|

市場調查報告書

商品編碼

2035140

日本公路貨運:市佔率分析、產業趨勢與統計及成長預測(2026-2031)Japan Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

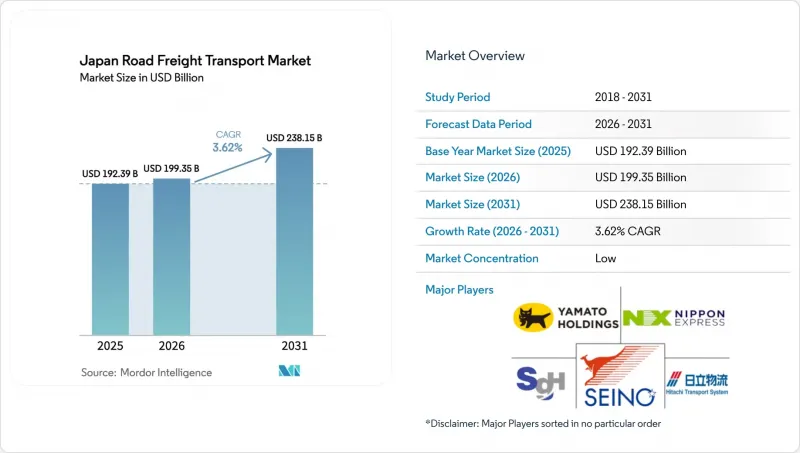

據估計,日本公路貨運市場規模在 2026 年將達到 1,993.5 億美元,高於 2025 年的 1,923.9 億美元,預計到 2031 年將達到 2,381.5 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 3.62%。

需求成長的動力源自於電子商務交易量的成長、批發零售業的蓬勃發展以及高速公路的建設縮短了運輸時間。同時,2024年4月生效的每位卡車駕駛人每年960小時加班時間上限,迫使業者重新評估其車輛部署和成本結構,並採用繼電器運輸、雙掛車和自動路線規劃等方式。擁有多元化車隊和技術投資預算的大型運輸公司正將這些限制轉化為提高利潤率的機遇,而中小企業則面臨著單位成本上升和議價能力下降的困境。除了藥品和生鮮食品對低溫運輸的需求不斷成長外,政府鼓勵散裝貨物轉向鐵路運輸的政策也進一步影響企業的競爭策略。

日本公路貨運市場趨勢與洞察

電子商務的快速成長和小包裹的激增

隨著小包裹量從2016年的39億件增加到2021年的48億件,配送時限不斷縮短,承運商被迫部署自動化分類系統和微型倉配中心。小批量、高頻次的貨運量正在取代大宗訂單,導致配送中心密度增加,車輛利用模式也隨之重組。大型平台正在投資建造區域配送中心,以兌現次日達的承諾,而末端配送車輛則採用路線最佳化軟體來彌補人手不足。東京-大阪走廊的運輸能力壓力最為顯著,因為該地區是消費需求的集中地。隨著小包裹量的持續成長,快速履約服務正在支撐日本的公路貨運市場。

2024年物流改革與價格透明度

960小時加班上限揭示了卡車運輸的真實成本,賦予承運商重新談判運費的權力。大型供應商迅速將增加的人事費用轉嫁給托運人,而小型企業則因加班柔軟性的喪失而面臨意想不到的成本上漲。價格透明度迫使零售商和製造商根據實際的運輸預算重新設計供應鏈。承運商現在掌握了談判主導,從而實現了期待已久的利潤率復甦,尤其是在運輸能力緊張的區域路線上。

960小時駕駛時限以下,司機嚴重短缺

調查顯示,81.4%的運輸公司無法招募足夠的司機,其中長途運輸公司受到的衝擊最大。過去,過度加班掩蓋了人手不足,但法律限制暴露了這個問題。如果不採取措施,到2026年,三分之一的車輛可能面臨停駛。由於生活方式的考慮,年輕一代對卡車駕駛人望而卻步,而退休人數卻持續成長。除非協同配送和自動駕駛解決方案廣泛應用,否則區域間貨運很可能會出現缺口。

細分市場分析

至2025年,批發和零售貿易將佔日本公路貨運市場規模的46.05%,預計2026年至2031年將以4.05%的複合年成長率成長。整合的全通路模式將門市補貨與直接配送至消費者結合,使承運商能夠整合快速消費的日用品和耐用消費品的運輸。更高的運輸頻率推動了對城市中心郊區(房地產稀缺且昂貴)越庫作業中心的需求。倉儲業正在引入機器人分類機,以應對閃購期間小包裹的激增。儘管製造業運輸量依然龐大,但精實生產實務正在降低單位產品的卡車行駛里程。建築物流將受到公共工程支出週期和與海岸防護設施維修相關的大型企劃的驅動。

人口老化正在重塑當地的消費趨勢,並促使各地方政府實施醫療物資配送和食品補給計畫。生鮮食品和藥品批發低溫運輸的日益複雜化,推高了專業運輸車輛的利潤率。同時,儘管石油和採礦業的需求保持穩定,但由於能源轉型和石化燃料運輸量的減少,其成長速度較為緩慢,但該行業龐大的規模表明,它將繼續在日本公路貨運市場中佔據主導地位。

這個市場仍然完全是國內市場,這反映了日本作為島國的地理位置及其複雜的國內貿易結構。在進出口貿易中,道路運輸僅用於港口、機場和內陸設施之間的「首公里」和「末公里」運輸。

高速公路的不斷擴建、收費系統的更新以及物流中心智慧閘門技術的引入,正在提高國內路線的效率,並保持日本公路貨運市場的成長動能。

2025年,整車運輸(FTL)作為工廠和物流中心之間大規模運輸的關鍵環節,仍將維持82.35%的市場佔有率。然而,受電商訂單分散化的推動,輕型貨車運輸(LTL)的成長率最高,2026年至2031年的複合年成長率(CAGR)將達到4.02%。數位市場將小批量貨物與貨車裝載空間進行匹配,提高了裝載效率並降低了單位成本。中轉營運幫助整車運輸車輛在遵守駕駛員工時規定的同時,維持幹線運輸的正常時間表。輕型貨車運輸的靈活性與零售策略相契合,有助於最大限度地減少庫存,並支持微型倉配中心的持續補貨。

零擔貨運的成長迫使承運商投資於動態路線規劃演算法,以減少空駛里程。位於高速公路交匯處的收貨點將來自不同托運人的小包裹集中到同一條路線上,從而提高了網路密度。零擔貨運的發展凸顯了日本公路貨運業向更靈活的物流模式轉變的結構性趨勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 按經濟活動分類的GDP構成

- 按經濟活動分類的GDP成長率

- 經濟表現及概覽

- 電子商務產業趨勢

- 製造業的發展趨勢

- 運輸和倉儲部門的GDP

- 物流績效

- 道路長度

- 出口趨勢

- 進口趨勢

- 燃油價格趨勢

- 卡車運輸營運成本

- 按車輛類型分類的運輸卡車數量

- 主要卡車供應商

- 公路貨運發展趨勢

- 公路貨運價格趨勢

- 按交通方式分享

- 通貨膨脹

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 電子商務的快速成長和小包裹的激增

- 2024年透過物流改革實現價格透明化

- 高速公路擴建及25公尺雙拖車通行許可

- 當日送達和低溫運輸發展

- 引進自動駕駛卡車專用車道

- 「自動流道路」輸送機走廊概念

- 市場限制因素

- 由於960小時駕駛時間限制,司機嚴重短缺。

- 柴油燃料成本增加,中小企業通行費上漲。

- 利用率低於35%,托盤標準化率達12%。

- 由於客運車輛過多,高速公路出現交通阻塞。

- 市場上的技術創新

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 需求者產業

- 農業、漁業、林業

- 建造

- 製造業

- 石油和天然氣、採礦和採石

- 批發和零售

- 其他

- 送貨地址

- 國內的

- 國際的

- 卡車裝載規範

- 全軌道公路(FTL)

- 小批量貨物(零擔)

- 貨櫃運輸

- 貨櫃運輸

- 非貨櫃運輸

- 距離

- 長途

- 短程交通

- 貨物形式

- 液體貨物

- 固體貨物

- 溫度控制

- 無溫度控制

- 具備溫度控制功能

第6章 競爭情勢

- 市場集中度

- 重大策略舉措

- 市佔率分析

- 公司簡介

- DHL Group

- Fukuyama Transporting Co., Ltd.

- Japan Post Co., Ltd.

- KRS Corporation

- Kintetsu Group Holdings Co., Ltd.

- Konoike Group(including Konoike Transport Co., Ltd.)

- LOGISTEED, Ltd.

- Marubeni Logistics Corporation

- Mitsui-Soko Holdings Co., Ltd.

- MOL Logistics Co., Ltd.

- Nippon Express Holdings

- Nisshin Transportation Co., Ltd.

- NYK Line(Including Yusen Logistics Co., Ltd.)

- Sankyu, Inc.

- SBS Holdings, Inc.

- Seino Holdings Co., Ltd.

- Senko Group Holdings Co., Ltd.

- SG Holdings Co., Ltd.

- Trancom Co., Ltd.

- Yamato Transport Co., Ltd.

第7章 市場機會與未來展望

Japan road freight transport market size in 2026 is estimated at USD 199.35 billion, growing from 2025 value of USD 192.39 billion with 2031 projections showing USD 238.15 billion, growing at 3.62% CAGR over 2026-2031.

Demand momentum stems from e-commerce volume expansion, renewed wholesale and retail trade activity, and expressway upgrades that shorten transit times. At the same time, the April 2024 cap limiting each truck driver to 960 overtime hours a year reshapes fleet deployment and cost structures, compelling operators to adopt relay transport, double-trailer rigs, and automated route planning. Major carriers with diversified fleets and technology budgets convert these constraints into margin opportunities, whereas smaller firms confront higher unit costs and shrinking bargaining power. Growing cold-chain needs in pharmaceuticals and fresh food, coupled with government programs to shift bulk cargo to rail, further influence competitive strategy.

Japan Road Freight Transport Market Trends and Insights

E-Commerce Boom and Parcel Proliferation

Parcel volumes climbed from 3.9 billion in fiscal 2016 to 4.8 billion in fiscal 2021, compressing delivery windows and pushing carriers to adopt automated sortation and micro-fulfillment hubs. Smaller, more frequent shipments replace bulk orders, raising stop density and reshaping vehicle-utilization models. Major platforms invest in regional distribution centers to meet one-day commitments, while last-mile fleets integrate routing software to offset labor constraints. Capacity strain is most evident along the Tokyo-Osaka corridor where consumer demand concentrates. Fast fulfillment promises sustain the Japan road freight transport market as parcel volumes continue their upward trend.

2024 Logistics-Reform Price Transparency

The 960-hour overtime ceiling exposes true trucking costs, giving carriers leverage to renegotiate rates. Large providers swiftly passed higher labor costs to shippers, while SME operators experienced sticker-shock from shrinking overtime flexibility. Transparent pricing forces retailers and manufacturers to redesign supply chains with realistic freight budgets. Negotiation dynamics now favor carriers, allowing long-overdue margin recovery, especially for rural routes where capacity is tight.

Acute Driver Shortage Under 960 H Cap

Surveys show 81.4% of carriers cannot recruit enough drivers, with long-haul operators worst hit. Excess overtime once masked labor scarcity; legal limits now expose a deficit that may ground one-third of fleets by 2026 if unaddressed. Young workers reject trucking due to lifestyle concerns, while retirements accelerate. Regional freight could face service gaps unless collaborative delivery or autonomous solutions scale quickly.

Other drivers and restraints analyzed in the detailed report include:

- Expressway Expansion and 25 M Double-Trailer Permits

- Same-Day Delivery and Cold-Chain Growth

- Rising Diesel and Toll Costs for SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wholesale and retail trade generated 46.05% of the Japan road freight transport market size in 2025 and is forecast to have a 4.05% CAGR between 2026-2031. Integrated omnichannel models merge store restocking with direct-to-consumer parcels, allowing carriers to pool volumes across fast-moving consumables and durable goods. High shipment frequency raises demand for cross-docking hubs near urban centers where real estate is scarce and expensive. Warehouses deploy robotic sorters to manage parcel surges during flash-sale events. Manufacturing traffic remains sizeable, but lean production curbs truck-kilometers per unit. Construction logistics hinges on public works spending cycles and mega-projects related to coastal protection upgrades.

Aging populations shape rural consumption trends, prompting medical supply deliveries and grocery replenishment programs run by municipal governments. Cold-chain complexity grows in fresh food and pharmaceutical wholesale, strengthening margins for specialized fleets. Meanwhile, the oil and mining sectors retain stable but low-growth demand as the energy transition moderates fossil-fuel transport volumes. The segment's scale ensures its continued dominance within the Japan road freight transport market.

The market remains 100% domestic, reflecting Japan's island geography and intricate internal trade flows. Imports and exports rely on road transport only for first and last mile moves between ports or airports and inland facilities.

Continued expressway expansion, updated tolling systems, and smart-gate technology at distribution centers sharpen domestic route efficiency and sustain the Japan road freight transport market's growth trajectory.

Full-truck-load kept 82.35% share in 2025 as it remains indispensable for bulk shipments between factories and distribution centers. Still, less-than-truck-load recorded the top growth rate at 4.02% CAGR between 2026-2031 on the back of e-commerce order fragmentation. Digital marketplaces match smaller consignments with truck space, lifting load factors and lowering cost per unit. Relay operations help FTL fleets comply with driver work-hour rules while maintaining line-haul schedules. LTL's agility meets inventory-light retail strategies, supporting continuous replenishment of micro-fulfillment sites.

Growth in LTL nudges carriers to invest in dynamic routing algorithms that cut empty mileage. Consolidation depots positioned at expressway interchanges combine different shippers' parcels into single runs, improving network density. The progress of LTL confirms a structural pivot toward flexible distribution within the Japan road freight transport industry.

The Japan Road Freight Transport Market Report is Segmented by End User Industry (Manufacturing, and More), Destination (Domestic and International), Truckload Specification (FTL and LTL), Distance (Long Haul and Short Haul), Goods Configuration (Fluid Goods and Solid Goods), Temperature Control (Non-Temperature and Temperature Controlled), and by Containerization. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL Group

- Fukuyama Transporting Co., Ltd.

- Japan Post Co., Ltd.

- K R S Corporation

- Kintetsu Group Holdings Co., Ltd.

- Konoike Group (including Konoike Transport Co., Ltd.)

- LOGISTEED, Ltd.

- Marubeni Logistics Corporation

- Mitsui-Soko Holdings Co., Ltd.

- MOL Logistics Co., Ltd.

- Nippon Express Holdings

- Nisshin Transportation Co., Ltd.

- NYK Line (Including Yusen Logistics Co., Ltd.)

- Sankyu, Inc.

- SBS Holdings, Inc.

- Seino Holdings Co., Ltd.

- Senko Group Holdings Co., Ltd.

- SG Holdings Co., Ltd.

- Trancom Co., Ltd.

- Yamato Transport Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 E-Commerce Boom and Parcel Proliferation

- 4.20.2 2024 Logistics-Reform?Driven Price Transparency

- 4.20.3 Expressway Expansion and 25 M Double-Trailer Permits

- 4.20.4 Same-Day Delivery and Cold-Chain Growth

- 4.20.5 Dedicated Autonomous Truck Lanes Roll-Out

- 4.20.6 "Autoflow-Road" Conveyor-Belt Corridor Vision

- 4.21 Market Restraints

- 4.21.1 Acute Driver Shortage Under 960 H Cap

- 4.21.2 Rising Diesel and Toll Costs for SMEs

- 4.21.3 <35 % Load Factor and 12 % Pallet Standardization

- 4.21.4 Passenger Traffic-induced Expressway Congestion

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Fukuyama Transporting Co., Ltd.

- 6.4.3 Japan Post Co., Ltd.

- 6.4.4 K R S Corporation

- 6.4.5 Kintetsu Group Holdings Co., Ltd.

- 6.4.6 Konoike Group (including Konoike Transport Co., Ltd.)

- 6.4.7 LOGISTEED, Ltd.

- 6.4.8 Marubeni Logistics Corporation

- 6.4.9 Mitsui-Soko Holdings Co., Ltd.

- 6.4.10 MOL Logistics Co., Ltd.

- 6.4.11 Nippon Express Holdings

- 6.4.12 Nisshin Transportation Co., Ltd.

- 6.4.13 NYK Line (Including Yusen Logistics Co., Ltd.)

- 6.4.14 Sankyu, Inc.

- 6.4.15 SBS Holdings, Inc.

- 6.4.16 Seino Holdings Co., Ltd.

- 6.4.17 Senko Group Holdings Co., Ltd.

- 6.4.18 SG Holdings Co., Ltd.

- 6.4.19 Trancom Co., Ltd.

- 6.4.20 Yamato Transport Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

西班牙公路貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)英國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)印尼陸上貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

西班牙公路貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)英國公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)印尼陸上貨運:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 2026-2030年全球公路貨運市場

2026-2030年全球公路貨運市場 2026年全球公路貨運市場報告

2026年全球公路貨運市場報告 陸上貨運市場:2026-2032年全球市場預測(依服務類型、貨物類型、所有權、車輛類型及最終用途分類)

陸上貨運市場:2026-2032年全球市場預測(依服務類型、貨物類型、所有權、車輛類型及最終用途分類) 公路貨運服務市場機會、成長促進因素、產業趨勢分析、預測(2026-2035年)美國公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美公路貨運市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

公路貨運服務市場機會、成長促進因素、產業趨勢分析、預測(2026-2035年)美國公路貨運:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南公路貨運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美公路貨運市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)