|

市場調查報告書

商品編碼

2063927

英國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)United Kingdom Combined Harvester - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

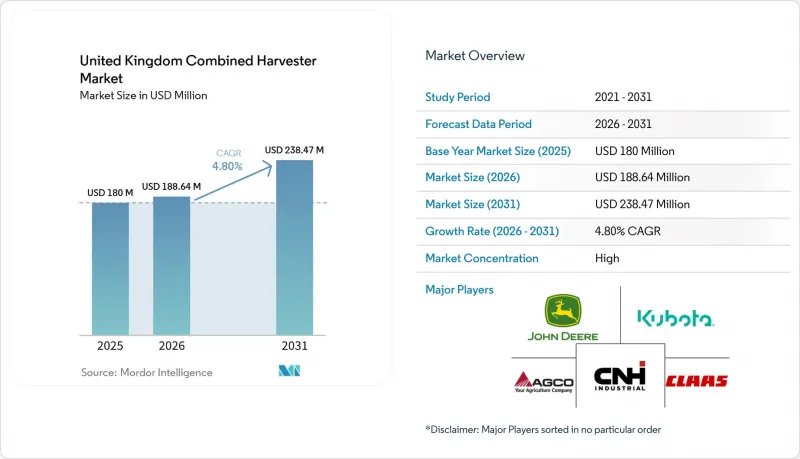

根據 Mordor Intelligence 預測,英國聯合收割機市場規模將從 2025 年的 1.8 億美元成長到 2026 年的 1.8864 億美元,到 2031 年將達到 2.3847 億美元,2026 年至 2031 年的複合年成長率為 4.8%。

本報告按產品類型(自走式聯合收割機和曳引機牽引式聯合收割機)、功率輸出(200馬力以下和以上)、技術(傳統技術和其他技術)、糧倉容量(8000公升以下、8001至12000公升和以上)以及最終用戶(大型商業農場和其他用戶)進行細分。市場預測以美元計價。

英國聯合收割機市場趨勢及洞察

老舊聯合收割機的更換需求

英國聯合收割機市場的更換需求正受到農場老舊收割機長期使用的影響。根據農業工程師協會預測,2024/25年度英國聯合收割機銷售量將降至280台,較前一年下降30%。新機銷售下降的原因在於農場盈利低迷,以及農民因農業收入波動而推遲資本投資。隨著農民延長現有聯合收割機的運作,預計全國範圍內對節能、高容量、技術先進的收割機的長期更換需求將會增加。

政府透過農業機械補貼提供支持

英國政府透過農業機械補貼推動英國收割機市場的機械現代化和精密農業的應用。據英國政府稱,2025年農業設備和技術基金提供的補貼金額從1,000英鎊(約1,340美元)到25,000英鎊(約3,3,500美元)不等。該計劃旨在推廣先進的農業技術,包括精密農業系統、作物監測工具以及聯合收割機自帶的除草和種子減量系統。政府的持續資助鼓勵農民和承包商投資於技術先進的收割設備和兼容精密農業的聯合收割機,從而提高作業效率、降低投入成本,並支持農業市場的永續農業實踐。

農作物價格波動會影響農民的收入。

農作物價格波動正在影響農民的盈利,並限制他們在英國聯合收割機市場的投資能力。根據布朗公司(Brown & Co.)的季度農業報告,英國飼料小麥的價格從2024年的每噸158英鎊(210.35美元)跌至2025年2月底的每噸178.30英鎊(212.18美元)。糧食價格下跌給糧食生產商的利潤率帶來了巨大壓力,尤其是在投入成本上升和農業收入不確定性增加的情況下。因此,許多農作物種植者正在推遲購買新的聯合收割機等資本密集型設備,並延長現有機械的運作。

細分市場分析

到2025年,自走式聯合收割機將佔據英國聯合收割機市場最大佔有率,達到67%。大規模商業農場和農業承包商更傾向於選擇自走式聯合收割機,因為它們在較短的收割季節中能夠提供更高的工作效率、更寬的收割寬度和更快的收割速度。大型農場尤其青睞自走式聯合收割機,以減少對勞動力的依賴並提高田間作業效率。這些機器擴大配備先進的自動化、遠端資訊處理和精密農業技術,從而提高了燃油效率並最大限度地減少了作物損失。此外,經銷商的大力支持和製造商提供的融資計劃也推動了對大容量自走式聯合收割機的持續成長需求。

預計2026年至2031年間,曳引機牽引式聯合收割機市場將以6.8%的複合年成長率(CAGR)高速成長。這一成長主要得益於中小農戶對經濟高效、初始投資成本更低的收割解決方案的需求不斷成長。對於糧食種植面積有限的農民而言,這些系統尤其具有吸引力,因為它們可以降低擁有成本,並為多樣化的農業經營提供柔軟性。此外,對二手農機市場和承包商收割服務的依賴也進一步推動了該細分市場的需求。同時,農場整合的趨勢也促使小規模農戶選擇更經濟實惠的收割方式,而不是投資大型自走式聯合收割機。

到2025年,馬力超過300匹的聯合收割機將佔據英國聯合收割機市場46%的佔有率。由於大馬力聯合收割機能夠提高收割速度、減少田間作業次數,並在較短的收割季節使用更寬的收割台,因此在大規模糧食農場和承包商中越來越受歡迎。在人手不足和天氣變化無常的情況下,快速收割作物至關重要,因此這些機器在綜合農業作業中也越來越受歡迎。配備自動化技術、大容量糧倉和精密農業系統的自走式聯合收割機的日益普及也推動了市場需求。高階聯合收割機仍然主要集中在商業農場和承包商手中,他們致力於最大限度地提高作業效率並最大限度地減少收割停機時間。

預計200馬力及以下的農機設備將達到最高成長,2026年至2031年的複合年成長率(CAGR)將達到7.3%。入門級聯合收割機持續吸引尋求更低擁有成本和更輕資金籌措的中小型農場,相比大型收割機而言,這些設備更具優勢。這些聯合收割機非常適合混合農業和小規模糧食種植,因為在這些情況下,投資大規模機械設備並不經濟。推動這一細分市場成長的因素還包括:對經濟實惠的收割解決方案的需求不斷成長、配備現代化功能的緊湊型機械設備的普及,以及越來越多的農民從人工或外包收割轉向機械化作業。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 老舊聯合收割機的更換需求

- 政府透過農業機械補貼提供支持

- 透過土地整合擴大平均農場面積

- 農業勞動力短缺和工資上漲

- 對適用於再生農業的收割機械的需求

- 製造商提供的融資降低了資本投資的門檻。

- 市場限制因素

- 農產品價格波動影響農民收入

- 與曳引機附件相比,其購置成本更高。

- 經銷商缺乏利用遠端資訊處理技術進行維護方面的專業知識。

- 英國脫歐後,對非歐洲機械設備的進口關稅提高

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 自走式聯合收割機

- 曳引機牽引式聯合收割機

- 額定功率

- 200馬力或以下

- 201~300 HP

- 超過300馬力

- 透過技術

- 傳統的

- 精準/智慧

- 按容量分類的糧倉容量

- 8,000 公升或以下

- 8,001~12,000 L

- 12,000 公升或更多

- 最終用戶

- 大型商業農場

- 中小農場

- 客製化招聘服務供應商

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- CLAAS KGaA mbH

- Kubota Corporation

- SAME DEUTZ-FAHR Italia SpA

- ISEKI & CO., LTD.

- Yanmar Holdings Co., Ltd.

- Rostselmash Ltd.

- Mahindra & Mahindra Limited

- Buhler Industries Inc.

- Gomselmash

- Ploeger Oxbo Group BV

- PREET TRACTORS PRIVATE LIMITED

- Tractors and Farm Equipment Limited(TAFE)

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom combined harvester market is projected to grow from USD 180.0 million in 2025 to USD 188.64 million in 2026 and USD 238.47 million by 2031, registering a CAGR of 4.8% between 2026 and 2031.

This report is Segmented by Product Type (Self-Propelled Combine Harvester and Tractor-Pulled Combine Harvester), by Power Rating (Up To 200 HP and More), by Technology (Conventional and More), by Grain Tank Capacity (Up To 8, 000 L, 8, 001-12, 000 L, and More), and by End User (Large-Scale Commercial Farms and More). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Combined Harvester Market Trends and Insights

Replacement Demand for Aging Combine Harvesters

Replacement demand in the United Kingdom's combined harvester market is being influenced by the prolonged use of older harvesting equipment on farms. According to the Agricultural Engineers Association, combine harvesters in the United Kingdom dropped to 280 units during the 2024/25 season, marking a 30% decrease compared to the previous season. This reduction in new machinery purchases is attributed to weak farm profitability and growers' postponed capital investments due to fluctuating agricultural returns. As farmers extend the operational lifespan of their existing combines, long-term replacement demand is anticipated to grow for more fuel-efficient, high-capacity, and technologically advanced harvesting equipment nationwide.

Government Support Through Farming Equipment Grants

Government support through agricultural equipment grants is driving machinery modernization and the adoption of precision farming in the United Kingdom's combined harvester market. According to the United Kingdom Government, the Farming Equipment and Technology Fund 2025 offers grants ranging from GBP 1,000 (USD 1,340) to GBP 25,000 (USD 33,500). This initiative promotes advanced agricultural technologies, including precision farming systems, crop-monitoring tools, and combine-mounted weed-seed-reduction systems. The continued availability of government-backed funding is encouraging farmers and contractors to invest in technologically advanced harvesting equipment and precision-compatible combine harvesters, enhancing operational efficiency, reducing input costs, and supporting sustainable farming practices within the agricultural market.

Fluctuating Crop Prices Affecting Farmer Income

Fluctuating crop prices are impacting farmer profitability and limiting investment capacity in the United Kingdom's combine harvester market. According to Brown & Co's Quarterly Agricultural Update, feed wheat prices in the United Kingdom fell to GBP 178.3 (USD 212.18) per metric ton by the end of Feb 2025, against GBP 158.0 (USD 210.35) in 2024. Declining grain prices have significantly reduced margins for cereal growers, particularly amid rising input costs and uncertain farm incomes. Consequently, many arable farmers are postponing capital-intensive purchases, such as new combine harvesters, and extending the operational lifespan of existing machinery.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Average Farm Size from Land Consolidation

- Farm Labor Shortages and Rising Wages

- High Purchase Cost Compared to Tractor Attachments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-propelled combine harvesters accounted for the largest 67% of the United Kingdom's combined harvester market share in 2025. Large commercial farms and agricultural contractors prefer self-propelled combines due to their higher operational efficiency, wider cutting capacity, and faster harvesting speeds during short crop collection periods. Adoption is particularly strong among consolidated farming estates aiming to reduce labor dependency and enhance field productivity. These machines increasingly feature advanced automation, telematics, and precision farming technologies, improving fuel efficiency and minimizing crop losses. Additionally, strong dealer support networks and manufacturer-backed financing programs are driving sustained demand for high-capacity self-propelled harvesting equipment.

The tractor-pulled combine harvesters market size is projected to grow at the fastest CAGR of 6.8% from 2026 to 2031. Growth is driven by increasing demand from small and medium-sized farms seeking cost-effective harvesting solutions with lower initial investment requirements. These systems are particularly appealing to growers managing limited cereal acreage, as they reduce ownership costs and offer flexibility for mixed-farming operations. The reliance on used machinery markets and contractor-supported harvesting services is further boosting demand in this segment. Additionally, trends in farm consolidation are encouraging smaller agricultural operators to adopt more affordable harvesting alternatives instead of investing in large self-propelled combine harvesters.

Above 300 HP held 46% of the United Kingdom's combined harvester market share in 2025. Large-scale cereal farms and contractor-operated harvesting fleets increasingly prefer high-horsepower combines because they improve harvesting speed, reduce field passes, and support wider headers during short harvesting windows. These machines are gaining traction across consolidated farming operations where labor shortages and weather variability require faster crop collection. Demand also benefits from rising adoption of self-propelled combines equipped with automation technologies, larger grain tanks, and precision farming systems. Premium combine models remain concentrated among commercial farms, and contractors focused on maximizing operational productivity and reducing harvesting downtime.

Up to 200 HP machines are anticipated to grow at the fastest 7.3% CAGR from 2026 to 2031. Entry-level combine harvesters continue attracting small and medium-sized farms seeking lower ownership costs and reduced financing burdens compared to larger harvesting equipment. These combines remain suitable for mixed-farming operations and smaller cereal acreage where high-capacity machinery is not economically viable. Growth in this segment is further supported by increasing demand for affordable harvesting solutions, the availability of compact machines with modern features, and expanding adoption among growers shifting from manual or contractor-based harvesting toward mechanized operations.

List of Companies Covered in this Report:

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- CLAAS KGaA mbH

- Kubota Corporation

- SAME DEUTZ-FAHR Italia S.p.A.

- ISEKI & CO., LTD.

- Yanmar Holdings Co., Ltd.

- Rostselmash Ltd.

- Mahindra & Mahindra Limited

- Buhler Industries Inc.

- Gomselmash

- Ploeger Oxbo Group B.V.

- PREET TRACTORS PRIVATE LIMITED

- Tractors and Farm Equipment Limited (TAFE)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Replacement demand for aging combine harvesters

- 4.2.2 Government support through farming equipment grants

- 4.2.3 Growth in average farm size from land consolidation

- 4.2.4 Farm labor shortages and rising wages

- 4.2.5 Demand for harvesters suited for regenerative farming

- 4.2.6 Manufacturer financing reducing equipment investment barriers

- 4.3 Market Restraints

- 4.3.1 Fluctuating crop prices affecting farmer income

- 4.3.2 High purchase cost compared to tractor attachments

- 4.3.3 Limited dealer expertise in telematics-based servicing

- 4.3.4 Rising import tariffs on non-European machinery after Brexit

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Self-Propelled Combine Harvesters

- 5.1.2 Tractor-Pulled Combine Harvesters

- 5.2 By Power Rating

- 5.2.1 Up to 200 HP

- 5.2.2 201-300 HP

- 5.2.3 Above 300 HP

- 5.3 By Technology

- 5.3.1 Conventional

- 5.3.2 Precision/Smart

- 5.4 By Grain Tank Capacity

- 5.4.1 Up to 8,000 L

- 5.4.2 8,001-12,000 L

- 5.4.3 Above 12,000 L

- 5.5 By End User

- 5.5.1 Large-Scale Commercial Farms

- 5.5.2 Small and Medium Farms

- 5.5.3 Custom Hiring Service Providers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Country Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 CLAAS KGaA mbH

- 6.4.5 Kubota Corporation

- 6.4.6 SAME DEUTZ-FAHR Italia S.p.A.

- 6.4.7 ISEKI & CO., LTD.

- 6.4.8 Yanmar Holdings Co., Ltd.

- 6.4.9 Rostselmash Ltd.

- 6.4.10 Mahindra & Mahindra Limited

- 6.4.11 Buhler Industries Inc.

- 6.4.12 Gomselmash

- 6.4.13 Ploeger Oxbo Group B.V.

- 6.4.14 PREET TRACTORS PRIVATE LIMITED

- 6.4.15 Tractors and Farm Equipment Limited (TAFE)

7 Market Opportunities and Future Outlook

聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測

聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測 聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年

聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年 中國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)動力輸出軸驅動式聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)動力輸出軸驅動式聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 聯合收割機市場:按類型和地區分類

聯合收割機市場:按類型和地區分類 多功能大豆聯合收割機市場預測至2034年-按類型、功能、動力來源、銷售管道、應用和地區分類的全球分析

多功能大豆聯合收割機市場預測至2034年-按類型、功能、動力來源、銷售管道、應用和地區分類的全球分析 聯合收割機市場報告:按類型、驅動類型、切割寬度、產量、應用和地區分類,2026-2034年

聯合收割機市場報告:按類型、驅動類型、切割寬度、產量、應用和地區分類,2026-2034年 2026-2030年全球聯合收割機市場複合材料鐵路車輪市場:按產品類型、安裝方式、材料、表面處理、塗層、應用類型和最終用戶分類,全球預測,2026-2032年

2026-2030年全球聯合收割機市場複合材料鐵路車輪市場:按產品類型、安裝方式、材料、表面處理、塗層、應用類型和最終用戶分類,全球預測,2026-2032年