|

市場調查報告書

商品編碼

2063339

德國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Germany Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

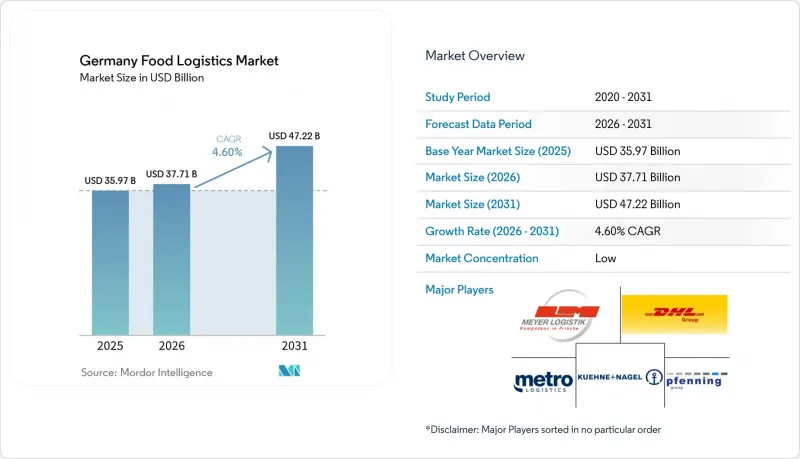

據 Mordor Intelligence 稱,2025 年德國食品物流市場價值 359.7 億美元,預計到 2031 年將達到 472.2 億美元,而 2026 年為 377.1 億美元,預測期(2026-2031 年)複合年成長率為 4.60%。

本報告按服務(運輸、倉儲、附加價值服務及其他)、溫控類型(低溫運輸和非低溫運輸)、最終產品類別(肉類和魚貝類、乳製品和冷凍甜點、水果和蔬菜、食品和飲料及其他)以及地區進行細分。市場預測以美元計價。

德國食品物流市場的趨勢與洞察

線上雜貨和食品配送服務的擴展

預計2025年,食品電商將佔德國食品雜貨銷售額的4.3%,同時維持較高的低溫運輸利用率,提高向都市區中心配送的頻率,並降低單次配送量。零售商傾向於採用混合型履約,將店內揀貨與集中式微型配送中心相結合,從而提高周轉率並減少易腐品的浪費。基於路線的宅配模式依賴可預測的訂單密度和最低購買量政策來確保單件盈利,這促使零售商採用預約配送和動態定價。每周定期採購的模式有助於提高車輛利用率,並維持人口稠密的大都會區冷藏運輸路線的穩定運作。這些趨勢強化了大都會圈物流網路中的多溫區樞紐網路,並增加了德國食品物流市場對冷藏和冷凍整合運輸能力的需求。

折扣零售商的主導地位

隨著自有品牌日益普及,以及平價商品通路不斷拓展分銷網路,折扣通路已經影響到定價和品類趨勢,進而影響到必需品和日用品的補貨模式。 Aldi Nord 位於 Lehrte-Aligse 的新物流中心於 2024 年底投入運營,清楚地展現了其單體物流中心的規模優勢,以及對需要可靠冷藏保管和裝卸貨平台規劃管理的生鮮產品品類的重視。不斷擴大的市場區域和高托盤周轉率使得折扣零售商能夠與物流公司協商更嚴格的交貨時限和更穩定的溫度控制,從而提高了對物流公司的基本服務要求。自有品牌的優質化增加了包裝和配套工作,這些工作通常外包給物流合作夥伴,從而帶動了折扣零售商價值鏈中增值業務的成長。隨著折扣零售商不斷追求可靠的新鮮度和高效的運營,這些因素正在提升多溫區物流和聯合包裝在德國食品物流市場中的作用。

嚴重的司機短缺危機

德國正面臨嚴重的司機短缺問題,這導致車輛運轉率下降,配送可靠性降低。產業和媒體通報顯示,未來十年內,這項短缺狀況將持續,退休人數將超過新入行人數。東西德之間的薪資差距使得招募和留住駕駛變得困難,而培訓時間和保險要求也限制了透過許可證改革來提升供應能力的速度。運輸公司正透過提高薪資、發放獎金和重新設計路線來應對,但人員配置不平衡仍然導致中標者撤回競標,並在生鮮食品銷售旺季期間造成門市交貨延誤。由於目前的營運模式無法取代人工搬運、驗收、交接和保全服務,自動駕駛仍然是長期的解決方案。這些限制表明,在德國食品物流市場透過新司機的加入和選擇性自動化緩解短缺之前,運輸能力和成本方面的短期壓力將持續存在。

細分市場分析

到2025年,運輸服務佔總收入的53.78%,成為一項重要的業務領域。這得歸功於生鮮食品和周轉率必需品在全國運輸路線和都會區內密集的區域間配送。在道路運輸,中短程路線支援冷藏和冷凍貨物的即時補貨,使得拖車利用率和碼頭周轉率成為德國食品物流市場網路性能的核心要素。倉儲業持續擴張,主要集中在多溫區和都市區微型倉配中心,業者會根據主要城市的訂單高峰日調整庫存佈局。鐵路運輸在上游工程原料和包裝材料的運輸中再次發揮重要作用,預計2026年的合約將使每年新增1000多列連接工業區的列車,與道路運輸相比,這將減少排放。預計到 2031 年,貼標、套件組裝和無塵室重新包裝等附加價值服務將以 5.64% 的複合年成長率成長。這反映了自有品牌本地化、促銷管理以及透過在低溫運輸設施內預組裝單位降低門市人事費用的需求。

IFS物流第三版要求跨站點和整個車隊進行持續的運作記錄、清潔週期記錄和物料平衡追蹤,並整合相關系統,這使得規模和合規性成為德國食品物流行業的關鍵優勢。策略性措施持續加強國內整合和專業路線建設,例如2026年的收購,將一個擁有100多名物流專家和車輛的網路整合到一個更廣泛的歐洲網路中。這些網路和運能的提升提高了食品托運人的服務水平,滿足了他們對可靠處理預約和保存期限保障的需求。隨著附加價值服務比例的增加,營運商正在將符合HACCP標準的流程整合到溫控空間中,並在保持合規性的同時支持大規模客製化,這進一步凸顯了全方位服務供應商在德國食品物流市場中的差異化優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 線上雜貨和食品宅配服務的擴展

- 折扣零售商的優勢

- 低溫運輸基礎設施現代化

- 永續性和綠色物流義務

- 定位為中歐物流樞紐

- 簡便食品和調理食品的成長

- 市場限制因素

- 嚴重的司機短缺危機

- 高昂的能源成本和營運成本

- 嚴格遵守規章制度

- 都市區物流空間短缺

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 零售業趨勢

第5章 市場規模與成長預測

- 按服務

- 運輸

- 路

- 鐵路

- 水

- 航空

- 倉儲業

- 附加價值服務及其他

- 運輸

- 溫度控制方法

- 低溫運輸

- 室溫(15-25 度C)

- 冷藏(2-8 度C)

- 冷凍(低於0°C)

- 非低溫運輸

- 低溫運輸

- 最終產品

- 肉類和水產品

- 乳製品和冷凍甜點

- 水果和蔬菜

- 食品/飲料

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nagel-Group

- DHL Group

- Pfenning group

- Metro Logistics

- Meyer Logistik

- Bruggemann Spedition+Logistik GmbH and Co. KG

- Kuehne Nagel

- Dachser

- Rhenus Logistics

- DSV

- Geodis

- Fiege Logistics

- Hellmann Worldwide Logistics

- BLG Logistics

- Quehenberger Logistics

- Worldwide Logistics Group

- NewCold

- Den Hartogh Logistics

- Kerry Logistics

- AIT Worldwide Logistics

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany food logistics market size was valued at USD 35.97 billion in 2025 and is estimated to grow from USD 37.71 billion in 2026 to reach USD 47.22 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031).

This report is Segmented by Services (Transportation, Warehousing, Value-Added Services, and Others), by Temperature-Control Type (Cold Chain and Non-Cold Chain), by End-Product Category (Meat & Seafood, Dairy & Frozen Desserts, Fruits & Vegetables, Food and Beverages, and Others), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Germany Food Logistics Market Trends and Insights

Online Grocery and Food Delivery Expansion

Food e-commerce reached an estimated 4.3% share of German grocery revenues in 2025, which sustained higher cold-chain utilization and more frequent, smaller drops to urban nodes. Retailers favor hybrid fulfillment that combines store-based picking and centralized micro-hubs, which improves asset turns and reduces spoilage in time-sensitive categories. Route-based home delivery models rely on predictable order densities and minimum-basket policies to protect unit economics, which encourages the use of scheduled slots and dynamic pricing. The shift to planned weekly baskets supports higher vehicle utilization and steadier refrigerated-lane flows across cities with dense catchment zones. These dynamics reinforce a multi-temperature footprint inside metropolitan distribution networks, which strengthens demand for integrated chilled and frozen capacity in the Germany food logistics market.

Discount Retailer Dominance

The discount channel set the tone on price and assortment as private-label penetration deepened and value formats expanded their distribution footprints, which shaped replenishment patterns for staples and convenience items. Aldi Nord's new Lehrte-Aligse logistics center, opened in late 2024, illustrates the scale of single-site throughput and the emphasis on fresh categories that require reliable cold storage and dock-door planning. Larger catchment areas and high pallet turns allow discounters to negotiate tighter delivery windows and consistent temperature controls, which lifts baseline service obligations for carriers. Premiumization within private labels adds packaging and kitting tasks that often shift to logistics partners, which creates growth for value-added operations linked to discount supply chains. These effects elevate the role of multi-temperature distribution and co-packing inside the Germany food logistics market as discounters seek efficiency with reliable freshness.

Acute Driver Shortage Crisis

Germany faces an acute driver deficit that strains fleet utilization and delivery reliability, with industry and media reports pointing to persistent gaps as retirements outpace new entrants through the decade. Wage differentials between western and eastern regions complicate recruitment and retention, while training timelines and insurance requirements limit the speed at which licensing reforms can improve availability. Carriers respond with higher pay, bonuses, and route redesign, but staffing imbalances still trigger rejected tenders and missed store windows during seasonal peaks for perishables. Autonomous driving remains a long-horizon option as human handling, custody transfer, and security roles cannot be replaced in current operating models. This constraint keeps short-term pressure on capacity and costs in the Germany food logistics market until new entrants and selective automation ease the shortage.

Other drivers and restraints analyzed in the detailed report include:

- Cold Chain Infrastructure Modernization

- Sustainability and Green Logistics Mandates

- High Energy and Operational Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation services accounted for 53.78% of revenues in 2025 as the dominant activity set, supported by dense regional flows for perishable foods and fast-moving staples across national corridors and urban catchments. Within road transport, short- to medium-haul routes underpin just-in-time replenishment for chilled and frozen items, which keeps trailer utilization and dock turns central to network performance in the Germany food logistics market. Warehousing continues to scale around multi-temperature zones and urban micro-fulfillment nodes, with operators aligning inventory placement to peak-day order profiles in major cities. Rail is regaining relevance for upstream ingredients and packaging, as seen in a 2026 contract that added more than 1,000 trains per year to connect industrial sites and reduce emissions versus road. Value-added services, including labeling, kitting, and cleanroom repacking, are projected to expand at a 5.64% CAGR to 2031, which reflects the need to localize private labels, manage promotions, and reduce store labor through pre-assembled units inside cold-chain facilities.

Scale and compliance are pivotal advantages in the Germany food logistics industry as IFS Logistics Version 3 demands always-on temperature logging, documented cleaning cycles, and mass-balance traceability that require integrated systems across sites and fleets. Strategic moves continue to strengthen national groupage and specialty routes, evidenced by a 2026 acquisition that integrated more than 100 logistics specialists and a fleet footprint into a broader European network. These network and capability upgrades lift the service floor for food shippers that depend on reliable dock appointments and shelf-life assurance. As value-added share rises, operators are embedding HACCP-compliant workflows in temperature-controlled spaces to support customization at scale while preserving audit readiness, which further differentiates full-service providers inside the Germany food logistics market.

List of Companies Covered in this Report:

- Nagel-Group

- DHL Group

- Pfenning group

- Metro Logistics

- Meyer Logistik

- Bruggemann Spedition + Logistik GmbH and Co. KG

- Kuehne Nagel

- Dachser

- Rhenus Logistics

- DSV

- Geodis

- Fiege Logistics

- Hellmann Worldwide Logistics

- BLG Logistics

- Quehenberger Logistics

- Worldwide Logistics Group

- NewCold

- Den Hartogh Logistics

- Kerry Logistics

- AIT Worldwide Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Online Grocery and Food Delivery Expansion

- 4.2.2 Discount Retailer Dominance

- 4.2.3 Cold Chain Infrastructure Modernization

- 4.2.4 Sustainability and Green Logistics Mandates

- 4.2.5 Central European Distribution Hub Position

- 4.2.6 Convenience Food and Ready-Meals Growth

- 4.3 Market Restraints

- 4.3.1 Acute Driver Shortage Crisis

- 4.3.2 High Energy and Operational Costs

- 4.3.3 Stringent Regulatory Compliance

- 4.3.4 Limited Urban Logistics Space

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Retail Landscape Influence

5 Market Size and Growth Forecasts

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Water

- 5.1.1.4 Air

- 5.1.2 Warehousing

- 5.1.3 Value-Added Services and Others

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non-Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-product Category

- 5.3.1 Meat & Seafood

- 5.3.2 Dairy & Frozen Desserts

- 5.3.3 Fruits & Vegetables

- 5.3.4 Food and Beverages

- 5.3.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Nagel-Group

- 6.4.2 DHL Group

- 6.4.3 Pfenning group

- 6.4.4 Metro Logistics

- 6.4.5 Meyer Logistik

- 6.4.6 Bruggemann Spedition + Logistik GmbH and Co. KG

- 6.4.7 Kuehne Nagel

- 6.4.8 Dachser

- 6.4.9 Rhenus Logistics

- 6.4.10 DSV

- 6.4.11 Geodis

- 6.4.12 Fiege Logistics

- 6.4.13 Hellmann Worldwide Logistics

- 6.4.14 BLG Logistics

- 6.4.15 Quehenberger Logistics

- 6.4.16 Worldwide Logistics Group

- 6.4.17 NewCold

- 6.4.18 Den Hartogh Logistics

- 6.4.19 Kerry Logistics

- 6.4.20 AIT Worldwide Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

食品低溫運輸市場報告:趨勢、預測與競爭分析(至2035年)

食品低溫運輸市場報告:趨勢、預測與競爭分析(至2035年) 食品物流市場:2026-2032年全球市場預測(依溫度分類、運輸方式、服務類型、食品類型及最終用戶分類)

食品物流市場:2026-2032年全球市場預測(依溫度分類、運輸方式、服務類型、食品類型及最終用戶分類) 食品低溫運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

食品低溫運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 食品物流市場機會、成長要素、產業趨勢分析及2026-2035年預測。中東食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)英國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

食品物流市場機會、成長要素、產業趨勢分析及2026-2035年預測。中東食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)英國食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本食品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區食品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)