|

市場調查報告書

商品編碼

1939641

泰國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Thailand Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

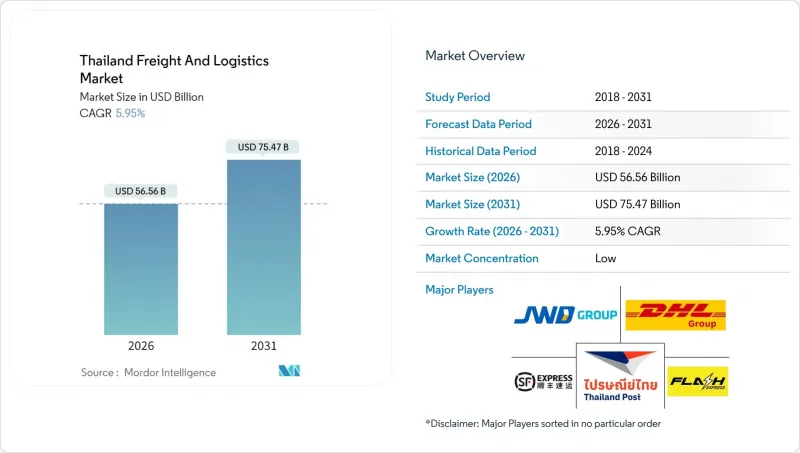

預計泰國貨運和物流市場將從 2025 年的 533.8 億美元成長到 2026 年的 565.6 億美元,到 2031 年達到 754.7 億美元,2026 年至 2031 年的複合年成長率為 5.95%。

泰國作為東協重要的多式聯運門戶,其製造業的持續回流以及政府主導的基礎設施投資,正支撐著這一穩定成長。大型政府計劃正在縮短運輸時間,而來自中國以外地區(中國+1)的投資湧入正在重塑配送走廊,並增加對綜合倉儲的需求。電子商務的成長持續推高小包裹量,要求業者對最後一公里網路進行現代化改造,並採用數據驅動的路線最佳化。從自動化倉庫到即時物聯網追蹤,數位化正成為一項至關重要的競爭優勢,而永續性的迫切需求正在加速向鐵路和電動卡車模式轉換。

泰國貨運物流市場趨勢及洞察

電子商務的快速成長和最後一公里配送的加速發展

隨著都市區家庭智慧型手機普及率超過90%,以及線上消費從偏好轉向日常必需品,小包裹量持續成長。網路技術的進步使曼谷能夠在保持全國次日達服務的同時,將平均配送時間縮短至24小時以內。國內快遞業者正將其策略從價格競爭轉向盈利管理,以提高單位盈利並釋放資金以進行自動化投資。區域合作推動了跨境物流的成長,泰國企業正利用中國平台實現對柬埔寨、寮國、越南、緬甸和越南(CLMV)市場的無縫配送。消費者對即時物流資訊的日益成長的需求,促使企業採用人工智慧驅動的動態路線規劃技術,以降低燃油成本和碳排放。

大型政府主導計劃(東部經濟走廊、2025-2026年規劃、陸上大橋)

東部經濟走廊(EEC)正推動新一輪港口、機場和鐵路互聯互通的升級改造,核准2024年將有168億美元的投資獲批。林查班港F碼頭擴建工程計畫於2027年新增400萬標準箱吞吐能力,屆時泰國貨櫃吞吐能力將提升40%。烏塔堡機場的多階段擴建工程正將該府打造成為三式聯運樞紐,實現高價值貨物從飛機到港口泊位六小時內的運輸。這些設施將提升多式聯運的連通性,並緩解公路交通瓶頸,有助於降低物流成本-目前物流成本佔泰國GDP的13%至14%。

物流成本持續居高不下(佔GDP的13-14%)

泰國的物流支出仍遠高於經合組織平均水平,這主要是由於該國80%的貨物運輸仍依賴道路運輸。分散的卡車運輸業者在採購燃料和設備方面議價能力有限,其中一半業者的卡車數量不足五輛。平均62小時的港口停留時間過長,增加了倉儲費和滯期費。由於商業銀行優先考慮風險較低的企業,中小型運輸公司面臨更嚴格的貸款條件。儘管2024年企業貸款增加了1.9%,但中小企業未償還貸款餘額卻有所下降。諸如經濟特區10%的企業所得稅率等獎勵應該能夠降低成本,但搬遷的先決條件限制了這些措施的實施。

細分市場分析

到2025年,製造業將佔總收入的32.21%,其中以東海岸的電子、汽車和石化產業叢集為支柱。高精度零件的配送需要溫控環境和快速清關,這有利於具備專業能力的企業。批發和零售預計將成為成長最快的行業,2026年至2031年的複合年成長率將達到6.38%,這主要得益於全通路零售商建立履約網路。更長的訂單截止時間和更豐富的當日送達時段正在推動對位於都市區消費者5公里半徑範圍內的微型倉配中心的需求。

食品加工企業和農業相關企業仍依賴冷藏運輸網路,將農村農場與曼谷的配送中心連結起來。由於地鐵和機場計劃,建築物流量依然強勁,但需求存在週期性波動。向電動車組裝的轉型帶來了電池組和稀土元素磁鐵等原料的進口,擴大了泰國的貨運和物流市場規模,而這些原料需要特殊的危險品處理。

截至2025年,貨運將佔泰國貨運和物流市場佔有率的61.12%,這反映了工業園區向港口和邊境口岸持續的大宗貨物運輸。東部經濟走廊與林查班港之間強大的基礎設施連接支撐了這一優勢。同時,快速成長的電子商務需求正在推動城際宅配(CEP)收入的成長,預計2026年至2031年其複合年成長率將達到6.92%。傳統的公路貨運公司正在整合即時遠端資訊處理技術,並與鐵路營運商合作,提供半多式聯運服務,從而降低高達12%的運輸成本。

物流業者正在實施倉庫管理系統,為托運人提供貨物可視性,從而實現預測性補貨並平抑季節性尖峰時段需求。隨著快遞網路日益密集,家用電器和電子產品的「額外」雙人配送服務正逐漸成為一項加值利基服務。政府的「陸橋計畫」旨在將跨印度洋-太平洋地區的貨櫃貨物流向南部海港,預計在2020年代中期進一步擴大泰國的貨運市場。同時,由於快遞業者引入了基於區域的定價和燃油額外費用費制度,預計貨運代理商在快遞行業的利潤率將有所提高。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 人口統計數據

- 按經濟活動分類的GDP分配

- 按經濟活動分類的GDP成長

- 通貨膨脹

- 經濟表現及概覽

- 電子商務產業的趨勢

- 製造業趨勢

- 運輸和倉儲業的GDP

- 出口趨勢

- 進口趨勢

- 燃油價格

- 卡車運輸營運成本

- 卡車運輸車隊規模(按類型)

- 主要卡車供應商

- 物流績效

- 透過交通方式分享

- 海運船隊運力

- 班輪運輸連接

- 停靠港口和航行記錄

- 貨運費率趨勢

- 貨物運輸量趨勢

- 基礎設施

- 法規結構(公路和鐵路)

- 法律規範(海事和航空)

- 價值鍊和通路分析

- 市場促進因素

- 電子商務的快速成長和最後一公里配送的加速發展

- 大型政府計劃(東部經濟走廊、2025-2026年規劃、陸上大橋)

- 製造業回歸及受「中國+1」策略影響的資金流入

- 數位化(人工智慧/運輸管理系統、物聯網視覺化、智慧倉庫管理)

- 強制推行綠色物流和促進鐵路電氣化

- 與柬埔寨、寮國、緬甸和越南(CLMV)國家的跨境貿易以及泛亞鐵路網路的活用狀況

- 市場限制

- 物流成本持續居高不下(約佔GDP的13-14%)

- 燃料價格波動及碳定價風險

- 電子商務平台對小型包裹遞送公司的利潤率帶來壓力

- 美國對泰國出口(汽車、電子設備)徵收關稅的風險

- 市場創新

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 終端用戶產業

- 農業、漁業、林業

- 建設業

- 製造業

- 石油天然氣、採礦和採石

- 批發和零售

- 其他

- 物流職能

- 快遞、快捷郵件和小包裹(CEP)

- 目的地

- 國內的

- 國際的

- 目的地

- 貨運代理

- 透過交通工具

- 航空

- 海路和內河航道

- 其他

- 透過交通工具

- 貨物運輸

- 透過交通工具

- 航空

- 管道

- 鐵路

- 路

- 海路和內河航道

- 透過交通工具

- 倉儲

- 透過溫度控制

- 非溫控型

- 溫度控制

- 透過溫度控制

- 其他服務

- 快遞、快捷郵件和小包裹(CEP)

第6章 競爭情勢

- 市場集中度

- 關鍵策略舉措

- 市佔率分析

- 公司簡介

- AP Moller-Maersk

- CMA CGM Group(Including CEVA Logistics)

- DHL Group

- DSV A/S(Including DB Schenker)

- FedEx

- Flash Express

- J&T Express

- JWD Group

- Kuehne+Nagel

- LEO Global Logistics Public Co., Ltd.

- Nippon Express Holdings.

- Profreight Group Co., Ltd.

- SCG Logistics, Ltd.

- SF Express(KEX-SF)

- Sub Sri Thai Public Co., Ltd.

- Thailand Post

- Toyota Tsusho(Thailand)Co., Ltd.

- Triple i Logistics Public Co., Ltd.

- United Parcel Service of America, Inc.(UPS)

- WICE Logistics Public Co., Ltd.

第7章 市場機會與未來展望

The Thailand freight and logistics market is expected to grow from USD 53.38 billion in 2025 to USD 56.56 billion in 2026 and is forecast to reach USD 75.47 billion by 2031 at 5.95% CAGR over 2026-2031.

Thailand's position as ASEAN's principal multimodal gateway, combined with sustained manufacturing reshoring and state-led infrastructure investment, underpins this steady expansion. Government mega-projects are compressing transit times, while China+1 investment inflows are reshaping distribution corridors and spurring demand for integrated warehousing. E-commerce continues to lift parcel volumes, prompting operators to modernize last-mile networks and deploy data-driven route optimization. Digitalization-from automated depots to real-time IoT tracking-has become a decisive competitive lever, and sustainability mandates are accelerating modal shifts toward rail and electric truck fleets.

Thailand Freight And Logistics Market Trends and Insights

E-Commerce Boom and Last-Mile Delivery Acceleration

Parcel volumes continue to rise as smartphone penetration surpasses 90% of urban households and online spending migrates from discretionary goods to daily staples. Network densification enables operators to shorten average delivery times to under 24 hours in Bangkok while maintaining nationwide next-day reach. Domestic CEP players have pivoted from aggressive price wars toward yield management, raising unit profitability and freeing cash flow for automation investments. Regional partnerships are unlocking cross-border volumes, with Thai firms leveraging Chinese platforms for seamless fulfillment into CLMV markets. Consumer expectation of real-time visibility is encouraging the rollout of AI-enabled dynamic routing, which cuts fuel costs and shrinks carbon footprints.

Government Mega-Projects (EEC, 2025-2026 Plan, Land Bridge)

The Eastern Economic Corridor anchors USD 16.8 billion of approved investment in 2024 and has catalyzed a new wave of port, airport, and rail link upgrades. The Laem Chabang Terminal F build-out, scheduled to add 4 million TEU capacity by 2027, expands Thailand's container handling headroom by 40%. U-Tapao airport's multi-phase expansion is transforming the province into a tri-modal junction capable of channeling high-value cargo from aircraft to seaport berth within six hours. These assets collectively reduce logistics costs-currently 13-14% of GDP-by lifting multimodal connectivity and alleviating road bottlenecks.

Persistently High Logistics Costs (13-14% of GDP)

Thailand's logistics outlay remains materially higher than the OECD average, largely because 80% of domestic cargo still moves by road. Fragmented trucking fleets lack bargaining power for fuel and equipment, and the median operator runs under five trucks. Port dwell times average 62 hours, adding storage and demurrage expenses. SME carriers face tighter credit as commercial banks prioritize lower-risk segments; SME loan balances fell in 2024 even as corporate lending inched up 1.9%. Policy incentives such as a 10% corporate tax rate in Special Economic Zones should ease the cost burden, yet relocation prerequisites temper uptake.

Other drivers and restraints analyzed in the detailed report include:

- Manufacturing Re-shoring and China+1 Inflows

- Digitalization (AI/TMS, IoT Visibility, Smart Warehousing)

- Fuel-Price Volatility and Carbon-Pricing Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing accounted for 32.21% of 2025 revenue, anchored by electronics, automotive, and petrochemical clusters in the Eastern Seaboard. High-precision component flows require climate-controlled environments and expedited customs clearance, favoring operators with specialized capabilities. Wholesale and Retail Trade is projected to register the fastest 6.38% CAGR (2026-2031) as omnichannel retailers embrace nationwide fulfillment meshes. Extended cut-off times and same-day delivery windows are pushing demand for micro-fulfillment centers within 5 kilometers of urban shoppers.

Food processors and agribusinesses continue to rely on refrigerated truck lanes linking upcountry farms to Bangkok distribution hubs. Construction logistics remain buoyant thanks to metro rail and airport projects, though they exhibit cyclical demand spikes. The shift toward electric-vehicle assembly is spawning new inbound flows of battery packs and rare-earth magnets, bolstering the Thailand freight and logistics market size for specialized dangerous-goods handling.

Freight Transport contributed 61.12% of Thailand freight and logistics market share in 2025, reflecting sustained bulk cargo flows from industrial estates to ports and border gates. Strong infrastructure links between the Eastern Economic Corridor and Laem Chabang underpin this dominance. At the same time, burgeoning e-commerce demand is propelling CEP revenues, expected to post a 6.92% CAGR between 2026-2031. Traditional road freight firms are integrating real-time telematics and partnering with rail operators to offer quasi-intermodal services that cut transit costs by up to 12%.

Logistics providers are embedding warehouse management systems that feed shipment visibility to shippers, enabling predictive replenishment and smoothing seasonal peaks. As CEP networks densify, "white-glove" two-person deliveries for appliances and electronics are emerging as value-added niches. The government's Land Bridge concept aims to divert trans-Indo-Pacific container flows through southern seaports, which could further expand the Thailand freight and logistics market size for freight transport by mid-decade. In contrast, forwarders expect margin uplift in CEP as operators implement zone-based pricing and fuel surcharge mechanisms.

The Thailand Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- A.P. Moller - Maersk

- CMA CGM Group (Including CEVA Logistics)

- DHL Group

- DSV A/S (Including DB Schenker)

- FedEx

- Flash Express

- J&T Express

- JWD Group

- Kuehne+Nagel

- LEO Global Logistics Public Co., Ltd.

- Nippon Express Holdings.

- Profreight Group Co., Ltd.

- SCG Logistics, Ltd.

- SF Express (KEX-SF)

- Sub Sri Thai Public Co., Ltd.

- Thailand Post

- Toyota Tsusho (Thailand) Co., Ltd.

- Triple i Logistics Public Co., Ltd.

- United Parcel Service of America, Inc. (UPS)

- WICE Logistics Public Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.23 Regulatory Framework (Sea and Air)

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 E-Commerce Boom and Last-Mile Delivery Acceleration

- 4.25.2 Government Mega-Projects (EEC, 2025-26 Plan, Land Bridge)

- 4.25.3 Manufacturing Re-Shoring and China+1 Inflows

- 4.25.4 Digitalisation (AI/TMS, IoT Visibility, Smart Warehousing)

- 4.25.5 Green-Logistics Mandates and Rail Electrification Push

- 4.25.6 Cross-Border CLMV Trade and Trans-Asian Rail Link Uptake

- 4.26 Market Restraints

- 4.26.1 Persistently High Logistics Cost (~13-14 % of GDP)

- 4.26.2 Fuel-Price Volatility and Carbon-Pricing Exposure

- 4.26.3 Parcel-Carrier Margin Squeeze by E-Commerce Platforms

- 4.26.4 U.S. Tariff Risks on Thai Exports (Autos, Electronics)

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Suppliers

- 4.28.3 Bargaining Power of Buyers

- 4.28.4 Threat of Substitutes

- 4.28.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 A.P. Moller - Maersk

- 6.4.2 CMA CGM Group (Including CEVA Logistics)

- 6.4.3 DHL Group

- 6.4.4 DSV A/S (Including DB Schenker)

- 6.4.5 FedEx

- 6.4.6 Flash Express

- 6.4.7 J&T Express

- 6.4.8 JWD Group

- 6.4.9 Kuehne+Nagel

- 6.4.10 LEO Global Logistics Public Co., Ltd.

- 6.4.11 Nippon Express Holdings.

- 6.4.12 Profreight Group Co., Ltd.

- 6.4.13 SCG Logistics, Ltd.

- 6.4.14 SF Express (KEX-SF)

- 6.4.15 Sub Sri Thai Public Co., Ltd.

- 6.4.16 Thailand Post

- 6.4.17 Toyota Tsusho (Thailand) Co., Ltd.

- 6.4.18 Triple i Logistics Public Co., Ltd.

- 6.4.19 United Parcel Service of America, Inc. (UPS)

- 6.4.20 WICE Logistics Public Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

全球貨運和物流市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年)

全球貨運和物流市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年) 2026年全球貨車市場報告2026年全球貨運和物流市場報告2026年全球零碳運輸市場報告

2026年全球貨車市場報告2026年全球貨運和物流市場報告2026年全球零碳運輸市場報告 貨運及物流市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、最終使用者及運輸方式分類

貨運及物流市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、最終使用者及運輸方式分類 2026-2030年全球貨物審核與支付市場

2026-2030年全球貨物審核與支付市場 中東歐貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)亞太地區貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)南美貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東歐貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)亞太地區貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)南美貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)