|

市場調查報告書

商品編碼

2072918

越南跨境電商物流:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Vietnam Cross-Border E-Commerce Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

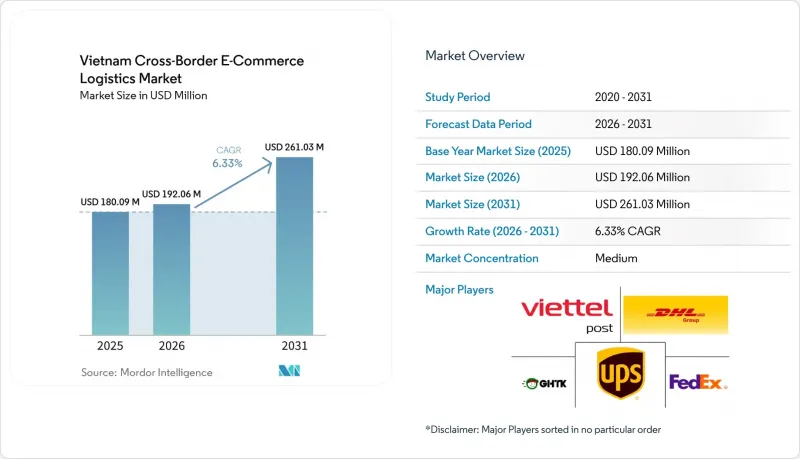

據 Mordor Intelligence 稱,越南跨境電子商務物流市場在 2025 年的價值為 1.8009 億美元,預計將從 2026 年的 1.9206 億美元成長到 2031 年的 2.6103 億美元,在預測期(2026-2031 年)的複合年成長率為 6.3%。

越南跨境電商物流市場正蓬勃發展,預計2025年,越南的貿易體系進出口總額將超過9,300億美元。同時,線上跨境貿易額仍維持在44.5億美元,顯示數位化跨境物流在越南整體貿易基礎中所佔佔有率仍然相對較小,這意味著該領域仍有巨大的成長空間。本報告按產品類型(食品飲料、個人護理、時尚等)、物流功能(運輸等)、經營模式(B2C、B2B、C2C)、配送速度(快遞、標準)以及物流流向(出口[北美、歐洲等]、進口[北美、歐洲等])進行細分。市場預測以美元計價。

越南跨境電商物流市場的趨勢與洞察

政策支持的跨境賣家生態系統正規化

2025年至2026年間,越南的法規環境從分散的規則體系轉變為更整合的框架。 《電子商務法(第122/2025/QH15號)》於2025年12月通過,並於2026年7月1日生效。該實施計劃也明確了各部會和地方政府在審查、培訓和製定相關法令方面的職責。此外,在法案起草過程中,透過課責外國平台在越南設立或指定法人實體,以履行課稅、爭議解決和消費者保護方面的義務,從而明確了跨境平台的責任。這項變更對越南跨境電商物流市場有重大影響,因為與合法市場相關的小包裹更有可能透過擁有可追溯系統的持牌業者運輸,而不是透過灰色通路網路運輸。這項政策週期也與《2026-2030年國家電子商務發展規劃》相聯繫,該規劃旨在支持數位基礎設施建設、改善物流以及提升跨境貿易透明度。因此,能夠將平台合規、海關單證和履約資料整合到單一營運體系中的承運商,在越南跨境電商物流市場中可能更具優勢。

市場主導的北亞進口小包裹擴張

越南的小包裹需求持續受到北亞供應與越南線上消費之間緊密聯繫的影響。官方行業數據顯示,越南跨境貿易規模與貿易總額相比仍然較小,這意味著即使平台主導的進口略有成長,隨著消費者使用量的增加,小包裹密度也可能迅速上升。針對低價值進口商品的新稅收措施也正在改變這些小包裹的配送方式。這是因為所有進口商品現在都需繳納增值稅(VAT),迫使企業實施更有系統的進口流程。這使得保稅倉庫和集中清關模式比僅處理零散的快遞更具吸引力,尤其是在處理大量小包裹時。實際上,如果大型企業能夠在不失去單據管理主導的前提下,預先部署庫存、進行集中清關並縮短配送時間,越南跨境電商物流市場將從中受益。

高昂的物流和逆向物流成本負擔

成本仍然是經銷商和物流供應商面臨的最明顯的營運限制因素之一。根據越南工商會(VCCI)提供的草案資料,跨境貨物的接收成本(包括關稅、增值稅和運輸費用)通常比國內庫存貨物高出30%至50%,這直接縮小了低價商品的競爭空間。越南的跨境電商物流市場在出口路線尤其脆弱。 「首公里」取貨(在河內和胡志明市以外地區)甚至在國際運輸開始之前就已經增加了成本。逆向物流更具挑戰性,因為國際退貨需要協調多個承運商、海關查核點和尚未標準化的當地檢驗程序。政府討論中已經提到,將附近的海外物流樞紐和保稅倉庫作為解決方案的一部分,這表明成本並非無關緊要的問題,而是一個結構性挑戰。在該網路成熟之前,越南的跨境電子商務物流市場對於低價值出口小包裹仍將效率低下,並將繼續依賴能夠將合規和處理成本分攤到大規模運輸池中的營運商。

細分市場分析

至2025年,消費性電器產品將佔越南跨境電商物流市場31.26%的佔有率,成為小批量跨境交易的主要收入來源。這一地位反映了其良好的業務特徵,包括相對較高的單價、重複購買需求以及與北亞製造業生態系統相契合的強大採購網路。在越南跨境電商物流市場中,電子產品也為清關、妥善處理和快速配送等服務提供了獲利空間。這是因為與基本生活必需品相比,消費者對物流履約的價格彈性較低。該品類與進口主導的需求高度契合。因此,家用電子電器不僅增加了物流量,而且在跨境前置作業時間至關重要的路線上,也對維持服務配置和配送路線密度發揮重要作用。這使得該品類對都市區門戶和保稅處理中心的網路設計具有顯著的影響力。

醫療保健、美容和個人護理是成長最快的產品類別,預計到2031年將以7.32%的複合年成長率成長。這表明未來的成長趨勢將從大宗電子設備的大宗購買轉向更頻繁、以品牌主導的小包裹運輸。越南的跨境電商物流市場正受益於此轉變,因為與體積較大的商品相比,美容相關小包裹通常密度較低、易於包裝,更適合重複的跨境訂單。因此,隨著需求從河內和胡志明市擴展到二線城市地區,這個類別對快遞服務的重要性日益凸顯。時尚和生活方式產業也繼續佔據重要的戰略地位,因為越南既是進口來源地,也是尋求直接進入國際市場的出口型經銷商的生產基地。相較之下,雖然家具單價高,但它也為越南的跨境電商物流業帶來了挑戰,包括退貨帶來的經濟負擔、損壞風險以及對海外倉庫的要求。由於食品和飲料行業需要遵守相關規定、保持產品質量,並且在某些情況下還需要進行溫度控制,因此其准入門檻比普通小包裹遞送行業更高,需要更專業的知識和技能。

到2025年,運輸業將佔越南跨境電商物流市場規模的67.94%,這印證了跨境實體運輸仍是該市場的核心。這並不令人意外,因為每一筆線上訂單都離不開幹線運輸、港口和機場裝卸以及最後一公里配送,之後才能提供高利潤服務。這個細分市場也反映了越南地處區域製造地和出口目的地之間的位置,這種結構性因素使得進出口路線的運輸需求始終居高不下。因此,在越南跨境電商物流市場中,運輸仍是決定時效性、路線經濟性和服務可靠性的關鍵要素。標準運輸也印證了這一點,因為大部分小包裹運輸仍然是以成本為導向,而不是以速度為導向。簡而言之,即使周邊服務日趨完善,運輸仍是該市場的基礎。

預計到2031年,附加價值服務將以11.50%的複合年成長率成長,成為越南跨境電商物流市場成長最快的功能領域。這表明,托運人和平台對綜合解決方案的需求日益成長,不再局限於基本的運輸服務,例如退貨處理、DDP和DDU選項、清關支援以及面向賣家的協調服務。官方政策方向也在推動這一發展,越南的物流發展藍圖呼籲增加對電商倉庫、數位化工具和綜合服務模式的投資。海關業務的數位化也推動了類似的趨勢,使能夠有效率地提交、管理和核對跨多個階段資料的服務提供者受益。隨著這些營運模式的普及,越南跨境電商物流業不再僅僅以貨物運輸為定義,而是以其將複雜的監管和營運流程轉化為實用服務的能力為核心。因此,儘管運輸目前仍佔據主導地位,附加價值服務未來很可能貢獻更大的利潤佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況及跨境電子商務物流在電子商務市場中的作用。

- 電子商務產業趨勢

- 消費者行為及供需分析

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 政策支持的跨境賣家生態系統的製度化

- 市場主導的北亞進口小包裹擴張

- 中小微型企業在家具和時尚產業的出口擴張

- 電子設備和美容相關小包裹的密度增加

- 將海關業務簡化為單一窗口,並利用保稅庫存。

- 跨境服務層在退貨、合規和 DDP/DDU 支援方面不斷成長。

- 市場限制因素

- 高昂的物流成本和逆向物流成本

- 目標市場中關稅、稅金和合規問題的複雜性。

- 取消低價值進口商品增值稅豁免

- 與大型物品退貨和損壞相關的經濟因素

- 技術創新前景

- 波特五力分析

- 跨境電子商務物流需求的變化

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模與成長預測

- 產品類型

- 食品/飲料

- 個人護理和居家護理

- 時尚與生活方式(配件、服裝、鞋類)

- 家具

- 家用電子電器和電器產品

- 其他產品

- 透過物流功能

- 運輸

- 道路運輸

- 航空

- 海路和內河航道

- 鐵路

- 倉儲、物流和庫存管理

- 附加價值服務及其他

- 運輸

- 按經營模式

- B2C

- B2B

- C2C

- 按配送速度

- 表達

- 標準

- 按流向

- 出口

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 南美洲

- 入境(進口)

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 南美洲

- 出口

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- SF Express(KEX-SF)

- Cainiao Network

- J&T Express

- Shopee Xpress(SPX Express)

- Viettel Post

- Giao Hang Nhanh(GHN)

- Vietnam Post(VNPost)

- FedEx

- United Parcel Service of America, Inc.(UPS)

- Lazada Logistics(LEX)

- BEST Express Vietnam

- Giao Hang Tiet Kiem(GHTK)

- Boxme Global

- CJ Logistics

- Kuehne+Nagel

- CMA CGM Group(Including CEVA Logistics)

- Janio Asia

- Nhat Tin Logistics(NTX)

- JD Logistics

- AP Moller-Maersk

第7章 市場機會與未來展望

According to Mordor Intelligence, the vietnam cross-border e-commerce logistics market size was valued at USD 180.09 million in 2025 and is estimated to grow from USD 192.06 million in 2026 to reach USD 261.03 million by 2031, at a CAGR of 6.33% during the forecast period (2026-2031).

The Vietnam cross-border e-commerce logistics market is expanding within a trade system that moved past USD 930 billion in total import and export turnover in 2025, while online cross-border trade remained at USD 4.45 billion, which shows that digital cross-border logistics still serves a relatively small share of Vietnam's wider trade base and therefore has room to deepen over time. This report is Segmented by Product Category (Foods and Beverages, Personal Care, Fashion, and More), by Logistics Function (Transportation, and More), by Business Model (B2C, B2B, C2C), by Delivery Speed (Express, Standard), and by Flow Direction (Outbound [North America, Europe, and More], Inbound [North America, Europe, and More]). The Market Forecasts are Provided in Value (USD).

Vietnam Cross-Border E-Commerce Logistics Market Trends and Insights

Policy-Backed Formalization of Cross-Border Seller Ecosystems

Vietnam's regulatory setting moved from scattered rules toward a more integrated framework across 2025 and 2026. The Law on E-Commerce No. 122/2025/QH15 was adopted in December 2025 and took effect on July 1, 2026, while the implementation plan assigns ministries and local authorities clear responsibilities for review, training, and follow-on decrees. The draft law process also made cross-border platform accountability more explicit by requiring foreign platforms to establish or authorize a legal entity in Vietnam for taxation, dispute handling, and consumer protection support. That change matters for the Vietnam cross-border e-commerce logistics market because parcel flows connected to formal marketplaces are more likely to move through licensed operators with traceable systems than through gray-channel networks. The same policy cycle is linked to the national e-commerce development plan for 2026 to 2030, which supports digital infrastructure, logistics improvement, and more transparent cross-border trade conditions. As a result, the Vietnam cross-border e-commerce logistics market is likely to favor carriers that can connect platform compliance, customs documentation, and fulfillment data into one operating stack.

Marketplace-Led Import Parcel Expansion from North Asia

Inbound parcel demand continues to be shaped by the close link between North Asian supply and Vietnamese online consumption. Official association material shows that Vietnam's online cross-border trade base remains small relative to total trade, which means even modest gains in platform-led imports can lift parcel density quickly when consumer adoption broadens. The new tax treatment for low-value imports also changes how these parcels move, because every inbound shipment now carries VAT handling obligations that push operators toward more structured import processes. This makes bonded and bulk-clearance models more attractive than fragmented express-only handling for very high parcel counts. In practice, the Vietnam cross-border e-commerce logistics market benefits when large operators can pre-position stock, clear in bulk, and shorten delivery windows without losing control over documentation.

High Logistics and Reverse-Logistics Cost Burden

Cost remains one of the clearest operating limits for sellers and logistics providers. VCCI material in the supplied draft states that cross-border goods often face landed costs that are 30%-50% higher than those for locally held inventory, once duties, VAT, and transport are included, which directly reduces the room to compete on low-ticket items. The Vietnam cross-border e-commerce logistics market is particularly exposed on export routes, where first-mile collection outside Hanoi and Ho Chi Minh City still adds cost before international transit even begins. Reverse logistics is even harder because international returns require coordination across multiple carriers, customs touchpoints, and local inspection steps that are not yet standardized. Government-linked discussions have already identified nearby overseas logistics hubs and bonded storage as part of the answer, indicating that the cost issue is not a marginal problem but a structural one. Until that network matures, the Vietnam cross-border e-commerce logistics market will remain less efficient for low-value export parcels and more reliant on operators that can spread compliance and handling costs across larger shipment pools.

Other drivers and restraints analyzed in the detailed report include:

- Export Scaling for Furniture and Fashion MSMEs

- Rising Electronics and Beauty Parcel Density

- Customs, Tax, and Destination-Market Compliance Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumer electronics and household appliances accounted for 31.26% of the Vietnam cross-border e-commerce logistics market in 2025, making the segment the main revenue driver for parcelized cross-border activity. This position reflects a favorable operating profile that combines relatively high unit values, repeat demand, and strong sourcing links with North Asian manufacturing ecosystems. In the Vietnam cross-border e-commerce logistics market, electronics also support better monetization for customs brokerage, careful handling, and faster delivery options, as buyers are less price-elastic in fulfillment than in basic commodity categories. The category fits well with import-driven demand. Consumer electronics, therefore, do more than add volume, because they help sustain service mix and route density in lanes where cross-border lead time matters. That role gives the segment an outsized influence on network design across urban gateways and bonded processing points.

Health, beauty, and personal care are the fastest-growing product categories, with a 7.32% CAGR through 2031, indicating that future growth is moving beyond large electronics baskets into more frequent, brand-led parcel flows. The Vietnam cross-border e-commerce logistics market benefits from this shift because beauty parcels are dense, easier to package, and often more compatible with repeat cross-border ordering than bulky goods are. That makes the category important for express services, especially when demand expands beyond Hanoi and Ho Chi Minh City into secondary urban centers. Fashion and lifestyle also remain strategically relevant, because Vietnam serves both as an import destination and as a production base for export-oriented sellers seeking direct international access. Furniture, by contrast, offers strong value per shipment but also exposes the Vietnam cross-border e-commerce logistics industry to more difficult return economics, damage risk, and overseas warehousing requirements. Foods and beverages add another specialized layer, because compliance, product integrity, and in some cases temperature control create higher entry barriers than those in standard parcel delivery.

Transport held 67.94% of the Vietnam cross-border e-commerce logistics market size in 2025, which confirms that physical movement across borders remains the core of the market. This is not surprising, because every digital order still depends on linehaul, port or airport handling, and last-mile execution before any higher-margin service can be sold. The segment also captures the effect of Vietnam's position between regional manufacturing centers and export destinations, which keeps transport demand structurally high across both import and export lanes. Within the Vietnam cross-border e-commerce logistics market, transport therefore remains the foundational function that determines timing, route economics, and service reliability. Standard delivery reinforces that point because a large portion of parcel volume still moves on cost-led rather than speed-led terms. In short, transport continues to anchor the market even as service sophistication around it rises.

Value-added services and others are projected to grow at an 11.50% CAGR through 2031, making it the fastest-moving functional area in the Vietnam cross-border e-commerce logistics market. This shows that shippers and platforms increasingly want integrated handling of returns, DDP and DDU choices, customs support, and seller-facing orchestration rather than basic movement alone. Official policy direction also supports that evolution, because the national logistics roadmap calls for stronger investment in e-commerce warehouses, digital tools, and integrated service models. Customs digitization strengthens the same trend by rewarding providers that can submit, manage, and reconcile data efficiently across multiple steps. As that operating model spreads, the Vietnam cross-border e-commerce logistics industry becomes less defined by freight movement alone and more by who can turn regulatory and operational complexity into a usable service layer. This is why transport still leads today, while value-added services are likely to capture more of the profit pool over time.

Complete Report Scope:

- By Product Category

- Foods and Beverages

- Personal and Household Care

- Fashion and Lifestyle (Accessories, Apparel, Footwear)

- Furniture

- Consumer Electronics and Household Appliances

- Other Products

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Business Model

- B2C

- B2B

- C2C

- By Delivery Speed

- Express

- Standard

- By Flow Direction

- Outbound (Exports)

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- South America

- Inbound (Imports)

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- South America

- Outbound (Exports)

List of Companies Covered in this Report:

- DHL Group

- SF Express (KEX-SF)

- Cainiao Network

- J&T Express

- Shopee Xpress (SPX Express)

- Viettel Post

- Giao Hang Nhanh (GHN)

- Vietnam Post (VNPost)

- FedEx

- United Parcel Service of America, Inc. (UPS)

- Lazada Logistics (LEX)

- BEST Express Vietnam

- Giao Hang Tiet Kiem (GHTK)

- Boxme Global

- CJ Logistics

- Kuehne+Nagel

- CMA CGM Group (Including CEVA Logistics)

- Janio Asia

- Nhat Tin Logistics (NTX)

- JD Logistics

- A.P. Moller - Maersk

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Cross-border E-commerce Logistics in E-commerce Market

- 4.2 Trends in E-Commerce Industry

- 4.3 Consumer Behavior and Demand-Supply Analysis

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Policy-Backed Formalization of Cross-Border Seller Ecosystems

- 4.6.2 Marketplace-Led Import Parcel Expansion from North Asia

- 4.6.3 Export Scaling for Furniture and Fashion MSMEs

- 4.6.4 Rising Electronics and Beauty Parcel Density

- 4.6.5 Single-Window Customs Digitization and Bonded Inventory Enablement

- 4.6.6 Cross-Border Service-Layer Growth in Returns, Compliance, and DDP/DDU Support

- 4.7 Market Restraints

- 4.7.1 High Logistics and Reverse-Logistics Cost Burden

- 4.7.2 Customs, Tax, and Destination-Market Compliance Complexity

- 4.7.3 Removal of Low-Value Import VAT Exemption

- 4.7.4 Bulky-Product Return and Damage Economics

- 4.8 Technology Innovations Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Rivalry Among Competitors

- 4.10 Evolution of Cross-border E-commerce Logistics Requirements

- 4.11 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Product Category

- 5.1.1 Foods and Beverages

- 5.1.2 Personal and Household Care

- 5.1.3 Fashion and Lifestyle (Accessories, Apparel, Footwear)

- 5.1.4 Furniture

- 5.1.5 Consumer Electronics and Household Appliances

- 5.1.6 Other Products

- 5.2 By Logistics Function

- 5.2.1 Transportation

- 5.2.1.1 Road

- 5.2.1.2 Air

- 5.2.1.3 Sea and Inland Waterways

- 5.2.1.4 Rail

- 5.2.2 Warehousing, Distribution and Inventory Management

- 5.2.3 Value-added Services and Others

- 5.2.1 Transportation

- 5.3 By Business Model

- 5.3.1 B2C

- 5.3.2 B2B

- 5.3.3 C2C

- 5.4 By Delivery Speed

- 5.4.1 Express

- 5.4.2 Standard

- 5.5 By Flow Direction

- 5.5.1 Outbound (Exports)

- 5.5.1.1 North America

- 5.5.1.2 Europe

- 5.5.1.3 Asia-Pacific

- 5.5.1.4 Middle East and Africa

- 5.5.1.5 South America

- 5.5.2 Inbound (Imports)

- 5.5.2.1 North America

- 5.5.2.2 Europe

- 5.5.2.3 Asia-Pacific

- 5.5.2.4 Middle East and Africa

- 5.5.2.5 South America

- 5.5.1 Outbound (Exports)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 SF Express (KEX-SF)

- 6.4.3 Cainiao Network

- 6.4.4 J&T Express

- 6.4.5 Shopee Xpress (SPX Express)

- 6.4.6 Viettel Post

- 6.4.7 Giao Hang Nhanh (GHN)

- 6.4.8 Vietnam Post (VNPost)

- 6.4.9 FedEx

- 6.4.10 United Parcel Service of America, Inc. (UPS)

- 6.4.11 Lazada Logistics (LEX)

- 6.4.12 BEST Express Vietnam

- 6.4.13 Giao Hang Tiet Kiem (GHTK)

- 6.4.14 Boxme Global

- 6.4.15 CJ Logistics

- 6.4.16 Kuehne+Nagel

- 6.4.17 CMA CGM Group (Including CEVA Logistics)

- 6.4.18 Janio Asia

- 6.4.19 Nhat Tin Logistics (NTX)

- 6.4.20 JD Logistics

- 6.4.21 A.P. Moller - Maersk

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

印度跨境B2C電子商務物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國跨境電子商務物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)越南跨境B2C電子商務物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度跨境電子商務物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)電子商務倉儲:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

印度跨境B2C電子商務物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國跨境電子商務物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)越南跨境B2C電子商務物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度跨境電子商務物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)電子商務倉儲:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 電子商務物流市場規模、佔有率和成長分析:按服務類型、模式、營運方式、產業和地區分類-2026-2033年產業預測

電子商務物流市場規模、佔有率和成長分析:按服務類型、模式、營運方式、產業和地區分類-2026-2033年產業預測 電子商務物流市場規模、佔有率、趨勢和預測:按產品類型、服務類型、業務領域和地區分類,2026-2034 年

電子商務物流市場規模、佔有率、趨勢和預測:按產品類型、服務類型、業務領域和地區分類,2026-2034 年 電子商務物流市場:依服務類型、供應商類型、營運模式、交付模式、經營模式、支付方式及最終用戶產業分類-2026-2032年全球市場預測

電子商務物流市場:依服務類型、供應商類型、營運模式、交付模式、經營模式、支付方式及最終用戶產業分類-2026-2032年全球市場預測 2026年全球跨境電子商務物流市場報告

2026年全球跨境電子商務物流市場報告 電子商務物流市場規模、市場佔有率和成長率;全球產業分析;按類型、應用和地區進行分析;以及未來預測(2026-2034 年)。

電子商務物流市場規模、市場佔有率和成長率;全球產業分析;按類型、應用和地區進行分析;以及未來預測(2026-2034 年)。