|

市場調查報告書

商品編碼

2066658

英國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)United Kingdom Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

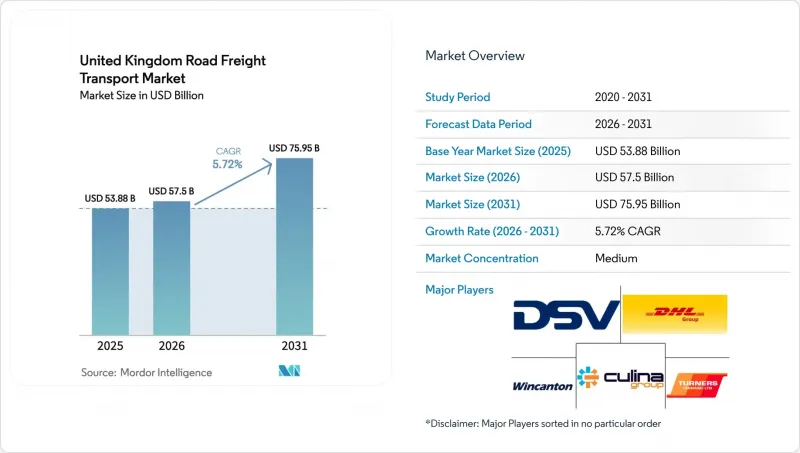

根據 Mordor Intelligence 預測,英國公路貨運市場規模預計在 2025 年達到 538.8 億美元,2026 年達到 575 億美元,到 2031 年達到 759.5 億美元,2026 年至 2031 年的複合年成長率為 5.72%。

本報告依最終用戶(農業、漁業/林業、其他)、目的地(國內、國際)、負載容量(整車運輸、零擔運輸)、容器化(貨櫃運輸、散裝運輸)、運輸距離(長途、短途)、貨物類型(液體、固體)和溫度控制方式(常溫、溫控)進行分類。市場預測以美元計價。

英國公路貨運市場趨勢與洞察

數位化邊境管制和海關現代化正在加速跨境運輸週期。

GVMS和BTOM已將申報資訊整合到單一的數位文件中,並在貨物抵達前進行處理,使得87%的貨物無需檢查即可清關,並將多佛港的跨境從2024年的47分鐘縮短至2025年的28分鐘。與歐盟ICS2系統的整合實現了運輸前風險分析,使拒收率降低了34%。需要溫控的托運人尤其受益,因為他們可以避免因長時間等待而導致的貨物劣化。更快捷的邊境通關進一步鞏固了英國公路貨運市場,將部分貨物從歐洲短程航線的空運中分流出去。承運商報告稱,由於先前閒置在港口的牽引車現在重新投入更高效、更能創造收益的營運中,周轉率提高了6-8%。數位申報的引入也加劇了英國公路貨運市場的競爭,使小規模的承運商能夠提供國際運輸服務。

大型企劃增加建築貨運量

光是HS2高鐵第一期工程預計到2028年就將消耗1,800萬噸骨材和120萬噸鋼材,而到2030年,下泰晤士河大橋的運輸量預計還將增加300萬噸。政府的基礎設施預算在2027年之前將平均每年達到1,410億美元,並已確保簽訂多年合約。這些項目將透過確保可預測的負載容量和促進車輛現代化改造(例如採用專用移動地板和低平板拖車)來提高資本效率。由於鐵路運輸能力仍然有限,長途運輸佔據了英國公路貨運市場的大部分貨物流量。此外,大量的建設項目將使運輸商免受零售業放緩的影響,並提供與經濟週期相反的收入穩定性。

缺乏符合歐盟法規 561/2006 其他要求的大型貨車 (HGV) 安全過夜停車位。

英國目前有52萬輛大型貨運車輛投入運營,但符合規定的停車位僅有1.1萬個,迫使68%的駕駛人違規停車,面臨罰款和吊銷駕照的處罰。在M1、M6和A1高速公路沿線的擁擠路段,停車位供需缺口高達4:1,導致駕駛人為了尋找停車位而繞行的次數增加了8%至12%,影響了他們的運作時間。繞行造成的路線變更降低了車輛的運輸效率,增加了燃油成本,並損害了英國公路貨運市場的可靠性。

細分市場分析

按最終用戶分類,預計到2025年,製造業將保持英國公路貨運市場40.65%的佔有率,而批發和零售貿易預計將以2.90%的複合年成長率(CAGR)實現最高成長,直至2031年。製造業將繼續保持其主要細分市場的地位,這得益於中部地區汽車生產和生物製藥叢集的擴張。同時,批發和零售貿易的成長則受到全通路模式的推動,這種模式需要更頻繁、更小批量的貨運。

先進治療藥物的溫控物流持續支持加值服務,並提振了對藥品的需求。同時,諸如HS2高鐵和下泰晤士河通道等基礎設施項目促進了建築材料的運輸;英國脫歐後農業領域轉向國內採購以及北海電廠的持續退役,也支撐了對特種貨物的需求。倫敦-都柏林走廊沿線資料中心的開發也為高價值、時效性強的運輸創造了機遇,促使承運商擴大服務能力。

從目的地來看,國際運輸預計將以3.10%的複合年成長率成長。雖然到2025年,國際運輸量僅佔總運輸量的34.43%,但由於數位化邊境改革顯著減少了邊境延誤,其成長速度超過了國內貨運。國內運輸仍佔據市場主導地位,這得益於英國人口密度高和地理結構等因素,但邊境效率的提高和自由港激勵措施正鼓勵更多公司參與跨境貿易。

國內運輸也受惠於主要公路幹線效率的提高,這有助於緩解長期存在的司機短缺問題。然而,北愛爾蘭的沿海運輸限制和合規複雜性等監管約束,正對跨海峽運輸的獲利能力構成壓力。為此,一些托運人正擴大採用無人駕駛拖車運輸解決方案,利用渡輪提高柔軟性並降低調度風險。

依運輸類型分類,全程公路運輸(FTL)在2025年佔英國公路貨運市場的83.36%,但預計到2031年,零擔運輸(LTL)將以2.93%的複合年成長率(CAGR)保持最高成長。全程公路運輸(FTL)繼續主導市場,這主要得益於大規模零售補貨運輸、汽車行業的準時制(JIS)供應鏈以及建築物流。其高裝載效率進一步增強了其在長途運輸路線上的成本優勢。

由於電子商務退貨量增加以及循環經濟實踐推動貨物日益分散,零擔貨運(LTL)正在蓬勃發展。數位化貨運平台的引入提高了退貨匹配率,並減少了空駛里程,縮小了與整車運輸的成本差距。然而,儘管結合整車運輸(FTL)和零擔運輸(LTL)的混合車輛營運策略能夠提高資產利用率,但其實施需要先進的規劃能力,而許多中型企業仍在建立這些能力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 按經濟活動分類的GDP構成

- 按經濟活動分類的GDP成長率

- 經濟表現及概覽

- 電子商務產業的趨勢

- 製造業的發展趨勢

- 運輸和倉儲部門的GDP

- 物流績效

- 道路長度

- 出口趨勢

- 進口趨勢

- 燃油價格趨勢

- 卡車運輸營運成本

- 按車輛類型分類的卡車擁有數量

- 主要卡車供應商

- 公路貨運發展趨勢

- 陸上貨運價格趨勢

- 按交通途徑分享

- 通貨膨脹

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 實現數位邊界和海關(GVMS、BTOM)的現代化將加速跨境貿易週期。

- 大型基礎設施項目(HS2高鐵、下泰晤士河通道)增加了建築材料運輸量。

- 製藥和生物技術製造群的興起推動了對溫度控制的需求。

- 60噸級公路列車的試運行提高了主要線路的生產效率。

- 由於針對企業的第三類法規,運輸量正在轉移到經過認證的低碳承運商。

- 有關循環經濟和產品回收的法律正在擴大逆向物流的流動。

- 市場限制因素

- 目前缺少符合歐盟法規 561/2006 其他要求的重型貨車 (HGV) 安全過夜停車位。

- 物流地產短缺;「金三角」地區的倉庫租金年複合成長率超過 12%。

- 英國脫歐後的沿海運輸限制和簽證限額限制了旺季期間的運輸能力。

- 零件和輪胎供應中斷,導致重型貨車運作時間延長。

- 市場上的技術創新

- 波特五力分析

第5章 市場規模與成長預測

- 終端用戶產業

- 農業、漁業、林業

- 建造

- 製造業

- 石油和天然氣、採礦和採石

- 批發和零售

- 其他

- 按目的地

- 國內的

- 國際的

- 依卡車負載容量

- 全軌道公路(FTL)

- 小批量貨物(零擔)

- 透過容器化

- 容器化

- 容器化

- 按運輸距離

- 長途

- 短程航線

- 按貨物類型

- 流體產品

- 實際產品

- 透過溫度控制

- 無溫度控制

- 溫度控制

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- AP Moller-Maersk

- Culina Group

- DACHSER

- DFDS

- DHL Group

- DSV A/S

- Girteka

- Gist Ltd

- Gregory Distribution Ltd

- GXO Logistics(Wincanton PLC)

- Howard Tenens

- Hoyer GmbH

- Kinaxia Logistics Ltd

- Marshalls Logistics

- Nordic Transport Group A/S

- Palletways

- Turners(Soham)Ltd

- United Parcel Service of America, Inc.(UPS)

- WH Malcolm Ltd

- XPO, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom road freight transport market size is projected to be USD 53.88 billion in 2025, USD 57.5 billion in 2026, and reach USD 75.95 billion by 2031, growing at a CAGR of 5.72% from 2026 to 2031.

This report is Segmented by End-User (Agriculture, Fishing & Forestry, and More), by Destination (Domestic, International), by Truckload (FTL, LTL), by Containerization (Containerized, Non-Containerized), by Distance (Long Haul, Short Haul), by Goods (Fluid, Solid), by Temperature (Non-Temperature, Temperature Controlled). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Road Freight Transport Market Trends and Insights

Digital Border & Customs Modernization Speeds Cross-Border Cycles

GVMS and BTOM consolidate declarations into a single digital file processed pre-arrival, allowing 87% of consignments to clear without inspection and cutting crossing times at Dover from 47 minutes to 28 minutes during 2024-2025. The link with the EU's ICS2 permits advance risk analysis that lowered rejection rates 34%. Temperature-controlled shippers benefit most, avoiding spoilage formerly caused by multi-hour queues. Faster borders also strengthen the United Kingdom road freight transport market by drawing volumes away from air freight on short European lanes. Operators report 6-8% asset-turn increases as tractors previously idling at ports re-enter revenue runs more quickly. Digital declarations further enable smaller haulers to offer international services, broadening competitive intensity inside the United Kingdom road freight transport market.

Infrastructure Mega-Projects Swell Construction Freight

HS2 Phase One alone consumes 18 million tons of aggregates and 1.2 million tons of steel through 2028, while the Lower Thames Crossing adds 3 million tons of deliveries through 2030. Government infrastructure budgets average USD 141 billion annually to 2027, ensuring multi-year contract visibility. These projects anchor predictable payloads that encourage fleet renewal into specialized walking-floor and low-loader trailers, raising capital efficiency. Long-haul segments of the United Kingdom road freight transport market capture the bulk of material flows as rail paths remain capacity-constrained. Construction volumes also cushion carriers against retail slowdowns, producing counter-cyclical revenue stability.

Shortage of Secure Overnight HGV Parking Meeting EU 561/2006 Rest Rules

Only 11,000 compliant spaces exist for 520,000 HGVs, forcing 68% of drivers into unlawful lay-bys where fines and operator-license sanctions loom. Hotspots on the M1, M6, and A1 experience 4:1 demand-supply gaps that add 8-12% detours for parking searches, trimming driver hours. Re-routing lowers fleet productivity, inflates fuel spend, and erodes service reliability inside the United Kingdom road freight transport market.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Pharma Biomanufacturing Clusters Drives Temperature-Controlled Demand

- 60-Tons Road-Train Pilot Boosts Trunk-Route Productivity

- Logistics-Real-Estate Scarcity Drives Warehouse Rents Above 12% CAGR.

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

By end user, manufacturing retained 40.65% of the United Kingdom road freight transport market share in 2025, while wholesale and retail trade is forecast to post the fastest 2.90% CAGR through 2031. Manufacturing remained the leading segment, supported by automotive production in the Midlands and the expansion of biopharma clusters, while wholesale and retail growth is being driven by omnichannel models that require more frequent, lower-volume shipments.

Temperature-controlled logistics for advanced therapies continue to support premium services and strengthen pharmaceutical demand. At the same time, infrastructure projects such as HS2 and the Lower Thames Crossing are boosting the movement of construction materials, while post-Brexit shifts toward domestic sourcing in agriculture and ongoing North Sea decommissioning sustain specialized freight demand. Emerging data center developments along the London-Dublin corridor are also creating opportunities for high-value, time-sensitive transport, encouraging fleets to expand service capabilities.

By destination, international movements delivered a 3.10% CAGR outlook, outperforming domestic freight despite holding only 34.43% of 2025 volumes after digital border reforms significantly reduced border delays. Domestic haulage continued to dominate the market, supported by dense population centers and the country's geographic structure, while improving border efficiency and Freeport incentives are encouraging more businesses to participate in cross-border trade.

Domestic operations are also benefiting from productivity gains on key motorway corridors, helping offset ongoing driver shortages. However, regulatory constraints such as cabotage limits and added compliance complexities in Northern Ireland are weighing on cross-Channel margins. In response, some shippers are increasingly adopting unaccompanied trailer solutions via ferry to improve flexibility and reduce scheduling risks.

By truckload, Full-truck-load services accounted for 83.36% of the United Kingdom road freight transport market size in 2025, while Less-than-truckload is forecast to post the fastest 2.93% CAGR through 2031. Full-truck-load activity continues to dominate, supported by large-scale retail replenishment, automotive just-in-sequence supply chains, and construction logistics, with higher payload efficiencies further strengthening its cost advantage on longer routes.

Less-than-truckload is expanding due to the rise in e-commerce returns and increasing shipment fragmentation driven by circular economy practices. The adoption of digital freight platforms is improving backhaul matching and reducing empty miles, helping narrow cost differences with full loads. However, while hybrid FTL-LTL fleet strategies offer better asset utilization, they require advanced planning capabilities that many mid-sized operators are still developing.

List of Companies Covered in this Report:

- A.P. Moller-Maersk

- Culina Group

- DACHSER

- DFDS

- DHL Group

- DSV A/S

- Girteka

- Gist Ltd

- Gregory Distribution Ltd

- GXO Logistics (Wincanton PLC)

- Howard Tenens

- Hoyer GmbH

- Kinaxia Logistics Ltd

- Marshalls Logistics

- Nordic Transport Group A/S

- Palletways

- Turners (Soham) Ltd

- United Parcel Service of America, Inc. (UPS)

- W H Malcolm Ltd

- XPO, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 Digital border & customs modernisation (GVMS, BTOM) speeds cross-border cycles

- 4.20.2 Infrastructure mega-projects (HS2, Lower Thames Crossing) swell construction freight

- 4.20.3 Rise of pharma biomanufacturing clusters driving temperature-controlled demand

- 4.20.4 60-tons road-train pilot boosts trunk-route productivity

- 4.20.5 Corporate Scope-3 mandates shifting volumes to certified low-carbon carriers

- 4.20.6 Circular-economy & product-returns laws expanding reverse-logistics flows

- 4.21 Market Restraints

- 4.21.1 Shortage of secure overnight HGV parking meeting EU 561/2006 rest rules

- 4.21.2 Logistics-real-estate scarcity; warehouse rents >12 % CAGR in Golden Triangle

- 4.21.3 Post-Brexit cabotage limits & visa caps curbing peak-season capacity

- 4.21.4 Parts & tyre supply disruptions prolonging HGV downtime

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 A.P. Moller-Maersk

- 6.4.2 Culina Group

- 6.4.3 DACHSER

- 6.4.4 DFDS

- 6.4.5 DHL Group

- 6.4.6 DSV A/S

- 6.4.7 Girteka

- 6.4.8 Gist Ltd

- 6.4.9 Gregory Distribution Ltd

- 6.4.10 GXO Logistics (Wincanton PLC)

- 6.4.11 Howard Tenens

- 6.4.12 Hoyer GmbH

- 6.4.13 Kinaxia Logistics Ltd

- 6.4.14 Marshalls Logistics

- 6.4.15 Nordic Transport Group A/S

- 6.4.16 Palletways

- 6.4.17 Turners (Soham) Ltd

- 6.4.18 United Parcel Service of America, Inc. (UPS)

- 6.4.19 W H Malcolm Ltd

- 6.4.20 XPO, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

西班牙公路貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印尼陸上貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

西班牙公路貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印尼陸上貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 2026-2030年全球公路貨運市場

2026-2030年全球公路貨運市場 2026年全球公路貨運市場報告

2026年全球公路貨運市場報告 陸上貨運市場:2026-2032年全球市場預測(依服務類型、貨物類型、所有權、車輛類型及最終用途分類)

陸上貨運市場:2026-2032年全球市場預測(依服務類型、貨物類型、所有權、車輛類型及最終用途分類) 公路貨運服務市場機會、成長促進因素、產業趨勢分析、預測(2026-2035年)美國公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本公路貨運:市佔率分析、產業趨勢與統計及成長預測(2026-2031)北美公路貨運市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

公路貨運服務市場機會、成長促進因素、產業趨勢分析、預測(2026-2035年)美國公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本公路貨運:市佔率分析、產業趨勢與統計及成長預測(2026-2031)北美公路貨運市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)