|

市場調查報告書

商品編碼

2063488

日本瓦楞紙板包裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Japan Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

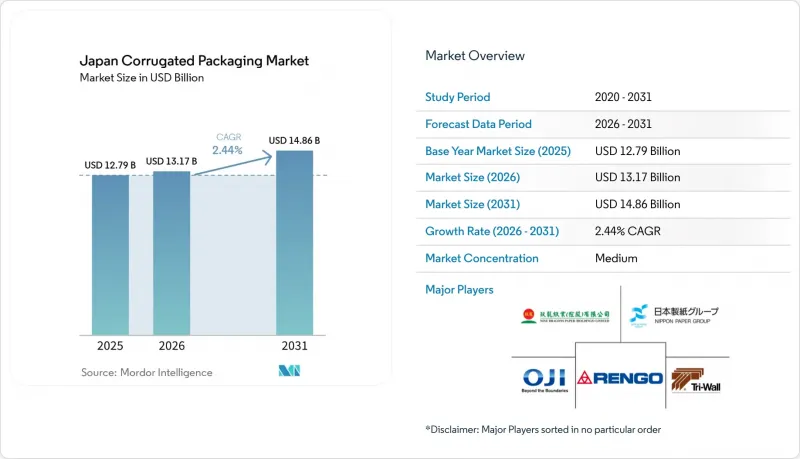

根據 Mordor Intelligence 預測,日本瓦楞紙板包裝市場規模將從 2025 年的 127.9 億美元和 2026 年的 131.7 億美元成長到 2031 年的 148.6 億美元,2026 年至 2031 年的複合年成長率為 2.4%。

本報告依材料(原生牛皮箱紙板、再生紙板等)、瓦楞類型(A型瓦楞、B型瓦楞等)、包裝類型(普通開槽紙盒等)、壁厚結構(單層、雙層等)、印刷技術(柔版印刷等)和終端用戶行業(加工食品等)進行分類。市場預測以美元計價。

日本瓦楞紙板包裝市場的趨勢與洞察

加速電子商務物流

日本消費者線上消費額高達26.1兆日圓(約1,864億美元),線上銷售額佔零售總額的近10%,小包裹處理量也因此穩定成長。光是食品線上銷售額就高達3.12兆日圓(約223億美元),推動了對隔熱防漏瓦楞紙箱的需求,以取代笨重的發泡聚苯乙烯冷藏箱。跨境購物額高達5.78兆日圓(約413億美元),也催生了符合中美兩國標籤規定的出口包裝盒的需求。訂閱式化妝品和D2C保健品牌的興起,增加了小包裹的遞送頻率,因此可根據需求客製化尺寸的數位印刷包裝袋更受歡迎。物流公司目前更傾向於使用更薄的瓦楞紙板和更精準的模切工藝,以最佳化卡車裝載效率和體積重量計費。

擴大加工食品和飲料的出口

預計到2025年,日本農產品和食品出口將成長12.8%,達到創紀錄的121億美元。這將推動對具有防潮性能和三層層級構造以增強承重能力的出口認證瓦楞紙板的需求成長。光是扇貝就佔6.5億美元(906億美元),需要冷藏散裝箱包裝;抹茶粉出口額幾乎加倍,達到5.2億美元(721億美元),促使加工商轉向使用更輕的E型瓦楞零售包裝。日本食品對美國的進口量增加了13.7%,對中國的進口量也增加了7.0%。這導致對能夠承受長途海運並在目的地港可回收的阻隔塗層瓦楞紙板提出了更嚴格的要求。

再生紙價格波動

2025年初,OCC(油瓦楞紙箱)的出口價格徘徊在每噸170至175美元左右,但隨著中國需求的激增,價格可能在幾週內上漲10至15美元。日本造紙商98%的原料依賴再生紙,由於向客戶調整價格的時間延遲一到兩個季度,他們正面臨利潤波動。雖然農曆新年期間需求的季節性放緩將暫時緩解壓力,但潛在的需求上升趨勢正在限制那些簽訂固定價格零售合約的加工商的利潤率。

細分市場分析

到2025年,再生箱板紙將佔日本瓦楞紙板包裝市場53.26%的佔有率,體現了日本世界領先的纖維回收系統。王子控股等國內大型企業營運的箱板紙工廠幾乎全部採用再生材料製成,為品牌商提供價格具競爭力的低碳供應鏈。原生牛皮紙在冷藏水產品和牛肉的海外運輸領域佔據著雖小但重要的市場佔有率,因為濕度會影響紙板的強度。半化學瓦楞紙板預計到2031年將以4.21%的複合年成長率成長,其優異的剛度重量比使其比傳統A型瓦楞紙板的材料用量減少了8.7%。在創新方面,大王製紙於2025年中期實現了纖維素奈米纖維複合材料的商業化。這種複合材料能夠製造出更薄的核心材料,且在承受上方壓力時不會變形。

這些複合材料也符合一項新的監管清單,該清單限制使用未經批准的黏合劑和塗料,鼓勵加工商採用單一材料結構。半化學產品對以體積重量收費、向都市區微型倉配中心出貨的電商小包裹尤其具有吸引力。牛皮紙食品出口商指出,其抗壓性能的提升可顯著減少長途運輸過程中因凹陷造成的索賠,降幅達兩位數。同時,原生牛皮紙供應商正在增加國內軟木的採購量,以對沖北美紙漿進口價格波動所帶來的風險。日本製紙木材公司計劃在2026會計年度之前採購100萬立方米軟木,這一趨勢便印證了這一點。

B型瓦楞紙板憑藉其3毫米的厚度,在緩衝性和體積效率之間取得了平衡,因此仍佔38.13%的貨運量,尤其是在飲料多包裝和便利商店補貨領域。然而,厚度僅1.5毫米的E型瓦楞紙板,由於托運人希望避免最後一公里配送卡車的體積重量費用,其年成長率高達3.73%。數位印刷商青睞E型瓦楞紙板光滑的表面,該表面能夠完美呈現1200dpi的圖像而不會出現紙襯翹曲,使其成為化妝品和糖果甜點行業的標準選擇。 Rengo公司領先的「三角瓦楞紙板」 (Delta Flute)厚度為2毫米,定位介於兩者之間,為零售商提供了一種「更輕、更低碳」的選擇,同時仍能承受嚴苛的分揀流程。

高階巧克力製造商現在指定使用G型瓦楞紙板製作禮盒,因為其厚度小於1毫米,既能實現可伸縮的盒蓋結構,又能保持盒體的剛性。加工商正在投資高精度瓦楞紙板生產設備和雷射壓紋機,以將微瓦楞紙板的厚度控制在±0.05毫米的公差範圍內。對於易碎的電子產品和玻璃製品,具有5毫米緩衝作用的A型瓦楞紙板仍然十分重要,但其重量增加的缺點阻礙了瓦楞紙板在日本包裝市場的全面復甦。瓦楞紙板種類的不斷豐富清楚地表明,隨著SKU數量的增加,紙盒製造商不得不選擇適合自身供應鏈經濟效益的紙板形狀,而不是依賴「通用」標準。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速電子商務物流

- 加工食品和飲料出口成長

- 監理政策轉向可回收包裝

- 近岸外包主導的電子產品生產

- 精釀啤酒廠對客製化包裝盒的需求

- 政府對生物基阻隔塗料的補貼

- 市場限制因素

- 再生紙價格波動

- 與可回收塑膠箱的競爭

- 麵粉廠缺水造成了許多限制。

- 對進口原生纖維的依賴

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 維珍工藝襯板

- 再生襯紙板

- 瓦楞紙板基紙

- 半化學蝕刻

- 其他材料

- 長笛類型

- 長笛

- 低音長笛

- C調長笛

- E 長笛

- F調長笛

- 按包裝類型

- 普通插槽容器

- 客製化模切盒

- 折疊紙箱

- 商店展示

- 托盤箱

- 其他包裝類型

- 依牆體類型

- 單層

- 雙層壁

- 三層壁

- 一邊

- 透過印刷技術

- 柔版印刷

- 數位噴墨列印

- Riso層壓

- 網版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 加工食品

- 生鮮食品和農產品

- 飲料

- 電器產品

- 個人護理化妝品

- 電子商務履約中心

- 製藥

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Dynapac Co., Ltd.

- Tri-Wall Limited

- Asahi Printing Co., Ltd.

- Nine Dragons Paper(Holdings)Limited

- Kyokuto Fatty-Acid

- Kyoshin Paper & Package

- Tokan Kogyo Co., Ltd.

- Nishiyama(NDK)Co., Ltd.

- Rengo Co., Ltd.

- Oji Holdings Corporation

- Nippon Paper Industries Co., Ltd.

- Daio Paper Corporation

- Chuoh Pack Industry Co., Ltd.

- Tomoku Co., Ltd.

- Ito Corrugated Industrial Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan corrugated packaging market size is projected to expand from USD 12.79 billion in 2025 and USD 13.17 billion in 2026 to USD 14.86 billion by 2031, registering a CAGR of 2.44% between 2026 and 2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, and More), Flute Type (A Flute, B Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single-Wall, Double-Wall, and More), Printing Technology (Flexographic Printing, and More), End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

Japan Corrugated Packaging Market Trends and Insights

Rising E-Commerce Logistics Acceleration

Parcel volumes keep rising as Japanese shoppers spend JPY 26.1 trillion (USD 186.4 billion) online, with penetration close to 10% of national retail sales. Online grocery alone accounted for JPY 3.12 trillion (USD 22.3 billion), requiring insulated, leak-resistant corrugated shippers that replace bulky EPS coolers. Cross-border purchases valued at JPY 5.78 trillion (USD 41.3 billion) create export-grade box requirements that meet China and U.S. labeling rules. Subscription cosmetics and D2C health brands increase the frequency of small parcels, favoring digitally printed mailers that can be right-sized on demand. Logistics companies now optimize truck cube and dimensional-weight fees, so thinner flutes and precise die cuts are preferred.

Growth in Processed Food and Beverage Exports

Japan's farm and food exports climbed 12.8% in 2025 to a record USD 12.1 billion, boosting demand for export-certified corrugated with moisture barriers and triple-wall stacking strength. Scallops alone contributed JPY 90.6 billion (USD 0.65 billion), requiring refrigerated bulk boxes, while powdered matcha nearly doubled to JPY 72.1 billion (USD 0.52 billion), prompting converters to shift toward lightweight E-flute retail packs. U.S. imports of Japanese foods grew 13.7%, and China rebounded 7.0%, tightening specifications for corrugated barrier coatings that can withstand long sea journeys while remaining recyclable at destination ports.

Recycled Paper Price Volatility

OCC export prices hovered at USD 170-175 per tonne in early 2025, yet Chinese demand spikes can push quotations up USD 10-15 within weeks. Japanese mills that rely on 98% recovered paper feedstock face profit swings because customer price adjustments lag by one to two quarters. Seasonal Lunar New Year slowdowns momentarily ease pressure, but the underlying upswing limits the margin for converters serving fixed-price retail contracts.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Shift Toward Recyclable Packaging

- Nearshoring-Led Electronics Output

- Competition From Returnable Plastic Crates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard claimed 53.26% of the Japanese corrugated packaging market in 2025, mirroring the country's world-leading fiber recovery culture. Domestic majors such as Oji Holdings operate containerboard mills with recycled content approaching 100%, providing brand owners with a low-carbon supply chain at a competitive price. Virgin Kraft retains a small but critical niche for chilled seafood and overseas beef shipments, where humidity can jeopardize board integrity. Semi-chemical fluting is on a 4.21% CAGR trajectory to 2031, as its superior stiffness-to-weight ratio grants an 8.7% material saving versus legacy A flute. On the innovation front, Daio Paper commercialized cellulose nanofiber composites in mid-2025, which enable a thinner medium without flattening under top-load.

These composites also satisfy new regulatory lists that restrict non-approved adhesives and coatings, pushing converters to embrace single-material builds. Semi-chemical products are especially attractive to e-commerce shippers that ship volumetric-weight-priced parcels to urban micro-fulfillment centers. Craft food exporters point to crush resistance gains that cut denting claims by double digits on long hauls. Meanwhile, virgin kraft suppliers hedge volatility in imported North American pulp by increasing domestic softwood procurement, a move signaled by Nippon Paper Lumber's 1 million m3 target for FY 2026.

B-flute continues to command 38.13% of shipments thanks to its 3 mm profile that balances cushioning and cube efficiency for beverage multipacks and convenience-store restocks. Yet E-flute, at a slender 1.5 mm, is growing 3.73% a year as shippers try to dodge dimensional-weight charges on last-mile vans. Digital printers applaud E flute's smoother surface that reproduces 1200 dpi graphics without liner washboarding, making it the go-to choice for cosmetics and confectionery. Rengo's proprietary Delta Flute, launched earlier, sits midway at 2 mm, giving retailers a "less weight, less carbon" option that still survives rough sortation.

Premium chocolatiers now specify G flute for gift boxes because its sub-1 mm thickness allows telescoping lids while retaining rigidity. Converters invest in high-precision corrugators and laser embossers to keep micro-flute calipers within +-0.05 mm tolerance. For fragile electronics and glassware, the Japan corrugated packaging market keeps A flute relevant due to its 5 mm cushion, although weight penalties limit widespread comeback. The broadening flute portfolio underscores how SKU proliferation forces box makers to match board geometry to supply-chain economics rather than rely on a one-size-fits-all standard.

List of Companies Covered in this Report:

- Dynapac Co., Ltd.

- Tri-Wall Limited

- Asahi Printing Co., Ltd.

- Nine Dragons Paper (Holdings) Limited

- Kyokuto Fatty-Acid

- Kyoshin Paper & Package

- Tokan Kogyo Co., Ltd.

- Nishiyama (NDK) Co., Ltd.

- Rengo Co., Ltd.

- Oji Holdings Corporation

- Nippon Paper Industries Co., Ltd.

- Daio Paper Corporation

- Chuoh Pack Industry Co., Ltd.

- Tomoku Co., Ltd.

- Ito Corrugated Industrial Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-Commerce Logistics Acceleration

- 4.2.2 Growth in Processed Food and Beverage Exports

- 4.2.3 Regulatory Shift Toward Recyclable Packaging

- 4.2.4 Nearshoring-Led Electronics Output

- 4.2.5 Craft-Brewery Demand for Custom Boxes

- 4.2.6 Government Subsidies for Bio-Based Barrier Coatings

- 4.3 Market Restraints

- 4.3.1 Recycled Paper Price Volatility

- 4.3.2 Competition From Returnable Plastic Crates

- 4.3.3 Water-Scarcity Constraints on Mills

- 4.3.4 Dependence on Imported Virgin Fiber

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-commerce Fulfillment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Dynapac Co., Ltd.

- 6.4.2 Tri-Wall Limited

- 6.4.3 Asahi Printing Co., Ltd.

- 6.4.4 Nine Dragons Paper (Holdings) Limited

- 6.4.5 Kyokuto Fatty-Acid

- 6.4.6 Kyoshin Paper & Package

- 6.4.7 Tokan Kogyo Co., Ltd.

- 6.4.8 Nishiyama (NDK) Co., Ltd.

- 6.4.9 Rengo Co., Ltd.

- 6.4.10 Oji Holdings Corporation

- 6.4.11 Nippon Paper Industries Co., Ltd.

- 6.4.12 Daio Paper Corporation

- 6.4.13 Chuoh Pack Industry Co., Ltd.

- 6.4.14 Tomoku Co., Ltd.

- 6.4.15 Ito Corrugated Industrial Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)菲律賓瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國瓦楞紙板包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)菲律賓瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國瓦楞紙板包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。美國瓦楞紙包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印尼瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。美國瓦楞紙包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印尼瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)