|

市場調查報告書

商品編碼

2063759

菲律賓瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Philippines Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

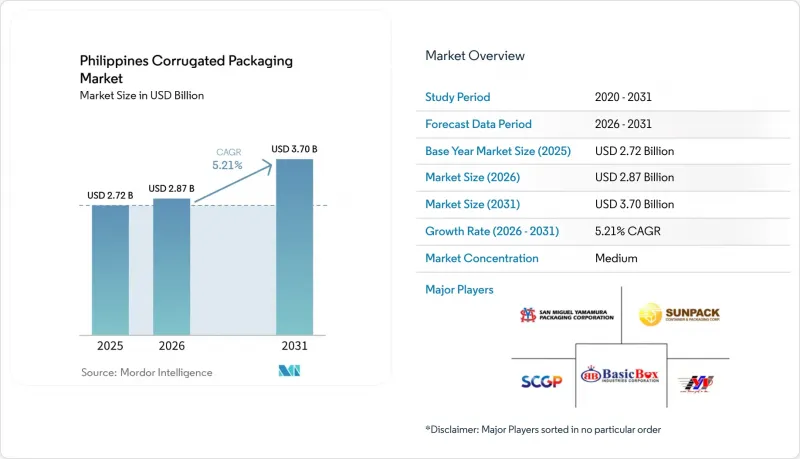

根據 Mordor Intelligence 預測,菲律賓瓦楞紙包裝市場規模將從 2025 年的 27.2 億美元和 2026 年的 28.7 億美元成長到 2031 年的 37 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.21%。

本報告依材料(原生牛皮箱紙板、再生紙板等)、瓦楞類型(A型瓦楞等)、包裝類型(普通開槽紙盒等)、壁厚結構(單層、雙層等)、印刷技術(柔版印刷等)和終端用戶行業(加工食品等)進行分類。市場預測以美元計價。

菲律賓瓦楞紙板包裝市場趨勢與洞察

電子商務的成長正在加速小包裹處理量的成長。

當日達和隔天達的承諾改變了分銷格局,從托盤式門市補貨轉變為數百萬件單件商品的配送。 11月11日和12月12日的限時搶購高峰迫使瓦楞紙板製造商儲備季節性紙板坯料,並調整瓦楞組合以在保持邊緣抗壓強度的同時限制貨物重量。陸運、海運和空運的多模態增加了紙板受潮的風險,促使業者轉向使用更輕且符合堆疊測試標準的再生纖維內襯。履約中心正在對紙箱尺寸進行標準化,以便自動化分類機能夠以最小的人工干預完成小包裹的掃描、貼標和生成清單。所有這些變化共同推動了菲律賓瓦楞紙板包裝市場,特別是馬尼拉大都會小包裹樞紐市場的需求成長。

政府對一次性塑膠製品的監管正在推動紙質替代品的發展。

《生產者延伸責任法》規定,品牌所有者必須在2024年前回收其塑膠包裝使用量的40%,並在2028年前回收80%,違者將面臨最高500萬美元的罰款。同時,財政部正力推對一次性塑膠袋徵收每公斤100美元的消費稅,預計將使零售價格上漲94%。地方性法規也加大了壓力,例如奎松市行政區禁止使用一次性塑膠製品,以及在全國逐步淘汰小袋。品牌所有者現在指定使用瓦楞紙板二級包裝和纖維基外帶容器,這些材料在可回收性評估中得分很高。這些法規促使採購負責人增加瓦楞紙板的供應,鞏固了菲律賓瓦楞紙包裝市場的成長動能。

國內和進口再生紙價格波動

2024年,隨著美國和歐盟的回收率下降,以及印尼的檢驗費用上漲,進口再生紙(OCC)的價格從歐洲95/5級每噸160美元上漲至美國DS-OCC級每噸230美元。本地加工商面臨雙重風險:一方面是進口紙張接收成本上升,另一方面是當非正規回收商減少供應時,市場價格波動加劇。由於只有44%的行政區(barangay)運作功能完善的資源回收設施,而馬尼拉大都會區的覆蓋率僅20%,造紙廠極易受到貨物延誤和纖維品質下降的影響。這些衝擊正在擠壓毛利率,並抑制菲律賓瓦楞紙包裝市場的短期投資意願。

細分市場分析

到2025年,再生瓦楞紙板將佔菲律賓瓦楞包裝市場56.12%的佔有率,這反映出菲律賓對國內再生紙(OCC)來源的結構性依賴。由於造紙商將本地包裝的瓦楞紙板與進口A級再生紙(OCC)混合使用,以彌補原生紙漿的短缺,菲律賓再生纖維瓦楞包裝市場持續成長。半化學瓦楞紙板預計將以7.13%的複合年成長率成長,在尋求重量更輕但承載強度相當的產品的島際運輸公司中越來越受歡迎,燃油額外費用的上漲進一步加劇了這一趨勢。原生牛皮箱紙板仍然是農產品和藥品出口的小眾市場,這些產品對防潮性能要求很高,其良好的印刷光澤度和濕強度使其價格較高。

瓦楞紙板芯材市場受惠於聯合紙漿造紙公司新建的日處理量870噸的舊瓦楞紙板(OCC)生產線。此生產線採用PrimeRotor篩網去除雜質,確保紙張寬度一致。此外,隨著農業部投資30億披索(約5,280萬美元)建造99座混合能源冷藏倉庫,高性能塗層的需求也逐漸成長。層級構造紙板採用蠟塗佈或生物塗層襯紙,可防止長途冷藏運輸過程中因冷凝而造成的損壞,從而在菲律賓瓦楞紙包裝市場中開闢出一個盈利的細分領域。進口舊瓦楞紙板價格的波動促使造紙商越來越依賴自有的回收中心,這些中心能夠以可預測的成本提供纖維,即使在電價上漲的情況下也能提高利潤率。

由於B型瓦楞紙板在耐壓性、印刷適性和與自動化裝箱機的兼容性方面表現出色,預計到2025年,其市場佔有率將達到41.37%。加工商正在採用連續式刀片系統,使他們能夠在不造成重大停機的情況下,快速切換B型瓦楞紙板、C型瓦楞紙板和E型瓦楞紙板,從而能夠快速適應季節性飲料托盤和電子設備收縮包裝的需求。 F型瓦楞紙板的厚度僅為B型瓦楞紙板的三分之一,預計其年複合成長率將達到6.89%,因為化妝品和智慧型手錶經銷商更青睞其纖薄的包裝,這種包裝可以裝入宅配袋,並降低體積重量附加費。

目前,菲律賓F型瓦楞紙板包裝市場規模仍小規模,但多道數位印刷技術正在推動單位利潤率的提升。 C型瓦楞紙板在重型罐裝產品的包裝領域仍佔有一席之地,但品牌商正致力於透過更薄的設計來降低上游工程成本。 E型瓦楞紙板也是披薩和服裝郵寄包裝中可折疊紙盒的可靠替代品。同時,A型瓦楞紙板的使用僅限於需要更強緩衝保護的大批量農產品出口。採用更薄的設計與港口現代化進程相契合,這縮短了運輸時間,降低了受潮風險,並使營運商能夠轉向更輕的包裝配置。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務的成長正在加速小包裹數量的成長。

- 快速過渡到永續和可回收紡織包裝

- 擴大加工食品和飲料製造地

- 政府對一次性塑膠製品的監管正在促進紙製品替代品的發展。

- 島際物流網路的現代化催生了對耐用、輕量包裝箱的需求。

- 引入數位印刷技術,為中小企業實現小批量客製化生產。

- 市場限制因素

- 國內和進口再生紙價格波動

- 來自柔軟性塑膠和可重複使用塑膠箱的替代品的威脅。

- 港口堵塞和運輸延誤導致前置作業時間和成本增加。

- 不斷上漲的電費推高了紙板生產機器的營運成本。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 維珍工藝襯板

- 再生襯紙板

- 瓦楞紙板基紙

- 半化學蝕刻

- 其他材料

- 長笛類型

- 長笛

- 低音長笛

- C調長笛

- E 長笛

- F調長笛

- 按包裝類型

- 普通插槽容器

- 客製化模切盒

- 折疊紙箱

- 商店展示

- 托盤箱

- 其他包裝類型

- 依牆體類型

- 單層

- 雙層壁

- 三層壁

- 一邊

- 透過印刷技術

- 柔版印刷

- 數位噴墨列印

- Riso層壓

- 網版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 加工食品

- 生鮮食品和農產品

- 飲料

- 電器產品

- 個人護理化妝品

- 電子商務履約中心

- 製藥

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SCG Packaging Public Company Limited

- San Miguel Yamamura Packaging Corp.

- Liberty Corrugated Boxes Mfg. Corp.

- Valenzuela Packaging Container Corp.

- Quality Corrugated Box Manufacturing Corp.

- Sunpack Container and Packaging Corp.

- Prime Worldwide Paper Packaging Corp.

- Steniel Graham Packaging Philippines Corp.

- Malinta Corrugated Boxes Manufacturing Corp.

- Basic Box Industries Corp.

- Papercon Philippines Inc.

- Central Corrugated Box Corp.

- Duraboard Packaging Corp.

- Three Dimensional Packaging Corp.

- Boxworld Co Inc.

- Basic Box Industries Corp.

- RM Box Center

第7章 市場機會與未來展望

According to Mordor Intelligence, the philippines corrugated packaging market size is projected to expand from USD 2.72 billion in 2025 and USD 2.87 billion in 2026 to USD 3.7 billion by 2031, registering a CAGR of 5.21% between 2026 to 2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, and More), Flute Type (A Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single-Wall, Double-Wall, and More), Printing Technology (Flexographic Printing, and More), End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

Philippines Corrugated Packaging Market Trends and Insights

E-Commerce Growth Accelerating Parcel Volumes

Same-day and next-day delivery commitments have transformed the distribution landscape, swapping palletized store replenishment for millions of single-item drop-offs. Flash-sale peaks on 11-11 and 12-12 force corrugators to stock seasonal blanks and adjust flute combinations that limit freight weight while preserving edge-crush strength. Multi-modal legs across road, sea, and air magnify humidity exposure, steering merchants toward lighter recycled-fiber liners that still pass stacking tests. Fulfillment centers are standardizing box footprints so automated sorters can scan, label, and manifest parcels with minimal human touch. These shifts collectively raise volumes for the Philippines' corrugated packaging market, especially in Metro Manila's parcel hubs.

Government Restrictions on Single-Use Plastics Favoring Paper-Based Alternatives

The Extended Producer Responsibility Act requires brand owners to recover 40% of their plastic packaging footprint in 2024, climbing to 80% by 2028, with fines up to USD 5 million for non-compliance. Simultaneously, the Department of Finance is pressing for a USD 100-per-kilogram excise tax on disposable plastic bags, potentially pushing retail bag prices up 94%. Local ordinances from Quezon City's civic complex ban on plastic disposables to nationwide sachet phase-outs compound the pressure. Brand owners now specify corrugated secondary packs and fiber-based takeout containers that score favorably on recyclability audits. These mandates are nudging procurement managers to lock in extra corrugated volumes, fortifying the growth arc of the Philippines corrugated packaging market.

Volatility in Domestic and Imported Recovered Paper Prices

Import OCC quotes swung from USD 160 per tonne for European 95/5 to USD 230 per tonne for U.S. DS-OCC in 2024 as U.S. and EU collection rates dipped and Indonesian inspection fees rose. Local converters suffer double exposure: higher landed costs on imported grades and erratic street-price jumps when informal-sector collectors thin out supply. Only 44% of barangays operate functional materials-recovery facilities, with Metro Manila's coverage at 20%, leaving mills vulnerable to cargo arrival lags and fiber quality downgrades. These shocks crimp gross margins and temper near-term investment appetite in the Philippines corrugated packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Shift Toward Sustainable and Recycled Fiber Packaging

- Expansion of Processed Food and Beverage Manufacturing Hubs

- Port Congestion and Shipping Delays Inflating Lead Times and Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard captured 56.12% of the Philippines corrugated packaging market in 2025, reflecting structural dependence on domestic OCC streams. The Philippines' corrugated packaging market for recycled fiber continues to grow as mills blend locally baled cartons with imported Class A OCC to offset the scarcity of virgin pulp. Semi-chemical fluting, forecast to grow at a 7.13% CAGR, is gaining favor among inter-island shippers seeking lighter grammages with similar stacking strength, a shift amplified by rising fuel surcharges. Virgin Kraft linerboard remains a niche for moisture-critical produce and pharmaceutical exports, where print gloss and wet-strength ratings justify the premium.

The corrugating medium benefits from United Pulp and Paper's new 870-TPD OCC line, which filters contaminants using PrimeRotor screens to stabilize runnability. Demand for performance coatings is inching up as the Department of Agriculture spends PHP 3 billion (USD 52.8 million) on 99 hybrid-energy cold storages. Triple-wall blanks with wax or bio-coated liners prevent condensation damage on long reefers, creating a profitable specialty pocket within the broader Philippines corrugated packaging market share landscape. Imported OCC volatility continues to push mills toward captive collection centers that lock in fiber at predictable costs, strengthening margins even as power tariffs rise.

B flute secured 41.37% market share in 2025 thanks to its balance of crush resistance, print surface, and compatibility with automatic case packers. Converters run continuous-knife setups that switch from B to C to E flute without major downtime, allowing rapid response to seasonal beverage trays or electronics shrink-wrap replacements. F flute, one-third the caliper of B, is projected for 6.89% CAGR as cosmetics and smart-watch sellers opt for slimmer parcels that fit courier pouches and reduce dimensional weight surcharges.

The Philippines corrugated packaging market size for F flute remains modest today yet offers higher unit margins because of multi-pass digital graphics. C flute maintains a foothold in heavy canned-goods packs, but brand owners eye upstream savings from thinner profiles. E flute doubles as a rigid alternative to folding cartons for pizza and apparel mailers, while A flute's usage is confined to bulk agro-exports requiring superior cushioning. Thin-profile adoption aligns with port modernization that reduces voyage time, easing moisture-ingress risks and enabling merchants to shift toward lighter makeup.

List of Companies Covered in this Report:

- SCG Packaging Public Company Limited

- San Miguel Yamamura Packaging Corp.

- Liberty Corrugated Boxes Mfg. Corp.

- Valenzuela Packaging Container Corp.

- Quality Corrugated Box Manufacturing Corp.

- Sunpack Container and Packaging Corp.

- Prime Worldwide Paper Packaging Corp.

- Steniel Graham Packaging Philippines Corp.

- Malinta Corrugated Boxes Manufacturing Corp.

- Basic Box Industries Corp.

- Papercon Philippines Inc.

- Central Corrugated Box Corp.

- Duraboard Packaging Corp.

- Three Dimensional Packaging Corp.

- Boxworld Co Inc.

- Basic Box Industries Corp.

- RM Box Center

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Growth Accelerating Parcel Volumes

- 4.2.2 Rapid Shift Toward Sustainable and Recycled Fiber Packaging

- 4.2.3 Expansion of Processed Food and Beverage Manufacturing Hubs

- 4.2.4 Government Restrictions on Single-Use Plastics Favoring Paper-Based Alternatives

- 4.2.5 Modernization of Inter-Island Logistics Networks Demanding Durable Lightweight Boxes

- 4.2.6 Adoption of Digital Printing Enabling Short-Run Customization for SMEs

- 4.3 Market Restraints

- 4.3.1 Volatility in Domestic and Imported Recovered Paper Prices

- 4.3.2 Substitution Threat From Flexible Plastics and Reusable Plastic Crates

- 4.3.3 Port Congestion and Shipping Delays Inflating Lead Times and Costs

- 4.3.4 Escalating Electricity Tariffs Increasing Corrugator Operating Expenses

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-commerce Fulfillment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SCG Packaging Public Company Limited

- 6.4.2 San Miguel Yamamura Packaging Corp.

- 6.4.3 Liberty Corrugated Boxes Mfg. Corp.

- 6.4.4 Valenzuela Packaging Container Corp.

- 6.4.5 Quality Corrugated Box Manufacturing Corp.

- 6.4.6 Sunpack Container and Packaging Corp.

- 6.4.7 Prime Worldwide Paper Packaging Corp.

- 6.4.8 Steniel Graham Packaging Philippines Corp.

- 6.4.9 Malinta Corrugated Boxes Manufacturing Corp.

- 6.4.10 Basic Box Industries Corp.

- 6.4.11 Papercon Philippines Inc.

- 6.4.12 Central Corrugated Box Corp.

- 6.4.13 Duraboard Packaging Corp.

- 6.4.14 Three Dimensional Packaging Corp.

- 6.4.15 Boxworld Co Inc.

- 6.4.16 Basic Box Industries Corp.

- 6.4.17 RM Box Center

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中國瓦楞紙板包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中國瓦楞紙板包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。美國瓦楞紙包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印尼瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板包裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。美國瓦楞紙包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印尼瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板包裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)