|

市場調查報告書

商品編碼

2063658

歐洲瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Europe Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

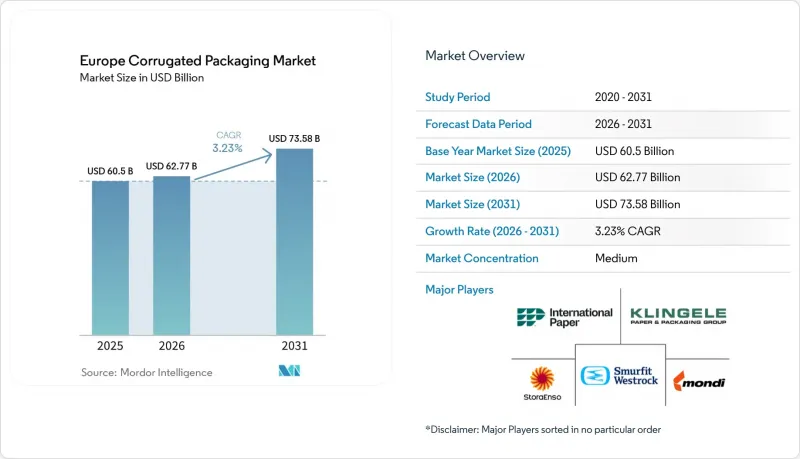

據 Mordor Intelligence 稱,歐洲瓦楞紙板包裝市場預計將從 2025 年的 605 億美元成長到 2026 年的 627.7 億美元,到 2031 年達到 735.8 億美元,2026 年至 2031 年的複合年成長率為 3.23%。

本報告依材料(原生牛皮箱紙板、再生紙板等)、瓦楞類型(A型瓦楞、E型瓦楞等)、包裝類型(普通開槽紙盒等)、壁厚結構(單層壁等)、印刷技術(柔版印刷等)、終端用戶行業(加工食品等)和地區進行細分。市場預測以美元計價。

歐洲瓦楞紙板包裝市場的趨勢與洞察

電子商務的快速發展正在推動對輕型運輸方式的需求。

現今,線上零售平台需要紙張重量紙板,既能承受多次自動化分類流程,又能降低小包裹運輸成本。亞馬遜和Mondi於2025年推出了一款重量減輕44克的郵件包裝袋,每年可處理數百萬份訂單,節省數千噸襯紙。 Smurfit Westrock透過推出紙質托盤纏繞膜替代塑膠拉伸膜,拓展了瓦楞紙板在穩定單元貨載的應用。 BHS Corrugated的輕量化產品系列在不影響抗壓性能的前提下,每平方公尺紙張重量減輕了20克。受成本、永續性和範圍3報告壓力等因素的驅動,此趨勢在三大電商市場尤為顯著。

快速消費品二級包裝向塑膠替代品過渡

為了遵守歐盟一次性塑膠指令,日常消費品製造商正在逐步淘汰收縮膜、托盤和翻蓋式容器。 DS Smith報告稱,到2025年,將以纖維基包裝取代超過12億個塑膠包裝。 Klingele和Maistapack合作推出了用於生鮮食品線的熱成型纖維托盤,取代了先前以聚苯乙烯為主的托盤。雖然產量隨著需求的成長而增加,但CEPI在2026年發出警告,表示加速替代將導致再生纖維出口,國內原料供應緊張,以及投入成本上升。

能源成本上漲給造紙廠的營業利潤率帶來了壓力。

2026年3月,天然氣價格超過68歐元/兆瓦時(73美元/兆瓦時)。在義大利,由於其電力高度依賴天然氣,天然氣價格高達111歐元/兆瓦時(119美元/兆瓦時)。斯特拉恩索公司耗資3000萬歐元(3,200萬美元)對海諾拉工廠維修,減少了11.3萬噸二氧化碳排放,但這需要數年的資本投資。能源價格飆升的影響最迅速地擠壓了沒有避險或汽電共生(CHP)設施的獨立造紙廠的利潤空間,迫使南歐的造紙廠暫時減產。

細分市場分析

截至2025年,再生瓦楞紙板將佔歐洲瓦楞紙板包裝市場佔有率的44.43%。完善的回收基礎設施以及來自食品、飲料和電商通路的穩定需求支撐了其市場主導地位。根據CEPI的2024年初步數據,箱板紙產量年增4.3%,證實了供應的韌性。受醫藥和高階食品行業對更高濕強度和阻隔塗層相容性的需求驅動,預計到2031年,原生牛皮箱紙板將以每年5.62%的速度成長。半化學成型瓦楞紙板在三層出口紙箱中日益重要,因為每克剛度比成本更重要。隨著加工商降低纖維品質的波動性,歐洲原生瓦楞紙板包裝市場將進一步擴大。

再生紙(OCC)價格的波動縮小了再生紙和原生紙之間的價格差距,降低了消費者對再生紙襯紙的自動成本偏好。 Meyer-Mellnhof指出,來自亞洲的進口壓力和斯堪的斯堪地那維亞的產能過剩是導致再生產品利潤率承壓的因素。儘管有關再生材料含量的監管要求仍然傾向於採購廢棄纖維,但如果功能性阻隔層或食品接觸法規使回收途徑複雜化,品牌商也可能接受原生原料。因此,如今材料配方不僅受價格影響,還受最終用途性能的影響,而這些細微的差別正在重塑歐洲瓦楞紙包裝市場的採購模式。

到2025年,B型瓦楞紙板仍將佔總產量的38.45%,其緩衝性和重量的平衡性備受青睞。品牌商越來越多採用E型瓦楞紙板進行直接印刷的零售包裝,預計到2031年,其年複合成長率(CAGR)將達到5.23%。數位白墨的引入消除了傳統印刷品質的差距,使E型瓦楞紙板成為化妝品和糖果甜點促銷應用的理想選擇。 BHS Corrugated的eCom產品針對E型瓦楞紙板和F型瓦楞紙板的生產進行了最佳化,在保持抗壓強度的同時,減少了紙張用量。

C型和A型瓦楞紙板雖然適用於承載重物,但在運輸空間、碳排放目標和貨架密度等因素優先於最大承載能力的地區,它們的市場佔有率正在下降。對可用空間的監管限制進一步推動了低矮瓦楞紙板的發展,因為超大尺寸的包裝容器可能會受到零售商的處罰。隨著零售商對貨架包裝尺寸進行標準化,加工商正在拓展微型瓦楞紙板的性能,並確保其在緊湊型包裝中保持強度,從而維持低矮瓦楞紙板在歐洲瓦楞紙板包裝市場規模預測中的成長勢頭。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務的快速發展正在推動對輕便型運輸方式的需求。

- 快速消費品二級包裝向塑膠替代品過渡

- 零售連鎖店對貨架包裝的需求不斷成長

- 透過瓦楞紙板生產線的自動化縮短前置作業時間。

- 食材自煮包和雜貨宅配服務的快速成長

- 歐盟包裝和包裝廢棄物法規規定的再生材料含量強制目標

- 市場限制因素

- 舊紙板(OCC)價格波動

- 能源成本上漲給造紙廠的營業利潤率帶來了壓力。

- 生鮮食品物流領域可重複使用塑膠箱的競爭

- 獲得許可證限制了瓦楞紙板生產設施的擴張。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 維珍工藝襯板

- 再生襯紙板

- 瓦楞紙板基紙

- 半化學蝕刻

- 其他材料

- 長笛類型

- 長笛

- 低音長笛

- C調長笛

- E 長笛

- F調長笛

- 按包裝類型

- 普通插槽容器

- 客製化模切盒

- 折疊紙箱

- 商店展示

- 托盤箱

- 其他包裝類型

- 依牆體類型

- 單層

- 雙層壁

- 三層壁

- 一邊

- 透過印刷技術

- 柔版印刷

- 數位噴墨列印

- Riso層壓

- 網版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 加工食品

- 生鮮食品和農產品

- 飲料

- 電器產品

- 個人護理化妝品

- 電子商務履約中心

- 製藥

- 其他終端用戶產業

- 按地區

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 比荷盧經濟聯盟

- 北歐國家

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit Westrock plc

- Mondi plc

- International Paper Company

- Stora Enso Oyj

- Saica Group

- VPK Group NV

- Pro-Gest SpA

- Klingele Papierwerke SE & Co. KG

- Model Holding AG

- Prinzhorn Holding GmbH

- Mayr-Melnhof Karton AG

- LEIPA Group GmbH

- Cartonajes International SL

- THIMM Group GmbH+Co. KG

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe corrugated packaging market size is expected to increase from USD 60.50 billion in 2025 to USD 62.77 billion in 2026 and reach USD 73.58 billion by 2031, growing at a CAGR of 3.23% over 2026-2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, and More), Flute Type (A Flute, E Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single-Wall, and More), Printing Technology (Flexographic Printing, and More), End-User Industry (Processed Foods, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Corrugated Packaging Market Trends and Insights

E-Commerce Boom Driving Demand for Lightweight Shipping Formats

Online retail platforms now specify lower-basis-weight boards that can withstand multiple automated sortation passes while reducing parcel freight costs. Amazon and Mondi released a 44-gram lighter mailer in 2025 that scales across millions of annual orders, saving thousands of tonnes of linerboard. Smurfit Westrock introduced a paper pallet wrap that substitutes plastic stretch film, widening corrugated's role in unit-load stabilization. Lightweight profiles from BHS Corrugated lower grammage by 20 g/m2 without sacrificing compression performance. Cost, sustainability, and Scope 3 reporting pressures make this driver most acute in the three largest e-commerce markets.

Shift Toward Plastic Substitution in FMCG Secondary Packaging

Fast-moving consumer goods owners are eliminating shrink wrap, trays, and clamshells as they work toward compliance with the EU Single-Use Plastics Directive. DS Smith reported that it would replace more than 1.2 billion plastic packs with fiber-based designs by 2025. Klingele's tie-up with Maistapack brought thermoformed fiber trays for fresh produce lines historically dominated by polystyrene. While demand lifts volume, Cepi cautioned in 2026 that accelerated substitution is draining recovered fibers to export markets, tightening domestic feedstock, and lifting input costs.

Rising Energy Costs Squeezing Mill Operating Margins

Natural-gas prices jumped above EUR 68/MWh (USD 73/MWh) in March 2026, with Italy paying EUR 111/MWh (USD 119/MWh) because of its gas-heavy power mix. Stora Enso's EUR 30 million (USD 32 million) Heinola upgrade cut emissions by 113,000 tCO2 yet required multi-year capex. Energy shocks compress margins fastest at independent mills that lack hedging or CHP capacity, prompting temporary curtailments in Southern Europe.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Recycled-Content Targets Under EU Rules

- Increasing Demand for Shelf-Ready Packaging in Retail Chains

- Volatility In Old Corrugated Container Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard owned 44.43% of Europe corrugated packaging market share in 2025. Widespread collection infrastructure and stable demand from grocery, beverage, and e-commerce channels anchor its dominance. Cepi's preliminary 2024 data showed containerboard output rising 4.3% year-on-year, confirming supply resilience. Virgin Kraft Linerboard is projected to grow at 5.62% annually through 2031, as pharmaceuticals and premium foods require higher wet-strength and greater barrier-coating compatibility. Semi-chemical fluting gains relevance in triple-wall export cartons, where stiffness per gram outweighs cost. The European corrugated packaging market for virgin grades will expand as converters mitigate fiber-quality variability.

Competitive pricing gaps between recycled and virgin sheets have narrowed due to volatile OCC costs, reducing the automatic cost preference for recycled liners. Mayr-Melnhof flagged import pressure from Asia and extra Scandinavian capacity as forces weighing on recycled margins. Regulatory recycled-content mandates still tilt purchasing toward post-consumer fibers, yet brands may accept virgin inputs when functional barriers or food-contact rules complicate recycling pathways. The material mix, therefore, hinges on end-use performance more than price alone, a nuance that reshapes procurement within the European corrugated packaging market.

B flute maintained 38.45% of overall volume in 2025, prized for its cushioning-to-weight balance. Brands are turning to E flute for direct-print retail-ready packs, propelling a 5.23% CAGR outlook through 2031. Digital white-ink launches eliminated historic print-quality gaps, making E flute viable for cosmetics and confectionery promotions. BHS Corrugated's eCom profile is optimized for E and F flute runs, reducing paper usage while maintaining compression strength.

C flute and A flute support heavy goods but lose share where freight space, carbon targets, and shelf density matter more than maximum stacking strength. Regulatory empty-space limits further favor thinner flutes because oversized containers risk retailer penalties. As retailers standardize shelf-ready dimensions, converters extend microflute capability to guarantee strength in compact forms, sustaining momentum for thin profiles in the Europe corrugated packaging market size forecasts.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Mondi plc

- International Paper Company

- Stora Enso Oyj

- Saica Group

- VPK Group NV

- Pro-Gest S.p.A.

- Klingele Papierwerke SE & Co. KG

- Model Holding AG

- Prinzhorn Holding GmbH

- Mayr-Melnhof Karton AG

- LEIPA Group GmbH

- Cartonajes International S.L.

- THIMM Group GmbH + Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce Boom Driving Demand for Lightweight Shipping Formats

- 4.2.2 Shift Toward Plastic Substitution in FMCG Secondary Packaging

- 4.2.3 Increasing Demand for Shelf-Ready Packaging in Retail Chains

- 4.2.4 Automation of Corrugator Lines Enabling Shorter Lead-Times

- 4.2.5 Rapid Growth of Meal-Kit and Grocery Delivery Services

- 4.2.6 Mandatory Recycled-Content Targets Under EU Packaging and Packaging Waste Regulation

- 4.3 Market Restraints

- 4.3.1 Volatility In Old Corrugated Container (OCC) Prices

- 4.3.2 Rising Energy Costs Squeezing Mill Operating Margins

- 4.3.3 Competition From Reusable Plastic Crates in Fresh-Produce Logistics

- 4.3.4 Limited Corrugator Capacity Additions Due to Permitting Hurdles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-commerce Fulfillment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

- 5.7 By Geography

- 5.7.1 Germany

- 5.7.2 France

- 5.7.3 United Kingdom

- 5.7.4 Italy

- 5.7.5 Spain

- 5.7.6 Benelux

- 5.7.7 Nordic Countries

- 5.7.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Mondi plc

- 6.4.3 International Paper Company

- 6.4.4 Stora Enso Oyj

- 6.4.5 Saica Group

- 6.4.6 VPK Group NV

- 6.4.7 Pro-Gest S.p.A.

- 6.4.8 Klingele Papierwerke SE & Co. KG

- 6.4.9 Model Holding AG

- 6.4.10 Prinzhorn Holding GmbH

- 6.4.11 Mayr-Melnhof Karton AG

- 6.4.12 LEIPA Group GmbH

- 6.4.13 Cartonajes International S.L.

- 6.4.14 THIMM Group GmbH + Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)菲律賓瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國瓦楞紙板包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)菲律賓瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國瓦楞紙板包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。美國瓦楞紙包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印尼瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板包裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。美國瓦楞紙包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印尼瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板包裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)