|

市場調查報告書

商品編碼

2063929

動力輸出軸驅動式聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)PTO Powered Combine Harvesters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

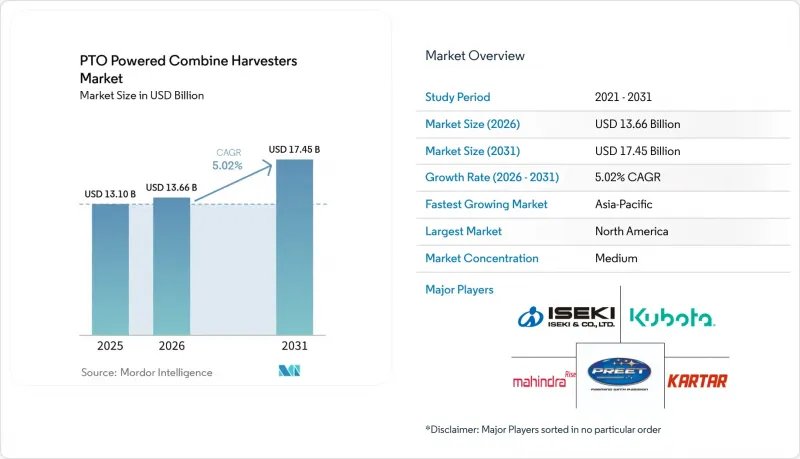

根據 Mordor Intelligence 預測,動力輸出軸驅動聯合收割機的市場規模預計將從 2025 年的 131 億美元和 2026 年的 136.6 億美元成長到 2031 年的 174.5 億美元,2026 年至 2031 年的複合年成長率為 5.02%。

本報告按以下類別分類:次類型(標準型、高容量型和特種作物型)、運輸方式(輪式和履帶式)、功率(150馬力以下、150-300馬力和300馬力以上)、應用領域(小麥、水稻及其他作物)以及地區(北美、南美、歐洲、亞太地區以及中東和非洲)。市場預測以美元計價。

全球動力輸出軸驅動聯合收割機市場趨勢及洞察

補貼主導的機械化計劃

在歐洲各地,農業機械化支援計畫和低利率農業投資方案旨在最大限度地減少資本投入,並促進引進與現有曳引機車隊相容的設備。在法國,歐洲投資基金和法國農業部於2025年5月擴大了「法國國家農業舉措」的規模。該舉措投資額超過20億歐元(22.7億美元),預計2028年將惠及超過15,000名農民。該融資計畫的重點是促進農業機械的投資和現代化改造,使農場和合作社能夠更好地獲得機械設備,同時降低引進收割設備的經濟門檻。

租賃車隊在南美洲的快速擴張

在整個南美洲,對農業機械租賃和合約收割服務的需求正在成長。這主要是由於農民越來越傾向於靈活使用機械而非擁有機械。季節性收割需求、農產品價格波動以及自走式機械的高昂購置成本等因素,正在推動共用和租賃營運模式的普及。透過利用租賃平台和外包機械化服務供應商,農民可以在收穫旺季最大限度地提高設備利用率,並在淡季最大限度地降低機械閒置成本。這種趨勢在尋求經濟高效且與曳引機相容的收割解決方案的中小糧食生產商中尤為明顯,從而導致區域農業市場對動力輸出軸驅動的聯合收割機的需求增加。

小規模農田農具與曳引機產量附件的限制

在小規模農戶眾多的地區,低馬力曳引機被廣泛使用,這限制了其與大型動力輸出軸(PTO)驅動式聯合收割機的作業兼容性,而後者需要高功率引擎才能穩定高效地運行。土地細分程度低和農業機械化程度不高,降低了投資高產能收割附件的經濟效益,尤其對中小農戶而言。在收割季節,農民往往依賴租賃的高馬力曳引機,這增加了營運成本,降低了動力輸出軸收割系統的成本效益。此外,專為低馬力曳引機設計的緊湊型動力輸出軸收割機通常處理能力較低,限制了高峰期的收割效率和面積覆蓋率。

細分市場分析

到2025年,標準型聯合收割機將佔據動力輸出軸驅動聯合收割機市場最大的佔有率,達到46%。該細分市場的優勢在於其與亞太、北美和歐洲混合穀物種植區廣泛使用的中馬力曳引機具有廣泛的兼容性。農民之所以青睞標準型聯合收割機,是因為它們擁有成本更低、維護更便捷,並且能夠與現有曳引機相容。此外,可改裝的精密農業系統和售後監測技術的日益普及,也提高了機器的使用壽命和作業效率。

從2026年到2031年,高產能細分市場預計將以7.6%的複合年成長率達到最高成長速度。這項需求成長主要得益於針對豆類、油籽和易碎穀物等作物專用收割系統的日益普及,這些系統能夠最大限度地減少收割過程中的穀物損傷。製造商不斷推出適應性強的脫粒系統、多樣化的分類技術以及適用於不同作物生長條件和細分農田的緊湊型收割附件。日益嚴重的勞動力短缺以及對減少收穫後損失的日益關注,正在推動專業農業應用領域的持續擴張。

到2025年,輪式聯合收割機將佔據動力輸出軸驅動聯合收割機市場62%的佔有率。其受歡迎的原因在於初始投資低、維護簡便,並且適用於主要糧食產區的乾旱土地條件。農民更青睞輪式聯合收割機,因為它們具有更優異的公路性能,並且能夠與現有的農業基礎設施相容。此外,與履帶式聯合收割機相比,輪式聯合收割機還具有零件供應充足、維護更簡單等優勢。懸吊系統和地形適應性的進步進一步提高了作業效率,同時保持了其在商業農業中的經濟性。

預計2026年至2031年間,履帶式收割機的年複合成長率將達到8.2%。這一成長主要得益於水稻種植環境中履帶式收割機的日益普及,因為在水稻種植環境中,提高牽引力和減少土壤壓實至關重要。水稻產區降雨量的波動和旱季的縮短,增加了能夠在複雜地形上作業的履帶式收割機的需求。水稻種植區的農民擴大採用履帶式收割機,以確保雨季期間的收割工作能夠持續運作,並最大限度地減少水稻田的收割損失。

區域分析

預計到2025年,北美將佔據動力輸出軸(PTO)驅動聯合收割機市場31.9%的佔有率。這一成長歸功於農業機械化的普及、曳引機的高普及率以及大規模區在收穫季節的強勁需求。美國和加拿大的農民正在擴大動力輸出軸收割系統的應用,以應對因天氣原因導致的收穫期縮短以及旺季作業期間出現的緊急收割需求。根據加拿大統計局預測,加拿大的小麥產量預計到2025年將達到3,496萬噸,這將推動商業性糧食生產中對機械化收割解決方案的需求。此外,租賃車輛的廣泛運作以及精密農業技術的日益普及也促進了全部區域收割設備的使用。

亞太市場預計將在2026年至2031年間以7.9%的複合年成長率(CAGR)實現最高成長,主要驅動力包括農業機械化程度的提高、農業勞動力短缺問題的日益嚴峻以及細分農業結構中曳引機兼容型收割系統的日益普及。印度和中國等國家持續推動農業機械化,旨在提高農業生產力並減少收穫後損失。主要農業經濟體的小規模農戶往往傾向於選擇與現有曳引機車隊相容的模組化、低成本收割解決方案。半自動、精密農業技術和小型收割平台的日益普及也推動了該地區的需求成長。水稻和小麥種植面積的不斷擴大也持續支撐著亞太農業市場對收割設備的長期需求。

在南美洲,隨著生產者尋求降低初始購置成本並靈活利用設備以適應不同季節的種植週期,以承包商為基礎的收割和機械共用業務持續擴張。根據巴西國家糧食供應公司(CONAB)預測,該國2024-2025年度的糧食產量預計將達到創紀錄的3.502億噸,這將推動全部區域對機械化收割能力的需求成長。為了因應日益成長的季節性收割需求,租賃車隊營運商和農業服務供應商正在南美洲各地擴大與曳引機相容的收割系統的部署。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 補貼主導的機械化計劃

- 南美洲租車車隊的快速擴張

- 改進混合動力動力輸出軸傳動系統以降低油耗

- 用於預測性維護的物聯網套件作為售後市場產品銷售

- 適用於丘陵農場的緊湊型履帶式動力輸出軸收割機的出現。

- 低排放動力輸出裝置營運產生的排碳權收入

- 市場限制因素

- 小規模農田中附件與曳引機產量比例過高所帶來的限制。

- 熟練的聯合收割機動力輸出裝置操作員短缺

- 季節性運作是導致投資報酬率下降的因素。

- 變速箱零件進口關稅

- 波特五力模型

第5章 市場規模與成長預測

- 按子類型

- 標準型

- 高容量型

- 用於特殊作物

- 透過運輸方式

- 帶輪子的

- 爬行型

- 依輸出類型

- 150馬力或以下

- 150~300HP

- 300馬力或以上

- 透過使用

- 小麥

- 米

- 大豆

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 中東

- 土耳其

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Kubota Corporation

- ISEKI & CO., LTD.

- Mahindra & Mahindra Ltd.

- Kartar Agro Industries Private Limited

- Preet Agro Industries Private Limited

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- CLAAS KGaA mbH

- SDF SpA

- Yanmar Holdings Co., Ltd.

- Zoomlion Heavy Industry Science and Technology Co., Ltd.

- Rostselmash JSC

- International Tractors Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the pTO powered combine harvester market size is projected to grow from USD 13.10 billion in 2025 and USD 13.66 billion in 2026, to USD 17.45 billion by 2031, registering a CAGR of 5.02% from 2026 to 2031.

This report is Segmented by Sub-Type (Standard, High-Capacity, and Specialty-Crop), by Movement Type (Wheel and Crawler), by Power Output (Below 150 HP, 150-300 HP, and Above 300 HP), by Application (Wheat, Rice, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global PTO Powered Combine Harvesters Market Trends and Insights

Subsidy-Led Mechanization Programs

Farm mechanization support programs and low-interest agricultural investment schemes across Europe are promoting the adoption of equipment compatible with existing tractor fleets, aiming to minimize capital expenditure. In France, the European Investment Fund and the French Ministry of Agriculture expanded the National Initiative for French Agriculture in May 2025. This initiative, with an investment volume exceeding EUR 2 billion (USD 2.27 billion), is projected to support over 15,000 farmers by 2028 . The financing program focuses on enhancing agricultural equipment investment and modernization, enabling farms and cooperatives to improve access to machinery while reducing financial barriers to adopting harvesting equipment.

Rapid Rental-Fleet Penetration in South America

The demand for agricultural machinery rental and contractor-based harvesting services is growing across South America as farmers increasingly prioritize flexible equipment access over ownership. Factors such as seasonal harvesting needs, fluctuating commodity prices, and the high acquisition costs of self-propelled machinery are driving the adoption of shared-utilization and lease-based operating models. Rental platforms and outsourced mechanized service providers allow farms to maximize equipment usage during peak harvest periods while minimizing idle machinery costs during off-seasons. This trend is particularly prominent among small and medium-sized grain producers seeking cost-effective, tractor-compatible harvesting solutions, thereby boosting the demand for PTO powered combine harvesters in the regional agricultural market.

High Attachment-to-Tractor Power-Ratio Limits on Small Plots

The prevalent use of low-horsepower tractors in smallholder farming regions restricts the operational compatibility of larger PTO powered combine harvesters, which require higher engine output for stable and efficient performance. Fragmented landholdings and limited farm mechanization reduce the economic viability of investing in high-capacity harvesting attachments, particularly for small and medium-sized farmers. During harvesting periods, farmers often depend on rented higher-horsepower tractors, which increases operational costs and diminishes the cost benefits of PTO based harvesting systems. Furthermore, compact PTO harvester models designed for low-horsepower tractors generally offer lower throughput, limiting harvesting efficiency and acreage coverage during peak agricultural seasons.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid PTO Driveline Retrofits that Cut Fuel

- Predictive-Maintenance IoT Kits Sold as Aftermarket

- Import Tariffs on Gearbox Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The standard segment accounted for the largest 46% share of the PTO powered combine harvester market in 2025. This segment benefits from broad compatibility with medium-horsepower tractors, which are widely used in mixed-grain farming regions across Asia-Pacific, North America, and Europe. Farmers prefer standard models due to their lower ownership costs, ease of maintenance, and compatibility with existing tractor fleets. Additionally, the growing availability of retrofit precision farming systems and aftermarket monitoring technologies is enhancing machinery lifecycles and operational efficiency.

The high-capacity segment is projected to grow at the fastest CAGR of 7.6% from 2026 to 2031. Demand growth is supported by rising adoption of crop-specific harvesting systems for pulses, oilseeds, and fragile grains that minimize grain damage during harvesting operations. Manufacturers are increasingly introducing adjustable threshing systems, variable cleaning technologies, and compact harvesting attachments suitable for diverse crop conditions and fragmented agricultural fields. Growing labor shortages and increasing focus on reducing post-harvest losses continue to strengthen adoption across specialty agricultural applications.

Wheel systems accounted for 62% of the PTO powered combine harvester market share in 2025. Their widespread adoption is attributed to lower acquisition costs, easier servicing requirements, and suitability for dryland farming conditions in major grain-producing regions. Farmers prefer wheel systems due to their superior road mobility and compatibility with existing agricultural infrastructure. Additionally, the segment benefits from the strong availability of replacement parts and lower maintenance complexity than tracked systems. Advances in suspension systems and terrain adaptability are further enhancing operational efficiency while preserving affordability for commercial farming operations.

Crawler systems are projected to grow at a CAGR of 8.2% from 2026 to 2031. This growth is driven by increasing adoption in wet-field agricultural conditions, where improved traction and reduced soil compaction are critical. Variability in rainfall and shorter field-drying periods in rice-producing regions are boosting demand for tracked harvesting systems capable of operating in challenging terrain. Farmers in paddy cultivation areas are increasingly adopting crawler systems to ensure harvesting continuity and minimize field losses during monsoon seasons.

Geography Analysis

North America is projected to account for 31.9% of the PTO-powered combine harvester market share in 2025. This growth is attributed to extensive farm mechanization, high tractor penetration, and strong seasonal demand for harvesting in large grain-producing regions. Farmers in the United States and Canada are increasingly adopting PTO harvesting systems to address contingency harvesting needs during compressed weather windows and peak seasonal operations. According to Statistics Canada, Canada's wheat production reached 34.96 million metric tons in 2025, driving demand for mechanized harvesting solutions in commercial grain operations. Additionally, strong rental fleet activity and the growing adoption of precision agriculture technologies are supporting the utilization of harvesting equipment across the regional agricultural sector.

The Asia-Pacific market is projected to grow at the fastest 7.9% CAGR from 2026 to 2031 due to expanding farm mechanization, rising agricultural labor shortages, and increasing adoption of tractor-compatible harvesting systems across fragmented farming structures. Countries such as India and China continue to promote mechanized farming practices to improve agricultural productivity and reduce post-harvest losses. Smaller landholdings in major agricultural economies favor modular and lower-cost harvesting solutions compatible with existing tractor fleets. The growing adoption of semiautonomous controls, precision farming technologies, and compact harvesting platforms is also strengthening regional demand. Expanding rice and wheat cultivation areas continue to support long-term harvesting equipment adoption across Asia-Pacific agricultural markets.

South America continues to witness increasing adoption of contractor-based harvesting and machinery-sharing operations as growers seek lower upfront ownership costs and flexible equipment access during seasonal crop cycles. Brazil's cereal production reached a record 350.2 million metric tons in the 2024-25 harvest season, according to Companhia Nacional de Abastecimento (CONAB), strengthening demand for mechanized harvesting capacity across major grain-producing regions . Rising seasonal harvesting demand is encouraging rental fleet operators and agricultural service providers to expand the deployment of tractor-compatible harvesting systems across South America.

- Kubota Corporation

- ISEKI & CO., LTD.

- Mahindra & Mahindra Ltd.

- Kartar Agro Industries Private Limited

- Preet Agro Industries Private Limited

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- CLAAS KGaA mbH

- SDF S.p.A.

- Yanmar Holdings Co., Ltd.

- Zoomlion Heavy Industry Science and Technology Co., Ltd.

- Rostselmash JSC

- International Tractors Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subsidy-led mechanization programs

- 4.2.2 Rapid rental-fleet penetration in South America

- 4.2.3 Hybrid PTO driveline retrofits that cut fuel

- 4.2.4 Predictive-maintenance IoT kits sold as aftermarket

- 4.2.5 Emergence of compact crawler PTO harvesters for hilly farms

- 4.2.6 Carbon-credit income for low-emission PTO operations

- 4.3 Market Restraints

- 4.3.1 High attachment-to-tractor power-ratio limits on small plots

- 4.3.2 Scarcity of trained PTO-combine operators

- 4.3.3 Seasonal idle time driving low return-on-investment

- 4.3.4 Import tariffs on gearbox components

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Sub-Type

- 5.1.1 Standard

- 5.1.2 High-Capacity

- 5.1.3 Specialty-Crop

- 5.2 By Movement Type

- 5.2.1 Wheel

- 5.2.2 Crawler

- 5.3 By Power Output

- 5.3.1 Below 150 HP

- 5.3.2 150-300 HP

- 5.3.3 Above 300 HP

- 5.4 By Application

- 5.4.1 Wheat

- 5.4.2 Rice

- 5.4.3 Soybean

- 5.4.4 Other Crops

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Kubota Corporation

- 6.4.2 ISEKI & CO., LTD.

- 6.4.3 Mahindra & Mahindra Ltd.

- 6.4.4 Kartar Agro Industries Private Limited

- 6.4.5 Preet Agro Industries Private Limited

- 6.4.6 Deere & Company

- 6.4.7 CNH Industrial N.V.

- 6.4.8 AGCO Corporation

- 6.4.9 CLAAS KGaA mbH

- 6.4.10 SDF S.p.A.

- 6.4.11 Yanmar Holdings Co., Ltd.

- 6.4.12 Zoomlion Heavy Industry Science and Technology Co., Ltd.

- 6.4.13 Rostselmash JSC

- 6.4.14 International Tractors Limited

7 Market Opportunities and Future Outlook

聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測

聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測 聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年

聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年 英國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

英國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 聯合收割機市場:按類型和地區分類

聯合收割機市場:按類型和地區分類 多功能大豆聯合收割機市場預測至2034年-按類型、功能、動力來源、銷售管道、應用和地區分類的全球分析

多功能大豆聯合收割機市場預測至2034年-按類型、功能、動力來源、銷售管道、應用和地區分類的全球分析 聯合收割機市場報告:按類型、驅動類型、切割寬度、產量、應用和地區分類,2026-2034年

聯合收割機市場報告:按類型、驅動類型、切割寬度、產量、應用和地區分類,2026-2034年 2026-2030年全球聯合收割機市場複合材料鐵路車輪市場:按產品類型、安裝方式、材料、表面處理、塗層、應用類型和最終用戶分類,全球預測,2026-2032年

2026-2030年全球聯合收割機市場複合材料鐵路車輪市場:按產品類型、安裝方式、材料、表面處理、塗層、應用類型和最終用戶分類,全球預測,2026-2032年