|

市場調查報告書

商品編碼

1940816

美國整車貨運經紀市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)United States FTL Freight Brokerage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

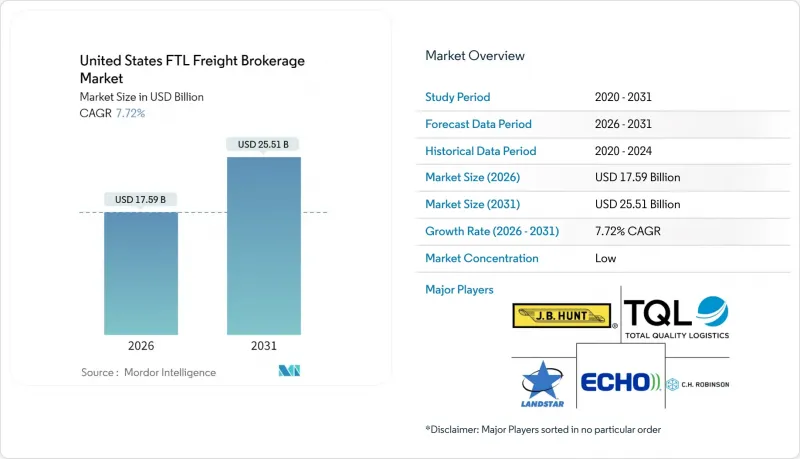

2025 年美國整車貨運經紀市場價值 163.3 億美元,預計到 2031 年將達到 255.1 億美元,高於 2026 年的 175.9 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 7.72%。

這種規模和成長軌跡凸顯了托運人如何迅速將採購方式轉向數位化、第三方整車運輸專家,其驅動力在於滿足電子商務需求、近岸外包以及基礎設施投資。平台主導的仲介業者整合了預測定價、API 連接和自動化合規性檢查,以減少人工環節、縮短結算週期並整合貨運量。同時,集中的購買力使頂級仲介能夠在司機隊伍老化、柴油價格波動和信貸緊縮等情況下確保運力。因此,隨著供應鏈數位化、跨境貨運量增加以及托運人尋求透過貨物整合來降低成本的策略,技術領先、深厚的承運商關係和多元化的設備組合正成為關鍵優勢。

美國整車貨運經紀市場趨勢與洞察

履約需求爆炸性成長

分散式庫存策略需要精細的運力管理,而傳統的自有資產承運商難以有效應對。借助人工智慧驅動的整合引擎,仲介透過減少空駛里程和縮短高達 35% 的運輸週期,降低了全通路零售商的服務成本。位於人口密集都市區的微型倉配中心促進了頻繁的小批量整車運輸,使仲介業者能夠快速匹配運力,從而獲益。快速送達客戶仍然是重中之重,這使得貨運代理能夠為緊急貨物的多站路線提供溢價,並鞏固了美國整車貨運代理市場作為電商網路值得信賴的合作夥伴的地位。

托運人的成本降低策略以及向整車運輸方式的轉變

透過整合超過 15,000 磅的貨物,製造商可以避免碼頭裝卸,減少責任索賠,並縮短運輸時間,與同等零擔 (LTL) 運輸路線相比,可節省 12% 至 18% 的成本。工廠直銷是汽車和工業供應鏈的首選,有助於實現準時制庫存控制。能夠協調區域整合中心的仲介可以提升美國整車 (FTL) 貨運代理市場的流量,隨著供應鏈管理者將速度置於最低單價之上,貨運量也會隨之增加。

長期存在的司機短缺問題和勞動力老化問題

預計到2024年,非固定薪資卡車駕駛人的就業人數將下降16.3%,這將是自2009年以來最大的降幅。獨立承包商的保險和融資成本將上漲20%,迫使部分承包商退出市場。藥物和酒精檢測違規行為以及2000年以前生產的卡車可能強制安裝電子記錄設備(ELD)將進一步降低運力。雖然擁有可靠承運商網路的仲介可以提高利潤率,但整體運力空間正在萎縮,這減緩了美國整車貨運仲介市場的成長潛力。

細分市場分析

到2025年,分銷業將占美國整車貨運仲介市場佔有率的30.35%,這反映了全通路零售商、批發商和電子商務平台對全國乾貨車運輸網路的依賴。庫存多元化帶來的頻繁補貨需求支撐了該行業的穩定成長。在《基礎設施投資與就業法案》的資金支持下,建設業預計在2031年之前實現5.18%的複合年成長率,成為成長最快的行業。平板貨車仲介負責協調鋼筋、預製牆體和重型設備運送到數千個工地,並在特殊路線上賺取高額運費。在製造業和汽車產業,近岸外包促進了組裝廠和供應商園區之間的同步,持續創造跨境運輸機會。雖然石油、天然氣和礦業的運輸量會隨商品週期波動,但農業、林業和漁業的運輸量具有季節性可預測性,這使得仲介可以透過策略性地將運力分配到收穫走廊來獲利。

終端用戶組合有助於利潤多元化。消費支出放緩可透過基礎建設支出抵消,而基礎建設支出將持續到2029年預算。利用數據分析的仲介透過根據商品價格波動對托運人進行細分並動態調整定價策略,從而在週期性波動中保持盈利。與聯邦緊急事務管理署(FEMA)相關的貨運量突然增加帶來了額外的商機。這種均衡的終端用戶組合有助於美國整車貨運仲介市場的長期穩健發展。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 履約需求爆炸性成長

- 托運人的成本削減計劃以及向整車運輸 (FTL)的模式轉換

- 數位化和API驅動的貨物匹配平台

- 美國和墨西哥之間近岸外包走廊的成長

- IIJA基礎設施計劃增加平板車運輸里程

- 由於聯邦緊急事務管理局(FEMA)的救災契約,暫時性激增

- 市場限制

- 長期存在的司機短缺問題和勞動力老化問題

- 柴油價格波動對仲介的利潤率帶來壓力。

- 雙重仲介和貨物盜竊詐騙導致信貸緊縮

- 主要貨運公司將自有車輛納入公司內部內部資源

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 貨運費率趨勢分析

- 政府重大政策

- 美國主要FTL經紀公司所在地分析

- 薪資和薪資制度的發展趨勢

第5章 市場規模及成長預測(以金額為準,2019-2030 年)

- 最終用戶

- 製造業和汽車業

- 石油和天然氣、採礦和採石

- 農業、漁業、林業

- 建造

- 分銷業

- 其他最終用戶

- 透過裝置

- 乾貨車

- 冷藏(冷藏車)

- 平板車/重型貨物運輸車

- 罐車/散裝貨物

- 特殊運輸/超大貨物

- 按貨物類型

- 普通貨物

- 冷藏貨物

- 按美國地區

- 東北

- 中西部

- 南部

- 西

第6章 競爭情勢

- 市場集中度

- 策略性舉措和併購

- 市佔率分析

- 公司簡介

- CH Robinson

- JB Hunt Transport Services

- Total Quality Logistics

- Echo Global Logistics

- Landstar System

- RXO

- Schneider

- WWEX Group(Worldwide Express)

- GlobalTranz

- Arrive Logistics

- Hub Group

- Mode Global

- Armstrong Transport Group

- Nolan Transportation Group

- Trinity Logistics

- PLS Logistics Services

- Allen Lund Company

- Werner Enterprises

- Kag Logistics Inc

- Scotlynn

第7章 市場機會與未來展望

The United States FTL Freight Brokerage Market was valued at USD 16.33 billion in 2025 and estimated to grow from USD 17.59 billion in 2026 to reach USD 25.51 billion by 2031, at a CAGR of 7.72% during the forecast period (2026-2031).

The scale and trajectory underscore how rapidly shippers are migrating procurement toward digital, third-party full-truckload specialists in response to e-commerce fulfillment imperatives, nearshoring, and infrastructure spending. Platform-driven intermediaries are consolidating volumes by integrating predictive pricing, API connectivity, and automated compliance checks that shrink manual touch points and shorten settlement cycles. At the same time, concentrated buying power allows top brokers to secure capacity despite an aging driver workforce, volatile diesel prices, and tightening credit. Technology leadership, deep carrier relationships, and diversified equipment portfolios therefore emerge as decisive advantages as supply chains digitize, cross-border traffic grows, and shippers pursue cost-out strategies through load consolidation.

United States FTL Freight Brokerage Market Trends and Insights

Explosive E-commerce Fulfillment Demand

Distributed inventory strategies require granular capacity management that traditional asset-based carriers cannot meet efficiently. Brokers using AI-driven consolidation engines reduce empty miles and compress transportation cycle times by up to 35%, improving cost-to-serve for omnichannel retailers. Micro-fulfillment hubs in dense urban zones stimulate frequent, small-lot full-truckload moves that reward intermediaries capable of rapid capacity matching. Speed-to-customer remains paramount, enabling premium pricing on expedited multi-stop routes and reinforcing the US FTL freight brokerage market as a go-to partner for e-commerce networks.

Shippers' Cost-Out Agenda and Modal Shift to FTL

Manufacturers consolidating loads above 15,000 lb avoid terminal handling, lower damage claims, and cut transit times, realizing 12-18% savings versus comparable LTL routings. Automotive and industrial supply chains favor direct-to-plant deliveries to sustain just-in-time inventory disciplines. Brokers able to orchestrate regional consolidation hubs draw incremental volume as supply chain managers re-prioritize velocity over lowest unit cost, reinforcing volume flows into the US FTL freight brokerage market.

Chronic Driver Shortage and Aging Workforce

Non-payroll trucking employment shrank 16.3% in 2024, the sharpest retrenchment since 2009. Independent contractors face 20% higher insurance and financing costs, pushing some off the road. Drug and Alcohol Clearinghouse violations and potential ELD mandates on pre-2000 trucks trim further capacity. Brokers with dependable carrier pools can raise margins, yet overall volume headroom narrows, slowing expansion potential for the US FTL freight brokerage market.

Other drivers and restraints analyzed in the detailed report include:

- Digitization and API-Driven Freight-Matching Platforms

- US-Mexico Nearshoring Corridor Growth

- Diesel-Price Volatility Compressing Broker Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Distributive trade accounted for 30.35% of the US FTL freight brokerage market share in 2025, reflecting omnichannel retailers, wholesalers, and e-commerce marketplaces that depend on nationwide dry-van networks. Growth remains stable as inventory decentralization favors frequent replenishment. Construction, accelerated by Infrastructure Investment and Jobs Act funding, registers the fastest 5.18% CAGR to 2031. Flatbed brokers coordinate rebar, prefabricated walls, and heavy equipment to thousands of work sites, capturing premium rates for specialized routings. Manufacturing and automotive continue to present cross-border opportunities as nearshoring drives synchronized flows between assembly plants and supplier parks. Oil, gas, and mining volumes fluctuate with commodity cycles, while agriculture, fishing, and forestry shipments retain seasonal predictability that brokers monetize through strategic positioning of capacity in harvest corridors.

The end-user mix supports margin diversification. A slowdown in consumer spending can be offset by infrastructure outlays that extend through 2029 appropriations. Brokers leveraging data analytics segment shippers by commodity volatility and adjust pricing strategies dynamically, sustaining profitability across cycles. FEMA-related episodic volume spikes provide additional upside. The balanced portfolio across end-users therefore underpins the long-run resilience of the US FTL freight brokerage market.

The US FTL Freight Brokerage Market Report is Segmented by End-User (Manufacturing and Automotive, Oil and Gas Mining and Quarrying, Agriculture Fishing and Forestry, Construction, Distributive Trade, and More), Equipment Type (Dry-Van, Refrigerated Reefer, Flatbed Heavy-Haul, Tanker Bulk, and More), Freight Type (General Freight, Refrigerated Freight), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- C.H. Robinson

- J.B. Hunt Transport Services

- Total Quality Logistics

- Echo Global Logistics

- Landstar System

- RXO

- Schneider

- WWEX Group (Worldwide Express)

- GlobalTranz

- Arrive Logistics

- Hub Group

- Mode Global

- Armstrong Transport Group

- Nolan Transportation Group

- Trinity Logistics

- PLS Logistics Services

- Allen Lund Company

- Werner Enterprises

- Kag Logistics Inc

- Scotlynn

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive e-commerce fulfilment demand

- 4.2.2 Shippers' cost-out agenda and modal shift to FTL

- 4.2.3 Digitisation and API-driven freight-matching platforms

- 4.2.4 US-Mexico nearshoring corridor growth

- 4.2.5 IIJA infrastructure projects boosting flatbed miles

- 4.2.6 FEMA disaster-relief contracts creating episodic spikes

- 4.3 Market Restraints

- 4.3.1 Chronic driver shortage and ageing workforce

- 4.3.2 Diesel-price volatility compressing broker margins

- 4.3.3 Double-brokering and cargo-theft fraud tightening credit

- 4.3.4 Private-fleet insourcing by big shippers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Insights into Freight Rates

- 4.9 Key Government Initiatives

- 4.10 Insights on the FTL Brokerage Hotspots in the United states

- 4.11 Wage and Pay-structure Trends

5 Market Size and Growth Forecasts (Value, 2019-2030)

- 5.1 By End-User

- 5.1.1 Manufacturing And Automotive

- 5.1.2 Oil And Gas, Mining, And Quarrying

- 5.1.3 Agriculture, Fishing, And Forestry

- 5.1.4 Construction

- 5.1.5 Distributive Trade

- 5.1.6 Other End Users

- 5.2 By Equipment Type

- 5.2.1 Dry-Van

- 5.2.2 Refrigerated (Reefer)

- 5.2.3 Flatbed / Heavy-haul

- 5.2.4 Tanker / Bulk

- 5.2.5 Specialized / Over-dimension

- 5.3 By Freight Type

- 5.3.1 General Freight

- 5.3.2 Refrigerated Freight

- 5.4 By U.S. Region

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 South

- 5.4.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves and MandA

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 C.H. Robinson

- 6.4.2 J.B. Hunt Transport Services

- 6.4.3 Total Quality Logistics

- 6.4.4 Echo Global Logistics

- 6.4.5 Landstar System

- 6.4.6 RXO

- 6.4.7 Schneider

- 6.4.8 WWEX Group (Worldwide Express)

- 6.4.9 GlobalTranz

- 6.4.10 Arrive Logistics

- 6.4.11 Hub Group

- 6.4.12 Mode Global

- 6.4.13 Armstrong Transport Group

- 6.4.14 Nolan Transportation Group

- 6.4.15 Trinity Logistics

- 6.4.16 PLS Logistics Services

- 6.4.17 Allen Lund Company

- 6.4.18 Werner Enterprises

- 6.4.19 Kag Logistics Inc

- 6.4.20 Scotlynn

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026年全球仲介業者轉運板市場報告

2026年全球仲介業者轉運板市場報告 歐洲貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)法國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)西班牙貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)貨運代理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)東協貨運代理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)北美貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

歐洲貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)法國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)西班牙貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)貨運代理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)東協貨運代理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)北美貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 貨運代理服務市場:依服務類型、運輸方式、客戶規模、貨物類型、技術應用及最終用戶產業分類-2026-2032年全球市場預測

貨運代理服務市場:依服務類型、運輸方式、客戶規模、貨物類型、技術應用及最終用戶產業分類-2026-2032年全球市場預測 全球貨運仲介市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球貨運仲介市場規模、佔有率、趨勢和成長分析報告(2026-2034)