|

市場調查報告書

商品編碼

1939568

南美貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)South America Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

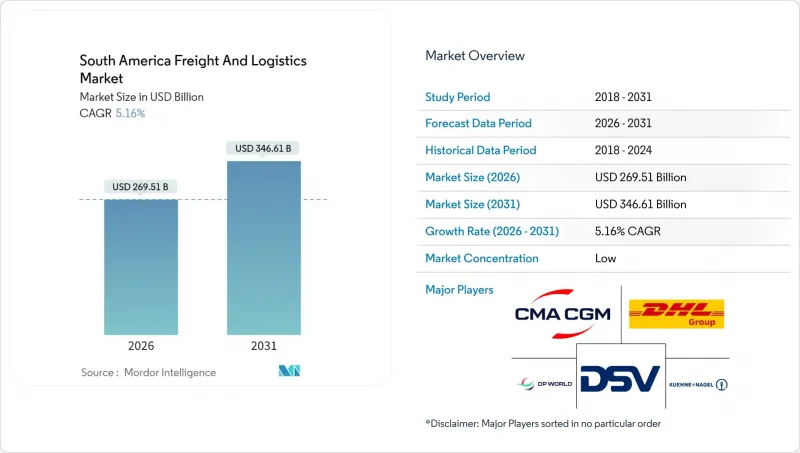

2025年南美貨運和物流市場價值為2,562.9億美元,預計到2031年將達到3,466.1億美元,高於2026年的2,695.1億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 5.16%。

這一擴張反映了該地區作為近岸外包目的地的吸引力、持續的基礎設施現代化以及數位化供應鏈解決方案的快速普及。巴西憑藉其多元化的工業基礎和港口網路保持著規模經濟優勢,而由中國支持的秘魯昌凱超級港預計將分流太平洋貿易流,並刺激內陸貨運量。電子商務的成長正在重塑對小包裹密集型網路的需求,而技術賦能的供應商可以提供靈活高效的「最後一公里」配送服務。然而,與氣候相關的河流水位波動、長期存在的道路堵塞以及複雜的跨境法規正在限制該行業的成長潛力。

南美洲貨運與物流市場趨勢及洞察

電子商務和最後一公里需求的快速成長

巴西、阿根廷和智利等大都會圈數位化零售的快速普及,正推動網路設計朝著以小包裹為中心的物流模式轉變,這需要密集的微型倉配中心網路。 Mercado Libre計劃在2025年底將其在巴西的配送中心數量從10個增加到21個,以支持其當日達和次日達的承諾。不斷成長的消費者期望正在推動對都市區分揀中心和低溫運輸微型倉庫的投資,這些設施能夠實現生鮮食品和藥品兩小時送達。小型包裹的出現降低了傳統零擔貨運的裝載率,同時也為限時送達服務提供了更高的定價空間。三大經濟體之間的跨境電子商務正在推動國際小包裹貨運量的成長,給傳統的海關程序帶來壓力,並刺激了對技術賦能的清關服務的需求。

近岸外包主導製造地遷移

為降低供應鏈風險,汽車和電子產品製造商正將生產從亞太地區轉移到南美,從而形成零件和成品的雙向流動。巴西的工業園區吸引著尋求南方共同市場(Mercosur)內優惠關稅待遇的供應商,而墨西哥日益增強的競爭力也給南美國家帶來了更大的壓力,迫使它們精簡物流成本。能夠整合多式聯運和合規安排的營運商將有機會佔據市場主導地位。由於設施位置取決於基礎設施質量,因此投資於靠近製造區的保稅倉庫的物流公司能夠創造強大的價值提案。

長期存在的公路和鐵路瓶頸

巴西-桑托斯走廊、阿根廷-羅薩裡奧糧食走廊和智利銅礦石走廊的運力限制導致貨物滯留時間過長,旺季期間每個貨櫃的滯期費超過200美元。老舊的單線鐵路和過時的號誌系統阻礙了模式轉換,而這種轉變本來可以緩解公路擁塞。資金短缺導致雙線鐵路和改良型多式聯運碼頭的建設進程延緩。擁有專屬運力的現有企業維持定價權,而依賴現有網路的新興企業則難以擴大規模。

細分市場分析

到2025年,製造業將佔南美洲貨運和物流市場規模的34.68%,其中巴西的汽車和電子產品叢集是核心。生產商優先選擇靠近港口的位置,以最大限度地減少內陸運輸的複雜性。受都市區購買力提升推動消費主導物流擴張的限制,預計2026年至2031年批發和零售業將以5.42%的複合年成長率成長。零售商正在將交叉轉運能力融入區域配送中心,以整合到貨並對小包裹進行分揀,從而實現最後一公里配送。

農業部門在收穫季節仍將保持其結構性重要地位,但低溫運輸出口的監管複雜性使其利潤率高於散裝糧食運輸。石油和天然氣貨物運輸增速放緩但貨運量保持穩定,為專業槽式貨櫃營運商提供了支撐。建築材料運輸需求與基礎設施投資激增密切相關,這有利於擁有靈活運輸合約的承運商。零售補貨和製造業供應鏈的整合為在供應鏈各個環節重複利用資產的綜合供應商創造了機會。

到2025年,貨運代理將成為最大的收入驅動力,佔南美貨運和物流市場規模的61.37%。商品出口、進口補給和工業供應鏈支撐著散貨和貨櫃貨物的持續流動。受電子商務和都市區當日達需求成長的推動,宅配業務(CEP)預計將在2026年至2031年間以5.73%的複合年成長率成長。隨著輕資產、小包裹遞送平台不斷擴大其覆蓋範圍,傳統卡車運輸業者在南美貨運和物流市場的佔有率將會下降。整合貨運代理和溫控倉儲服務的營運商透過為高成長的農產品出口商提供合規包裝服務,正在獲得價格優勢。

技術應用也在重塑價值結構。貨運匹配應用程式提高了卡車運轉率,並使小規模車隊能夠參與傳統的個人貨運網路。貨運代理業務仍然很重要,因為它們需要應對歐盟碳排放調節機制和森林砍伐預防認證,而這些措施增加了文件負擔。 Expeditors 2024 年第三季在拉丁美洲的營收成長了 31%,這凸顯了市場對合規驅動型貨運代理服務的高階需求。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 人口統計數據

- 按經濟活動分類的GDP分配

- 按經濟活動分類的GDP成長

- 通貨膨脹

- 経済パフォーマンスと概要

- 電子商務產業的趨勢

- 製造業の動向

- 運輸和倉儲業的GDP

- 出口趨勢

- 進口趨勢

- 燃油價格

- トラック輸送の運営コスト

- 卡車運輸車隊規模(按類型)

- 主要トラック供給業者

- 物流績效

- 輸送モード別シェア

- 海上輸送船隊の積載能力

- 班輪運輸連接

- 寄港地とパフォーマンス

- 貨物運賃の動向

- 貨物輸送量の動向

- 基礎設施

- 法規結構(公路和鐵路)

- 阿根廷

- 巴西

- 智利

- 秘魯

- 法規結構(海事和航空)

- 阿根廷

- 巴西

- 智利

- 秘魯

- 價值鍊和通路分析

- 市場促進因素

- 電子商務和最後一公里需求的快速成長

- 近岸外包主導製造地遷移

- 港口和走廊基礎設施開發

- 利用數位貨運平台提高整車運輸價格

- 為高附加價值農產品出口提供低溫運輸支持

- 透過區域自由貿易協定深化關稅同盟

- 市場限制

- 長期存在的公路和鐵路瓶頸

- 高昂的物流稅費和通行費

- 南方共同市場區域內跨境監管的片段化

- 氣候變遷造成的破壞(洪水、乾旱)

- 市場創新

- ポーターの五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- エンドユーザー産業

- 農業、漁業、林業

- 建造

- 製造業

- 石油天然氣、採礦和採石

- 批發和零售

- 其他

- 物流職能

- 宅配、速遞和小包裹(CEP)

- 目的地タイプ別

- 國內的

- 國際的

- 目的地タイプ別

- 貨運代理

- 透過交通工具

- 航空

- 海上,内陸水路

- 其他

- 透過交通工具

- 貨物運輸

- 透過交通工具

- 航空

- 管道

- 鐵路

- 路

- 海上,内陸水路

- 透過交通工具

- 倉儲和存儲

- 温度管理別

- 非温度管理

- 溫度控制

- 温度管理別

- 其他服務

- 宅配、速遞和小包裹(CEP)

- 國家

- 阿根廷

- 巴西

- 智利

- 秘魯

- 南美洲其他地區

第6章 競合情勢

- 市場集中度

- 主要な戦略的動きs

- 市佔率分析

- 公司簡介

- Agencias Universales SA(AGUNSA)

- Alonso Group

- Americold

- CMA CGM Group(Including CEVA Logistics)

- Correios

- DHL Group

- DP World

- DSV A/S(Including DB Schenker)

- Expeditors International of Washington, Inc.

- FedEx Corp.

- Kuehne+Nagel

- Log-In Logistica Integrada

- MercadoLibre, Inc.

- Rappi Logistics

- Romeu

- Rumo Logistica

- SAAM

- Scan Global Logistics(Including Blu Logistics)

- TASA Logistica

- United Parcel Service of America, Inc.(UPS)

第7章 市場機會與未來展望

The South America freight and logistics market was valued at USD 256.29 billion in 2025 and estimated to grow from USD 269.51 billion in 2026 to reach USD 346.61 billion by 2031, at a CAGR of 5.16% during the forecast period (2026-2031).

The expansion reflects the region's appeal as a nearshoring destination, continued infrastructure modernization, and rapid adoption of digital supply-chain solutions. Brazil retains scale benefits through its diversified industrial base and port network, while Peru's China-backed Chancay megaport is set to redirect Pacific trade flows and stimulate hinterland freight volumes. E-commerce growth is reshaping demand toward parcel-intensive networks that reward technology-enabled providers with agile last-mile capabilities. At the same time, climate-driven river level volatility, chronic road bottlenecks, and complex cross-border regulation temper the sector's growth potential.

South America Freight And Logistics Market Trends and Insights

E-Commerce Boom and Last-Mile Demand

Rapid digital retail adoption across metropolitan Brazil, Argentina, and Chile is transforming network design toward parcel-heavy flows that require dense micro-fulfillment footprints. Mercado Libre plans to raise its Brazilian distribution center count from 10 to 21 by end-2025 to support same-day and next-day delivery commitments. Heightened consumer expectations are pulling investment into urban sortation hubs and cold-chain micro-depots capable of meeting two-hour delivery windows for fresh groceries and pharmaceuticals. Parcel fragmentation pushes load factors down for traditional LTL yet enables premium pricing for time-definite services. Cross-border e-commerce among the three largest economies is adding international parcel volumes that test legacy customs procedures and stimulate demand for tech-enabled brokerage.

Nearshoring-Led Manufacturing Relocation

Supply-chain de-risking motivates automotive and electronics producers to relocate capacity from Asia-Pacific toward South America, generating bidirectional freight flows of components and finished goods. Brazil's industrial clusters attract suppliers seeking tariff advantages within MERCOSUR, while Mexico's competitiveness raises pressure on southern neighbors to streamline logistics costs. Integrated providers that can orchestrate multimodal moves and regulatory compliance stand to capture disproportionate share. Facility siting decisions hinge on infrastructure quality; therefore, logistics firms that invest in bonded warehousing close to manufacturing zones create compelling value propositions.

Chronic Road and Rail Bottlenecks

Capacity limitations in Brazil's Santos corridor, Argentina's Rosario grain routes, and Chile's copper corridors translate into prolonged dwell times and demurrage costs exceeding USD 200 per container during peak seasons. Legacy single-track rail and outdated signaling hamper modal shifts that could relieve road congestion. Funding gaps slow double-tracking and intermodal terminal upgrades. Incumbent providers with dedicated capacity maintain pricing power, while start-ups reliant on fluid networks struggle to scale.

Other drivers and restraints analyzed in the detailed report include:

- Port and Corridor Infrastructure Upgrades

- Digital Freight Platforms Improving Truck Load Factors

- High Logistics Taxes and Tolls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing generated 34.68% of the South America freight and logistics market size in 2025, anchored by Brazil's autos and electronics clusters. Producers favor near-port locations to minimize inland drayage complexity. Wholesale and retail trade is projected for a 5.42% CAGR (2026-2031)as rising urban purchasing power fuels consumption-driven logistics. Retailers deploy regional distribution centers with embedded cross-dock functions that consolidate inbound freight and stage parcels for last-mile delivery.

Agriculture remains structurally significant during harvest cycles, yet compliance-heavy cold-chain exports provide higher margins than bulk grain shipments. Oil and gas cargoes display lower growth but stable volumes that support specialized tank container operators. Construction freight demand tracks infrastructure spending surges, rewarding carriers with flexible capacity contracts. Convergence of retail replenishment and manufacturing inputs creates opportunities for integrated providers that reuse assets across supply-chain stages.

Freight transport contributed the largest revenue slice, equal to 61.37% of the South America freight and logistics market size in 2025. Commodity exports, import replenishment, and industrial resupply underpin sustained bulk and container flows. CEP activities are forecast for a 5.73% CAGR (2026-2031), catalyzed by urban e-commerce and same-day delivery commitments. The South America freight and logistics market share held by legacy truckload carriers will trend lower as asset-light parcel platforms widen service reach. Providers integrating freight forwarding with temp-controlled warehousing gain pricing leverage by bundling compliance services for high-growth agrifood exporters.

Technology adoption also reshapes value pools. Load-matching applications increase truck utilization, allowing small fleets to penetrate formerly relationship-based freight networks. Freight forwarding retains relevance by navigating EU carbon adjustment mechanisms and deforestation certifications that increase documentary burden. Expeditors' 31% Latin American revenue jump in Q3 2024 illustrates the premium demand for compliance-centric forwarding.

The South America Freight and Logistics Market Report is Segmented by Logistics Function (Courier, Express, and Parcel, Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services), End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Wholesale and Retail Trade, Others), and Geography (Chile, Argentina, and Brazil). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Agencias Universales SA (AGUNSA)

- Alonso Group

- Americold

- CMA CGM Group (Including CEVA Logistics)

- Correios

- DHL Group

- DP World

- DSV A/S (Including DB Schenker)

- Expeditors International of Washington, Inc.

- FedEx Corp.

- Kuehne+Nagel

- Log-In Logistica Integrada

- MercadoLibre, Inc.

- Rappi Logistics

- Romeu

- Rumo Logistica

- SAAM

- Scan Global Logistics (Including Blu Logistics)

- TASA Logistica

- United Parcel Service of America, Inc. (UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.22.1 Argentina

- 4.22.2 Brazil

- 4.22.3 Chile

- 4.22.4 Peru

- 4.23 Regulatory Framework (Sea and Air)

- 4.23.1 Argentina

- 4.23.2 Brazil

- 4.23.3 Chile

- 4.23.4 Peru

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 E-Commerce Boom and Last-Mile Demand

- 4.25.2 Nearshoring-Led Manufacturing Relocation

- 4.25.3 Port and Corridor Infrastructure Upgrades

- 4.25.4 Digital Freight Platforms Improving Truck Load Factors

- 4.25.5 Cold-Chain Compliance for High-Value Agrifood Exports

- 4.25.6 Regional Free-Trade Agreements Deepening Customs Union

- 4.26 Market Restraints

- 4.26.1 Chronic Road and Rail Bottlenecks

- 4.26.2 High Logistics Taxes and Tolls

- 4.26.3 Mercosur Cross-Border Regulatory Fragmentation

- 4.26.4 Climate-Driven Disruption (Floods, Droughts)

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Suppliers

- 4.28.3 Bargaining Power of Buyers

- 4.28.4 Threat of Substitutes

- 4.28.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Peru

- 5.3.5 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Agencias Universales SA (AGUNSA)

- 6.4.2 Alonso Group

- 6.4.3 Americold

- 6.4.4 CMA CGM Group (Including CEVA Logistics)

- 6.4.5 Correios

- 6.4.6 DHL Group

- 6.4.7 DP World

- 6.4.8 DSV A/S (Including DB Schenker)

- 6.4.9 Expeditors International of Washington, Inc.

- 6.4.10 FedEx Corp.

- 6.4.11 Kuehne+Nagel

- 6.4.12 Log-In Logistica Integrada

- 6.4.13 MercadoLibre, Inc.

- 6.4.14 Rappi Logistics

- 6.4.15 Romeu

- 6.4.16 Rumo Logistica

- 6.4.17 SAAM

- 6.4.18 Scan Global Logistics (Including Blu Logistics)

- 6.4.19 TASA Logistica

- 6.4.20 United Parcel Service of America, Inc. (UPS)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

全球貨運和物流市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年)

全球貨運和物流市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年) 2026年全球貨車市場報告2026年全球貨運和物流市場報告2026年全球零碳運輸市場報告

2026年全球貨車市場報告2026年全球貨運和物流市場報告2026年全球零碳運輸市場報告 貨運及物流市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、最終使用者及運輸方式分類

貨運及物流市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、最終使用者及運輸方式分類 2026-2030年全球貨物審核與支付市場

2026-2030年全球貨物審核與支付市場 中東歐貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)亞太地區貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東歐貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)亞太地區貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)