|

市場調查報告書

商品編碼

1692554

英國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)United Kingdom Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

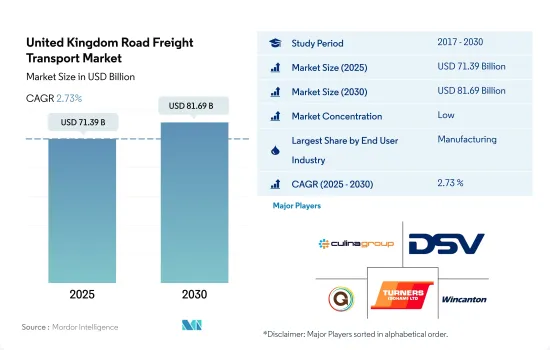

預計 2025 年英國公路貨運市場規模將達到 713.9 億美元,到 2030 年將達到 816.9 億美元,預測期間(2025-2030 年)的複合年成長率為 2.73%。

英國智慧製造資料中心(SMDH)舉措旨在提高中小企業的生產力並活躍公路貨運市場。

- 2022年,製造業在英國經濟中發揮至關重要的作用,貢獻了GDP的8%以上,相當於約2,700億美元。在製造業中,消費品佔據主導地位,佔了市場收益的 72% 佔有率。道路運輸的主要企業包括德國郵政敦豪集團、聯邦快遞、特納斯(索哈姆)有限公司、聯合包裹服務公司(UPS)和 Wincanton PLC。

- 2022年,英國零售和批發業佔GDP的6%以上。線下零售包括商店、百貨公司、超級市場、市場攤販甚至送貨上門銷售。在英國,線下零售額佔整個零售市場的68%以上。由於貨物需要有效率地運輸到各個零售店,大量的線下零售正在推動對公路貨運服務的需求。 Tesco 是英國最大的食品零售商,在全國擁有 4,169 家門市。另一家大公司 Sainsbury PLC 是一家多通路零售商,在英國擁有 1,400 家門市,提供雜貨、家居用品和服飾。

英國公路貨運市場趨勢

隨著消費者履約中心需求的成長,預計到 2027 年英國倉庫數量將達到 214,000 個

- 2024 年 5 月,杜拜環球港務集團在考文垂開設了迄今為止最大的倉庫,佔地 598,000 平方英尺,這是 5,000 萬英鎊(6,092 萬美元)投資的一部分,旨在增強客戶競爭力。此前,英國政府於 2023 年 9 月在比斯特開設了一座佔地 270,000 平方英尺的音樂和視訊分銷倉庫,該倉庫將處理英國70% 的實體音樂和 35% 的家庭娛樂產品。 DP World 先前已在特倫特河畔伯頓開設了一個 75,000 平方英尺的倉庫,並在倫敦門戶物流中心開設了一個 230,000 平方英尺的多用戶倉庫。杜拜環球港務集團在南安普敦和倫敦門戶設有樞紐,業務遍及 78 個國家,控制全球 10% 的貿易。預計這些舉措將提高該產業對 GDP 的貢獻。

- 英國大型倉庫的數量正在快速成長。到 2027 年,預計全球整體將有約 214,000 個面積超過 50,000 平方英尺的倉庫。許多倉庫將作為電子商務履約中心,到 2027 年,大約 18% 的倉庫將用於消費者履約。這一成長表明,隨著電子商務的擴張,作為貿易物流中心的倉庫比例開始轉向消費者履約中心。

英國政府對燃油價格有很大影響,燃油稅和增值稅(標準稅率為 20%)構成了汽油和柴油價格的大部分。

- 2022年8月,原油價格跌破100美元,月末收在每桶90.63美元。 2023年油價進一步下跌,5月跌至每桶72.50美元的低點。 2024年3月,英國汽油價格平均為每公升150.1披索,為2023年11月以來的最高水準。這是由於油價上漲以及中東局勢惡化導致英鎊兌美元走弱。雖然整體通膨有所緩和,但 3 月汽油和柴油價格上漲。 2024 年 4 月以色列對伊朗發動報復性攻擊後,油價飆升,隨後開始下跌。

- 2024 年 6 月,英國政府確認計畫在 2030 年強制要求噴射機燃料中至少含有 10% 的永續航空燃料 (SAF)。目前,SAF 比傳統燃料稀缺且昂貴,因此很難在航空領域增加其使用。 SAF 佔世界噴射機燃料的佔有率不到 0.1%。政府對 SAF 的授權將於 2025 年 1 月開始,但需獲得立法核准。這是 2022 年「Jet Zero」策略的延續,該策略的目標是到 2050 年實現航空業淨零排放。

英國公路貨運業概況

英國公路貨運市場細分,該市場的五個主要參與者是 Culina Group、DSV A/S(De Sammensluttede Vognmaend af Air and Sea)、Gregory Distribution Ltd.、Turners (Soham) Ltd. 和 Wincanton PLC。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 按經濟活動分類的GDP分佈

- 經濟活動GDP成長

- 經濟表現及概況

- 電子商務產業趨勢

- 製造業趨勢

- 交通運輸倉儲業GDP

- 物流績效

- 道路長度

- 出口趨勢

- 進口趨勢

- 燃油價格趨勢

- 卡車運輸成本

- 卡車持有量(按類型)

- 主要卡車供應商

- 公路貨運噸位趨勢

- 公路貨運價格趨勢

- 模態共享

- 通貨膨脹率

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 農業、漁業和林業

- 建設業

- 製造業

- 石油和天然氣、採礦和採石

- 批發和零售

- 其他

- 匯出目的地

- 國內的

- 國際貨運

- 卡車負載容量

- 整車裝載 (FTL)

- 零擔運輸 (LTL)

- 貨櫃運輸

- 貨櫃運輸

- 沒有容器

- 運輸距離

- 遠距

- 短途運輸

- 產品成分

- 流體產品

- 固體貨物

- 溫度控制

- 非溫控

- 溫度控制

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- AP Moller-Maersk

- Culina Group

- DACHSER

- 德國鐵路公司(包括德鐵信可)

- DHL Group

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Gist Ltd.

- Gregory Distribution Ltd.

- Howard Tenens

- Hoyer GmbH

- Kinaxia Logistics Limited

- Turners(Soham)Ltd.

- United Parcel Service of America, Inc.(UPS)

- WH Malcolm Ltd.

- Wincanton PLC

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 全球物流市場概覽

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(市場促進因素、限制因素、機會)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

- 外匯

The United Kingdom Road Freight Transport Market size is estimated at 71.39 billion USD in 2025, and is expected to reach 81.69 billion USD by 2030, growing at a CAGR of 2.73% during the forecast period (2025-2030).

UK's Smart Manufacturing Data Hub (SMDH) initiative aims to boost SME productivity, fueling the road freight market

- In 2022, the manufacturing sector played a significant role in the United Kingdom's economy, contributing over 8% to the GDP, equivalent to around USD 270 billion. The dominant subset within manufacturing was consumer goods, commanding a substantial 72% share of market revenue. Some of the major players in road transportation are Deutsche Post DHL Group, FedEx, Turners (Soham) Limited, United Parcel Service (UPS), and Wincanton PLC.

- In 2022, the retail and wholesale trade in the UK accounted for over 6% of the nation's GDP. Offline retail encompasses shops, department stores, supermarkets, market stalls, and even door-to-door sales. In the UK, offline retail sales make up more than 68% of the total retail market. This significant share of offline retail drives the demand for road freight services, as goods need to be transported efficiently to various retail outlets. Tesco stands as the UK's largest grocery retailer, boasting 4,169 stores nationwide. Another major player, Sainsbury PLC, operates as a multi-channel retailer, offering groceries, household goods, and clothing, with a footprint of 1,400 stores across the UK.

United Kingdom Road Freight Transport Market Trends

The UK's warehouse count is expected to reach 214,000 by 2027 due to a rise in demand for consumer fulfillment centers

- In May 2024, DP World opened its largest warehouse yet, a 598,000 sq ft facility in Coventry, as part of a GBP 50 million (USD 60.92 million) investment to boost customer competitiveness. This follows the September 2023 opening of a 270,000 sq ft music and video distribution warehouse in Bicester, handling 70% of the UK's physical music and 35% of home entertainment products. Previously, DP World opened a 75,000 sq ft site in Burton upon Trent and a 230,000 sq ft multi-user warehouse at London Gateway's logistics hub. Alongside its hubs at Southampton and London Gateway, operating in 78 countries, DP World manages 10% of global trade. Such initiaves are expected to boost the GDP contribution from the sector.

- The number of large warehouses in the United Kingdom is rapidly increasing. By 2027, there are expected to be around 214,000 warehouses larger than 50,000 square feet globally. Many of these warehouses are to serve as e-commerce fulfillment centers, and approximately 18% of all warehouses will be for consumer fulfillment by 2027. This increase suggests the global expansion of e-commerce as the proportion of warehouses operating as trade distribution hubs begins to shift in favor of consumer fulfillment centers.

UK government has a major influence on fuel prices, and both fuel duty and VAT (standard 20% rate) make up majority of the petrol and diesel prices

- In August 2022, the oil price dropped under USD 100 and finished the month at USD 90.63 a barrel. Prices dropped further in 2023, and by May, a barrel of oil was down to USD 72.50. In March 2024, petrol prices in the UK averaged 150.1p per litre, the highest since November 2023. This is due to rising oil prices due to Middle East tensions and a weaker pound against the dollar. Although overall inflation has eased, petrol and diesel prices increased in March. Oil prices have since dropped after spiking following Israel's retaliatory attack on Iran in April 2024.

- In June 2024, the UK government confirmed it plans to require at least 10% sustainable aviation fuel (SAF) in jet fuel by 2030. Currently, SAF is scarce and more expensive than traditional fuels, making it challenging to increase its use in aviation. SAF represents less than 0.1% of jet fuel globally. The government's SAF mandate, pending legislative approval, is set to start in January 2025. This follows the 2022 "Jet Zero" strategy aiming for net-zero emissions in aviation by 2050.

United Kingdom Road Freight Transport Industry Overview

The United Kingdom Road Freight Transport Market is fragmented, with the major five players in this market being Culina Group, DSV A/S (De Sammensluttede Vognmaend af Air and Sea), Gregory Distribution Ltd., Turners (Soham) Ltd. and Wincanton PLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 GDP Distribution By Economic Activity

- 4.2 GDP Growth By Economic Activity

- 4.3 Economic Performance And Profile

- 4.3.1 Trends in E-Commerce Industry

- 4.3.2 Trends in Manufacturing Industry

- 4.4 Transport And Storage Sector GDP

- 4.5 Logistics Performance

- 4.6 Length Of Roads

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Pricing Trends

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Major Truck Suppliers

- 4.13 Road Freight Tonnage Trends

- 4.14 Road Freight Pricing Trends

- 4.15 Modal Share

- 4.16 Inflation

- 4.17 Regulatory Framework

- 4.18 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 A.P. Moller - Maersk

- 6.4.2 Culina Group

- 6.4.3 DACHSER

- 6.4.4 Deutsche Bahn AG (including DB Schenker)

- 6.4.5 DHL Group

- 6.4.6 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.7 Gist Ltd.

- 6.4.8 Gregory Distribution Ltd.

- 6.4.9 Howard Tenens

- 6.4.10 Hoyer GmbH

- 6.4.11 Kinaxia Logistics Limited

- 6.4.12 Turners (Soham) Ltd.

- 6.4.13 United Parcel Service of America, Inc. (UPS)

- 6.4.14 W H Malcolm Ltd.

- 6.4.15 Wincanton PLC

7 KEY STRATEGIC QUESTIONS FOR ROAD FREIGHT CEOS

8 APPENDIX

- 8.1 Global Logistics Market Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate

公路貨運服務市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

公路貨運服務市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 中國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)亞太公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)北美跨國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印尼公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)德國公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)日本公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)東協公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)亞太公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)北美跨國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印尼公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)德國公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)日本公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)東協公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)