|

市場調查報告書

商品編碼

2061750

美國瓦楞紙包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

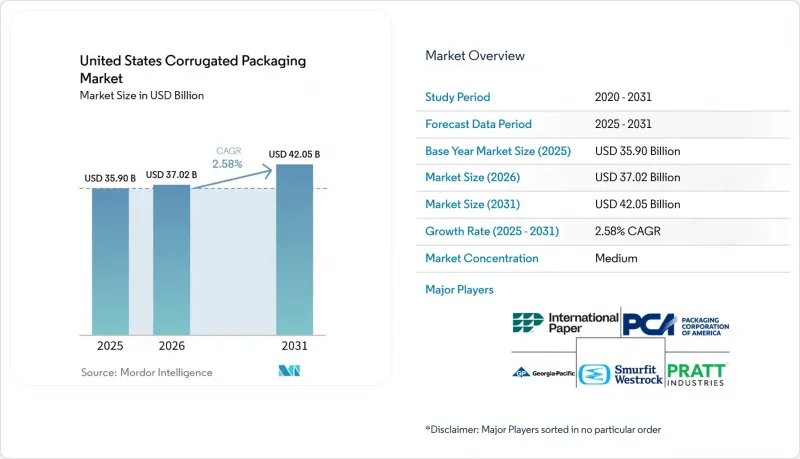

據 Mordor Intelligence 稱,2025 年美國瓦楞紙板包裝市場價值為 359 億美元,預計到 2031 年將達到 420.5 億美元,而 2026 年為 370.2 億美元,預測期(2026-2031 年)的複合年成長率為 2.58%。

本報告按材料(原生牛皮箱紙板、再生紙板等)、瓦楞類型(A型瓦楞等)、包裝類型(普通開槽紙盒等)、壁厚結構(單層、雙層等)、印刷技術(柔版印刷等)和終端用戶行業(加工食品等)進行細分。市場預測以美元計價。

美國瓦楞紙板包裝市場趨勢與洞察

電子商務履約需求激增

美國瓦楞紙包裝市場正以前所未有的速度擴張,小包裹遞送網路承諾當日送達。到2025年,亞馬遜、沃爾瑪和第三方物流公司將新增超過5,000萬平方英尺的履約空間,而每個設施都需要符合精確厚度公差的自動化紙箱。宅配業者以體積重量收費的做法促使托運人要求使用尺寸合適的包裝,從而增加了對客製化模切包裝的需求。 Smurfit Westrock公司的「Track Vision」平台預計到2025年將追蹤超過130萬個包裹,展示了數位雙胞胎如何減少空轉次數。為此,國際紙業公司決定投資2.25億美元在密西西比州新建一家工廠,以維持其在美國東南部主要都會區提供當日送達的服務。該工廠計劃於 2027 年底投入運作。因此,履約變得更加集中,在美國瓦楞紙板包裝市場,區域產能正在整合,從而縮短了前置作業時間。

轉向塑膠替代品和強制性循環經濟

加州、科羅拉多州、緬因州、馬裡蘭州、明尼蘇達州、奧勒岡州和佛蒙特州的「生產者延伸責任制」(EPR)法規要求品牌所有者為回收和分揀系統資金籌措,這為紡織基材料的發展提供了政策推動力。光是加州參議院第54號法案就規定,到2032年,一次性包裝的回收率必須達到65%,這將促進瓦楞紙板材料的選擇,而瓦楞紙板的回收率目前已高達71-76%。為了抓住這些法規帶來的需求,普拉特工業公司投資1.2億美元,於2025年在喬治亞華納羅賓斯開設了一家再生材料複合工廠。即將提交國會審議的《STEWARD法案》預計將實現全國範圍內的監管統一,並降低合規成本。隨著政策推進的加速,美國瓦楞紙包裝市場正受惠於其閉合迴路紡織基礎設施。

牛皮紙漿供應鏈持續波動

2026年,中國短纖維紙漿基準價格上漲至約每噸570美元,而美國北部漂白針葉木牛皮紙漿在2026年1月的價格維持在每噸730美元左右。 2026年1月,Domtar公司關閉了位於克羅夫頓的工廠,該工廠年產能為38萬噸,導致調整產能下降,迫使美國箱板紙廠轉而採購高成本更高的斯堪地那維亞紙漿。 2026年初,從北歐到美國沿岸地區的海運費用超過每個40英尺貨櫃3,200美元,推高了收貨成本。這些趨勢威脅到美國瓦楞紙包裝市場中非一體化加工商的利潤率,推動了垂直整合和長期供應合約的簽訂。

細分市場分析

預計到2025年,再生瓦楞紙板將維持61.57%的市場佔有率並確立成本優勢,而原生牛皮瓦楞紙板預計將以3.03%的複合年成長率推動材料市場成長。化妝品和電子產業對印刷品質日益成長的需求,推動了對原生纖維光滑表面的需求。 Domtal工廠的關閉導致原生紙漿供應緊張,現貨價格上漲至每噸730美元。在此價位上,原生紙漿與傳統再生材料的價格差距正在縮小。由於許多品牌現在都指定使用森林管理委員會(FSC)認證的產品,因此,能夠平衡再生纖維和原生纖維使用的造紙商有機會贏得合約。因此,高品質的印刷應用正在為美國瓦楞包裝市場帶來新的價值來源。

循環經濟監管的日益嚴格推動了高再生紙漿含量產品的市場成長,而普拉特工業公司正是這一領域的主要參與者。然而,像白色面層紙板這樣的混合材料在商店展示領域也越來越受歡迎。國際紙業公司每年處理700萬噸廢棄舊瓦楞紙箱,從而減少了對進口紙漿的依賴,並強化了其內部纖維回收循環。由此形成的層級構造材料生態系統意味著,在美國瓦楞紙包裝市場,性能和品牌要求以及價格如今都影響著纖維的選擇。

儘管C型瓦楞紙板在2025年佔出貨量的39.10%,但預計到2031年,E型瓦楞紙板將以4.13%的複合年成長率超越所有其他類型,因為消費電子和化妝品行業在保持保護性能的同時,也需要更輕的包裝。 E型瓦楞紙板具有諸多功能優勢,例如其更薄的瓦楞厚度使其體積重量更低,並且適用於機器人包裝生產線。此外,它也符合個人化包裝的趨勢,因為數位噴墨印表機可以在微型瓦楞紙板上更清晰地列印圖案。對於易碎的玻璃和陶瓷製品,A型瓦楞紙板仍然提供最佳的緩衝性能,但其市場佔有率正在下降,因為加工商正在重新設計襯墊,而不是過度定製紙板。這些成分的變化持續加大美國瓦楞包裝市場創新的壓力。

適用於機器人的紙箱需要嚴格的厚度控制,這有利於運作先進製程監控系統的大規模一體化工廠。 Smurfit Westrock 和 BHS Corrugate 已針對微型瓦楞紙板最佳化了瓦楞紙板的生產設備和印刷生產線,幫助大型企業維持市場佔有率。小規模送紙機可滿足特定生產需求,但在更換瓦楞形狀時會產生更高的浪費風險。因此,低矮瓦楞紙板的單位成本經濟競爭將推動美國瓦楞包裝市場的資本投資週期。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務履約需求激增

- 向塑膠替代品過渡和強制性循環經濟

- 擴大當日生鮮配送網路

- RFID嵌入式智慧瓦楞紙箱的技術整合

- D2C訂閱服務的成長

- 加速製造業向美國近岸外包

- 市場限制因素

- 牛皮紙漿供應鏈持續波動

- 能源成本上漲對瓦楞紙板原紙生產經濟的影響

- 擴大農業供應鏈中可重複使用塑膠容器的使用

- 監管壓力對森林管理認證的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 維珍工藝襯板

- 再生襯紙板

- 瓦楞紙板基紙

- 半化學蝕刻

- 其他材料

- 長笛類型

- 長笛

- 低音長笛

- C調長笛

- E 長笛

- F調長笛

- 按包裝類型

- 普通插槽容器

- 客製化模切盒

- 折疊紙箱

- 商店展示

- 托盤箱

- 其他包裝類型

- 透過牆體結構

- 單層

- 雙層壁

- 三層壁

- 一邊

- 透過印刷技術

- 柔版印刷

- 數位噴墨列印

- Riso層壓

- 網版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 加工食品

- 生鮮食品和農產品

- 飲料

- 紙製品

- 電器產品

- 個人護理化妝品

- 電子商務履約中心

- 製藥

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- International Paper Company

- Smurfit Westrock plc

- Packaging Corporation of America

- Georgia-Pacific LLC

- Pratt Industries Inc.

- Sonoco Products Company

- Cascades Inc.

- The BoxMaker Inc.

- Mondi Group

- Jamestown Container Companies

- Graphic Packaging Holding Company

- R&R Corrugated Packaging Group

- Great Little Box Company Ltd.

- Liberty Corrugated LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states corrugated packaging market size was valued at USD 35.90 billion in 2025 and estimated to grow from USD 37.02 billion in 2026 to reach USD 42.05 billion by 2031, at a CAGR of 2.58% during the forecast period (2026-2031).

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, and More), Flute Type (A Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single, Double, and More), Printing Technology (Flexographic, and More), and End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Corrugated Packaging Market Trends and Insights

E-Commerce Fulfilment Demand Surge

The United States corrugated packaging market is expanding fastest, where parcel networks promise same-day delivery. Amazon, Walmart, and third-party logistics firms added more than 50 million square feet of fulfillment space in 2025, each facility requiring automation-compatible boxes that hold precise caliper tolerances. Dimensional-weight fees from parcel carriers push shippers toward right-sized packaging, which lifts demand for custom die-cut formats. Smurfit Westrock's Track Vision platform traced over 1.3 million packages in 2025 and illustrated how digital twins reduce empty-mile trucking. International Paper responded by committing USD 225 million to a greenfield plant in Mississippi, scheduled for late 2027, to stay within a one-day delivery radius of major southeastern metros. Fulfillment density is therefore reinforcing regional capacity clusters and shortening lead times across the United States corrugated packaging market.

Shift Toward Plastic Substitution And Circular Economy Mandates

Extended producer responsibility rules in California, Colorado, Maine, Maryland, Minnesota, Oregon, and Vermont require brand owners to finance collection and sorting systems, creating a policy tailwind for fiber substrates. California Senate Bill 54 alone mandates a 65% recycling rate for single-use packaging by 2032, tilting material selection toward corrugated grades, which already have a 71-76% recovery rate. Pratt Industries opened a USD 120 million recycled-content plant in Warner Robins, Georgia, in 2025 to capture demand from these mandates. Federal STEWARD Act deliberations in Congress could harmonize rules nationwide and compress compliance costs. As policy momentum accelerates, the United States corrugated packaging market benefits from its closed-loop fibre infrastructure.

Ongoing Kraft Pulp Supply Chain Volatility

China's short-fiber pulp benchmark for 2026 rose to roughly USD 570 per ton, while domestic northern bleached softwood kraft held near USD 730 per ton in January 2026. Domtar's January 2026 closure of its 380,000-ton Crofton mill removed swing capacity and forced U.S. linerboard mills to source higher-cost Scandinavian pulp. Ocean freight from Northern Europe to the Gulf Coast exceeded USD 3,200 per forty-foot container early in 2026, pushing landed costs higher. These dynamics threaten margins for non-integrated converters inside the United States corrugated packaging market and encourage vertical integration or long-term supply contracts.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Same-Day Grocery Delivery Networks

- Technological Integration Of RFID-Embedded Smart Corrugated Boxes

- Rising Energy Costs Impacting Boxboard Production Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard maintained 61.57% share in 2025, anchoring cost leadership, yet virgin kraft linerboard is forecast to pace material growth at a 3.03% CAGR. Print-quality requirements in cosmetics and electronics are pulling demand toward the smoother surface that virgin fiber delivers. Domtar's mill closure tightened virgin supply, nudging spot pulp toward USD 730 per ton, a level that narrows traditional recycled discounts. Many brands now specify Forest Stewardship Council certificates, so mills balancing recycled and virgin fiber can win contracts. Consequently, premium graphics applications are injecting fresh value pools into the United States corrugated packaging market.

Rising circular-economy mandates favor high recycled content, a space where Pratt Industries operates exclusively. Yet blended options such as white-top linerboard are gaining traction in point-of-purchase displays. International Paper already processes 7 million tons of old corrugated containers annually, reducing exposure to imported pulp and reinforcing internal fiber loops. The resulting two-tier material ecosystem ensures that performance and branding demands, rather than price alone, govern fiber choice across the United States corrugated packaging market.

C flute commanded 39.10% of 2025 shipments, but E flute is projected to outpace all others at a 4.13% CAGR through 2031 as consumer electronics and cosmetics seek lighter packs that remain protective. Thinner calipers cut dimensional weight and suit robotic packing lines, giving E flute a functional edge. Digital inkjet presses also print more cleanly on micro flutes, aligning with the trend toward personalized packaging. For fragile glassware and ceramics, A flute still offers the highest cushioning, yet its share is declining as converters redesign inserts rather than over-specify board. These mix shifts keep innovation pressure high within the United States corrugated packaging market.

Robot-friendly boxes need tight caliper control, which favors large integrated facilities running advanced process monitors. Smurfit Westrock and BHS Corrugated have tailored corrugators and press lines for micro flutes, helping big players defend their share. Smaller sheet feeders fill niche runs but must absorb higher scrap risk when shifting between flute profiles. The battle for unit economics at thin calipers will therefore shape equipment investment cycles across the United States corrugated packaging market.

List of Companies Covered in this Report:

- International Paper Company

- Smurfit Westrock plc

- Packaging Corporation of America

- Georgia-Pacific LLC

- Pratt Industries Inc.

- Sonoco Products Company

- Cascades Inc.

- The BoxMaker Inc.

- Mondi Group

- Jamestown Container Companies

- Graphic Packaging Holding Company

- R&R Corrugated Packaging Group

- Great Little Box Company Ltd.

- Liberty Corrugated LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Fulfillment Demand Surge

- 4.2.2 Shift Toward Plastic Substitution and Circular Economy Mandates

- 4.2.3 Expansion of Same-Day Grocery Delivery Networks

- 4.2.4 Technological Integration of RFID-Embedded Smart Corrugated Boxes

- 4.2.5 Growth of Direct-to-Consumer Subscription Services

- 4.2.6 Accelerating Nearshoring of Manufacturing to the United States

- 4.3 Market Restraints

- 4.3.1 Ongoing Kraft Pulp Supply Chain Volatility

- 4.3.2 Rising Energy Costs Impacting Boxboard Production Economics

- 4.3.3 Increasing Adoption of Reusable Plastic Containers in Produce Supply Chains

- 4.3.4 Regulatory Pressure on Forest Stewardship Certifications

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Paper Products

- 5.6.5 Electrical Products

- 5.6.6 Personal Care and Cosmetics

- 5.6.7 E-commerce Fulfillment Centers

- 5.6.8 Pharmaceuticals

- 5.6.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 International Paper Company

- 6.4.2 Smurfit Westrock plc

- 6.4.3 Packaging Corporation of America

- 6.4.4 Georgia-Pacific LLC

- 6.4.5 Pratt Industries Inc.

- 6.4.6 Sonoco Products Company

- 6.4.7 Cascades Inc.

- 6.4.8 The BoxMaker Inc.

- 6.4.9 Mondi Group

- 6.4.10 Jamestown Container Companies

- 6.4.11 Graphic Packaging Holding Company

- 6.4.12 R&R Corrugated Packaging Group

- 6.4.13 Great Little Box Company Ltd.

- 6.4.14 Liberty Corrugated LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)菲律賓瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國瓦楞紙板包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

南美瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)菲律賓瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國瓦楞紙板包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印尼瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板包裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

瓦楞紙板包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。亞太地區瓦楞紙包裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)印尼瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度瓦楞紙包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡瓦楞紙包裝市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板包裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)