|

市場調查報告書

商品編碼

2063486

印尼瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Indonesia Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

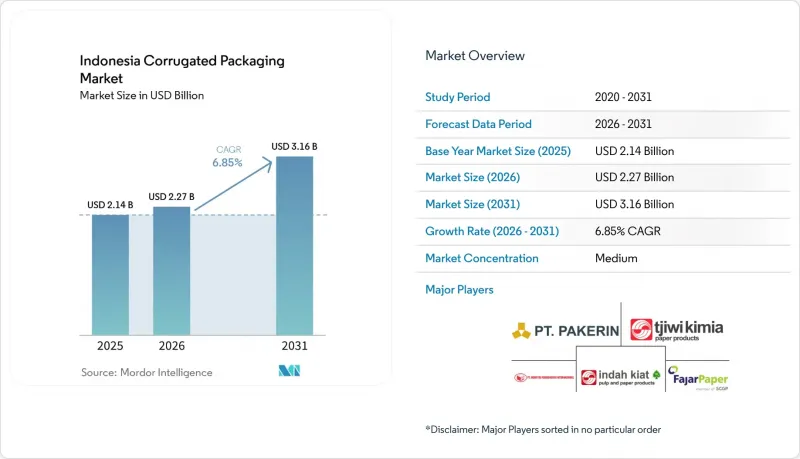

根據 Mordor Intelligence 預測,印尼瓦楞紙板包裝市場規模將從 2025 年的 21.4 億美元成長到 2026 年的 22.7 億美元,到 2031 年達到 31.6 億美元,2026 年至 2031 年的複合年成長率為 6.85%。

本報告依材料(原生牛皮箱紙板、再生紙板、瓦楞紙核心材料等)、瓦楞類型(A型瓦楞等)、包裝類型(普通開槽紙盒等)、壁厚結構(單層、雙層等)、印刷技術(柔版印刷等)和終端用戶行業(加工食品等)進行細分。市場預測以美元計價。

印尼瓦楞紙板包裝市場趨勢與洞察

電子商務出貨量激增

印尼快速成長的小包裹經濟正在重新定義包裝盒設計,各大平台都在最佳化包裝,以規避體積重量課稅並提高最後一公里配送效率。主要社交電商通路的日銷售額如今已達到數百萬筆微訂單,這要求包裝盒採用更薄的E型和F型瓦楞紙板、尺寸精準的模切工藝以及快速的設計變更。履約中心正在部署自動化切割機,可將包裝盒的空隙減少高達20%,迫使加工商提供按需客製化的空白包裝盒,而非現成的標準槽型包裝盒。由於缺乏全國統一的回收標準,跨境經銷商難以合規,因此,為了防止退貨過程中包裝損壞,較大包裹的包裝材料也趨於加厚。隨著網路經濟向爪哇島以外的地區擴展,那些能夠將即時配送與區域樞紐連接起來的加工商,將佔據電子商務浪潮中得天獨厚的優勢。

塑膠減量政策正在加速紡織材料的採用。

生產者延伸責任制 (EPR) 法規和區域性塑膠禁令正迫使品牌轉向纖維基二次包裝。政府的循環經濟藍圖旨在 2029 年實現全面的廢棄物管理,這促使雅加達和峇裡島的零售商從收縮膜轉向瓦楞紙托盤和可折疊紙盒。跨國公司現在要求供應商獲得 ISO 14001 認證,降低了小規模紙盒製造商的進入門檻。然而,農村地區的有效回收有限且不均衡,因為只有 60% 的城市居民能夠獲得正規的廢棄物收集服務。這種複雜的法規體系為能夠平衡環境因素和區域特定供應鏈的加工商提供了商機。

再生紙板(OCC)/紙漿價格波動

2026年1月,美國再生瓦楞紙板(OCC)出口價格達到每短噸130美元,由於印尼的強制檢驗,現貨採購還需額外付費。 2025年下半年,漂白硬木牛皮紙漿價格徘徊在每噸530美元左右,但對中國需求下降的擔憂可能導致價格進一步下跌。紙漿價格每波動50美元,都會對非垂直整合加工企業的利潤趨勢產生顯著影響。這種價格波動迫使許多中型企業推遲自動化和數位印刷的升級,使它們只能依賴低利潤的商品產業。

細分市場分析

在印尼瓦楞紙包裝市場,預計2025年,再生箱板紙將佔材料銷售額的61.86%,顯示國內對廢棄舊瓦楞紙箱回收的投資卓有成效。原生牛皮紙仍然是出口型食品和製藥企業防潮的關鍵材料,但由於碳排放報告成本不斷上漲,其市場佔有率仍然有限。作為瓦楞紙板結構基石的紙芯,預計將以7.20%的複合年成長率成長,因為加工商在保持紙箱抗壓性能的同時,也在降低紙芯的紙張重量。半化學成型瓦楞紙板由於其優異的剛度重量比,仍然滿足高階家電和托盤箱的需求,但其高能耗限制了其主流應用。由於都市區回收路線的污染問題導致纖維產量下降,造紙商目前正在混合進口和國產廢紙以達到破損強度目標。因此,在印尼瓦楞紙板包裝市場,那些引進了先進滾筒碎漿機、能夠實現高產量和低淡水消耗的造紙商更受青睞。

這些次生影響正蔓延至加工業者的採購趨勢。旨在減少範圍3排放的跨國公司現在要求競標的箱板紙必須經過產銷監管鏈(CoC)認證,這增加了小規模紙板廠的文件要求。同時,儘管國內食品製造商在預算方面有所顧慮,但特種防潮塗層(比未塗佈原紙貴10-15%)在熱帶出口路線上的市場佔有率正在不斷擴大。隨著電價上漲,利用生質能和太陽能發電設施的綜合企業進一步擴大了成本差距,這凸顯了規模經濟和擁有自有纖維為何仍然是印尼瓦楞紙包裝市場長期風險對沖手段的重要性。

C型瓦楞紙板厚度為4毫米,兼顧了麵條、食用油和飲料等產品的分層和緩衝性能,預計到2025年將佔總產量的42.50%。同時,E型瓦楞紙板厚度約為1.6毫米,由於電商平台尋求降低小包裹體積重量,其市場正以8.08%的複合年成長率快速成長。數位印刷製造商青睞E型瓦楞紙板和F型瓦楞紙板光滑的表面,因為這有助於提高圖像解析度,使品牌能夠直接在運輸箱上印刷社交媒體所需的圖形。

B型瓦楞紙板傳統上是零售展示的理想選擇,但隨著行銷人員轉向更輕的瓦楞壁和能夠獨立於瓦楞結構吸收衝擊的專用內襯,B型瓦楞紙板正面臨困境。 A型瓦楞紙板作為易碎玻璃製品的保護材料,依然佔據著一席之地;而微型瓦楞紙板則被用於可折疊的瓦楞混合產品中,這些產品兼具圖形展示和運輸保護功能。 E型瓦楞紙板的加工要求較小的瓦楞間隙和更潔淨的內襯,因此,那些能夠自行生產測試內襯的一體化製造商,憑藉更少的壓痕缺陷,在印尼瓦楞包裝市場獲得了競爭優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務出貨量激增

- 塑膠減量政策正在加速纖維的採用。

- 印尼加工食品產業的擴張

- 擴大國內紙漿和造紙產能

- 數位印刷和柔版印刷在小批量生產的應用進展

- 對自動化物流履約的投資正在推動使用尺寸合適的包裝盒。

- 市場限制因素

- OCC價格波動/紙漿價格

- 能源和物流成本不斷上漲

- 濕度導致強度降低,因此需要採取高成本的保護措施。

- 廢料收集系統分散化和回收率低

- 產業生態系分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 維珍工藝襯板

- 再生襯紙板

- 紙板芯

- 半化學法製槽

- 其他材料

- 長笛類型

- 長笛

- 低音長笛

- C調長笛

- E 長笛

- F調長笛

- 按包裝類型

- 普通插槽容器

- 客製化模切盒

- 折疊紙箱

- 商店展示

- 托盤箱

- 其他包裝類型

- 依牆體類型

- 單層

- 雙層壁

- 三層壁

- 一邊

- 透過印刷技術

- 柔版印刷

- 數位噴墨列印

- Riso層壓

- 網版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 加工食品

- 生鮮食品和農產品

- 飲料

- 電器產品

- 個人護理化妝品

- 電子商務履約中心

- 製藥

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- PT Indah Kiat Pulp & Paper Tbk

- PT Pabrik Kertas Tjiwi Kimia Tbk

- PT Pabrik Kertas Indonesia(Pakerin)

- PT Fajar Surya Wisesa Tbk

- PT Industri Pembungkus Internasional

- PT Surabaya Mekabox

- PT Satyamitra Kemas Lestari Tbk

- PT Gema Putra Abadi

- PT Sapta Warna Cemerlang

- PT Kedawung Setia Corrugated Carton Box Industrial

- PT Edpack Karunia Persada

- PT Indo Packaging

- Rengo Co., Ltd.

- Oji Holdings Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the indonesia corrugated packaging market size is expected to increase from USD 2.14 billion in 2025 to USD 2.27 billion in 2026 and reach USD 3.16 billion by 2031, growing at a CAGR of 6.85% over 2026-2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, and More), Flute Type (A Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single, Double, and More), Printing Technology (Flexographic, and More), and End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Corrugated Packaging Market Trends and Insights

Surge in E-Commerce Shipments

Indonesia's booming parcel economy is redefining box design as platforms optimize packaging to avoid dimensional-weight tariffs and improve last-mile efficiency. Daily sales on major social-commerce channels now spawn millions of micro-orders that favor thinner E and F flutes, right-sized die-cuts, and rapid art changes. Fulfillment centers are installing automated cutters that reduce void space by up to 20 percent, compelling converters to provide on-demand blanks rather than pre-made regular slotted containers. The absence of a unified national recyclability standard adds compliance complexity for cross-border sellers, so outsized parcels often revert to heavier gauges to guarantee intact returns. As the internet economy expands beyond Java, converters that synchronize just-in-time deliveries with regional hubs are best placed to ride the e-commerce wave.

Plastic-Reduction Policies Accelerating Fiber Adoption

Extended Producer Responsibility rules and localized plastic bans are nudging brands toward fiber-based secondary packaging. The government's circular roadmap aims to achieve complete waste management by 2029, prompting retailers in Jakarta and Bali to switch from shrink wrap to corrugated trays and folding cartons. Multinationals now require ISO 14001 certification from suppliers, lifting entry barriers for smaller box plants. Adoption, however, is uneven, as only 60 percent of urban residents have access to formal waste collection, limiting effective recycling in secondary cities. This regulatory mosaic creates openings for converters that pair green credentials with region-specific supply chains.

Volatility in OCC / Pulp Prices

In January 2026, old-corrugated-container exports from the United States reached USD 130 per short ton, and Indonesia's compulsory inspections added extra cost to spot purchases. Bleached hardwood kraft pulp tracked near USD 530 per tonne late in 2025, yet looming Chinese demand weakness threatens another dip. Every USD 50 swing in pulp pricing materially alters the profit trajectories of converters without vertical integration. Such volatility forces many mid-tier players to delay automation or digital-printing upgrades, locking them into low-margin commodity segments.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Indonesia's Processed Food Industry

- Growth of Domestic Pulp and Paper Capacity

- Rising Energy and Logistics Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Indonesia corrugated packaging market drew 61.86% of 2025 material revenue from recycled linerboard, validating domestic investments in old-corrugated-containers recovery. Virgin Kraft grades remain mandatory for export-oriented food and pharma shippers wanting moisture resistance, yet rising carbon reporting costs keep their share modest. Corrugating medium, the backbone of flute structure, is on track for a 7.20% CAGR, paced by converters trimming basis weight while protecting box compression. Semi-chemical fluting still secures premium appliance and pallet cases due to its superior stiffness-to-weight, though its larger energy footprint limits mainstream adoption. Mills now mix imported and local scrap to hit burst-strength targets after contamination issues reduced fiber yield in several urban collection streams. The Indonesian corrugated packaging market, therefore, rewards mills that install advanced drum pulpers that achieve higher yields and freshwater savings.

Second-order effects ripple through converter buying. Chain-of-custody-certified linerboard is now featured in bids from multinational customers seeking Scope 3 cuts, increasing documentation requirements for smaller sheet plants. Meanwhile, specialty moisture-barrier coatings, priced 10-15% above uncoated stock, gain ground in tropical export lanes despite budget pushback from domestic food producers. Integrated players leveraging biomass power and solar arrays further widen cost gaps as grid tariffs climb, underscoring why scale plus in-house fiber remains the long-term hedge within the Indonesia corrugated packaging market.

C flute supplied 42.50% of 2025 volume because its 4 mm caliper balances stacking and cushioning for noodles, oils, and beverages. E flute, at roughly 1.6 mm, is sprinting ahead at an 8.08% CAGR as e-commerce hubs chase dimensional-weight savings per parcel. Digital printers praise E and F flutes for smoother surfaces that improve image resolution, enabling brands to print social media graphics directly on shipping cases.

B flute, historically favored for retail displays, is under pressure as marketers migrate to lighter walls and engineered inserts that handle shock separately from the corrugated structure. A flute remains a niche guardrail for fragile glassware, while microflute designs slot into folding carton hybrids that merge graphics with shipping protection. Because converting E flute needs tighter gaps and cleaner liner, integrated producers with on-site testliner enjoy fewer crush rejects, sharpening their edge in the Indonesia corrugated packaging market.

List of Companies Covered in this Report:

- PT Indah Kiat Pulp & Paper Tbk

- PT Pabrik Kertas Tjiwi Kimia Tbk

- PT Pabrik Kertas Indonesia (Pakerin)

- PT Fajar Surya Wisesa Tbk

- PT Industri Pembungkus Internasional

- PT Surabaya Mekabox

- PT Satyamitra Kemas Lestari Tbk

- PT Gema Putra Abadi

- PT Sapta Warna Cemerlang

- PT Kedawung Setia Corrugated Carton Box Industrial

- PT Edpack Karunia Persada

- PT Indo Packaging

- Rengo Co., Ltd.

- Oji Holdings Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in E-Commerce Shipments

- 4.2.2 Plastic-Reduction Policies Accelerating Fiber Adoption

- 4.2.3 Expansion of Indonesia's Processed Food Industry

- 4.2.4 Growth of Domestic Pulp & Paper Capacity

- 4.2.5 Advances in Digital & Flexographic Printing for Short Runs

- 4.2.6 Investment in Automated Fulfilment Boosting Right-Sized Boxes

- 4.3 Market Restraints

- 4.3.1 Volatility in OCC / Pulp Prices

- 4.3.2 Rising Energy & Logistics Costs

- 4.3.3 Humidity-Driven Strength Loss Requiring Costly Barriers

- 4.3.4 Fragmented Scrap-Collection & Low Recycling Rates

- 4.4 Industry Ecosystem Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-Commerce Fulfilment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 PT Indah Kiat Pulp & Paper Tbk

- 6.4.2 PT Pabrik Kertas Tjiwi Kimia Tbk

- 6.4.3 PT Pabrik Kertas Indonesia (Pakerin)

- 6.4.4 PT Fajar Surya Wisesa Tbk

- 6.4.5 PT Industri Pembungkus Internasional

- 6.4.6 PT Surabaya Mekabox

- 6.4.7 PT Satyamitra Kemas Lestari Tbk

- 6.4.8 PT Gema Putra Abadi

- 6.4.9 PT Sapta Warna Cemerlang

- 6.4.10 PT Kedawung Setia Corrugated Carton Box Industrial

- 6.4.11 PT Edpack Karunia Persada

- 6.4.12 PT Indo Packaging

- 6.4.13 Rengo Co., Ltd.

- 6.4.14 Oji Holdings Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)菲律賓瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國瓦楞紙板包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)菲律賓瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國瓦楞紙板包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。美國瓦楞紙包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板包裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。美國瓦楞紙包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板包裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)