|

市場調查報告書

商品編碼

2066659

印尼陸上貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Indonesia Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

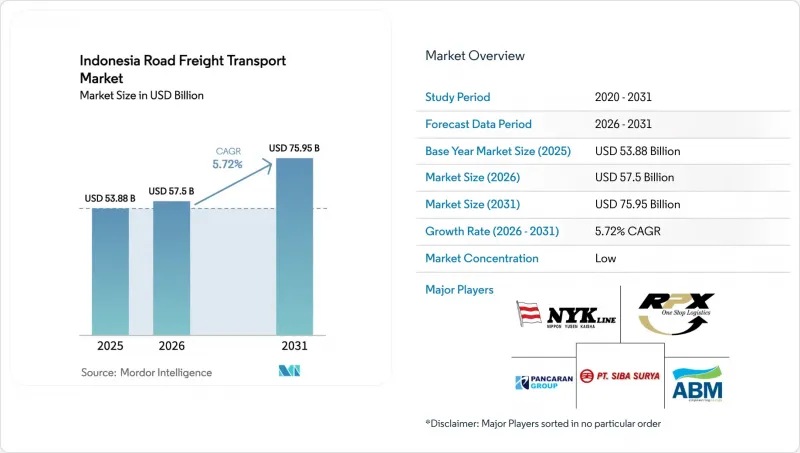

根據 Mordor Intelligence 預測,印尼陸路貨運市場規模預計將從 2025 年的 538.8 億美元成長到 2026 年的 575 億美元,到 2031 年達到 759.5 億美元,2026 年至 2031 年的複合年成長率為 5.72%。

國家物流生態系統 (NLE) 的日益普及正在縮短門到港的運輸週期,而歐盟4柴油排放標準的實施則提高了車輛的可靠性,迫使承運商對其設備進行現代化改造。本報告按最終用戶產業(如農業)、目的地(國內、國際)、整車負載容量(FTL、LTL)、容器化(貨櫃運輸、散裝運輸)、運輸距離(長途、短程)、貨物類型(液體、固體)以及溫度控制(非溫控、溫控)進行細分。市場預測以美元計價。

印尼陸上貨運市場趨勢及洞察。

透過國家物流生態系統實現電子清關,縮短了從門到港的周期時間。

NLE將海關、港口營運商和貨運代理商整合到一個統一的數位化平台,將文件處理時間從3-5天縮短至24小時以內。陸路運輸商先前承擔等待時間的成本,如今由於清訂單時間的縮短,卡車運轉率得以提高,訂單到付款的周期也得以縮短。早期用戶報告稱,門到港的運輸時間縮短了18-22%。該平台與東協海關過境系統整合,提高了跨境運輸的可預測性,並支援準時制生產。隨著NLE平台持續擴展到其他港口,這些優勢將惠及爪哇島以外的地區,從而推動整個印尼陸上貨運市場的成長。

由於國內疫苗和生技藥品的生產,藥品低溫運輸迅速發展

生物製藥的年產量已超過10億劑,預計2026年底將增加至15億劑。如此龐大的產量需要符合藥品良好分銷規範(GDP)的運輸方式,並需將溫度控制在2-8°C之間,同時進行即時監控。隨著Calve Pharma和IndoPharma新增生物製藥生產線,對冷藏拖車和數據記錄系統的需求增加了一倍。印尼食品藥物管理局(BPOM)的嚴格監管提高了非官方營運商的准入門檻,使擁有檢驗流程的承運商更具優勢。因此,低溫運輸產業的成長速度超過了印尼整體陸上貨運市場的成長速度。

爪哇-蘇門答臘走廊的貨物竊盜保險費飆升。

由於竊盜率上升了18%至22%,高價值貨物的保險成本也飆升了15%至20%。中小貨運公司面臨利潤率壓力,或被迫將風險轉嫁給托運人,從而降低了自身的競爭力。 GPS設備、封條設備和護送團隊等額外成本進一步推高了營運成本,使其增加了3%至5%。由於各州執法機關之間缺乏協調,有組織犯罪得以利用休息站的漏洞,導致托運人在競標貨物時要求採取高標準的安保措施。因此,印尼陸上貨運市場的產業重組正在加速進行。

細分市場分析

到2025年,批發和零售將佔印尼陸上貨運市場的34.24%,反映出爪哇島一、二線城市強勁的消費需求。預計該領域的複合年成長率將達到6.58%,成為成長最快的領域,這主要得益於便利商店的擴張以及連鎖藥局引入健康保健產品。目前,運輸網路的設計正朝著消費品和生物製藥的混合運輸方向發展,從而提高服務頻率和車輛運轉率。製造業憑藉卡拉旺的汽車產業中心和巴淡島的電子產業叢集保持穩定的基礎,但其對全球製造業回流的影響仍令人擔憂。

石油天然氣、採礦和採石業受益於蘇拉威西島鎳價上漲和加里曼丹島煤炭出口成長,從而帶動了對專用重型運輸設備的需求。建築材料運輸與正在進行的國家戰略項目密切相關,水泥和鋼鐵的運輸遵循可預測的時間表。農業和水產養殖業利用冷藏物流來獲取蝦子和山竹的出口溢價,而資料中心建設等新興產業則產生不規則的、專案特定的貨運需求。這些相互交織的物流流支撐著印尼陸上貨運市場的多元化成長。

即使到了2025年,國內運輸仍將佔據62.88%的市場佔有率,貨運公司將透過公路和渡輪相結合的方式為6000個有人居住的島嶼提供服務。爪哇島和蘇門答臘島收費公路的建設將使旅行時間縮短多達20%,提高服務可靠性,並為庫存削減策略奠定基礎。

然而,由於北方物流系統(NLE)與東協系統互通性提升,邊境等待時間縮短了約50%,印尼對馬來西亞、新加坡和泰國的國際貨運正以6.65%的複合年成長率快速成長。 「海上收費公路」的營運打造了可預測的多式聯運樞紐,強化了國內路線規劃。同時,巴淡島和棉蘭附近的保稅物流中心正逐漸成為國際拼箱貨運的樞紐。吉隆坡-新加坡-雅加達走廊如今能夠實現電子產品和藥品的“準時交貨”,縮小了陸運與海運的服務成本差距。這些互補的物流流正推動印尼陸上貨運市場的強勁成長。

到2025年,整車運輸(FTL)在印尼陸上貨運市場仍將佔據80.19%的佔有率。這主要得益於棕櫚油、煤炭和鎳礦等貨物的大規模運輸,這些貨物本身就適合裝滿拖車。為遵守《重量和尺寸法規》(ODOL),運輸方式正轉向多軸模組化卡車,這將使法定負載容量提高30%,並提升整車運輸的成本競爭力。

同時,在Kargo Technologies和Deliveree等平台的推動下,零擔貨運(LTL)正以6.41%的複合年成長率保持強勁成長。這些平台匯集了中小企業的貨物,並建構了最佳化的多目的地路線。演算法調度和動態定價提高了車輛裝載率,降低了小規模托運人的單位貨運成本。現有的整車運輸(FTL)承運商也積極響應,推出混合服務,利用按需零擔貨運填補空置空間,模糊了不同運輸類別之間的界限。這種雙軌發展趨勢正在推動印尼陸上貨運市場的健康多元化。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 按經濟活動分類的GDP構成

- 按經濟活動分類的GDP成長率

- 經濟表現及概覽

- 電子商務產業的趨勢

- 製造業的發展趨勢

- 運輸和倉儲部門的GDP

- 物流績效

- 道路長度

- 出口趨勢

- 進口趨勢

- 燃油價格趨勢

- 卡車運輸營運成本

- 按車輛類型分類的卡車擁有數量

- 主要卡車供應商

- 陸上貨運發展趨勢

- 陸上貨運價格趨勢

- 不同交通途徑的使用率

- 通貨膨脹

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 透過國家物流系統 (NLE) 實現電子清關,正在縮短從門到港的周期時間。

- 由於國內疫苗和生技藥品的生產,藥品低溫運輸迅速擴張。

- 強制過渡到歐盟4柴油引擎正在提高車輛的可靠性和轉售價值。

- 強制使用 B40 生質柴油穩定了長途貨運公司的柴油燃料採購成本。

- 蘇拉威西島的鎳電池供應鏈正在產生大量的原料流入。

- ODOL逐步淘汰正在提振高容量模組化軌道組的需求。

- 市場限制因素

- 爪哇-蘇門答臘航線的貨物竊盜保險費飆升。

- 即使在私有化之後,港口出口的擁擠問題依然存在,導致等待時間延長。

- 除了 Jasa-Marga 系統之外,其他分散的收費系統加劇了不同路線之間的成本差異。

- 液化天然氣加氣網建設進展緩慢,延緩了替代燃料卡車的引進。

- 市場上的技術創新

- 波特五力分析

第5章 市場規模與成長預測

- 按最終用戶行業分類

- 農業、漁業、林業

- 建造

- 製造業

- 石油和天然氣、採礦和採石

- 批發和零售

- 其他

- 按目的地

- 國內的

- 國際的

- 依卡車負載容量

- 全軌道公路(FTL)

- 小批量貨物(零擔)

- 透過容器化

- 容器化

- 容器化

- 按運輸距離

- 長途

- 短程航線

- 按貨物類型

- 流體產品

- 實際產品

- 透過溫度控制

- 無溫度控制

- 溫度控制

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- Bali Pro Cargo

- CJ Logistics Corporation

- DHL Group

- DSV

- Geodis

- JNE Express

- Ninja Express

- NYK Line

- NYK Line(Yusen Logistics Malaysia)

- Pancaran Group

- PT ABM Investama Tbk(PT Cipta Krida Bahari)

- PT Citrabati Logistik International

- PT Prima International Cargo

- PT Repex Wahana(RPX)

- PT Samudera Indonesia Tangguh

- PT Siba Surya

- PT.DMS Logistics Indonesia

- Rhenus Group

- Seacon Logistics

- Total Logistics

第7章 市場機會與未來展望

According to Mordor Intelligence, the indonesia road freight transport market is expected to increase from USD 53.88 billion in 2025 to USD 57.50 billion in 2026 and reach USD 75.95 billion by 2031, growing at a CAGR of 5.72% over 2026-2031.

Rising adoption of the National Logistics Ecosystem (NLE) compresses door-to-port cycle times, while Euro-4 diesel standards improve fleet reliability, pushing carriers to modernize equipment. This report is Segmented by End-User (Agriculture, and More), by Destination (Domestic, International), by Truckload (FTL, LTL), by Containerization (Containerized, Non-Containerized), by Distance (Long Haul, Short Haul), by Good Configuration (Fluid, Solid), and by Temperature (Non-Temperature Controlled, Temperature Controlled). The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Road Freight Transport Market Trends and Insights

National Logistics Ecosystem E-clearance Accelerating Door-to-Port Cycle Times

NLE integrates customs, port operators, and freight forwarders on one digital platform, shrinking documentation processing from three to five days to under 24 hours. Road carriers that previously absorbed idle-time costs now experience faster gate release, improving truck utilization and shortening order-to-cash cycles. Early adopters have reported 18-22% shorter door-to-port intervals. The platform's alignment with the ASEAN Customs Transit System improves predictability for cross-border trips and supports just-in-time manufacturing. Ongoing rollout to secondary ports will extend these gains beyond Java, fostering broader Indonesia road freight transport market growth.

Pharmaceutical Cold-chain Surge from Domestic Vaccine & Biologics Production

Bio Farma's annual output already exceeds 1 billion vaccine doses, and capacity is expected to rise to 1.5 billion by 2026 end. These volumes require Good Distribution Practice-compliant transport holding 2-8 °C and real-time monitoring. Kalbe Farma and Indofarma have added biologics lines, doubling demand for refrigerated trailers and data-logger systems. Strict BPOM oversight increases barriers for informal operators, favoring established fleets with validated processes. The cold-chain segment therefore outpaces the overall Indonesia road freight transport market.

Sharp Rise in Cargo-Theft Insurance Premiums Along Java-Sumatra Corridors

Insurance costs for high-value cargoes have surged 15-20% after an 18-22% uptick in theft incidents. Smaller carriers endure margin compression or shift risk onto shippers, reducing competitiveness. Added expenses for GPS devices, seals, and convoy escorts raise operating costs by another 3-5%. Law-enforcement coordination gaps across provinces enable organized crime to exploit rest-area vulnerabilities, encouraging shippers to mandate advanced security when tendering loads. Market consolidation thus accelerates in the Indonesia road freight transport market.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Euro-4 Diesel Transition Improving Fleet Reliability and Resale Values

- B40 Biodiesel Mandate Stabilizing Diesel Supply Costs for Long-Haul Carriers

- Persistent Port Gate-Out Congestion Post-Privatization Extending Dwell Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wholesale and retail trade accounted for 34.24% of the Indonesia road freight transport market size in 2025, reflecting dense consumer demand across Java's tier-1 and tier-2 cities. This segment also exhibits the fastest 6.58% CAGR as convenience stores expand and pharmacy chains roll out health-and-wellness lines. Network designs now co-load consumer goods with biologics, intensifying route frequency and boosting vehicle utilization. Manufacturing sustains a steady baseline via automotive hubs in Karawang and electronics clusters in Batam, though exposure to global re-shoring remains a watch point.

Oil and gas, mining, and quarrying benefit from Sulawesi's nickel upswing and Kalimantan's coal exports, calling for specialized heavy-haul equipment. Construction freight aligns with ongoing National Strategic Projects, moving cement and steel on predictably scheduled runs. Agriculture and aquaculture adopt refrigerated logistics to capture export premiums for shrimp and mangosteen, while emerging verticals such as data-center construction generate episodic project loads. The overlapping flows collectively support diversified growth in the Indonesia road freight transport market.

Domestic moves still dominate with a 62.88% share in 2025 as shippers service 6,000 inhabited islands via road-ferry combinations. Toll-road build-out on Java and Sumatra cuts travel times by up to 20%, raising service reliability and underpinning inventory reduction strategies.

However, international volumes into Malaysia, Singapore, and Thailand are expanding faster at a 6.65% CAGR, assisted by NLE-to-ASEAN system interoperability that slashes border waits by roughly 50%. Sea Tollway sailings create predictable intermodal nodes, enhancing domestic route planning, whereas bonded logistics centers near Batam and Medan anchor international consolidation. The Kuala Lumpur-Singapore-Jakarta corridor now supports just-in-sequence deliveries for electronics and pharma, narrowing cost-of-service gaps with ocean freight. These complementary flows anchor resilient expansion for the Indonesia road freight transport market.

Full-truck-load retained 80.19% of Indonesia road freight transport market in 2025, driven by bulk palm oil, coal, and nickel ore consignments that naturally fill trailers. ODOL compliance pushes fleets toward multi-axle modular rigs that lift legal payload by up to 30%, enhancing FTL cost competitiveness.

Less-than-truck-load, meanwhile, grows at a brisk 6.41% CAGR as platforms such as Kargo Technologies and Deliveree aggregate SME volumes into optimized multi-drop routes. Algorithmic dispatch and dynamic pricing improve vehicle load factors, lowering per-unit freight for smaller shippers. Established FTL fleets respond by launching hybrid offerings that back-fill empty legs with on-demand LTL loads, blurring category lines. This dual evolution supports healthy diversification within the Indonesia road freight transport market.

List of Companies Covered in this Report:

- Bali Pro Cargo

- CJ Logistics Corporation

- DHL Group

- DSV

- Geodis

- JNE Express

- Ninja Express

- NYK Line

- NYK Line (Yusen Logistics Malaysia)

- Pancaran Group

- PT ABM Investama Tbk (PT Cipta Krida Bahari)

- PT Citrabati Logistik International

- PT Prima International Cargo

- PT Repex Wahana (RPX)

- PT Samudera Indonesia Tangguh

- PT Siba Surya

- PT.DMS Logistics Indonesia

- Rhenus Group

- Seacon Logistics

- Total Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 National Logistics Ecosystem (NLE) e-clearance accelerating door-to-port cycle times

- 4.20.2 Pharmaceutical cold-chain surge from domestic vaccine & biologics production

- 4.20.3 Mandatory Euro-4 diesel transition improving fleet reliability and resale values

- 4.20.4 B40 biodiesel mandate stabilising diesel supply costs for long-haul carriers

- 4.20.5 Sulawesi nickel-to-battery corridor creating heavy inbound raw-material flows

- 4.20.6 ODOL phase-out law spurring demand for higher-capacity modular trucksets

- 4.21 Market Restraints

- 4.21.1 Sharp rise in cargo-theft insurance premiums along Java-Sumatra corridors

- 4.21.2 Persistent port gate-out congestion post-privatisation extending dwell times

- 4.21.3 Fragmented non-Jasa-Marga toll billing systems inflating en-route cost variance

- 4.21.4 Sparse LNG refuelling network delaying alternative-fuel truck adoption

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Bali Pro Cargo

- 6.4.2 CJ Logistics Corporation

- 6.4.3 DHL Group

- 6.4.4 DSV

- 6.4.5 Geodis

- 6.4.6 JNE Express

- 6.4.7 Ninja Express

- 6.4.8 NYK Line

- 6.4.9 NYK Line (Yusen Logistics Malaysia)

- 6.4.10 Pancaran Group

- 6.4.11 PT ABM Investama Tbk (PT Cipta Krida Bahari)

- 6.4.12 PT Citrabati Logistik International

- 6.4.13 PT Prima International Cargo

- 6.4.14 PT Repex Wahana (RPX)

- 6.4.15 PT Samudera Indonesia Tangguh

- 6.4.16 PT Siba Surya

- 6.4.17 PT.DMS Logistics Indonesia

- 6.4.18 Rhenus Group

- 6.4.19 Seacon Logistics

- 6.4.20 Total Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

西班牙公路貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)英國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

西班牙公路貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)英國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 2026-2030年全球公路貨運市場

2026-2030年全球公路貨運市場 2026年全球公路貨運市場報告

2026年全球公路貨運市場報告 陸上貨運市場:2026-2032年全球市場預測(依服務類型、貨物類型、所有權、車輛類型及最終用途分類)

陸上貨運市場:2026-2032年全球市場預測(依服務類型、貨物類型、所有權、車輛類型及最終用途分類) 公路貨運服務市場機會、成長促進因素、產業趨勢分析、預測(2026-2035年)美國公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本公路貨運:市佔率分析、產業趨勢與統計及成長預測(2026-2031)北美公路貨運市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

公路貨運服務市場機會、成長促進因素、產業趨勢分析、預測(2026-2035年)美國公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本公路貨運:市佔率分析、產業趨勢與統計及成長預測(2026-2031)北美公路貨運市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)