|

市場調查報告書

商品編碼

2066657

西班牙公路貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Spain Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

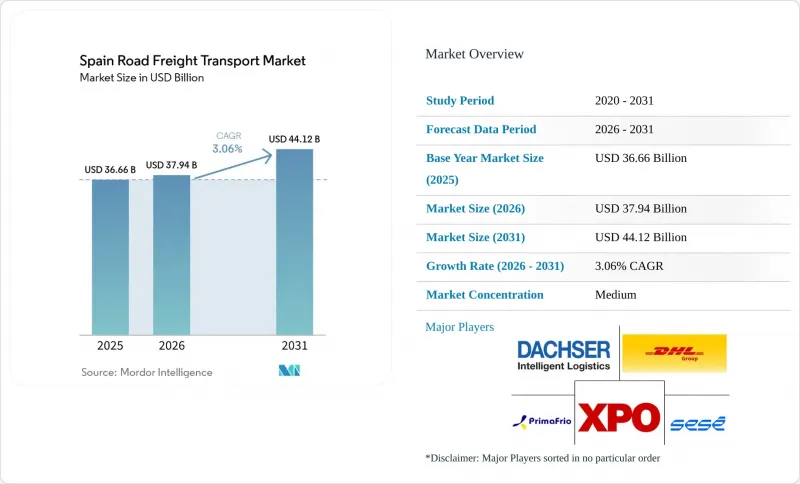

據 Mordor Intelligence 稱,2025 年西班牙公路貨運市場規模為 366.6 億美元,預計 2026 年將達到 379.4 億美元,到 2031 年將達到 441.2 億美元,預測期(2026-2031 年)複合年成長率為 3.06%。

西班牙公路貨運市場持續受惠於其超過95%的國內運輸佔有率、約15億噸的年公路貨運量,以及其作為地中海地區生產基地和通往大西洋門戶的雙重角色。本報告按終端用戶行業(例如農業)、目的地(例如國內)、整車負載容量(例如整車運輸)、容器化(例如貨櫃運輸)、運輸距離(例如長途運輸)、貨物類型(例如液體貨物)和溫度控制(例如溫控貨物)進行分類。市場預測以美元計價。

西班牙公路貨運市場趨勢與洞察

由於疫苗和高檔食品的出口,低溫運輸發展迅速。

預計到2024年,藥品出口額將達到184億歐元(216.4億美元),這些藥品需要2至8攝氏度的溫度控制,這推動了對符合GDP標準且具備即時監控能力的承運商的需求成長,並促使他們支付更高的費用。同時,價值620億歐元(729.3億美元)的高價值食品(例如有機柑橘和伊比利亞豬肉)的出口依賴不間斷的冷藏,因此需要全年運作以應對季節性波動。專業承運商正在利用基於區塊鏈的可追溯性和隔熱交換箱來提高利潤率。歐盟2017/625號法規規定的獸醫邊境檢查雖然增加了運輸停留時間,但也提升了合規承運商的價值。像Primafrio這樣的承運商正在使用專有的遠端資訊處理技術,繞過普通貨物運輸網路,與製藥廠商簽訂合約。

數位化貨運市場簡化了空車運輸流程。

該平台的實施已將空駛里程率從2020年的28%降低至2024年的22%,從而節省了1.8億歐元(2.1173億美元)的燃油成本,並使承運商的資產運轉率提高了12%至18%。運輸能力的即時可見性使得小批量貨物的預訂可在兩時限內完成,需求預測可提前24至48小時進行。小規模承運商現在可以直接取得托運人的運輸量,而隨著透明度的提高,仲介的利潤空間正在縮小。將海關程序、替代性爭議解決機制(ADR)和司機資格整合到預訂流程中,減少了繁瑣的行政手續,並加快了跨境運輸的發展。年輕的物流經理傾向於使用基於應用程式的採購方式,預計2024年數位交易量將年增35%。

歐盟流動方案:沿海運輸和休息期的合規負擔

根據2024年的規定,非居住者運輸業者每週最多只能進行三次沿海運輸,並且需要四天的冷卻期,這導致運營商成本增加了8%至12%。每四周強制返回本國的規定使北歐路線上的有效駕駛時間減少了15%至20%,迫使業者引入繼電器系統並增派司機。智慧行車記錄器的遠端監控消除了監管方面的灰色地帶。為了彌補與東道國之間的工資差距,在法國和德國運營的西班牙運輸業者的人事費用增加了高達30%。運輸公司正在邊境附近設立司機換班站以維持卡車的運轉率,但換班過程會帶來調度風險。

細分市場分析

到2025年,製造業將佔西班牙公路貨運市場佔有率的37.51%,這主要得益於245萬輛汽車的產量和強勁的藥品出口。加泰隆尼亞、阿拉貢和巴斯克地區工廠與港口之間穩定的零件流通將保障大宗運輸路線的暢通。批發和零售貿易正以3.52%的複合年成長率成長,這反映了依賴頻繁多地點訪問的全通路履約模式,並推動了小批量運輸的使用。預計到2026年,建築相關貨運將為歐盟資助的700億歐元(823.4億美元)計畫提供支持,之後將逐漸下降。在農業領域,柑橘和蔬菜出口的季節性高峰推動了對冷藏運輸能力的需求成長。

隨著製造商採用需要零售式分銷的直接面對消費者 (DTC) 策略,以及大型零售商進軍簡化組裝業務,不斷演變的經營模式導致行業界限日益模糊。這種混合模式迫使承運商提供靈活的服務項目。隨著近岸外包趨勢推動零件運輸,西班牙融合製造業和零售業的公路貨運市場預計將進一步擴張。來自不同行業的需求緩解了運輸量的波動,並有助於維持穩定的車輛運轉率。

到2025年,國內運輸將主導西班牙陸上貨運市場,佔其市場總規模的64.07%,這得益於該國4,700萬消費者以及區域分工。高密度運輸走廊連接加泰隆尼亞的工廠、安達盧西亞的農場和消費中心馬德里,為可預測的往返運輸提供了保障。都市區低排放氣體區的引入促使馬德里和巴塞隆納採取行動,加速了都市區電動車隊的普及。

國際貨運正以3.60%的複合年成長率快速成長,這得益於伊比利亞半島陸路運輸路線的拓展以及經由「馬爾哈巴行動」(Operation Marhaba)運往摩洛哥的貨運量創下歷史新高。歐盟的「流動性一攬子計畫」(Mobility Package)雖然增加了合規難度,但也為與低薪競爭對手創造了公平的競爭環境。目前正在審議中的直布羅陀海峽隧道計畫預示著未來連接北非的突破性舉措,但其影響預計要到2035年或更晚才能顯現。

汽車、農產品和建築材料的大規模出口使得整車運輸(FTL)保持了83.07%的市場佔有率。專用路線最佳化了駕駛人的工作時間,並減少了裝卸過程中的貨物損壞。基於生產計劃的往返行程規劃有效降低了成本。

西班牙零擔貨運 (LTL) 3.43% 的複合年成長率主要歸因於電子商務運輸量的減少以及西班牙公路貨運業向樞紐輻射式模式的轉變。數位化市場的引入使裝載率提升至近 90%,縮小了傳統的效率差距。運輸公司正在馬德里和瓦倫西亞附近投資建造自動化交叉轉運設施,以加快夜間分類週期。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 按經濟活動分類的GDP構成

- 按經濟活動分類的GDP成長率

- 經濟表現及概覽

- 電子商務產業的趨勢

- 製造業的發展趨勢

- 運輸和倉儲部門的GDP

- 物流績效

- 道路長度

- 出口趨勢

- 進口趨勢

- 燃油價格趨勢

- 卡車運輸營運成本

- 按車輛類型分類的卡車擁有數量

- 主要卡車供應商

- 公路貨運發展趨勢

- 陸上貨運價格趨勢

- 按交通途徑分享

- 通貨膨脹

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 疫苗和高階食品出口推動低溫運輸繁榮

- 數位化貨運市場簡化了回程傳輸。

- 獎勵使用低排放車輛,並支持車輛報廢。

- 英國脫歐後路線變更導致對伊比利亞高架橋的需求增加

- 超高容量風力發電廠項目

- 對32公尺超大型卡車的管制將提高運輸走廊的運輸能力。

- 市場限制因素

- 歐盟流動方案:與遵守沿海運輸和休息期相關的負擔

- 根據“Mercancias 30”計劃,補貼轉換為鐵路貨運。

- 地中海沿岸航運路線上的洪水相關保險費飆升。

- 貨櫃港口自動化進展緩慢,導致陸路交通擁擠。

- 市場上的技術創新

- 波特五力分析

第5章 市場規模與成長預測

- 按最終用戶行業分類

- 農業、漁業、林業

- 建造

- 製造業

- 石油和天然氣、採礦和採石

- 批發和零售

- 其他

- 按目的地

- 國內的

- 國際的

- 依卡車負載容量

- 整車運輸 (FTL)

- 小批量貨物(零擔)

- 透過容器化

- 容器化

- 容器化

- 按運輸距離

- 長途

- 短距離

- 按貨物類型

- 液態產品

- 實際產品

- 按類型進行溫度控制

- 無溫度控制

- 溫控型

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- AP Moller-Maersk

- DACHSER

- Almar Iberia Logistics

- Alonso Group(Transportes Alonso Salcedo)

- CMA CGM Group(CEVA Logistics)

- DHL Group

- DSV A/S

- FM Logistic

- Girteka

- Grupo Sese

- International Distributions Services(GLS)

- JSV Logistics

- La Poste Group(Seur Geopost)

- Marcotran

- Primafrio

- Rhenus Group

- Rohlig Logistics

- Transfesa Logistics

- Trucksters

- XPO, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the spain road freight transport market size was valued at USD 36.66 billion in 2025 and is projected to reach USD 37.94 billion in 2026 to USD 44.12 billion by 2031, at a 3.06% CAGR during the forecast period (2026-2031).

High domestic modal share above 95%, annual road-borne freight volumes near 1.5 billion Tons, and the country's dual role as Mediterranean production hub and Atlantic gateway continue to anchor the Spain road freight transport market. This report is Segmented by End User Industry (Agriculture, and More), by Destination (Domestic, and More), by Truckload Specification (FTL, and More), by Containerization (Containerized, and More), by Distance (Long Haul, and More), by Goods Configuration (Fluid Goods, and More), by Temperature Control (Temperature Controlled, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Road Freight Transport Market Trends and Insights

Cold-Chain Boom from Vaccine and Premium Food Exports

Pharmaceutical exports worth EUR 18.4 billion (USD 21.64 billion) in 2024 required 2-8 °C integrity, expanding premium-rate demand for GDP-compliant carriers equipped with real-time monitoring. Simultaneously, EUR 62 billion (USD 72.93 billion) in high-value food exports such as organic citrus and Iberian pork hinge on unbroken refrigeration, generating year-round utilization that mitigates seasonality. Specialized fleets adopt blockchain-enabled traceability and insulated swap bodies to capture margin uplift. Veterinary border inspections under EU 2017/625 add transit dwell but reinforce the value of compliance-certified providers. Operators like Primafrio leverage proprietary telematics to win contracts from pharmaceutical manufacturers that shun general freight networks.

Digital Freight Marketplaces Streamline Backhauls

Platform adoption lowered empty running from 28% in 2020 to 22% in 2024, saving EUR 180 million (USD 211.73 million) in fuel and improving carrier asset utilization by 12-18%. Real-time capacity visibility enables partial-load booking within two-hour windows and demand forecasting 24-48 hours ahead. Smaller fleets gain direct access to shipper volumes, but broker margins compress as transparency rises. Integration of customs, ADR, and driver credentials into booking workflows cuts paperwork friction, accelerating cross-border uptake. Youthful logistics managers favor app-based procurement, pushing digital transactions up 35% year-over-year in 2024.

EU Mobility Package Cabotage and Rest-Time Compliance Burden

The 2024 rules cap non-resident carriers at three cabotage trips in seven days and enforce four-day cooling-off periods, lifting operator costs 8-12%. Mandatory home return every four weeks reduces productive driving by 15-20% on Northern Europe runs, compelling relay systems or extra drivers. Smart tachographs enable remote enforcement, removing gray zones. Wage alignment with host countries inflates Spanish carrier labor cost up to 30% in France or Germany. Fleets deploy driver-swap hubs near borders to protect truck utilization, but handovers introduce scheduling risk.

Other drivers and restraints analyzed in the detailed report include:

- Low-Emission Fleet Incentives and Scrappage Schemes

- Iberian Land-Bridge Demand Post-Brexit Rerouting

- Rail-Freight Subsidy Shift Under Mercancias 30 Program

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing contributed 37.51% of Spain road freight transport market share in 2025, underpinned by 2.45 million vehicle outputs and robust pharmaceutical exports. Consistent component flows between Catalonia, Aragon, and Basque plants and ports sustain high-volume lanes. Wholesale and retail trade, scaling at a 3.52% CAGR, mirrors omnichannel fulfillment patterns that depend on frequent multi-stop rounds, stimulating less-than-truck-load uptake. Construction freight rides EUR 70 billion (USD 82.34 billion) EU-funded projects through 2026 before tapering. Agriculture's seasonal peaks in citrus and vegetable exports intensify refrigerated capacity requirements.

Evolving models blur boundaries as manufacturers adopt direct-to-consumer strategies needing retail-style distribution, while large retailers move into light assembly. This hybridization compels carriers to offer flexible service menus. The Spain road freight transport market for manufacturing and retail combined is projected to widen further as nearshoring trends spark incremental component shipments. Diverse sectoral demand smooths volume volatility and underpins steady fleet utilization.

Domestic shipments dominated with 64.07% of the Spain road freight transport market size in 2025 backed by the nation's 47 million consumers and inter-regional specializations. High-density corridors connect Catalonia's factories, Andalusia's farms, and Madrid's consumption hub, supporting predictable backhauls. Urban low-emission zones force adaptation in Madrid and Barcelona, catalyzing electric urban fleets.

International freight expands faster at 3.60% CAGR as Iberian land-bridge routes grow and Morocco traffic via Operation Marhaba sets new records. The EU Mobility Package complicates compliance but levels the playing field against low-wage competitors. Pending Gibraltar Strait tunnel studies hint at transformative future links to North Africa, yet impacts remain post-2035.

Full-truck-load maintained 83.07% market share owing to large batch exports of autos, produce, and construction material. Dedicated routes optimize driver hours and reduce handling damage. Savings accrue from consistent round-trip planning anchored by production calendars.

Less-than-truck-load's 3.43% CAGR traces back to e-commerce parcelization and the Spain road freight transport industry pivot to hub-and-spoke. Digital marketplaces raise load factors toward 90%, closing the historical efficiency gap. Operators invest in automated cross-docks near Madrid and Valencia to speed nightly sort cycles.

List of Companies Covered in this Report:

- A.P. Moller-Maersk

- DACHSER

- Almar Iberia Logistics

- Alonso Group (Transportes Alonso Salcedo)

- CMA CGM Group (CEVA Logistics)

- DHL Group

- DSV A/S

- FM Logistic

- Girteka

- Grupo Sese

- International Distributions Services (GLS)

- JSV Logistics

- La Poste Group (Seur Geopost)

- Marcotran

- Primafrio

- Rhenus Group

- Rohlig Logistics

- Transfesa Logistics

- Trucksters

- XPO, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 Cold-Chain Boom from Vaccine and Premium Food Exports

- 4.20.2 Digital Freight Marketplaces Streamline Backhauls

- 4.20.3 Low-Emission Fleet Incentives and Scrappage Schemes

- 4.20.4 Iberian Land-Bridge Demand Post-Brexit Rerouting

- 4.20.5 Wind-Farm Component Super-Load Projects

- 4.20.6 32-m Mega-Truck Regulations Enhance Corridor Capacity

- 4.21 Market Restraints

- 4.21.1 EU Mobility Package Cabotage and Rest-Time Compliance Burden

- 4.21.2 Rail-Freight Subsidy Shift under Mercancias 30 Program

- 4.21.3 Flood-Related Insurance Premium Escalation on Mediterranean Routes

- 4.21.4 Container-Port Automation Delays Causing Landside Congestion

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 By Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 By Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 By Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 By Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 By Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 By Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 A.P. Moller-Maersk

- 6.4.2 DACHSER

- 6.4.3 Almar Iberia Logistics

- 6.4.4 Alonso Group (Transportes Alonso Salcedo)

- 6.4.5 CMA CGM Group (CEVA Logistics)

- 6.4.6 DHL Group

- 6.4.7 DSV A/S

- 6.4.8 FM Logistic

- 6.4.9 Girteka

- 6.4.10 Grupo Sese

- 6.4.11 International Distributions Services (GLS)

- 6.4.12 JSV Logistics

- 6.4.13 La Poste Group (Seur Geopost)

- 6.4.14 Marcotran

- 6.4.15 Primafrio

- 6.4.16 Rhenus Group

- 6.4.17 Rohlig Logistics

- 6.4.18 Transfesa Logistics

- 6.4.19 Trucksters

- 6.4.20 XPO, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

英國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)印尼陸上貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

英國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)印尼陸上貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 2026-2030年全球公路貨運市場

2026-2030年全球公路貨運市場 2026年全球公路貨運市場報告

2026年全球公路貨運市場報告 陸上貨運市場:2026-2032年全球市場預測(依服務類型、貨物類型、所有權、車輛類型及最終用途分類)

陸上貨運市場:2026-2032年全球市場預測(依服務類型、貨物類型、所有權、車輛類型及最終用途分類) 公路貨運服務市場機會、成長促進因素、產業趨勢分析、預測(2026-2035年)美國公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本公路貨運:市佔率分析、產業趨勢與統計及成長預測(2026-2031)北美公路貨運市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

公路貨運服務市場機會、成長促進因素、產業趨勢分析、預測(2026-2035年)美國公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本公路貨運:市佔率分析、產業趨勢與統計及成長預測(2026-2031)北美公路貨運市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)