|

市場調查報告書

商品編碼

2072804

德國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Germany Combine Harvesters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

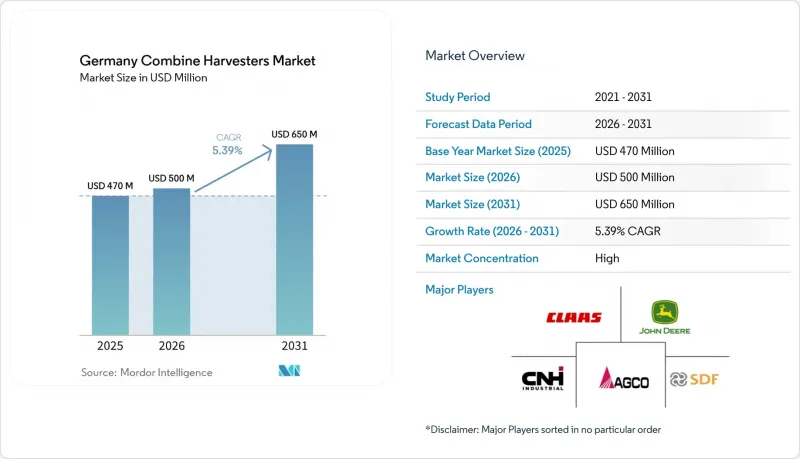

據 Mordor Intelligence 稱,2025 年德國聯合收割機市場價值 4.7 億美元,預計 2026 年將達到 5 億美元,2031 年將達到 6.5 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.39%。

本報告按產品類型(輪式聯合收割機、卡車式聯合收割機、混合動力聯合收割機)和功率輸出等級(200馬力以下、200-300馬力、200馬力以上)進行分類。市場預測以美元計價。

德國聯合收割機市場趨勢及洞察

歐盟第五階段排放氣體法規正在促使車輛更換。

新的顆粒物和氮氧化物排放標準將於2025年強制實施,屆時對老舊聯合收割機進行改造以符合新標準將不再經濟。為此,CLAAS於2023年10月開始在其位於哈爾斯溫克爾和勒芒的工廠生產的所有符合第五階段排放標準的聯合收割機中加註氫化植物油(HVO)100。這使得用戶在保持保固權益的同時,與化石柴油相比,二氧化碳排放量最多可減少90%。由於北美地區的產量有限,符合標準的進口車輛供應量也有限,有助於維持二手車的殘值,並促使買家盡快購買新車。第五階段排放法規透過加快更換週期、促進先進技術的應用以及支援德國聯合收割機市場的成長,正在推動長期需求。

勞動力短缺正在加速對自動化的需求。

隨著農業勞動力老化和季節性勞動力減少,自動化已成為採購標準的首要任務。根據2025年的初步數據,德國農業、林業和漁業部門的就業人數預計將減少3,000人,降幅為0.5%,總計56.2萬人。這一降幅凸顯了這些產業勞動力長期存在的結構性衰退。德國統一後整合了大規模土地的東德合作農場,在多班次收割季節面臨勞動力短缺的挑戰。 Dia公司的「預測地面速度自動化」和CNH公司的自主糧食處理系統,透過使經驗不足的員工能夠維持穩定的加工能力,幫助東德大型合作農場緩解人手不足。

高初始投資

對於德國聯合收割機市場而言,高昂的初始投資仍是一大限制因素。這提高了購買門檻,延長了投資回收期,並推遲了機器的更換,尤其對於中小農場而言更是如此。儘管德國繼續引領歐洲聯合收割機市場,但高昂的成本負擔正在抑制更換需求,並促使買家考慮融資、租賃或共用所有權模式,而非完全擁有。例如,到2025年,德國聯合收割機的價格將因型號和規格的不同而有很大差異,從約翰迪爾S7900的675,648美元到約翰迪爾T5500的318,435美元不等。對於一個150公頃的農場來說,擁有一台聯合收割機的成本相當於3到5年的淨利潤,這導致許多買家選擇以每小時200歐元(210美元)的價格簽訂租賃契約,進而擠壓了承包商的利潤空間。

細分市場分析

預計到2025年,輪式聯合收割機將在德國聯合收割機市場佔最大佔有率,達到52%。輪式聯合收割機的優點在於其能夠適應各種土壤條件,並且便於在田間和公路之間移動。它們適用於混合農業,且機動性相對較強,因此成為許多德國農民的實用之選。履帶式聯合收割機的市佔率相對較小,主要集中在德國南部丘陵地區。例如,CLAAS Lexion 8500於2025年7月上市,配備549馬力引擎和先進的懸吊系統,旨在減少在土壤鬆軟地區作業時的土壤壓實。

混合動力聯合收割機是成長最快的細分市場,預計2026年至2031年將以9.2%的複合年成長率成長。混合動力收割機的普及也惠及租賃企業,因為更低的油耗可以提高每小時的利潤率。隨著電池價格的下降,目的地設備製造商(OEM)計劃在2020年代中期推出混合動力收割機,預計到2031年,混合動力收割機在德國聯合收割機市場的佔有率將達到兩位數。更嚴格的排放氣體法規和對更高效收割解決方案的需求預計將進一步推動混合動力收割機的普及。此外,混合動力收割機在高生產力作業中表現更佳,這將使其對大規模商業農場更具吸引力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟第五階段排放氣體法規正在促使車輛更換。

- 勞動力短缺正在加速對自動化的需求。

- 由 Landwaldschaftich Rentenbank 提供的津貼貸款

- 精密農業的引進提高了大容量聯合收割機的投資報酬率 (ROI)。

- 隨著生質燃料原料作物種植面積的增加,需要專用的收割台。

- 使用氫化植物油(HVO)的引擎在其整個生命週期內可降低燃料成本。

- 市場限制因素

- 高初始投資

- 糧食價格波動給農民的現金流帶來了壓力。

- 各州新菸鹼類殺蟲劑法規的新進展

- 經銷商缺乏能夠操作先進電子設備的技術人員

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 輪式聯合收割機

- 履帶式聯合收割機

- 混合式聯合收割機

- 額定功率

- 不足200馬力

- 200~300 HP

- 300~400 HP

- 400馬力或以上

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CLAAS KGaA mbH

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- SDF SpA

- Kubota Corporation

- Rostselmash Joint-Stock Company

- Lovol Heavy Industry Co., Ltd.

- Yanmar Holdings Co., Ltd.

- Sampo-Rosenlew Oy

- Arbos Group SpA

- Buhler Industries Inc.

- Open Joint-Stock Company Gomselmash

- Zoomlion Heavy Industry Science & Technology Co., Ltd

- ISEKI & Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany combine harvesters market size was valued at USD 470 million in 2025 and is projected to reach USD 500 million in 2026 and USD 650 million by 2031, registering a CAGR of 5.39% between 2026 and 2031.

This report is Segmented by Product Type ( Wheel Combine Harvesters, Track Combine Harvesters, and Hybrid Combine Harvesters), and by Power Rating (Below 200 HP, 200 To 300 HP, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Combine Harvesters Market Trends and Insights

European Union Stage V Emission Norms Triggering Fleet Renewal

New particulate matter and nitrogen oxide thresholds that became mandatory in 2025 rendered older combines uneconomical to retrofit. CLAAS responded by factory-filling all Stage V combine manufactured at its Harsewinkel and Le Mans plants with Hydrotreated Vegetable Oil (HVO) 100 from October 2023, enabling operators to achieve up to 90% CO2 reduction compared to fossil diesel while maintaining warranty coverage . Tight North American output has limited the pool of compliant imports, sustaining residual values and encouraging buyers to secure new inventory quickly. Stage V norms serve as a long-term driver of demand by accelerating replacement cycles, promoting the adoption of advanced technology, and supporting growth in Germany's combine harvester market.

Labor Scarcity Accelerating Demand for Automation

An aging farm workforce and fewer seasonal operators have pushed automation to the top of procurement criteria. Preliminary data for 2025 indicates that employment in Germany's agriculture, forestry, and fishing sector declined by 3,000 individuals, representing a 0.5% decrease to a total of 562,000. This reduction highlights a long-term structural decline in the sector's workforce. Cooperative farms in Eastern Germany, which consolidated large landholdings following reunification, face staffing challenges during multi-shift harvest periods. Deere's Predictive Ground Speed Automation and CNH's autonomous grain cart system enable less-experienced staff to achieve consistent throughput, offsetting labor tightness in large eastern cooperatives.

High Upfront Capital Outlay

High upfront capital requirements remain a significant restraint on Germany's combine harvesters market, as they increase the purchase barrier, extend payback periods, and delay fleet renewal, particularly for small and medium-sized farms. While Germany continues to lead Europe's combine harvesters market, the high cost burden slows replacement demand and encourages buyers to explore financing, leasing, or shared-use models instead of outright ownership. For example, in 2025, combine harvesters prices in Germany vary significantly depending on the model and specifications, with listings ranging from USD 675,648 for a John Deere S7900 to USD 318,435 for a John Deere T5500. For a 150-hectare farm, ownership costs can equate to three to five years of net income, prompting many buyers to opt for rental contracts priced at EUR 200 (USD 210) per hour, which also compresses contractor margins.

Other drivers and restraints analyzed in the detailed report include:

- Subsidized Financing from Landwirtschaftliche Rentenbank

- Precision-Agriculture Adoption Improving Return of Investment (ROI) on High-Capacity Combine

- Grain-Price Volatility Squeezing Farm Cash Flow

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wheel combine harvesters accounted for the largest segment, 52% of the Germany combine harvesters market share in 2025. The dominance of wheel combine is attributed to their versatility across various soil conditions and ease of movement between fields and public roads. Their suitability for mixed farming operations and relatively straightforward mobility make them a practical choice for many German farmers. Track combine harvesters hold a smaller market share, primarily concentrated in Southern Germany's hilly terrain. For instance, CLAAS's Lexion 8500, introduced in July 2025, features a 549 HP engine and advanced suspension systems designed to reduce soil compaction in sensitive areas.

Hybrid combine harvesters are the fastest-growing segment, forecast to grow at a 9.2% CAGR from 2026 to 2031. Hybrid adoption also benefits rental fleets because lower fuel burn improves hourly margins. As battery prices drop, Original Equipment Manufacturers (OEMs) plan mid-decade rollouts that could lift the Germany combine harvesters market share for hybrids to double digits by 2031. Stricter emissions regulations and the demand for more efficient harvesting solutions are projected to drive adoption. Enhanced performance in high-output operations may also make hybrids more appealing to large commercial farms.

Complete Report Scope:

- By Product Type

- Wheel Combine Harvesters

- Track Combine Harvesters

- Hybrid Combine Harvesters

- By Power Rating

- Below 200 HP

- 200 to 300 HP

- 300 to 400 HP

- Above 400 HP

List of Companies Covered in this Report:

- CLAAS KGaA mbH

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- SDF S.p.A.

- Kubota Corporation

- Rostselmash Joint-Stock Company

- Lovol Heavy Industry Co., Ltd.

- Yanmar Holdings Co., Ltd.

- Sampo-Rosenlew Oy

- Arbos Group S.p.A.

- Buhler Industries Inc.

- Open Joint-Stock Company Gomselmash

- Zoomlion Heavy Industry Science & Technology Co., Ltd

- ISEKI & Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 European Union Stage V emission norms triggering fleet renewal

- 4.2.2 Labor scarcity accelerating demand for automation

- 4.2.3 Subsidized financing from Landwirtschaftliche Rentenbank

- 4.2.4 Precision-agriculture adoption is improving Return of Investment (ROI) on high-capacity combines

- 4.2.5 Rising biofuel-feedstock acreage needs specialty headers

- 4.2.6 Hydrotreated Vegetable Oil (HVO) ready engines lower lifecycle fuel costs

- 4.3 Market Restraints

- 4.3.1 High upfront capital outlay

- 4.3.2 Grain-price volatility is squeezing farm cash flow

- 4.3.3 Emerging state-level neonics restrictions

- 4.3.4 Shortage of dealer technicians for advanced electronics

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Wheel Combine Harvesters

- 5.1.2 Track Combine Harvesters

- 5.1.3 Hybrid Combine Harvesters

- 5.2 By Power Rating

- 5.2.1 Below 200 HP

- 5.2.2 200 to 300 HP

- 5.2.3 300 to 400 HP

- 5.2.4 Above 400 HP

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market-Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 CLAAS KGaA mbH

- 6.4.2 Deere & Company

- 6.4.3 CNH Industrial N.V.

- 6.4.4 AGCO Corporation

- 6.4.5 SDF S.p.A.

- 6.4.6 Kubota Corporation

- 6.4.7 Rostselmash Joint-Stock Company

- 6.4.8 Lovol Heavy Industry Co., Ltd.

- 6.4.9 Yanmar Holdings Co., Ltd.

- 6.4.10 Sampo-Rosenlew Oy

- 6.4.11 Arbos Group S.p.A.

- 6.4.12 Buhler Industries Inc.

- 6.4.13 Open Joint-Stock Company Gomselmash

- 6.4.14 Zoomlion Heavy Industry Science & Technology Co., Ltd

- 6.4.15 ISEKI & Co., Ltd.

7 Market Opportunities and Future Outlook

北美聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測

聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測 聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年法國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)英國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)動力輸出軸驅動式聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年法國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)英國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)動力輸出軸驅動式聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 聯合收割機市場:按類型和地區分類

聯合收割機市場:按類型和地區分類