|

市場調查報告書

商品編碼

2063975

中國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Combine Harvesters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

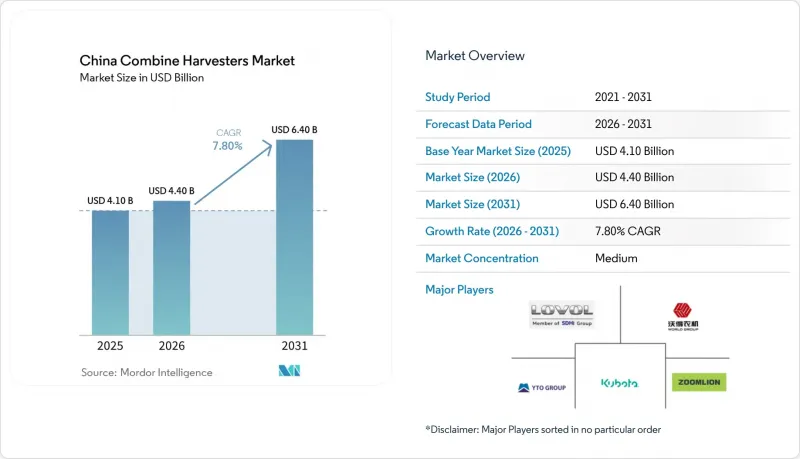

根據 Mordor Intelligence 預測,中國聯合收割機市場規模預計在 2025 年達到 41 億美元,2026 年達到 44 億美元,到 2031 年達到 64 億美元,2026 年至 2031 年的複合年成長率為 7.8%。

本報告按類型(自走式、曳引機牽引式、動力輸出軸驅動式模組化聯合收割機)、功率輸出範圍(120馬力以下、120-200馬力、201-300馬力及以上)和發展趨勢(輪式和履帶式)進行分類。市場預測以美元計價。

中國聯合收割機市場趨勢及洞察

透過補貼促進機械化

中國2026年農業機械採購基金將增加至33.3億美元,較2024年成長10.7%。此外,高產量聯合收割機的補貼率已從傳統機型的30%提高到35%至40%。陝西省將每秒處理能力6公斤的履帶式聯合收割機的補貼上限從5,250美元提高到6,300美元,加快了切向滾筒式收割機的淘汰。棉花收割機現在可享有11200美元的補貼,顯示補貼範圍擴大到主要糧食作物以外。 2024-2026年產品目錄規定,必須安裝北斗接收器和損失感測器才能獲得補貼,這迫使製造商統一遠端資訊處理功能。在黑龍江省,北斗導航收割機已覆蓋65萬公頃農田,減少了高達12%的重複作業浪費。江蘇省農業合作社引進了3000台配備即時產量測繪功能的收割機,用於實施變數施肥。這一系列政策將250馬力收割機的投資回收期從六年縮短至四年,直接提高了年出貨量,並加速了設備更新換代速度。

農村地區勞動力短缺和人事費用上升

農村地區60歲及以上居民的比例從2005年的9.55%上升到2021年的18.57%,預計到2030年將達到30%。到2024年,陸豐市人工收割工人的日薪將上漲至17美元,比2020年增加35%。機械化服務的成本為每0.067公頃8至11美元,這意味著小規模農戶每0.067公頃可淨節省42美元。目前,全國有1,170萬名持證收割機操作員,而機械操作員則有5,010萬名,顯示技能差距正在擴大。河北省文安合作社為15台聯合收割機加裝了鋸齒篩,減少了0.85%的糧食損失。在內蒙古奈曼旗,75133.3公頃土地已整合為452個合作社,40台聯合收割機組成的作業隊伍,每台可收割600公頃土地。由於農民的平均年齡超過55歲,加上年輕勞動力因遷移到都市區而減少,機械化已成為應對人事費用飆升的唯一現實解決方案。

引進機械設備成本高昂,資金不足。

200-300馬力的自走式聯合收割機在補貼前售價為28,000美元至49,000美元,相當於一個耕種1.33公頃農田的家庭3-5年的淨農業收入。補貼償還期限最長可達購機後6個月,迫使農民依賴過渡貸款。農村信用社提供的貸款利率為4.5%-6.0%,但抵押要求使得多達一半的申請者無法獲得貸款。鄭州中聯公司生產的4LZ-9B型聯合收割機的標價為25,200美元至30,800美元,但即使獲得6,800美元的補貼,實際支出仍比家庭平均可支配收入高出40%。租賃率低於15%,遠低於北美40%的租賃率。濰柴樂沃旗下的飛迪租賃和中聯重科金融均提供24個月分期付款方案,首付4200美元,月供1100美元,但車輛利用率仍低於10%。對於馬力超過300匹的車型,價格更是高達8.4萬美元,負擔也更重。因此,由於資金限制,車輛更換速度緩慢,尤其是在試點區域以外的地區。

細分市場分析

到2025年,自走式聯合收割機將佔中國聯合收割機市場64%的佔有率,成為最大的市場佔有率。其寬敞的駕駛室和較低的振動使其成為老年操作員的首選。雙軸流式設計可將損耗控制在1.2%以內,與切向滾筒系統相比,處理能力提高15-20%。半餵入式稻米收割機的處理能力雖然比自走式低40%,但在稻田中仍廣泛使用,因為稻草需要完整保留。預計到2031年,曳引式聯合收割機市場將以8.9%的複合年成長率成長,超過其他細分市場。這是因為價格在11,200美元至16,800美元之間的曳引機牽引式聯合收割機在四川省狹窄的梯田中仍然非常實用。在油菜和花生田中,由於專用收割機的成本效益不高,動力輸出軸模組化套件正被擴大採用。向自走式機械的轉變清楚地表明了中國聯合收割機市場將大部分研發資金投入了哪裡。

向自走式系統的轉變與智慧聯合收割機的補貼政策相契合。 2025年出貨的北斗系統收割機中,70%為工廠預裝而非後期改裝。管理300-800公頃土地的合作社最傾向於更換,因為較高的初始投資是合理的。曳引機牽引式收割機仍然支援入門級機械化,但其操作性差,令用戶望而卻步。模組化套件的優點在於可以靈活地安裝在現有曳引機上,但在小麥種植密集的田地中存在局限性。鑑於補貼趨勢和更嚴格的損失標準,中國聯合收割機市場正不可逆轉地底盤。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 透過補貼促進機械化

- 農村地區勞動力短缺和人事費用上升

- 國家糧食安全政策提高了糧食損失的標準。

- 對相容北斗系統的智慧能量採集器給予補貼和優惠待遇

- 政府對糧食採購中可接受的糧食損耗制定了更嚴格的標準。

- 土地整治試辦區域需要大馬力機械

- 市場限制因素

- 高昂的初始設備投資成本和信貸差異

- 土地碎片化限制了大型機械的使用。

- 由於收穫期縮短,導致季節性供應過剩

- 中國第六屆非道路柴油燃料相容性成本

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 自推進式

- 全進料軸流式

- 完全供應的切向鼓

- 半飼式水稻收割機

- 曳引機牽引式(拖曳式)

- PTO驅動模組化聯合收割機

- 自推進式

- 輸出功率範圍(馬力)

- 不到120馬力

- 120-200馬力

- 201-300馬力

- 超過300馬力

- 按趨勢

- 輪型

- 兩輪驅動

- 四輪驅動

- 爬行型

- 橡膠履帶履帶車

- 鋼履帶履帶車

- 輪型

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Weichai Lovol Intelligent Agricultural Technology CO., LTD

- Jiangsu World Agriculture Machinery Co., Ltd.

- China First Tractor Group(YTO Group)

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- KUBOTA Corporation

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- CLAAS KGaA mbH

- Shandong Shifeng Group

- Zhengzhou Zhonglian Harvest Machinery

- Zhejiang Liulin Agricultural Equipment

- Xingguang Agricultural Machinery

- Rostselmash

- Sampo Rosenlew

- Yanmar Co., Ltd.

- Shandong Wuzheng Group

- Preet Agro Industries

- Iseki & Co.

第7章 市場機會與未來展望

According to Mordor Intelligence, the china combine harvester market size expanded to USD 4.1 billion in 2025 and is projected to reach USD 4.4 billion in 2026, and USD 6.4 billion by 2031, growing at a CAGR of 7.8% from 2026 to 2031.

This report is Segmented by Type ( Self-Propelled, Tractor-Pulled, and PTO-Powered Modular Combines), by Power Range (Less Than 120 HP, 120-200 HP, 201-300 HP, and More), and by Movement ( Wheel Type and Crawler Type). The Market Forecasts are Provided in Terms of Value (USD).

China Combine Harvesters Market Trends and Insights

Subsidy-Backed Mechanization Push

China's 2026 machinery purchase fund grew to USD 3.33 billion, a 10.7% increase over 2024, and high-feed-rate combines now receive 35-40% reimbursement, up from 30% for legacy machines. Shaanxi lifted the subsidy ceiling for six-kilogram-per-second tracked models from USD 5,250 to USD 6,300, accelerating the retirement of tangential-drum units. Cotton pickers now qualify for USD 11,200, confirming that support extends beyond staple grains. The 2024-2026 catalog also links eligibility to BeiDou receivers and loss sensors, forcing manufacturers to bundle telematics. Heilongjiang deployed BeiDou-guided harvesters across 650,000 hectares, trimming overlap waste by up to 12%. Jiangsu cooperatives installed 3,000 units with live yield mapping, which informs variable-rate fertilization. This policy suite cuts payback from 6 to 4 years for 250-horsepower machines, directly boosting annual shipments and speeding up replacement cycles.

Rural Labor Shortage and Rising Wage Costs

The share of rural residents aged 60 and above climbed from 9.55% in 2005 to 18.57% in 2021 and is forecast to hit 30% by 2030. Daily wages for manual harvesters in Lufeng rose to USD 17 in 2024, up 35% from 2020. Mechanized services charge USD 8-11 per 0.067 hectares, resulting in a net saving of USD 42 per 0.067 hectares for smallholders. Certified harvester operators stand at 11.7 million, while the machinery workforce is 50.1 million, widening the skills gap. Wen'an Cooperative in Hebei retrofitted 15 combines with serrated sieves, reducing grain loss to 0.85%. Inner Mongolia's Naiman Banner consolidated 75,133.3 hectares into 452 cooperatives, allowing fleets of 40 combines to serve 600-hectare blocks. As the median farmer age surpasses 55 and urban migration drains young workers, mechanization becomes the only feasible hedge against escalating labor costs.

High Upfront Machine Cost and Credit Gaps

Self-propelled 200-300 horsepower combines cost USD 28,000-49,000 before subsidy, which is equivalent to three to five years of net farm income for households tilling 1.33 hectares. Subsidy reimbursement lags purchase by up to six months, forcing reliance on bridge loans. Rural credit unions charge 4.5-6.0% interest, yet collateral rules exclude up to half of applicants. Zhengzhou Zhonglian's 4LZ-9B lists at USD 25,200-30,800; after a USD 6,800 subsidy, the net outlay still exceeds the average household disposable income by 40%. Leasing penetration is below 15%, compared with 40% in North America. Weichai Lovol's Feidi Leasing and Zoomlion Financial offer 24-month plans with a USD 4,200 down payment and USD 1,100 monthly payments, yet uptake is under 10%. The burden is steeper for models with more than 300 horsepower, costing USD 84,000. Financial constraints, therefore, slow fleet renewal, especially outside pilot zones.

Other drivers and restraints analyzed in the detailed report include:

- National Food-Security Agenda Elevating Grain-Loss Standards

- BeiDou-Enabled Smart-Harvester Subsidy Incentives

- Fragmented Land Holdings Limit Large-Machine Utility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-propelled combines captured 64% of the China combine harvester market size in 2025, representing the largest share. Wider cabs and lower vibration make them the preferred choice for aging operators. Dual-axial-flow architectures meet the 1.2% loss ceiling and deliver 15-20% higher throughput than tangential drums. Half-feed rice persists in straw-retention paddies, though at a 40% throughput penalty. The tractor-pulled segment is projected to expand at a CAGR of 8.9% through 2031, outpacing other segments, as tractor-pulled units, priced at USD 11,200-16,800, remain relevant for Sichuan's narrow terraces. PTO modular kits are gaining traction in rapeseed and peanut plots where dedicated harvesters are uneconomical. The pivot to self-propelled machines underscores where the China combine harvester market will direct most R&D funding.

Self-propelled adoption also aligns with smart-harvester subsidies; 70% of BeiDou-equipped units shipped in 2025 were factory-installed rather than retrofitted. Replacement intent is strongest among cooperatives managing 300-800 hectares that can justify the higher outlay. Tractor-pulled models still anchor entry-level mechanization, yet a lack of comfort stalls operator interest. Modular kits benefit from flexible deployment on existing tractors but face limits in heavy wheat stands. Given subsidy bias and stricter loss norms, the China combine harvester market is tilting irrevocably toward high-spec self-propelled chassis.

List of Companies Covered in this Report:

- Weichai Lovol Intelligent Agricultural Technology CO., LTD

- Jiangsu World Agriculture Machinery Co., Ltd.

- China First Tractor Group (YTO Group)

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- KUBOTA Corporation

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- CLAAS KGaA mbH

- Shandong Shifeng Group

- Zhengzhou Zhonglian Harvest Machinery

- Zhejiang Liulin Agricultural Equipment

- Xingguang Agricultural Machinery

- Rostselmash

- Sampo Rosenlew

- Yanmar Co., Ltd.

- Shandong Wuzheng Group

- Preet Agro Industries

- Iseki & Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subsidy-backed mechanization push

- 4.2.2 Rural labor shortage and rising wage costs

- 4.2.3 National food-security agenda elevating grain-loss standards

- 4.2.4 BeiDou-enabled smart-harvester subsidy incentives

- 4.2.5 Stricter grain-loss quotas for state grain procurement

- 4.2.6 Land-consolidation pilot zones demanding high-HP machines

- 4.3 Market Restraints

- 4.3.1 High upfront machine cost and credit gaps

- 4.3.2 Fragmented land holdings limit large-machine utility

- 4.3.3 Harvest-window compression causing seasonal over-capacity

- 4.3.4 China VI non-road diesel compliance costs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Self-propelled

- 5.1.1.1 Full-feed axial-flow

- 5.1.1.2 Full-feed tangential-drum

- 5.1.1.3 Half-feed rice combines

- 5.1.2 Tractor-pulled (trailing)

- 5.1.3 PTO-powered modular combines

- 5.1.1 Self-propelled

- 5.2 By Power Range (HP)

- 5.2.1 Less than 120 HP

- 5.2.2 120 - 200 HP

- 5.2.3 201 - 300 HP

- 5.2.4 More than 300 HP

- 5.3 By Movement

- 5.3.1 Wheel Type

- 5.3.1.1 Two-wheel-drive

- 5.3.1.2 Four-wheel-drive

- 5.3.2 Crawler Type

- 5.3.2.1 Rubber-track crawlers

- 5.3.2.2 Steel-track crawlers

- 5.3.1 Wheel Type

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Weichai Lovol Intelligent Agricultural Technology CO., LTD

- 6.4.2 Jiangsu World Agriculture Machinery Co., Ltd.

- 6.4.3 China First Tractor Group (YTO Group)

- 6.4.4 Zoomlion Heavy Industry Science & Technology Co., Ltd.

- 6.4.5 KUBOTA Corporation

- 6.4.6 Deere & Company

- 6.4.7 CNH Industrial N.V.

- 6.4.8 AGCO Corporation

- 6.4.9 CLAAS KGaA mbH

- 6.4.10 Shandong Shifeng Group

- 6.4.11 Zhengzhou Zhonglian Harvest Machinery

- 6.4.12 Zhejiang Liulin Agricultural Equipment

- 6.4.13 Xingguang Agricultural Machinery

- 6.4.14 Rostselmash

- 6.4.15 Sampo Rosenlew

- 6.4.16 Yanmar Co., Ltd.

- 6.4.17 Shandong Wuzheng Group

- 6.4.18 Preet Agro Industries

- 6.4.19 Iseki & Co.

7 Market Opportunities and Future Outlook

聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測

聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測 聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年

聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年 英國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)動力輸出軸驅動式聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

英國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)動力輸出軸驅動式聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 聯合收割機市場:按類型和地區分類

聯合收割機市場:按類型和地區分類 多功能大豆聯合收割機市場預測至2034年-按類型、功能、動力來源、銷售管道、應用和地區分類的全球分析

多功能大豆聯合收割機市場預測至2034年-按類型、功能、動力來源、銷售管道、應用和地區分類的全球分析 聯合收割機市場報告:按類型、驅動類型、切割寬度、產量、應用和地區分類,2026-2034年

聯合收割機市場報告:按類型、驅動類型、切割寬度、產量、應用和地區分類,2026-2034年 2026-2030年全球聯合收割機市場複合材料鐵路車輪市場:按產品類型、安裝方式、材料、表面處理、塗層、應用類型和最終用戶分類,全球預測,2026-2032年

2026-2030年全球聯合收割機市場複合材料鐵路車輪市場:按產品類型、安裝方式、材料、表面處理、塗層、應用類型和最終用戶分類,全球預測,2026-2032年