|

市場調查報告書

商品編碼

1692539

德國公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Germany Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

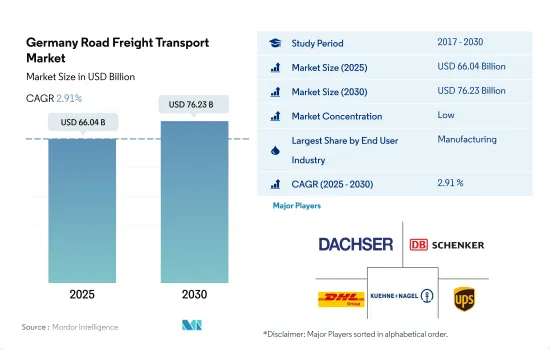

預計 2025 年德國公路貨運市場規模將達到 660.4 億美元,到 2030 年將達到 762.3 億美元,預測期間(2025-2030 年)的複合年成長率為 2.91%。

預計德國建築業產出將從 2024 年開始復甦,從而推動公路貨運服務的需求。

- 積層製造在世界各地越來越受歡迎。在歐洲,積層製造預計在 2023 年至 2030 年期間實現 20.7% 的複合年成長率。德國是歐洲最大的市場,預計未來幾年將成長高達 15%。多個行業正在推動成長要素,包括航太、醫療設備、運輸和汽車。近年來,積層製造已擴展到消費品和珠寶飾品等新的應用領域。隨著積層製造的發展,公路貨運的需求預計也會增加。

- 預計政府對基礎設施計劃的支出增加將推動建築終端用戶領域的成長。在交通運輸、可再生能源、住宅和製造業投資的支持下,建築業產出預計將從 2024 年開始復甦。此外,預計農產品出口的成長將支持農業、漁業和林業終端用戶領域。德國新聯合政府的目標是到 2030 年讓 30% 的可耕地採用有機農業方法管理,因此未來幾年有機農業產量可望增加。

德國公路貨運市場趨勢

德國是歐洲物流和運輸領域的領導者,對環保運輸方式的投資不斷增加。

- 2024年7月,德國政府啟動全國建置重型車輛快速充電網路的計劃。該舉措符合柏林到2045年實現碳中和運輸部門的宏偉目標。儘管溫室氣體排放預計將在2023年大幅下降,達到歐洲最大經濟體70年來的最低水平,但運輸部門仍在努力達到環境基準。德國的目標是到2030年,大約三分之一的重型道路運輸將實現電動化或使用合成甲烷或氫氣等電動燃料。

- 德國政府打算投資鐵路而不是公路,以促進環境保護、永續性和高效運輸。 2022 年,德國鐵路、聯邦政府和地方政府在鐵路基礎設施投資約 136 億歐元(145.1 億美元)。下薩克森州、漢堡州、不來梅州、梅克倫堡-前波美拉尼亞和石勒蘇益格-荷爾斯泰因州與德國鐵路公司共同投資,到 2030 年對其鐵路網路進行現代化改造。

歐洲維修季結束,德國E5汽油價格暴跌

- 2024年5月底,E5汽油價格較4月大幅下跌,最後一週下跌4.91美元/100公升。下降的原因是歐洲維護季節結束、煉油廠產量增加以及進口量增加。德國從阿姆斯特丹、鹿特丹和安特衛普進口的汽油一直在穩步成長,5月份德國港口接收汽油量為8,500桶/天,而出口量則下降至3,700桶/天。供應過剩和維護季節的結束導致德國 E5 汽油價格下跌。同時,柴油價格上漲導致南部和東部市場動盪。

- 德國消費者面臨物價上漲最快的局面,年通膨率高企主要是由於俄烏戰爭以來能源和食品價格的極端上漲。德國是世界上最大的天然氣進口國之一。約95%的天然氣消費量依賴進口來滿足。 2022年,55%的天然氣進口將來自俄羅斯,30%來自挪威,13%來自荷蘭。德國也預計,受歐盟排放權交易的影響,2027年燃料價格將大幅上漲。與2026年相比,2027年初,汽油價格將上漲每公升38美分,天然氣價格將上漲每度約3美分。

德國公路貨運業概況

德國公路貨運市場較為分散,市場上最大的五家參與者(按字母順序排列)為:DACHSER、德國鐵路股份公司(包括 DB Schenker)、DHL 集團、Kuehne+Nagel 和美國聯合包裹服務公司(UPS)。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 按經濟活動分類的GDP分佈

- 按經濟活動分類的GDP成長

- 經濟表現及概況

- 電子商務產業趨勢

- 製造業趨勢

- 交通運輸倉儲業GDP

- 物流績效

- 道路長度

- 出口趨勢

- 進口趨勢

- 燃油價格趨勢

- 卡車運輸成本

- 卡車持有量(按類型)

- 主要卡車供應商

- 公路貨運噸位趨勢

- 公路貨運價格趨勢

- 模態共享

- 通貨膨脹率

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 農業、漁業和林業

- 建設業

- 製造業

- 石油和天然氣、採礦和採石

- 批發和零售

- 其他

- 匯出目的地

- 國內貨運

- 國際貨運

- 卡車負載容量

- 整車裝載 (FTL)

- 零擔運輸 (LTL)

- 貨櫃運輸

- 貨櫃運輸

- 沒有容器

- 距離

- 遠距

- 短途運輸

- 產品成分

- 流體產品

- 固體貨物

- 溫度控制

- 非溫控

- 溫度控制

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- AP Moller-Maersk

- DACHSER

- Deutsche Bahn AG(including DB Schenker)

- DHL Group

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Expeditors International of Washington, Inc.

- Kuehne+Nagel

- Raben Group

- United Parcel Service of America, Inc.(UPS)

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 全球物流市場概覽

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(市場促進因素、限制因素、機會)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

- 外匯

簡介目錄

Product Code: 92356

The Germany Road Freight Transport Market size is estimated at 66.04 billion USD in 2025, and is expected to reach 76.23 billion USD by 2030, growing at a CAGR of 2.91% during the forecast period (2025-2030).

Construction output is expected to pick up from 2024 in Germany and drive the demand for road freight services

- Additive manufacturing is becoming more popular worldwide. In Europe, additive manufacturing is expected to record a CAGR of 20.7% between 2023 and 2030. Germany is the largest market in Europe and is expected to grow up to 15% in the coming years. Several industries, such as aerospace, medical devices, transportation, and automotive, are the main growth drivers. In the last few years, additive manufacturing has been extended to new applications like consumer goods and jewelry. With the growth of additive manufacturing, road freight demand is expected to increase as well.

- The increased government spending on infrastructure projects is expected to drive the growth of the construction end-user segment. Construction output is expected to pick up from 2024, supported by investments in the transport, renewable energy, housing, and manufacturing sectors. Moreover, the rise in agricultural exports is expected to support the agriculture, fishing, and forestry end-user segment. Organic agricultural production is expected to increase in the coming years as Germany's new coalition government aims to have 30% of the country's cultivated land under organic management by 2030.

Germany Road Freight Transport Market Trends

Germany leads European logistics and transportation, with rising investment initiatives focused on Eco-friendly mode of transport

- In July 2024, the German government initiated a nationwide project to establish a fast-charging network tailored for heavy-duty vehicles. This initiative aligns with Berlin's ambitious goal to achieve a carbon-neutral transport sector by 2045. Despite a notable drop in greenhouse gas emissions in 2023, marking a 70-year low for Europe's largest economy, the transport segment has struggled to hit its environmental benchmarks. Germany is targeting that roughly one-third of its heavy road haulage will be electrically powered or utilize electrically produced fuels like synthetic methane or hydrogen by 2030.

- The German government intends to invest more in rail than roads to promote environmental protection, sustainability, and effective transportation. In 2022, Deutsche Bahn, the federal government, and the local and regional governments invested roughly EUR 13.6 billion (USD 14.51 billion) in rail infrastructure. Lower Saxony, Hamburg, Bremen, Mecklenburg-Western Pomerania, and Schleswig-Holstein, together with DB, invested in modernizing their rail networks by 2030.

E5 gasoline prices in Germany dropped sharply due to end of maintenance season in Europe

- At the end of May 2024, E5 gasoline prices dropped significantly compared to April, with prices USD 4.91/100L lower in the last week. This decline is due to the end of the maintenance season in Europe, leading to increased refinery production and rising imports. Gasoline imports from Amsterdam-Rotterdam-Antwerp to Germany have steadily risen, with German seaports receiving 8,500 b/d in May, while exports fell to 3,700 b/d. The oversupply and end of maintenance season are driving down E5 gasoline prices in Germany. Meanwhile, diesel prices in the south and east are causing market disruptions.

- German consumers faced the fastest price rise, and the high annual inflation rate was primarily driven by extreme price increases for energy and groceries since the Russia-Ukraine War. Germany is among the world's biggest natural gas importers. Around 95% of its gas consumption is met by imports. In 2022, 55% of gas imports came from Russia, 30% from Norway, and 13% from the Netherlands. Moreover, Germany anticipates a fuel price jump from 2027 EU emissions trading. An increase of 38 cents per liter of petrol and around 3 cents per kilowatt hour of natural gas at the beginning of 2027 compared to 2026.

Germany Road Freight Transport Industry Overview

The Germany Road Freight Transport Market is fragmented, with the major five players in this market being DACHSER, Deutsche Bahn AG (including DB Schenker), DHL Group, Kuehne+Nagel and United Parcel Service of America, Inc. (UPS) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 GDP Distribution By Economic Activity

- 4.2 GDP Growth By Economic Activity

- 4.3 Economic Performance And Profile

- 4.3.1 Trends in E-Commerce Industry

- 4.3.2 Trends in Manufacturing Industry

- 4.4 Transport And Storage Sector GDP

- 4.5 Logistics Performance

- 4.6 Length Of Roads

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Pricing Trends

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Major Truck Suppliers

- 4.13 Road Freight Tonnage Trends

- 4.14 Road Freight Pricing Trends

- 4.15 Modal Share

- 4.16 Inflation

- 4.17 Regulatory Framework

- 4.18 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 A.P. Moller - Maersk

- 6.4.2 DACHSER

- 6.4.3 Deutsche Bahn AG (including DB Schenker)

- 6.4.4 DHL Group

- 6.4.5 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.6 Expeditors International of Washington, Inc.

- 6.4.7 Kuehne+Nagel

- 6.4.8 Raben Group

- 6.4.9 United Parcel Service of America, Inc. (UPS)

7 KEY STRATEGIC QUESTIONS FOR ROAD FREIGHT CEOS

8 APPENDIX

- 8.1 Global Logistics Market Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate

02-2729-4219

+886-2-2729-4219

公路貨運市場按服務類型、車輛類型、最終用途、貨物類型和所有權分類-2025-2032年全球預測

公路貨運市場按服務類型、車輛類型、最終用途、貨物類型和所有權分類-2025-2032年全球預測 2025年公路貨運全球市場報告

2025年公路貨運全球市場報告 日本公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

日本公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 道路貨物運輸的歐洲市場(2025年)

道路貨物運輸的歐洲市場(2025年) 公路貨運市場-全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、服務、應用、地區及競爭細分,2020-2030 年)

公路貨運市場-全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、服務、應用、地區及競爭細分,2020-2030 年) 2025-2033年日本公路貨運市場報告(依產品類型、目的地、貨車規格、貨櫃運輸、距離、溫度控制、最終用戶和地區)

2025-2033年日本公路貨運市場報告(依產品類型、目的地、貨車規格、貨櫃運輸、距離、溫度控制、最終用戶和地區) 公路貨運服務市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測中國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)亞太公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)

公路貨運服務市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測中國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)亞太公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)

▼