|

市場調查報告書

商品編碼

2072751

北美聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Combine Harvesters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

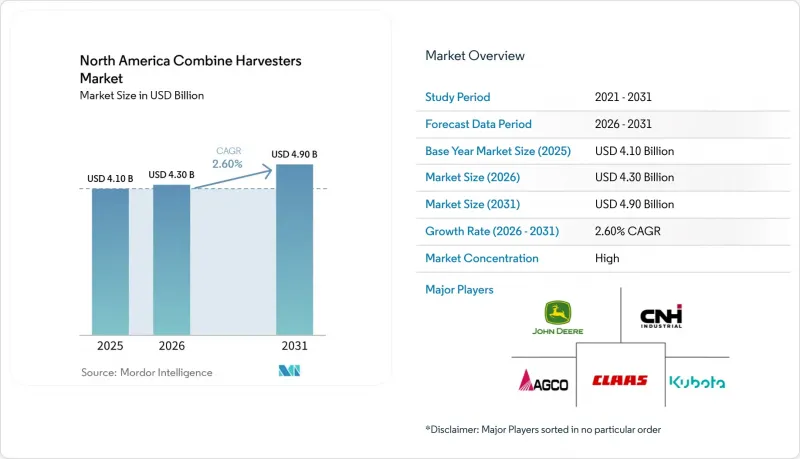

根據 Mordor Intelligence 預測,北美聯合收割機市場規模將從 2025 年的 41 億美元和 2026 年的 43 億美元成長到 2031 年的 49 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 2.60%。

本報告按產品類型(傳統秸稈行走式聯合收割機、旋轉式聯合收割機、混合式聯合收割機和履帶式聯合收割機)、功率輸出等級(200馬力以下、200-300馬力、300-400馬力和400馬力以上)以及國家/地區(美國、加拿大、墨西哥、北美及其他地區)進行細分。市場預測以美元計價。

北美聯合收割機市場趨勢及洞察

人事費用上升和勞動短缺

世界銀行數據顯示,農業勞動力的減少正在加速大型糧食農場全面採用機械化耕作方式。預計農業勞動力佔比將從2024年的1.56%下降到2025年的1.52%。 2024年,迪爾公司推出了配備「預測地面速度自動化」和自動收割設定的S7系列聯合收割機,旨在提高收割的一致性、生產效率和操作便利性。儘管時薪很高,北達科他州、蒙大拿州、薩斯喀徹爾和亞伯達等地區仍面臨嚴重的勞動力短缺。這導致薪資上漲,提高了自動和半自動聯合收割機的投資回報率,並最終降低了勞動力需求。配備先進自動化功能的聯合收割機的租賃價格正在上漲,反映出人們願意投資於能夠最大限度減少勞動力需求的功能。因此,勞動力短缺正在推高價格,並推動北美聯合收割機市場持續轉型為先進技術。

精密農業的引進與整合

聯合收割機已發展成為“移動資料中心”,可將帶有位置資訊的產量、水分、蛋白質等測量數據即時傳輸到雲端控制面板。迪爾公司的「2025 SmartPan」整合方案可在卡車抵達穀倉前提供穀物品質分析結果,從而將操作人員牢牢地融入公司的生態系統中。美國環保署 (EPA) 在切薩皮克灣和五大湖地區實施的養分管理法規等監管因素,正在推動可追溯農業化學品資料的需求。嵌入式的分析功能還支援可變飼料配比計劃,從而完善了收割和投入品施用之間的閉迴路。這些協同效應正在提高設備留存率,降低轉換成本,並為北美聯合收割機市場的長期成長奠定基礎。

先進聯合收割機的初始投資成本很高

先進聯合收割機的高昂初始投資成本嚴重限制了北美聯合收割機市場的發展,尤其對占美國農業經營90%的中小農場造成了衝擊。 AGCO公司報告稱,2024年第三季淨銷售額約為25億美元,反映出與去年同期相比,農業機械需求有所下降,因為利潤率下降導致生產者推遲了機械採購。小規模農戶越來越傾向於二手設備和季節性租賃,這延長了設備的更換週期。在墨西哥,平均農場規模不足500英畝,如果沒有仍在發展中的合作社模式,引進新機械在經濟上是不可行的。這一趨勢凸顯了設備共用和租賃等替代所有權模式的重要性,它們有助於解決該地區小規模農戶面臨的經濟困境。

細分市場分析

旋轉式聯合收割機憑藉著處理高水分玉米的卓越能力,預計到2025年將佔據北美聯合收割機市場65%的佔有率,成為最大的細分市場。傳統的秸稈行走式收割機仍在乾旱的小麥產區使用,但隨著種植面積轉向玉米和大豆,其市場佔有率正在萎縮。以AGCO的「Gleaner」系列為代表的混合式收割機,在需要柔軟性處理多種作物的合約收割機用戶中佔據了一小塊市場。雖然旋轉式聯合收割機的主導地位預計將得以保持,但競爭的重點正在轉向平台的多功能性,原始設備製造商(OEM)正在增加快拆式車軸套件,使農民能夠在四小時內完成輪式和履帶式收割機的切換。

履帶式聯合收割機是成長最快的機型,預計從2026年到2031年將達到創紀錄的7.8%的複合年成長率。儘管秋季多雨導致收割期縮短,土壤壓實風險增加,但其成長速度仍超過所有其他類型的聯合收割機。履帶式聯合收割機的需求成長主要來自北達科他州、明尼蘇達州和加拿大東部,這些地區的黏土土壤正在迅速飽和。更大的接觸面積可以降低地面壓力,從而保持土壤狀況,有利於春季播種。此外,操作人員也重視履帶式聯合收割機更高的轉售價值,這正在縮小其與輪式聯合收割機的總擁有成本差距。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人事費用上升和勞動短缺

- 精密農業的引進與整合

- 政府補助和優惠貸款

- 加快大型農場車輛更換週期

- OEM(原始設備製造商)提供的基於訂閱的自主軟體升級

- 穀物運輸車輛和聯合收割機自動化互通性標準

- 市場限制因素

- 先進聯合收割機的初始投資成本很高

- 商品價格波動影響農民的現金流

- 半導體和液壓元件供應鏈中的限制因素

- 區域電信差異阻礙了即時遠端資訊處理的廣泛應用。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 傳統秸稈行走式聯合收割機

- 旋轉式聯合收割機

- 混合式聯合收割機

- 履帶式聯合收割機

- 按輸出類別

- 不足200馬力

- 200~300 HP

- 300~400 HP

- 400馬力或以上

- 國家

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deere & Company

- Case IH Agriculture

- CNH Industrial NV

- AGCO Corporation

- CLAAS KGaA mbH

- Kubota Corporation

- Rostselmash Joint-Stock Co.

- Sampo Rosenlew Oy

- Yanmar Holdings Co., Ltd.

- Same Deutz-Fahr Italia SpA

- TRIBINE Harvester LLC

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- Oxbo International Corporation

- Preet Tractors Private Ltd.

- ISEKI & Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america combine harvesters market size is projected to expand from USD 4.10 billion in 2025 and USD 4.30 billion in 2026 to USD 4.90 billion by 2031, registering a CAGR of 2.60% between 2026 and 2031.

This report is Segmented by Product Type (Conventional Straw-Walker Combines, Rotary Combines, Hybrid Combines, and Tracked Combines), by Power Class (Below 200 HP, 200 To 300 HP, 300 To 400 HP, and Above 400 HP), by Country (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD).

North America Combine Harvesters Market Trends and Insights

Rising Labor Costs and Labor Shortages

A decline in agricultural employment is accelerating the adoption of full mechanization across large grain farms, as indicated by World Bank data. Employment in agriculture decreased to 1.52% in 2025, compared to 1.56% in 2024. In 2024, Deere & Company introduced the S7 Series combines featuring Predictive Ground Speed Automation and automated harvest settings to improve harvesting consistency, productivity, and ease of operation. Regions such as North Dakota, Montana, Saskatchewan, and Alberta are experiencing significant labor shortages despite high hourly wages. This has led to wage inflation, enhancing the return on investment for autonomous and semi-autonomous harvesters, thereby reducing labor demand. Leasing rates for combines equipped with advanced automation are increasing, reflecting a willingness to invest in features that minimize workforce requirements. Consequently, labor constraints are driving premium pricing and supporting the ongoing shift toward advanced technology in the North America combine harvesters market.

Precision-Agriculture Adoption and Integration

Combines have evolved into rolling data centers that stream location-tagged yield, moisture, and protein metrics to cloud dashboards. Deere's 2025 SmartPan integration delivers grain-quality analytics before the truck reaches the elevator, locking operators into its ecosystem. Regulatory drivers such as the Environmental Protection Agency (EPA) nutrient-management rules in the Chesapeake Bay and Great Lakes regions heighten demand for traceable agronomic data. Embedded analytics also support variable-rate fertilizer planning, closing the loop between harvest and input application. These synergies intensify equipment stickiness, raise switching costs, and underpin long-run growth for the North America combine harvesters market.

High Upfront Capital Costs for Advanced Combines

High upfront capital costs for advanced combine harvesters significantly constrain the North America combine harvesters market, particularly impacting small and medium-sized farms, which constitute 90% of farming operations in the United States. AGCO Corporation reported approximately USD 2.5 billion in net sales in Q3 2024, reflecting a year-over-year decline amid weaker agricultural equipment demand as growers delayed machinery purchases because of tighter farm margins. Smaller operators increasingly favor used units or seasonal rentals, lengthening upgrade cycles. In Mexico, the average farm size is below 500 acres, rendering new machines uneconomical without cooperative models that are still nascent. This trend underscores the growing importance of alternative ownership models, such as equipment sharing and leasing, to address the economic constraints faced by smaller farming operations in the region.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies and Preferential Financing

- Original Equipment Manufacturer (OEM) Subscription-Based Autonomous Software Upgrades

- Rural Connectivity Gaps Limiting Real-Time Telematics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rotary combines led the largest segment, with 65% of the North America combine harvesters market share in 2025, owing to superior throughput in high-moisture corn. Conventional straw-walker models persist in drier wheat belts, but their share erodes as acreage tilts toward corn and soybeans. Hybrid architectures, championed by AGCO's Gleaner line, capture a small niche among custom harvesters that need multi-crop flexibility. Rotary dominance will remain intact, but the competitive narrative is shifting toward platform versatility, with Original Equipment Manufacturer (OEM) adding quick-attach axle kits that let growers convert between wheels and tracks in under four hours.

Tracked combines are the fastest-growing, forecast to post the fastest 7.8% CAGR through 2026 to 2031, outpacing all other product types as wetter autumns shorten harvest windows and soil-compaction risk climbs. Rising demand for tracks comes primarily from North Dakota, Minnesota, and eastern Canada, where clay soils saturate quickly. Larger contact patches lower ground pressure, preserving soil tilth for spring planting. Operators also value higher resale prices for tracked units, narrowing total cost-of-ownership gaps with wheeled alternatives.

Complete Report Scope:

- By Product Type

- Conventional Straw-Walker Combines

- Rotary Combines

- Hybrid Combines

- Tracked Combines

- By Power Class

- Below 200 HP

- 200 to 300 HP

- 300 to 400 HP

- Above 400 HP

- By Country

- United States

- Canada

- Mexico

- Rest of North America

List of Companies Covered in this Report:

- Deere & Company

- Case IH Agriculture

- CNH Industrial N.V.

- AGCO Corporation

- CLAAS KGaA mbH

- Kubota Corporation

- Rostselmash Joint-Stock Co.

- Sampo Rosenlew Oy

- Yanmar Holdings Co., Ltd.

- Same Deutz-Fahr Italia S.p.A.

- TRIBINE Harvester LLC

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- Oxbo International Corporation

- Preet Tractors Private Ltd.

- ISEKI & Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising labor costs and labor shortages

- 4.2.2 Precision-agriculture adoption and integration

- 4.2.3 Government subsidies and preferential financing

- 4.2.4 Accelerated fleet-replacement cycles on large farms

- 4.2.5 Original Equipment Manufacturer (OEM)subscription-based autonomous software upgrades

- 4.2.6 Interoperability standards for grain cart-combine automation

- 4.3 Market Restraints

- 4.3.1 High upfront capital costs for advanced combines

- 4.3.2 Commodity-price volatility impacting farm cash flow

- 4.3.3 Semiconductor and hydraulic component supply-chain constraints

- 4.3.4 Rural connectivity gaps limiting real-time telematics

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Conventional Straw-Walker Combines

- 5.1.2 Rotary Combines

- 5.1.3 Hybrid Combines

- 5.1.4 Tracked Combines

- 5.2 By Power Class

- 5.2.1 Below 200 HP

- 5.2.2 200 to 300 HP

- 5.2.3 300 to 400 HP

- 5.2.4 Above 400 HP

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

- 5.3.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 Case IH Agriculture

- 6.4.3 CNH Industrial N.V.

- 6.4.4 AGCO Corporation

- 6.4.5 CLAAS KGaA mbH

- 6.4.6 Kubota Corporation

- 6.4.7 Rostselmash Joint-Stock Co.

- 6.4.8 Sampo Rosenlew Oy

- 6.4.9 Yanmar Holdings Co., Ltd.

- 6.4.10 Same Deutz-Fahr Italia S.p.A.

- 6.4.11 TRIBINE Harvester LLC

- 6.4.12 Zoomlion Heavy Industry Science & Technology Co., Ltd.

- 6.4.13 Oxbo International Corporation

- 6.4.14 Preet Tractors Private Ltd.

- 6.4.15 ISEKI & Co., Ltd.

7 Market Opportunities and Future Outlook

聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測

聯合收割機市場規模、佔有率和成長分析:按設備移動方式、驅動系統、引擎功率、目標作物和地區分類-2026-2033年產業預測 聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年

聯合收割機市場:按類型、引擎功率、驅動系統、應用和銷售管道-全球預測,2026-2032年 德國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)法國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)英國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)動力輸出軸驅動式聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

德國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)法國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)英國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中國聯合收割機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)動力輸出軸驅動式聯合收割機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 聯合收割機市場:按類型和地區分類

聯合收割機市場:按類型和地區分類