|

市場調查報告書

商品編碼

2072716

歐洲聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe Combine Harvesters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

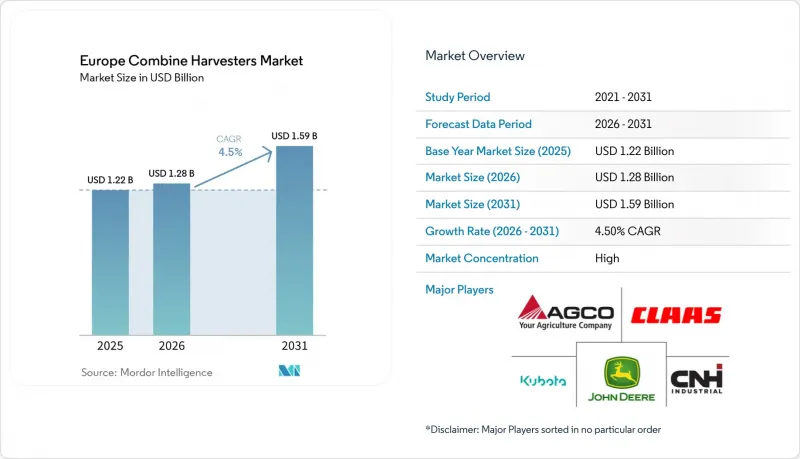

據 Mordor Intelligence 稱,2025 年歐洲聯合收割機市值為 12.2 億美元,2026 年為 12.8 億美元,預計到 2031 年將達到 15.9 億美元,在預測期(2026-2031 年)以 4.50% 的複合年成長率。

本報告按類型(自走式聯合收割機、曳引機牽引式聯合收割機、動力輸出軸驅動式聯合收割機)、功率輸出(150馬力以下、151-300馬力、301-450馬力、450馬力以上)和地區(德國、法國、英國、義大利等)進行分類。市場預測以美元計價。

歐洲聯合收割機市場趨勢及洞察

勞動力短缺和農業勞動成本上升

不斷上漲的農業勞動力成本和持續的勞動力短缺正在推動歐洲聯合收割機市場機械化的發展。據北愛爾蘭農業工資委員會稱,北愛爾蘭的農業工資計畫從2026年4月1日起上調,官方最低工資將根據年齡和等級的不同,設定為8至14.44英鎊(約10.80至19.49美元)。這些調整後的工資將適用於受北愛爾蘭《農業人事費用(監管)法》保護的農業工人。此外,歐盟統計局報告稱,2025年歐洲人事費用持續上漲,東歐工資水平正逐步接近西歐水平,波蘭和羅馬尼亞的工資漲幅分別為8.8%和10.6%。為了因應這些趨勢,農民正在大型農場投資購買聯合收割機,以提高收割效率,減少對季節性工人的依賴,並確保及時收割。

歐盟通用農業政策(CAP)對機械化的補貼

在通用下,財政支持計畫透過補貼發展中農業地區農機投資成本的很大一部分,降低了多個歐洲國家購買聯合收割機的門檻。波蘭於2025年擴大了其農業機械融資計劃,以鼓勵中大型農場增加設備購買和機械設備現代化改造。同樣,羅馬尼亞也增加了農業機械投資的核准津貼數量。然而,由於行政流程耗時,許多農民在獲得補貼前就必須依賴過渡貸款或商業貸款。補貼發放時間、資金籌措取得管道和貸款可用性的差異,持續影響歐洲聯合收割機市場的短期機械購買週期和更換需求模式。

大宗商品價格波動抑制了資本投資。

歐洲各地糧食和小麥價格的波動導致農場盈利和現金流出現不確定性,迫使農民推遲購買新的聯合收割機。根據歐盟委員會的《短期展望》,歐盟糧食產量預計在2025/26年度達到約2.8億噸,年增約4.1%。雖然這一成長有望改善供應狀況,但糧食價格仍將面臨壓力。儘管產量有所回升,但大宗商品價格下跌和農業獲利能力的不確定性抑制了農民購買昂貴收割設備的意願。因此,許多農民將重點放在控制營運成本上,而不是更換機械,導致歐洲聯合收割機市場訂單減少,資本投資決策也被推遲。

細分市場分析

預計到2025年,自走式聯合收割機將佔據歐洲聯合收割機市場78.3%的佔有率。這一主導地位得益於中大型農場對自走式聯合收割機的廣泛應用,因為自走式收割機將收割、脫粒和穀物分揀整合到單一作業中,顯著提高了收割效率。包括迪爾公司(Deere & Company)和克拉斯集團(Claas KGaA mbH)在內的領導企業正不斷改進自走式聯合收割機,為其配備GPS導航、精密農業技術和即時產量監測系統等功能。相較之下,動力輸出軸驅動式聯合收割機預計在2026年至2031年間達到最高的複合年成長率(CAGR),達到7.9%。這一成長主要歸功於波蘭和羅馬尼亞等東歐國家中小農場需求的不斷成長,這些國家的農民優先考慮初始投資少以及與現有曳引機基礎設施的兼容性。

此外,小型和中型聯合收割機的市場需求日益成長,以滿足小規模農場在降低擁有成本的同時實現收割機械化的需求。動力輸出軸驅動的聯合收割機因其維護相對簡單且能與現有曳引機柔軟性配合使用,仍是價格敏感型農戶的理想選擇。然而,由於收割效率低且缺乏先進的自動化技術,其在歐洲大型商業農場的普及程度受到限制。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 勞動力短缺和農業勞動成本上升

- 歐盟通用農業政策中的機械化補貼

- 第五階段排放氣體法規正在加速車輛的更新換代。

- 精密農業與遠端資訊處理的融合

- 引入履帶式聯合收割機以減少土壤壓實。

- 東歐農業機械共用所有製合作社的興起

- 市場限制因素

- 高昂的購置和維修成本

- 商品價格波動抑制了資本投資。

- 先進電子設備維修技術人員短缺

- 電網限制正在減緩電動車和混合動力汽車汽車的普及。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 自走式聯合收割機

- 曳引機牽引式聯合收割機

- 動力輸出軸驅動的聯合收割機

- 依輸出類型

- 小於150馬力

- 151~300 HP

- 301~450 HP

- 450馬力或以上

- 按地區

- 德國

- 法國

- 英國

- 義大利

- 波蘭

- 西班牙

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Claas KGaA mbH

- SDF SpA

- Kubota Corporation

- Mahindra & Mahindra Ltd.

- Rostselmash

- Yanmar Holdings Co., Ltd.

- Gomselmash

- ISEKI & CO.,LTD.

- Tera YatIrIm Teknoloji Holding AS(Sampo Rosenlew)

- Weichai Lovol Intelligent Agricultural Technology CO., LTD(SDHI Group)

- YTO Group Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe combine harvesters market size was valued at USD 1.22 billion in 2025 to USD 1.28 billion in 2026, and reach USD 1.59 billion by 2031, growing at a CAGR of 4.50% over the forecast period (2026-2031).

This report is Segmented by Type (Self-Propelled Combine, Tractor-Pulled Combine, and PTO-Powered Combine), by Power Output (Less Than 150 HP, 151 - 300 HP, 301 - 450 HP, and Above 450 HP), and by Geography (Germany, France, The United Kingdom, Italy, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Combine Harvesters Market Trends and Insights

Labor Shortage and Rising Farm-Labor Costs

Increasing agricultural labor costs and ongoing worker shortages are driving the adoption of mechanization in the European combine harvesters market. In Northern Ireland, agricultural wage rates are due to rise from 1 April 2026, with official minimum hourly rates set at (£8.00 to £14.44), about USD 10.80 to USD 19.49 depending on age and grade, according to the Agricultural Wages Board . These revised rates apply to agricultural workers covered under the Agricultural Wages (Regulation) Order in Northern Ireland. Additionally, Eurostat reported continued labor-cost inflation across Europe in 2025, with labor costs increasing by 8.8% in Poland and 10.6% in Romania, as wages in Eastern Europe gradually align with those in Western Europe. These developments are prompting farmers to invest in combine harvesters to improve harvesting efficiency, reduce reliance on seasonal labor, and ensure timely crop harvesting in large-scale farming operations.

EU Common Agricultural Policy Subsidies for Mechanization

Financial support programs under the Common Agricultural Policy are reducing purchasing barriers for combine harvesters in several European countries by subsidizing a significant portion of machinery investment costs in developing agricultural regions. Poland expanded its agricultural machinery financing programs in 2025, facilitating increased equipment purchases and fleet modernization among medium- and large-scale farms. Similarly, Romania increased grant approvals for agricultural machinery investments. However, lengthy administrative processing timelines have led many farmers to rely on bridge financing and commercial loans before receiving subsidies. Variations in subsidy timing, financing access, and loan availability continue to influence short-term machinery purchasing cycles and replacement demand patterns in the European combine harvesters market.

Commodity Price Volatility Dampening Capital Expenditure

Fluctuating grain and wheat prices across Europe are creating uncertainty in farm profitability and cash flows, prompting farmers to delay investments in new combine harvesters. According to the European Commission's Short-Term Outlook, EU cereal production is projected to reach approximately 280 million tonnes in 2025/26, up around 4.1% year-over-year. This growth is projected to improve supply conditions but will also continue to exert pressure on grain prices. Despite a recovery in production volumes, lower commodity prices and uncertainty about farm returns have weakened purchasing confidence in high-value harvesting equipment. Consequently, many farmers are focusing on managing operational costs rather than replacing machinery, leading to reduced order activity and postponed capital expenditure decisions in the European combine harvesters market.

Other drivers and restraints analyzed in the detailed report include:

- Stage V Emission Norms Accelerating Fleet Replacement

- Precision-Farming and Telematics Integration

- Shortage of Service Technicians for Advanced Electronics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-propelled combines are projected to account for 78.3% of the Europe combine harvesters market share in 2025. This dominance is driven by their widespread adoption on medium- and large-scale farms, where they enhance harvesting efficiency by combining harvesting, threshing, and grain cleaning into a single operation. Leading manufacturers, including Deere & Company and Claas KGaA mbH, are continuously improving self-propelled combines with features such as GPS steering, precision farming technologies, and real-time yield monitoring systems. In contrast, the PTO-powered segment is projected to achieve the fastest CAGR of 7.9% during 2026-2031. This growth is attributed to increasing demand from small- and medium-sized farms in Eastern European countries like Poland and Romania, where farmers prioritize lower capital investment and compatibility with existing tractor infrastructure.

The market is also experiencing rising demand for compact and mid-range combine harvesters, which cater to smaller farm operations seeking mechanized harvesting solutions at reduced ownership costs. PTO-powered combines remain attractive to price-sensitive farmers due to their simpler maintenance requirements and operational flexibility with existing tractors. However, their adoption among large commercial farming operations across Europe is limited by lower harvesting productivity and the lack of advanced automation technologies.

Complete Report Scope:

- By Type

- Self-Propelled Combine

- Tractor-Pulled Combine

- PTO-Powered Combine

- By Power Output

- Less Than 150 HP

- 151 - 300 HP

- 301 - 450 HP

- Above 450 HP

- By Geography

- Germany

- France

- United Kingdom

- Italy

- Poland

- Spain

- Rest of Europe

List of Companies Covered in this Report:

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Claas KGaA mbH

- SDF S.p.A.

- Kubota Corporation

- Mahindra&Mahindra Ltd.

- Rostselmash

- Yanmar Holdings Co., Ltd.

- Gomselmash

- ISEKI & CO.,LTD.

- Tera YatIrIm Teknoloji Holding A.S. (Sampo Rosenlew)

- Weichai Lovol Intelligent Agricultural Technology CO., LTD (SDHI Group)

- YTO Group Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Labor shortage and rising farm-labor costs

- 4.2.2 EU Common Agricultural Policy subsidies for mechanization

- 4.2.3 Stage V emission norms accelerating fleet replacement

- 4.2.4 Precision-farming and telematics integration

- 4.2.5 Adoption of track-based combines to cut soil compaction

- 4.2.6 Rise of machinery-sharing cooperatives in Eastern Europe

- 4.3 Market Restraints

- 4.3.1 High purchase and maintenance costs

- 4.3.2 Commodity-price volatility dampening capital expenditure

- 4.3.3 Shortage of service technicians for advanced electronics

- 4.3.4 Grid limitations slowing electric and hybrid uptake

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Self-Propelled Combine

- 5.1.2 Tractor-Pulled Combine

- 5.1.3 PTO-Powered Combine

- 5.2 By Power Output

- 5.2.1 Less Than 150 HP

- 5.2.2 151 - 300 HP

- 5.2.3 301 - 450 HP

- 5.2.4 Above 450 HP

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 France

- 5.3.3 United Kingdom

- 5.3.4 Italy

- 5.3.5 Poland

- 5.3.6 Spain

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Claas KGaA mbH

- 6.4.5 SDF S.p.A.

- 6.4.6 Kubota Corporation

- 6.4.7 Mahindra&Mahindra Ltd.

- 6.4.8 Rostselmash

- 6.4.9 Yanmar Holdings Co., Ltd.

- 6.4.10 Gomselmash

- 6.4.11 ISEKI & CO.,LTD.

- 6.4.12 Tera YatIrIm Teknoloji Holding A.S. (Sampo Rosenlew)

- 6.4.13 Weichai Lovol Intelligent Agricultural Technology CO., LTD (SDHI Group)

- 6.4.14 YTO Group Corporation

7 Market Opportunities and Future Outlook

北美聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測

聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測 聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年德國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)法國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)英國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)動力輸出軸驅動式聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年德國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)法國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)英國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)動力輸出軸驅動式聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 聯合收割機市場:按類型和地區分類

聯合收割機市場:按類型和地區分類