|

市場調查報告書

商品編碼

2043909

北美軟設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Soft Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

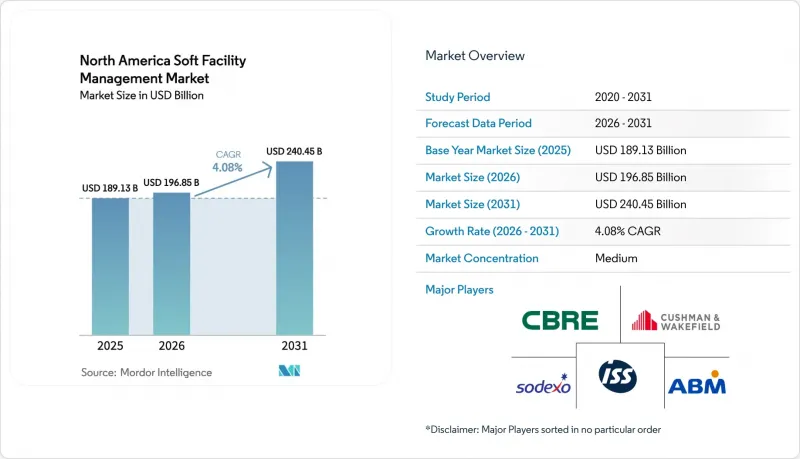

2025 年北美軟設施管理市場價值為 1,891.3 億美元,預計到 2031 年將達到 2,404.5 億美元,而 2026 年為 1968.5 億美元,預測期內複合年成長率為 4.08%。

(2026-2031 年),這表明能夠將勞動密集型服務與數位化管理相結合的供應商具有穩定的成長潛力。

儘管混合辦公模式、大型專案的竣工以及以健康為導向的維修計劃提振了合約需求,但對成本上升的擔憂正在加速企業從內部團隊向外包和績效合約的轉變。買家現在評估提案不再以小時人事費用為依據,而是以「每平方英尺可清潔的總成本」為依據,並透過物聯網儀錶板檢驗。能夠透過機器人技術和人工智慧驅動的工作指令最佳化,將工時減少兩位數的整合商,正在贏得多年期企業合約。與一般工資規則、PFAS 禁令以及網路安全指令相關的法規日益複雜,這意味著擁有專門合規負責人並能夠保護客戶免受訴訟風險的供應商仍然具有顯著優勢。

北美軟設施管理市場的趨勢與洞察

北美大型建設工程成長

在超過10億美元的大型建設項目中,軟性服務的調配被納入關鍵路徑,從而確保入住前的收入。例如,戈迪·豪國際大橋和Hudson隧道項目,均透過在交付前數月對清潔和安保服務進行綜合競標,縮短了傳統的銷售週期。這種早期簽約迫使供應商迅速擴大招聘、設備租賃和安全培訓規模,同時確保五年以上的可預測現金流。 2025年初,非住宅項目的訂單累積訂單達到9.2個月,為2019年以來的最高水平,顯示未來項目儲備充足。在地鐵和橋樑等受住宅房地產波動影響較小的領域,擁有危險物品處理資格和密閉空間作業經驗的承包商更受青睞。中期來看,計劃於2026年至2028年間竣工的大規模將把資本投資轉化為持續的業務收益,從而支持高於區域平均水平的成長。

商業不動產外包趨勢

企業業主和租戶優先選擇可變成本契約,以便靈活應對運轉率波動,並持續削減清潔和安保等非核心服務的人員配置。目前,一體化合約約佔外包支出的五分之一,高於2020年的15%,凸顯了其快速普及。資產組合整合簡化了發票匹配,減少了對採購人員的需求,並提高了轉換負責人的門檻。這解釋了為何提供禮賓式服務的建築租戶續租率提高了8個百分點。這一趨勢在配套設施競爭激烈的甲級辦公室中最為顯著,但即使是郊區建築的業主也在嘗試基於績效的定價模式,以在租賃續簽過程中保障淨營業利潤。

清潔人員人事費用上升和高離職率

預計2019年至2025年間,清潔工人的薪資中位數將上漲19.1%,超過整體薪資通膨率,對淨利率6%至10%的承包商帶來壓力。在紐約和舊金山等高成本大都會地區,離職率據通報超過75%,迫使公司為每位新員工承擔1,200至1,800美元的入職成本。許多競標現在都在合約中加入年度價格調整條款,在消費者物價指數的基礎上增加1個百分點,以應對意外的工資上漲。雖然機器人技術高效,但由於需要大量的資本投入和維護計劃,其應用僅限於利用率足以抵消投資成本的大規模場所。勞動力短缺威脅到服務水準的達標,並可能給供應商帶來經濟處罰和合約終止的風險,因此,勞動力短缺已成為企業成長面臨的最緊迫障礙。

細分市場分析

預計到2031年,安保和辦公室支援服務將以5.76%的年均成長率成長,高於北美整體軟性設施管理市場的平均水準。這項需求主要受混合辦公室模式的推動,這些模式需要無縫銜接的門禁控制、訪客篩選以及整合到辦公室體驗應用程式中的禮賓服務。清潔服務仍然是核心業務板塊,預計到2025年將佔總收入的38.89%,但隨著動作感測器和最佳化巡邏路線的普及,每個衛生間的清潔工時有所減少,其成長速度正在放緩。隨著企業越來越重視實體安全和網路安全整合領域的人才招聘,預計到2031年,北美與安保營運相關的軟性設施管理市場規模將達到100億美元。

建築業主正日益將保全、行李搬運和辦公空間預訂整合到單一的前台服務中,從而推高了每平方英尺的服務費用。在企業園區,餐飲服務的重要性正恢復到疫情前水平,餐飲補貼計畫預計到2025年,現場辦公人數將增加高達18個百分點。園林綠化、蟲害控制和廢棄物管理服務目前仍較為分散,但正在整合到綜合總合約中,從而簡化合規和報告流程。前台、郵件收發室和安保的綜合合約也為供應商提供了提升銷售活動管理和緊急應變培訓的切入點,從而擴大了其從客戶處獲得的收入佔有率。

預計到2025年,外包合約將佔市場支出的65.44%,年複合成長率達5.23%,凸顯了企業將固定人事費用轉化為變動成本的意願。其中,綜合設施管理合約成長最為迅速,反映出採購部門致力於精簡供應商名單,並將即時分析引入服務交付流程。相較之下,內部專案佔比為34.56%,主要局限於受安全許可要求和感染控制規程限制的行業。

在北美軟性設施管理市場,整合式服務包的佔有率預計將大幅成長。這是因為採購團隊可以將績效儀錶板整合到合約中,並近乎即時地對供應商實施獎懲措施。單一服務合約正逐漸失去市場支持,因為協調的摩擦如今已超過了價格折扣帶來的收益。捆綁式和非整合式服務包則為試驗外包的中型企業提供了一個過渡方案。通常情況下,一旦試點階段證明了成本節約,這些企業就會轉而升級到完全整合的合約。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 北美大型建設項目擴張

- 商業不動產外包趨勢

- 加大對醫療基礎建設的投資

- 實施一體化設施管理平台

- 對 WELL 和 Fitwel 認證工作空間的需求正在推動對專業軟體服務的需求。

- 租戶體驗應用程式的普及擴大了對家政服務的需求。

- 市場限制因素

- 人事費用上升和清潔工人離職率率高。

- FM數據平台日益成長的網路安全風險。

- 由於 PFAS 化學物質法規的限制,洗滌劑配方受到限制。

- 現場服務承包商的保險費上漲

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 價格分析

- 對與市場相關的宏觀經濟趨勢進行評估

第5章 市場規模與成長預測

- 按服務類型

- 打掃

- 安全和辦公支持

- 餐飲

- 其他軟體服務

- 按服務類型

- 內部

- 外包

- 單服務調頻廣播

- 捆綁式調頻廣播

- 綜合設施管理(IFM)

- 按公司規模

- 大公司

- 中小企業

- 按最終用戶行業分類

- 商業(IT/電信、零售、倉儲)

- 飯店餐飲業(飯店、餐廳)

- 機構和公共基礎設施

- 衛生保健

- 行業與流程

- 住宅和休閒

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CBRE Group Inc.

- Sodexo Inc.

- ISS A/S

- ABM Industries Inc.

- Cushman & Wakefield Plc

- Aramark Corporation

- Jones Lang LaSalle Incorporated

- GDI Integrated Facility Services Inc.

- Guardian Service Industries Inc.

- Emeric Facility Services

- SMI Facility Services

- AHI Facility Services Inc.

- Calico Building Services Inc.

- CleanNet USA Inc.

- ServiceMaster Clean

- Compass Group PLC

- Pritchard Industries Inc.

- Coverall North America Inc.

- Vanguard Cleaning Systems Inc.

- Flagship Facility Services

- Jani-King International Inc.

- Shine Facility Services

- Cintas Corporation

第7章 市場機會與未來展望

The North America Soft Facility Management Market size was valued at USD 189.13 billion in 2025 and is estimated to grow from USD 196.85 billion in 2026 to reach USD 240.45 billion by 2031, at a CAGR of 4.08% during the forecast period (2026-2031), illustrating steady headroom for vendors that can pair labor-intensive services with digital oversight.

Hybrid work schedules, mega-project completions, and wellness-oriented retrofit programs are reinforcing contract demand, while cost-inflation concerns are accelerating the pivot from in-house teams to outsourced, performance-priced agreements. Buyers now judge proposals on total cost per cleanable square foot, verified through Internet of Things dashboards, rather than on hourly labor rates. Integrators able to prove double-digit reductions in labor hours through robotics or AI work-order routing are winning multi-year enterprise deals. Regulatory complexity linked to prevailing-wage rules, PFAS bans, and cybersecurity directives continues to favor suppliers with dedicated compliance staff and the ability to de-risk clients from litigation exposure.

North America Soft Facility Management Market Trends and Insights

Growth of Mega Construction Projects in North America

Mega builds valued above USD 1 billion are embedding soft-service mobilization into the critical path, guaranteeing revenue before occupancy. Examples include the Gordie Howe International Bridge and the Gateway Hudson Tunnel, both of which executed integrated cleaning and security bids months ahead of handover, shortening traditional sales cycles. Early award of these contracts forces vendors to scale recruitment, equipment leasing, and safety training rapidly but locks in predictable cash flows for 5-plus years. The backlog indicator for non-residential projects hit 9.2 months in early 2025, the highest since 2019, signaling a robust future pipeline. Contractors with hazardous-material certifications and confined-space experience are favored for underground rail and bridge assets, segments less vulnerable to residential real-estate cycles. Over the medium term, substantial completions scheduled between 2026 and 2028 will convert capex into recurring service revenue, supporting above-average regional growth.

Rising Outsourcing Trend Across Commercial Real Estate

Corporate landlords and occupiers continue divesting non-core janitorial and security staff in favor of variable-cost contracts that flex with fluctuating occupancy. Integrated contracts now account for roughly one-fifth of outsourced spend, up from 15% in 2020, highlighting the speed of adoption. Portfolio consolidation simplifies invoice reconciliation, trims procurement headcount, and raises switching barriers, which explains why tenant-retention rates improved eight percentage points in buildings offering concierge-style services. The trend is strongest in Class A towers where amenity arms races intensify, but even suburban landlords are experimenting with performance pricing to defend net operating income as leases roll.

Rising Labor Costs and High Employee Turnover in the Janitorial Workforce

Median janitorial wages rose 19.1% from 2019 to 2025, outpacing overall wage inflation and squeezing margins for contractors operating on 6-10% net profits. High-cost metros like New York and San Francisco report turnover exceeding 75%, forcing agencies to spend USD 1,200-1,800 in onboarding costs per replacement. Many bidders now insert annual price-escalator clauses pegged to the consumer price index plus one percentage point to hedge unexpected wage hikes. Robotics helps but requires hefty capital outlays and maintenance programs, limiting penetration to large footprints where utilization justifies investment. Staffing strain can jeopardize service-level compliance, exposing vendors to financial penalties and contract termination, making labor availability the most immediate brake on growth.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Healthcare Infrastructure Investment

- Adoption of Integrated Facility Management Platforms

- PFAS Chemical Regulations Restricting Cleaning Formulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Security and office support services are set to expand at 5.76% annually through 2031, exceeding the overall North America soft facility management market average. Demand is fueled by hybrid work models that require frictionless access control, visitor vetting, and concierge desks woven into workplace-experience apps. Cleaning, still the backbone at 38.89% of 2025 revenue, faces slower expansion as motion sensors and optimized routing cut labor-minutes per restroom. The North America soft facility management market size attached to security roles is slated to reach double-digit billions by 2031 as enterprises prioritize physical-cyber convergence hiring.

Landlords increasingly combine guard posts, package handling, and workspace reservations into a single reception function, boosting per-square-foot service fees. Catering resumes its pre-pandemic importance on corporate campuses, where subsidized food programs lifted on-site attendance by up to 18 percentage points in 2025. Landscaping, pest control, and waste management remain fragmented but are being wrapped into bundled master agreements that simplify compliance and reporting. Integrated reception, mailroom, and security contracts also provide a gateway for vendors to upsell event management and emergency preparedness training, deepening wallet share.

Outsourced arrangements captured 65.44% of market spending in 2025 and are projected to rise at a 5.23% CAGR, emphasizing the appetite to convert fixed payrolls into variable costs. Within this pool, integrated facility management contracts are the fastest-moving slice, a reflection of procurement's determination to cut vendor lists and insert real-time analytics into service delivery. In contrast, in-house programs cling to 34.56%, largely in sectors bound by security-clearance mandates or infection-control protocols.

North America soft facility management market share for integrated packages is poised to jump as procurement teams embed performance dashboards into contracts, letting them sanction or reward suppliers in near real time. Single-service deals are losing favor because coordination friction now outweighs marginal price discounts. Bundled but non-integrated packages serve as a bridge for mid-size enterprises experimenting with outsourcing; many flow into fully integrated renewals after pilot phases validate savings.

The North America Soft Facility Management Market Report is Segmented by Service Type (Cleaning, Security and Office Support, Catering, and More), Offering Type (In-House, and Outsourced), Organisation Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- CBRE Group Inc.

- Sodexo Inc.

- ISS A/S

- ABM Industries Inc.

- Cushman & Wakefield Plc

- Aramark Corporation

- Jones Lang LaSalle Incorporated

- GDI Integrated Facility Services Inc.

- Guardian Service Industries Inc.

- Emeric Facility Services

- SMI Facility Services

- AHI Facility Services Inc.

- Calico Building Services Inc.

- CleanNet USA Inc.

- ServiceMaster Clean

- Compass Group PLC

- Pritchard Industries Inc.

- Coverall North America Inc.

- Vanguard Cleaning Systems Inc.

- Flagship Facility Services

- Jani-King International Inc.

- Shine Facility Services

- Cintas Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of Mega Construction Projects in North America

- 4.2.2 Rising Outsourcing Trend Across Commercial Real Estate

- 4.2.3 Increasing Healthcare Infrastructure Investment

- 4.2.4 Adoption of Integrated Facility Management Platforms

- 4.2.5 Demand for WELL and Fitwel Certified Workspaces Driving Specialized Soft Services

- 4.2.6 Proliferation of Tenant Experience Apps Enhancing Housekeeping Service Demand

- 4.3 Market Restraints

- 4.3.1 Rising Labor Costs and High Employee Turnover in Janitorial Workforce

- 4.3.2 Heightened Cybersecurity Risks for FM Data Platforms

- 4.3.3 PFAS Chemical Regulations Restricting Cleaning Formulations

- 4.3.4 Insurance Premium Inflation for On-site Service Contractors

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Cleaning

- 5.1.2 Security and Office Support

- 5.1.3 Catering

- 5.1.4 Other Soft Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single-service FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM (IFM)

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 Commercial (IT/Telecom, Retail, Warehouses)

- 5.4.2 Hospitality (Hotels, Restaurants)

- 5.4.3 Institutional and Public Infrastructure

- 5.4.4 Healthcare

- 5.4.5 Industrial and Process

- 5.4.6 Residential and Leisure

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group Inc.

- 6.4.2 Sodexo Inc.

- 6.4.3 ISS A/S

- 6.4.4 ABM Industries Inc.

- 6.4.5 Cushman & Wakefield Plc

- 6.4.6 Aramark Corporation

- 6.4.7 Jones Lang LaSalle Incorporated

- 6.4.8 GDI Integrated Facility Services Inc.

- 6.4.9 Guardian Service Industries Inc.

- 6.4.10 Emeric Facility Services

- 6.4.11 SMI Facility Services

- 6.4.12 AHI Facility Services Inc.

- 6.4.13 Calico Building Services Inc.

- 6.4.14 CleanNet USA Inc.

- 6.4.15 ServiceMaster Clean

- 6.4.16 Compass Group PLC

- 6.4.17 Pritchard Industries Inc.

- 6.4.18 Coverall North America Inc.

- 6.4.19 Vanguard Cleaning Systems Inc.

- 6.4.20 Flagship Facility Services

- 6.4.21 Jani-King International Inc.

- 6.4.22 Shine Facility Services

- 6.4.23 Cintas Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球共消化設施市場報告全球設施管理服務市場:機會與策略展望(至2035年)

2026年全球共消化設施市場報告全球設施管理服務市場:機會與策略展望(至2035年) 西班牙綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)菲律賓綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

西班牙綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)菲律賓綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)