, Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Certified-Organic Food Volumes Requiring Dedicated Cold Logistics

- 4.2.2 Tightening HACCP / ISO 22000 Audits Raising Demand for Compliant 3PL Warehouses

- 4.2.3 Seafood Nearshoring to Brittany & Normandy Boosting Domestic Reefer Mileage

- 4.2.4 Common Agricultural Policy (CAP) Grants Driving On-Farm Cold-Storage Modernization

- 4.2.5 Reopening of Perpignan-Rungis Refrigerated Rail Corridor Expanding Multimodal Options

- 4.2.6 Renewable-Energy Ammonia Refrigeration Hubs Lowering Rural Distribution Costs

- 4.3 Market Restraints

- 4.3.1 Scarcity of Natural-Refrigerant Equipment Delaying Fleet & Warehouse Upgrades

- 4.3.2 Municipal Axle-Weight Limits on Secondary Roads Constraining High-Capacity Reefers

- 4.3.3 Escalating Insurance Premiums Linked to Temperature-Excursion Liability

- 4.3.4 Data Fragmentation Among SMEs Hindering End-To-End Cold-Chain Visibility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea and Inland Water

- 5.1.1.4 Air

- 5.1.2 Warehousing and Storage

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-Product Category

- 5.3.1 Meat, Seafood, and Poultry

- 5.3.2 Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Horticulture (Fresh Fruits & Vegetables)

- 5.3.4 Processed Food Products

- 5.3.5 Pet Food

- 5.3.6 Others (Spreads, Seasoning, dressing, Specialty & Functional Foods, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 STEF

- 6.4.2 GEODIS

- 6.4.3 DHL Group

- 6.4.4 Kuehne + Nagel

- 6.4.5 Denjean Logistique

- 6.4.6 Groupe Olano

- 6.4.7 XPO

- 6.4.8 FM Logistic

- 6.4.9 DSV (Incl. DB Schenker)

- 6.4.10 Dachser

- 6.4.11 Transgourmet France

- 6.4.12 Ceva Logistics (CMA CGM)

- 6.4.13 Constellation Cold Logistics

- 6.4.14 Rhenus Logistics

- 6.4.15 Lacroix Logistics

- 6.4.16 Delanchy Group

- 6.4.17 Le Roy Logistique

- 6.4.18 DGS Transports

- 6.4.19 Yusen Logistics

- 6.4.20 AIT Worldwide Logistics, Inc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

食品低溫運輸市場報告:趨勢、預測與競爭分析(至2035年)

食品低溫運輸市場報告:趨勢、預測與競爭分析(至2035年) 食品物流市場:2026-2032年全球市場預測(依溫度分類、運輸方式、服務類型、食品類型及最終用戶分類)

食品物流市場:2026-2032年全球市場預測(依溫度分類、運輸方式、服務類型、食品類型及最終用戶分類) 食品低溫運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

食品低溫運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 食品物流市場機會、成長要素、產業趨勢分析及2026-2035年預測。中東食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)英國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

食品物流市場機會、成長要素、產業趨勢分析及2026-2035年預測。中東食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)英國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)