|

市場調查報告書

商品編碼

2063311

歐洲貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Europe Freight Brokerage Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

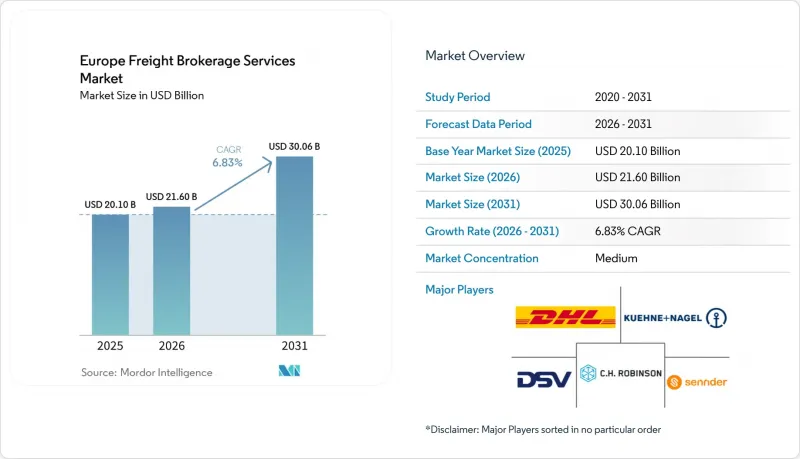

據 Mordor Intelligence 稱,歐洲貨運代理市場預計將從 2025 年的 201 億美元成長到 2026 年的 216 億美元,到 2031 年達到 300.6 億美元,2026 年至 2031 年的複合年成長率為 6.83%。

中歐製造業回流正將貨運量轉移到歐盟內部運輸路線,而歐盟範圍內電子運單的引入則加快了交易速度並提高了審計追蹤的透明度。本報告按服務類型(整車運輸、零擔運輸)、車輛類型(乾貨車、冷藏車等)、運輸距離(長途、區域內、近距離)、商業模式(傳統模式、資產持有模式等)、最終用戶(製造業/汽車業、建築業等)、客戶規模(大型企業、中型企業、小規模企業)以及國家/地區(德國、英國、其他國家/地區(德國地區)進行細分。市場預測以美元計價。

歐洲貨運代理服務市場的趨勢與洞察

由於製造業回流,歐盟製造業貨運量激增。

汽車和電子產品製造商正將產能從亞洲轉移到波蘭和捷克共和國,從而增加了東西走廊沿線的往返貨運量。 Waberer公司新增了鐵路物流服務,支持向維謝格拉德地區的工廠提供即時零件供應,預計2024年銷售額將達到7.575億歐元(8.925億美元),年增6.5%。由於工廠生產計畫的波動幅度很小,能夠確保這些路線貨運能力穩定的仲介將獲得定價權。然而,他們還必須應對跨境運輸法規,例如國內運輸、駕駛人工作時間和基於二氧化碳排放的通行費等,這些法規因國家而異。

歐盟範圍內電子運單(eCMR)的實施

目前,已有34個歐洲國家認可eCMR作為合法的交貨證明,從而減少了邊境文書工作造成的延誤,並使仲介能夠更快地開立發票。 2025年4月,Transporeon將eCMR整合到其貨運市場平台,使貨運代理商能夠競標現貨貨運並即時取得電子簽章。對於處理單次貨運中多個取貨和送貨的零擔貨運仲介而言,文件工作流程的自動化降低了每個托盤的管理成本,並最佳化了現金流量。

柴油和AdBlue價格的波動給中間商利潤帶來了壓力。

燃油價格上漲正在縮小客戶固定報價與承運商實際發票之間的利潤空間。德國引入的與二氧化碳排放掛鉤的卡車通行費進一步加劇了成本的不確定性,迫使仲介實施浮動燃油額外費用,而一些托運人對此持抵制態度。無法對沖風險的中小型仲介業者正在將業務出售給規模更大、財務狀況更穩定的集團。

細分市場分析

到2025年,整車運輸(FTL)在歐洲貨運代理市場將保持58.45%的佔有率,這得益於可預測的工廠到配送中心(DC)路線和準時交貨。同時,輕型卡車運輸(LTL)預計將以8.75%的複合年成長率成長,這主要受電子商務帶來的小型化趨勢以及貨物共乘經濟效益的推動,後者提高了拖車裝載效率。數位化平台在零擔運輸領域表現卓越,它們利用演算法識別人工容易忽略的取貨點,從而縮短了取貨到交付的周期。

仲介正擴大採用混合模式,將合約式整車運輸(用於可預測路線)與零擔運輸(用於吸收過剩運力)相結合。藥品托運人通常透過整車運輸常溫貨物,同時將溫控托盤貨物轉運至認證的零擔運輸網路以控制成本,這從戰略上增加了仲介管理這兩種服務類型並遵守監管鏈協議的需求。隨著原料藥的普及,托運人希望在同一平台上即時取得整車和零擔的報價,這進一步模糊了歐洲貨運仲介市場的營運界線。

由於乾貨車用途廣泛且資產可用性高,其在歐洲貨運仲介市場中佔比高達 41.66%。然而,隨著疫苗、胰島素和生鮮食品的供應逐漸恢復正常,冷藏貨車市場預計到 2031 年將以 9.57% 的複合年成長率成長。由於溫度偏差的監管罰款可能會抵消整體貨運利潤,因此,能夠檢驗冷藏車感測器數據並提供異常情況分析的仲介正從中獲利。

平板拖車和階梯式拖車仍然容易受到經濟週期的影響,因為它們依賴建築開工和基礎設施資金籌措。隨著化學品和食用油需求的成長,油罐車的需求也在穩步成長,但高昂的安全培訓成本仍然是准入門檻。因此,仲介選擇專業方向取決於他們是追求運輸量的穩定性還是高利潤,而隨著歐洲貨運經紀市場貨物類型的多樣化,這種權衡取捨變得越來越明顯。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 由於製造業回流,歐盟製造業貨運量激增。

- 歐盟範圍內電子運單(eCMR)的實施

- 人工智慧驅動的動態定價釋放了隱藏車道的盈利。

- mRNA和生物製藥物流導致低溫運輸需求激增

- 都市區的微型倉配中心正在分割最後一公里配送路線。

- 創業投資整合數位仲介

- 市場限制因素

- 柴油和AdBlue價格的波動正在縮小仲介之間的價差。

- 歐盟的《供應鏈實質審查法》加重了合規負擔。

- 網路攻擊日益猖獗,正在削弱貨運商對數位平台的信任。

- 跨境收費標準的不一致導致管理成本飆升。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模及成長預測(價值,10億美元)

- 按服務

- 全軌道公路(FTL)

- 低於100%的運費(零擔運輸)

- 其他

- 按設備類型/按拖車類型

- 乾燒

- 冷藏車

- 平板/階梯式平板車

- 油輪(散裝液體和化學品)

- 其他

- 按運輸距離

- 長途運輸(超過 500 英里)

- 按地區(100-500英里)

- 近距離(不到100英里)

- 按經營模式

- 傳統貨運代理

- 資產持有型貨運經紀

- 代理貨運經紀

- 數位貨運代理

- 按最終用戶行業分類

- 製造業/汽車

- 建築和基礎設施項目

- 石油、天然氣、採礦、化工

- 農業/食品/飲料

- 零售、快速消費品和批發分銷

- 醫療和藥品

- 電子商務與第三方物流履約

- 其他終端用戶產業

- 按客戶規模

- 大型企業貨運商(年營業額超過1億美元)

- 中型貨運公司(年營業額1000萬美元至1億美元)

- 中小企業(營業額低於1000萬美元)

- 國家

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 比利時

- 北歐國家(瑞典、丹麥、挪威、芬蘭)

- 波蘭

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- CH Robinson

- EMO Trans

- XPO Inc.

- Kuehne+Nagel

- Sennder

- DSV A/S

- GEODIS

- CMA CGM Group(Including CEVA Logistics)

- Dachser

- Hellmann Worldwide Logistics

- Transporeon

- LKW WALTER

- Girteka Logistics

- Waberer's Group

- Ewals Cargo Care

- Rhenus Logistics

- Yusen Logistics(Part of NYK Line)

- Raben Group

- Scan Global Logistics

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe freight brokerage market size is expected to increase from USD 20.10 billion in 2025 to USD 21.60 billion in 2026 and reach USD 30.06 billion by 2031, growing at a 6.83% CAGR over 2026-2031.

Manufacturing reshoring across Central Europe is re-routing freight volumes toward intra-EU lanes, while the EU-wide rollout of electronic consignment notes is accelerating transaction velocity and audit-trail transparency. This report is Segmented by Service (FTL, LTL), by Equipment (Dry, Refrigerated Van, and More), by Haul (Long-Haul, Regional, Local), by Business (Traditional, Asset-Based, and More), by End-User (Manufacturing & Automotive, Construction, and More), by Customer Size (Large, Mid-Market, Small Business), and by Country (Germany, UK, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Freight Brokerage Services Market Trends and Insights

Reshoring-Driven Surge in Intra-EU Manufacturing Freight

Automotive and electronics producers are relocating capacity from Asia into Poland and Czechia, increasing round-trip hauls on east-west corridors. Waberer's recorded EUR 757.5 million (USD 892.5 million) revenue in 2024, up 6.5%, after adding rail logistics services that anchor just-in-time parts flows for factories in the Visegrad region. Brokers that can secure predictable capacity across these lanes gain pricing power because plant schedules tolerate minimal variance. However, they must also manage border-crossing rules on cabotage, driver work-hours, and CO2-based tolls, which differ by country.

EU-Wide Rollout of Electronic Freight Documents (eCMR)

Thirty-four European states now recognize eCMR as legal proof of delivery, trimming paperwork delays at borders and enabling brokers to bill faster. Transporeon embedded eCMR into its Freight Marketplace in April 2025, allowing forwarders to tender spot loads and capture electronic signatures in real time. For LTL brokers that juggle multiple hand-offs per trip, automated document workflows lower administrative costs per pallet and strengthen cash-flow cycles.

Diesel & AdBlue Price Volatility Compresses Brokerage Spreads

Fuel spikes narrow margins between fixed customer quotes and carrier invoices. Germany's new CO2-indexed truck toll compounds cost unpredictability, pushing brokers to introduce floating fuel surcharges that some shippers resist. Smaller intermediaries, unable to hedge exposure, are selling to well-capitalized groups.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Dynamic Pricing Unlocks Hidden Lane Profitability

- Booming Cold-Chain Demand from mRNA and Biopharma Logistics

- EU Supply-Chain Due-Diligence Law Raises Compliance Overhead

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full-truckload retained 58.45% of the Europe freight brokerage market share in 2025, anchored by predictable factory-to-DC routes and time-critical deliveries. Less-than-truckload, however, is projected to expand at 8.75% CAGR, propelled by e-commerce parcelization and the economics of load pooling that improve trailer fill rates. Digital platforms excel in LTL because algorithms identify consolidation points humans overlook, compressing pickup-to-delivery cycles.

Brokers increasingly run hybrid models, blending contracted FTL for predictable lanes with spot LTL to absorb surplus capacity. Pharmaceutical shippers often allocate ambient FTL but divert temperature-sensitive pallets into certified LTL networks to control cost, reinforcing the strategic need for brokers to manage both service types without breaking chain-of-custody protocols. As APIs proliferate, shippers expect instant access to both FTL and LTL quotes inside the same dashboard, further blurring operational boundaries inside the Europe freight brokerage market.

Dry vans delivered 41.66% of Europe freight brokerage market size, thanks to versatility and asset availability. Yet refrigerated vans are on a 9.57% CAGR trajectory through 2031 as vaccine, insulin, and fresh-food flows normalize at elevated baselines. The Brokers that validate reefer sensor data and provide exception dashboards earn premium margins because regulatory fines for temperature excursions can wipe out entire shipment profits.

Flatbed and step-deck trailers remain cyclical, tied to construction starts and infrastructure funding. Tanker demand grows modestly with chemicals and edible oils, but high safety training costs act as a barrier to entry. Specialization decisions therefore, hinge on whether brokers seek volume stability or margin premium, a trade-off increasingly visible as the Europe freight brokerage market diversifies cargo profiles.

List of Companies Covered in this Report:

- DHL Group

- C.H. Robinson

- EMO Trans

- XPO Inc.

- Kuehne+Nagel

- Sennder

- DSV A/S

- GEODIS

- CMA CGM Group (Including CEVA Logistics)

- Dachser

- Hellmann Worldwide Logistics

- Transporeon

- LKW WALTER

- Girteka Logistics

- Waberer's Group

- Ewals Cargo Care

- Rhenus Logistics

- Yusen Logistics (Part of NYK Line)

- Raben Group

- Scan Global Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Reshoring-driven surge in intra-EU manufacturing freight

- 4.2.2 EU-wide rollout of electronic freight documents (eCMR)

- 4.2.3 AI-driven dynamic pricing unlocks hidden lane profitability

- 4.2.4 Booming cold-chain demand from mRNA and biopharma logistics

- 4.2.5 Urban micro-fulfilment hubs fragment last-mile road legs

- 4.2.6 Venture-capital-fuelled consolidation among digital brokers

- 4.3 Market Restraints

- 4.3.1 Diesel & AdBlue price volatility compresses brokerage spreads

- 4.3.2 EU supply-chain due-diligence law raises compliance overhead

- 4.3.3 Escalating cyber-attacks erode shipper trust in digital platforms

- 4.3.4 Persisting cross-border toll heterogeneity inflates admin costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Bn)

- 5.1 By Service

- 5.1.1 Full-Truckload (FTL)

- 5.1.2 Less-than-Truckload (LTL)

- 5.1.3 Others

- 5.2 By Equipment / Trailer Type

- 5.2.1 Dry Van

- 5.2.2 Refrigerated Van

- 5.2.3 Flatbed / Step-Deck

- 5.2.4 Tanker (Bulk Liquid and Chemical)

- 5.2.5 Others

- 5.3 By Haul Length

- 5.3.1 Long-Haul (More than 500 miles)

- 5.3.2 Regional (100-500 miles)

- 5.3.3 Local (Less than 100 miles)

- 5.4 By Business Model

- 5.4.1 Traditional Freight Brokerage

- 5.4.2 Asset-Based Freight Brokerage

- 5.4.3 Agent Model Freight Brokerage

- 5.4.4 Digital Freight Brokerage

- 5.5 By End-User Industry

- 5.5.1 Manufacturing and Automotive

- 5.5.2 Construction and Infrastructure Projects

- 5.5.3 Oil, Gas, Mining and Chemicals

- 5.5.4 Agriculture and Food / Beverage

- 5.5.5 Retail, FMCG and Wholesale Distribution

- 5.5.6 Healthcare and Pharmaceuticals

- 5.5.7 E-commerce and 3PL Fulfilment

- 5.5.8 Other End-User Industry

- 5.6 By Customer Size

- 5.6.1 Large Enterprise Shippers (More than USD 100 M)

- 5.6.2 Mid-Market Shippers (USD 10-100 M)

- 5.6.3 Small Businesses (Less than USD 10 M)

- 5.7 By Country

- 5.7.1 Germany

- 5.7.2 United Kingdom

- 5.7.3 France

- 5.7.4 Italy

- 5.7.5 Spain

- 5.7.6 Netherlands

- 5.7.7 Belgium

- 5.7.8 Nordics (Sweden, Denmark, Norway, Finland)

- 5.7.9 Poland

- 5.7.10 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 C.H. Robinson

- 6.4.3 EMO Trans

- 6.4.4 XPO Inc.

- 6.4.5 Kuehne+Nagel

- 6.4.6 Sennder

- 6.4.7 DSV A/S

- 6.4.8 GEODIS

- 6.4.9 CMA CGM Group (Including CEVA Logistics)

- 6.4.10 Dachser

- 6.4.11 Hellmann Worldwide Logistics

- 6.4.12 Transporeon

- 6.4.13 LKW WALTER

- 6.4.14 Girteka Logistics

- 6.4.15 Waberer's Group

- 6.4.16 Ewals Cargo Care

- 6.4.17 Rhenus Logistics

- 6.4.18 Yusen Logistics (Part of NYK Line)

- 6.4.19 Raben Group

- 6.4.20 Scan Global Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026年全球仲介業者轉運板市場報告

2026年全球仲介業者轉運板市場報告 法國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)西班牙貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)貨運代理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)東協貨運代理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)北美貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

法國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)西班牙貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)貨運代理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)東協貨運代理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)北美貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 貨運代理服務市場:依服務類型、運輸方式、客戶規模、貨物類型、技術應用及最終用戶產業分類-2026-2032年全球市場預測美國整車貨運經紀市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

貨運代理服務市場:依服務類型、運輸方式、客戶規模、貨物類型、技術應用及最終用戶產業分類-2026-2032年全球市場預測美國整車貨運經紀市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 全球貨運仲介市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球貨運仲介市場規模、佔有率、趨勢和成長分析報告(2026-2034)