|

市場調查報告書

商品編碼

2061749

中國瓦楞紙板包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

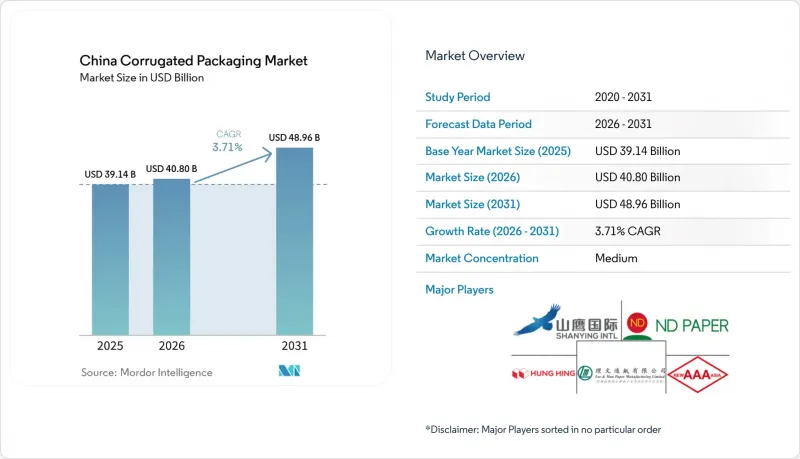

根據 Mordor Intelligence 預測,中國瓦楞紙板包裝市場規模預計到 2025 年將達到 391.4 億美元,到 2026 年將達到 408 億美元,到 2031 年將達到 489.6 億美元,2026 年至 2031 年的複合成長率為 3.71%。

本報告依材料(原生牛皮箱紙板、再生紙板、瓦楞紙核心材料等)、瓦楞類型(A型瓦楞等)、包裝類型(普通開槽紙盒等)、壁厚結構(單層、雙層等)、印刷技術(柔版印刷等)和終端用戶行業(加工食品等)進行細分。市場預測以美元計價。

中國瓦楞紙板包裝市場趨勢與洞察

電子商務履約需求不斷成長

2024年,中國處理了1,750億小包裹,其中瓦楞紙箱約佔68%。這鞏固了物流通路作為中國瓦楞紙包裝市場最大單一需求通路的地位。履約中心正從傳統的開槽紙箱轉向尺寸合適的模切紙箱,減少填充材,使自動化生產線能夠在30秒內完成包裝週期。京東物流在2024年減少了超過10億個二次包裝紙箱,迫使製造商的競爭不再局限於產量,而是前置作業時間、數位化客製化和設計精度。海南自貿港和粵港澳大灣區的跨境經銷商對符合國際航空運輸協會(IATA)體積重量規定的微型瓦楞紙箱有需求,儘管平均紙張厚度有所下降,但單位需求仍在持續成長。預計到 2025 年,即時電商將創造 4.9 兆元人民幣(6,800 億美元)的商品總值,它正在將包裝轉變為螢幕廣告,並促使品牌為可膠印、適合相機拍攝的運輸包裝盒支付 40-60% 的溢價。

加強環境法規,鼓勵可回收包裝

生態環境部已將瓦楞紙箱再生材料含量標準從先前的70%提高到2027年的85%。因此,2025年再生箱板紙的佔比穩定在63.21%。 2025年再生紙進口配額降至420萬噸的措施收緊了國內再生紙市場,導致價格年增12%。各省正在實施的生產者延伸責任制(EPR)試點計畫將回收成本轉嫁給品牌所有者,浙江和江蘇兩省正在加快輕質材料和替代纖維的試點推廣。在醫藥領域,新的T/CNPPA 3029-2025標準規定了低水蒸氣滲透性,使原生牛皮紙在低溫運輸紙盒方面具有監管優勢。大型造紙企業利用規模經濟來吸收廢水處理和揮發性有機化合物 (VOC) 對策方面的投資,而本地加工企業在「十四五」規劃期間卻面臨著利潤率下降 8% 至 12% 的困境。

再生紙進口政策的變化

預計到2025年,在雜質含量限制為0.3%的情況下,進口量將減少至420萬噸。這導致造紙企業面臨現貨市場價格飆漲的風險,清關時間也從7天延長至18天。國內再生紙(OCC)價格上漲了12%,給沒有自有造紙設施的加工商帶來了壓力。此外,儘管在可回收性方面有所妥協,但一些買家仍在轉向使用軟包裝袋。傳統上偏好使用美國長纖維廢紙的沿海造紙企業正在將資金重新配置到原生紙漿上。例如,九龍集團投資48億美元在北海建設的紙漿廠,年產能110萬噸化學紙漿。都市區瓦楞紙板廢棄物的收集系統仍然分散,35%的都市區瓦楞紙板廢棄物當作混合廢棄物收集,這增加了脫墨成本,削弱了小規模造紙企業的競爭力。

細分市場分析

到2025年,再生瓦楞紙板將佔中國瓦楞包裝市場63.21%的佔有率,這反映了到2027年宅配瓦楞紙箱強制使用85%再生材料的規定。一體化造紙企業正透過覆蓋全國的廢紙回收網路確保原料供應優勢,從而鞏固其成本競爭力。原生牛皮箱紙板預計將以4.77%的複合年成長率成長,超過整體市場增速,因為生鮮食品出口商和高階電商品牌對更高環壓強度、抗撕裂性和更光滑的印刷表面提出了更高的要求。九龍紙業北海工廠和利曼紙業對特種牛皮紙的升級改造正瞄準這個高階市場。瓦楞原紙生產商正在測試以竹子和稻草為原料的半化學漿,以規避軟木的風險,但由於這些紙漿對濕度敏感,目前仍僅限於低濕度物流路線。

為了在不使用蠟的情況下實現可回收性,生物基阻隔塗層和澱粉基黏合劑的試點生產正在擴大,這表明中國瓦楞紙包裝市場正呈現兩極分化:一方面是大規模生產的再生材料產品的利基市場,另一方面是規模較小但利潤豐厚的原生紙漿市場。同時,《中國國家藥品和包裝法》(T/CNPPA 3029-2025)中有關食品接觸和藥品的相關法規,正引導對溫度控制要求嚴格的應用轉向原生紙漿,從而確保價格緩衝,抵消不斷上漲的原料成本。因此,加工商的策略也呈現兩極化:通用型製造商追求再生箱板紙的效率,而高附加價值專業製造商則憑藉優質牛皮紙和功能性塗層吸引品牌商。

由於B型瓦楞紙板在緩衝性和成本方面兼顧,預計到2025年,其在中國瓦楞紙板包裝市場將佔34.15%的佔有率。然而,隨著跨境經銷商尋求最佳化體積重量,以及化妝品品牌對膠印圖案的需求增加,預計到2031年,F型瓦楞紙板的年複合成長率將達到4.15%。 F型瓦楞紙板的厚度(0.75-1.0毫米)可直接進行膠印,無需膠印覆膜,從而減少庫存體積。這對於高度限制的自動化倉庫尤其重要。

E型瓦楞紙板仍然是零售展示的理想選擇,它既能提供足夠的剛性,又能保證合理的板材成本。 A型瓦楞紙板厚度為5毫米,目前仍用於易碎陶瓷和重型工業零件的包裝,但由於市場對輕質材料的需求不斷成長,其市場佔有率正在下降。目前,瓦楞紙板機械的OEM製造商正在推出快速更換卡盒系統,使工廠能夠在15分鐘內完成瓦楞型材的更換,從而方便中小企業採用微型瓦楞紙板,並加速其普及。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 產業價值鏈分析

- 波特五力分析

- 宏觀經濟因素對市場的影響

- 全球瓦楞紙板包裝市場概覽

- 投資分析

第5章 市場動態

- 市場促進因素

- 電子商務履約需求不斷成長

- 加強環境法規,鼓勵可回收包裝

- 生鮮食品和食品宅配服務的成長

- 都市化正在推動消費品的消費。

- 國家獎勵促進輕量化包裝創新

- 中小企業引入數位化按需瓦楞紙箱

- 市場限制因素

- 再生紙進口政策的波動

- 與軟質塑膠包裝的競爭

- 最後一公里物流瓶頸:托盤標準化

- 新創公司推出的生質塑膠瓦楞紙板替代品

第6章 市場規模與成長預測

- 材料

- 維珍工藝襯板

- 再生襯紙板

- 紙板芯

- 半化學法製槽

- 其他材料

- 長笛類型

- 長笛

- 低音長笛

- C調長笛

- E 長笛

- F調長笛

- 按包裝類型

- 普通插槽容器

- 客製化模切盒

- 折疊紙箱

- 商店展示

- 托盤箱

- 其他包裝類型

- 依牆體類型

- 單層

- 雙層壁

- 三層壁

- 一邊

- 透過印刷技術

- 柔版印刷

- 數位噴墨列印

- Riso層壓

- 網版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 加工食品

- 生鮮食品和農產品

- 飲料

- 紙製品

- 電器產品

- 個人護理化妝品

- 電子商務履約中心

- 製藥

- 其他終端用戶產業

第7章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Shanying International Holdings Co. Ltd.

- Nine Dragons Paper(Holdings)Limited

- Lee & Man Paper Manufacturing Ltd.

- Hung Hing Printing Group Limited

- New Asia Packaging Co. Ltd.

- HengFeng Packaging Materials Co. Ltd.

- Shanghai DE Printed Box

- Belpax

- Baoding Yueyang Packaging

- ZZ Group International Holdings Limited

- Jingxing Paper

- Minfeng Special Paper Co. Ltd.

- Yutian Hs Packaging Co. Ltd.

- Dongguan Jianxin

- Rizhao Forest Packaging

- Sinopack Industries Ltd.

- International Paper(China)Co. Ltd.

- Smurfit Westrock plc

第8章 市場機會與未來展望

- 評估未開發的領域和未滿足的需求

According to Mordor Intelligence, the china corrugated packaging market size is projected to be USD 39.14 billion in 2025, USD 40.80 billion in 2026, and reach USD 48.96 billion by 2031, growing at a CAGR of 3.71% from 2026 to 2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, and More), Flute Type (A Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single, Double, and More), Printing Technology (Flexographic, and More), and End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Corrugated Packaging Market Trends and Insights

Expanding E-Commerce Fulfillment Demand

China processed 175 billion parcels in 2024, and corrugated boxes accounted for roughly 68% of that volume, cementing the channel as the single largest off-taker in the China corrugated packaging market. Fulfillment centers are shifting from regular slotted containers to right-sized, die-cut boxes that reduce void fill, enabling automated lines to complete a pack cycle in under 30 seconds. JD Logistics eliminated more than 1 billion secondary cartons in 2024, forcing converters to compete on lead time, digital customization, and design precision rather than tonnage. Cross-border sellers in the Hainan Free Trade Port and the Greater Bay Area demand micro flute formats that comply with International Air Transport Association dimensional-weight rules, sustaining unit growth even as average board weight declines. Livestream shopping, a channel that generated CNY 4.9 trillion (USD 0.68 trillion) in gross merchandise value during 2025, has turned packaging into on-screen advertising, prompting brands to pay 40%-60% premiums for litho-laminated, camera-ready shippers.

Rising Environmental Regulations Favoring Recyclable Packaging

The Ministry of Ecology and Environment raised the recycled-content threshold for new corrugated boxes to 85% by 2027, up from a 70% baseline, anchoring recycled linerboard's 63.21% share in 2025. Import quotas that cut recovered-paper inflows to 4.2 million tonnes in 2025 tightened domestic scrap markets, lifting prices 12% year on year. Provincial extended-producer-responsibility pilots shift collection costs to brand owners, accelerating lightweighting and alternative-fiber trials in Zhejiang and Jiangsu. In pharmaceuticals, the new T/CNPPA 3029-2025 standard specifies low moisture-vapor transmission, carving a regulatory moat for virgin kraft grades in cold-chain cartons. Large mills capitalize on scale to absorb wastewater and VOC-control capex, while regional converters face margin erosion of 8%-12% under the 14th Five-Year Plan.

Volatility in Recovered Paper Import Policies

Imports slid to 4.2 million tonnes in 2025 under a 0.3% contamination cap, exposing mills to spot-market spikes and lengthening customs clearance from 7 to 18 days. Domestic OCC prices rose 12%, squeezing converters without captive pulping and prompting some buyers to shift to flexible pouches despite recyclability trade-offs. Coastal mills that historically favored long-fiber American scrap are reallocating capital to virgin pulp, illustrated by Nine Dragons' USD 4.8 billion Beihai complex with 1.1 million tonnes of chemical pulp. Municipal collection remains fragmented, with 35% of urban corrugated waste still co-mingled, adding de-inking costs and weakening small-mill competitiveness.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Fresh Produce and Food Delivery Services

- Urbanization Driving Consumer Goods Consumption

- Competition from Flexible Plastic Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard accounted for 63.21% of the China corrugated packaging market in 2025, reflecting the mandated 85% recycled content requirement for express parcels by 2027. Integrated mills capture feedstock advantages through nationwide OCC collection networks, anchoring their cost leadership. Virgin Kraft linerboard is forecast to expand at 4.77% CAGR, outperforming overall growth as fresh-produce exporters and luxury e-commerce brands demand higher ring-crush strength, tear resistance, and cleaner print surfaces. Nine Dragons' Beihai mill and Lee and Man's specialty-kraft upgrades target this premium. Corrugating medium producers are testing semi-chemical pulps from bamboo and straw to hedge softwood risks, though moisture sensitivity still confines such grades to low-humidity logistics corridors.

Bio-based barrier coatings and starch adhesives are scaling up in pilot runs to achieve recyclability without wax, signaling that the China corrugated packaging market will bifurcate into high-volume recycled-content and smaller, high-margin virgin niches. In parallel, food-contact and pharmaceutical mandates under T/CNPPA 3029-2025 steer critical temperature-controlled applications toward virgin fiber, guaranteeing a price umbrella that offsets higher raw-material costs. The converter strategy, therefore, splits commodity players chase recycled linerboard efficiency, while value-added specialists court brand owners with premium kraft and functional coatings.

B flute held 34.15% of the China corrugated packaging market share in 2025 because of its cushioning-to-cost balance in general merchandise. However, the F flute is accelerating at 4.15% CAGR through 2031 as cross-border sellers optimize for dimensional weight and cosmetics brands seek offset-level graphics. The flute's 0.75-1.0 mm caliper allows direct lithographic printing, eliminating litho-lamination steps and lowering inventory bulk, which is vital in automated warehouses with height constraints.

E flute remains the compromise format for retail-ready displays, offering rigidity with acceptable board economy. A flute persists for fragile ceramics and heavy industrial parts owing to its 5 mm thickness, though its share erodes under lightweighting mandates. Corrugator OEMs now ship quick-change cassette systems that let factories swap flute profiles in under 15 minutes, democratizing micro flute access for small and medium enterprises and enhancing adoption momentum.

List of Companies Covered in this Report:

- Shanying International Holdings Co. Ltd.

- Nine Dragons Paper (Holdings) Limited

- Lee & Man Paper Manufacturing Ltd.

- Hung Hing Printing Group Limited

- New Asia Packaging Co. Ltd.

- HengFeng Packaging Materials Co. Ltd.

- Shanghai DE Printed Box

- Belpax

- Baoding Yueyang Packaging

- ZZ Group International Holdings Limited

- Jingxing Paper

- Minfeng Special Paper Co. Ltd.

- Yutian Hs Packaging Co. Ltd.

- Dongguan Jianxin

- Rizhao Forest Packaging

- Sinopack Industries Ltd.

- International Paper (China) Co. Ltd.

- Smurfit Westrock plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Overview of the Global Corrugated Packaging Market

- 4.6 Investment Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Expanding E-Commerce Fulfillment Demand

- 5.1.2 Rising Environmental Regulations Favoring Recyclable Packaging

- 5.1.3 Growth in Fresh Produce and Food Delivery Services

- 5.1.4 Urbanization Driving Consumer Goods Consumption

- 5.1.5 Provincial Incentives for Lightweight Packaging Innovation

- 5.1.6 Adoption of Digital Print-On-Demand Corrugated Boxes by SMEs

- 5.2 Market Restraints

- 5.2.1 Volatility in Recovered Paper Import Policies

- 5.2.2 Competition from Flexible Plastic Packaging

- 5.2.3 Bottlenecks in Last-Mile Logistics Pallet Standardization

- 5.2.4 Emerging Bioplastic Corrugated Alternatives from Startups

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Material

- 6.1.1 Virgin Kraft Linerboard

- 6.1.2 Recycled Linerboard

- 6.1.3 Corrugating Medium

- 6.1.4 Semi-Chemical Fluting

- 6.1.5 Other Materials

- 6.2 By Flute Type

- 6.2.1 A Flute

- 6.2.2 B Flute

- 6.2.3 C Flute

- 6.2.4 E Flute

- 6.2.5 F Flute

- 6.3 By Packaging Type

- 6.3.1 Regular Slotted Containers

- 6.3.2 Die-Cut Custom Boxes

- 6.3.3 Folding Cartons

- 6.3.4 Point-of-Purchase Displays

- 6.3.5 Pallet Boxes

- 6.3.6 Other Packaging Types

- 6.4 By Wall Type

- 6.4.1 Single-Wall

- 6.4.2 Double-Wall

- 6.4.3 Triple-Wall

- 6.4.4 Single Face

- 6.5 By Printing Technology

- 6.5.1 Flexographic Printing

- 6.5.2 Digital Inkjet Printing

- 6.5.3 Litho-Lamination

- 6.5.4 Screen Printing

- 6.5.5 Other Printing Technologies

- 6.6 By End-User Industry

- 6.6.1 Processed Foods

- 6.6.2 Fresh Food and Produce

- 6.6.3 Beverages

- 6.6.4 Paper Products

- 6.6.5 Electrical Products

- 6.6.6 Personal Care and Cosmetics

- 6.6.7 E-commerce Fulfillment Centers

- 6.6.8 Pharmaceuticals

- 6.6.9 Other End-User Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles

- 7.4.1 Shanying International Holdings Co. Ltd.

- 7.4.2 Nine Dragons Paper (Holdings) Limited

- 7.4.3 Lee & Man Paper Manufacturing Ltd.

- 7.4.4 Hung Hing Printing Group Limited

- 7.4.5 New Asia Packaging Co. Ltd.

- 7.4.6 HengFeng Packaging Materials Co. Ltd.

- 7.4.7 Shanghai DE Printed Box

- 7.4.8 Belpax

- 7.4.9 Baoding Yueyang Packaging

- 7.4.10 ZZ Group International Holdings Limited

- 7.4.11 Jingxing Paper

- 7.4.12 Minfeng Special Paper Co. Ltd.

- 7.4.13 Yutian Hs Packaging Co. Ltd.

- 7.4.14 Dongguan Jianxin

- 7.4.15 Rizhao Forest Packaging

- 7.4.16 Sinopack Industries Ltd.

- 7.4.17 International Paper (China) Co. Ltd.

- 7.4.18 Smurfit Westrock plc

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)菲律賓瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)菲律賓瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。美國瓦楞紙包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印尼瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板包裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。美國瓦楞紙包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印尼瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板包裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)