|

市場調查報告書

商品編碼

2063308

法國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)France Freight Brokerage Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

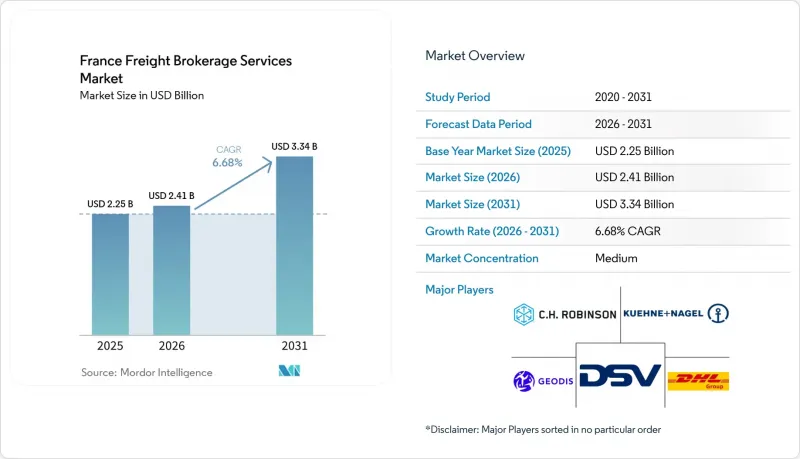

根據 Mordor Intelligence 預測,法國貨運代理服務市場規模將從 2025 年的 22.5 億美元成長到 2026 年的 24.1 億美元,到 2031 年將達到 33.4 億美元,2026 年至 2031 年的複合年預計成長率為 6.68%。

本報告按服務類型(整車運輸、零擔運輸)、車輛類型(乾貨車、冷藏車等)、運輸距離(長途、本地、近距離)、商業模式(傳統模式、資產持有模式等)、最終用戶(製造業/汽車業、建築業等)和客戶規模(大型企業、中型企業、中小企業)進行分類。市場預測以美元計價。

法國貨運代理服務市場的趨勢與洞察

基於 CSRD 的強制性供應鏈視覺性將促進仲介的採用。

法國《違規碳排放揭露指令》(CSRD)要求約5萬家公司自2025年1月起揭露範圍3的運輸排放,迫使托運人與提供符合ISO 14083標準的碳資料和即時追蹤服務的供應商合作。不合規將面臨罰款,且平均每年報告成本高達120萬歐元(約142萬美元),這促使企業將報告外包給擁有自動化儀錶板的仲介。法國跨國公司如今已將環境報告列為三大採購標準之一,隨著仲介將複雜的審計法規轉化為更易於托運人使用的介面,法國貨運仲介服務市場正在不斷擴張。該指令的域外適用意味著歐盟以外的供應商也需遵守類似的報告要求,從而擴大了對跨境仲介服務的需求。早期採用者正透過基於區塊鏈的排放計算證明以及與企業資源計劃(ERP)系統的API整合來脫穎而出。

城市集散中心的擴張促進了越庫作業中介服務。

到2026年,巴黎將建成15個微型樞紐,里昂將建成8個微型樞紐,為零排放配送區提供服務,使仲介能夠整合來自多個托運人的托盤貨物,並將卡車裝載率提高到80-85%。由於市政法規已禁止超過3.5噸的歐5柴油車輛駛入主要城市中心,仲介對增值越庫作業和限時配送服務收取額外費用。此外,集貨中心透過縮短配送路線和減少30-40%的最後一公里配送時間,也為電子商務的當日送達承諾提供了支持。歐洲投資銀行和地方政府的公共津貼降低了私人樞紐投資的風險,並進一步促進了都市區零擔(大對大)貨運代理業務的成長。

反壟斷機構對仲介費用透明度的審查正在推高合規成本。

歐盟競爭主管機關正在調查現貨貨運中高達12%至25%的隱性利潤,並要求仲介將支付給承運人的款項與服務費分開。法國競爭主管機關目前強制要求提供詳細發票,這迫使企業進行IT系統升級、法律審查和客戶再培訓,所有這些都給中型企業的息稅折舊攤銷前利潤(EBITDA)帶來了壓力。最高可達銷售額10%的罰款增加了風險,並減緩了法國貨運仲介服務市場的地理擴張和技術投資。

細分市場分析

預計到2031年,法國貨運代理服務市場的收入將以8.06%的複合年成長率成長,零擔貨運(LTL)的佔有率正在不斷擴大。同時,到2025年,整車貨運(FTL)仍將佔據57.53%的市場。巴黎和里昂的集散中心提高了零擔貨車的運轉率,並支持了當日送達的承諾,這吸引了許多電商企業。相較之下,整車貨運雖然提供了從工廠到倉庫的穩定運輸路線,但卻面臨司機短缺和保險成本上漲的壓力。

人工智慧驅動的貨物共乘技術已將零擔貨運匹配時間縮短至3小時,提高了準時交貨率。整車幹線運輸與零擔都市區運輸相結合的混合解決方案模糊了運輸環節的界限,使仲介提升銷售配套服務。針對危險物品和超大貨物的專業服務在建設業和化學工業的需求支撐下,保持小眾但穩定的市場地位。

乾貨車運輸佔法國貨運代理服務市場的40.68%,但隨著疫苗和生技藥品運輸量的增加,冷藏貨櫃的市場佔有率正以8.68%的複合年成長率快速成長。第一季防疫宣傳活動期間,溫控運輸能力的短缺使得仲介能夠收取15%至20%的附加費,推動了法國貨運代理服務市場的發展。安裝在拖車上的物聯網感測器能夠偵測壓縮機故障,防止貨物變質,並提升承運商的服務水準。

由於藥品良好儲存規範 (GDP) 的合規性和端到端序列化要求,對可視性的需求日益成長,促使貨運仲介投資區塊鏈日誌以檢驗溫度控制的完整性。平板車和油罐車在建築和化學品運輸的支持下保持著穩定的市場佔有率,但由於其易受經濟週期影響,因此其成長速度落後於整體市場成長速度。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基於 CSRD 的強制性供應鏈視覺性正在加速仲介的採用。

- 都市區收貨點的擴張促進了越庫作業仲介業務的發展。

- 氫燃料卡車補貼計畫(「H2 Mobility France」)擴大了綠色能源來源。

- 英國脫歐後實施的數位化海關程序促進了英吉利海峽貿易量的成長。

- 人工智慧驅動的動態定價引擎提高了負載匹配的效率。

- 循環經濟中的逆向物流流程正在創造高盈利的返程運輸路線。

- 市場限制因素

- 對仲介費用透明度的反壟斷審查增加了合規成本。

- 鐵路和電動卡車用電價格的波動正在削弱多模態的成本競爭力。

- 針對貨運平台的網路攻擊日益加劇,正在削弱托運人的信心。

- 運輸公司保險費的急劇上漲給獨立運輸公司的運輸能力帶來了壓力。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按服務

- 全軌道公路(FTL)

- 低於100%的運費(零擔運輸)

- 其他

- 按設備類型/按拖車類型

- 乾燒

- 冷藏車

- 平板/階梯式平板車

- 油輪(散裝液體/化學品)

- 其他

- 按運輸距離

- 長途運輸(超過 500 英里)

- 按地區(100-500英里)

- 近距離(不到100英里)

- 按經營模式

- 傳統貨運代理

- 資產持有型貨運經紀

- 代理貨運經紀

- 數位貨運代理

- 按最終用戶行業分類

- 製造業/汽車

- 建築和基礎設施項目

- 石油、天然氣、採礦和化工

- 農業/食品/飲料

- 零售、快速消費品和批發分銷

- 醫療和藥品

- 電子商務與第三方物流履約

- 其他終端用戶產業

- 按客戶規模

- 大型企業貨運商(年營業額超過1億美元)

- 中型貨運公司(年營業額1000萬美元至1億美元)

- 中小企業(營業額低於1000萬美元)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- DSV

- Geodis

- CH Robinson

- Kuehne+Nagel

- Sennder

- Upply

- FM Logistic

- Clicktrans

- Emo Trans

- Carmovia

- Alpega Teleroute

- Groupe CAT

- Transporeon

- B2PWeb

- Cocolis

- Fretlink

- Chronotruck

- FretBay

- Waygoo

第7章 市場機會與未來展望

According to Mordor Intelligence, the france freight brokerage services market size is expected to increase from USD 2.25 billion in 2025 to USD 2.41 billion in 2026 and reach USD 3.34 billion by 2031, growing at a CAGR of 6.68% over 2026-2031.

This report is Segmented by Service (FTL, LTL), by Equipment (Dry Van, Refrigerated Van, and More), by Haul Length (Long-Haul, Regional, Local), by Business (Traditional, Asset-Based, and More), by End-User (Manufacturing/Automotive, Construction, and More), and by Customer Size (Large Enterprise, Mid-Market, Small Business). The Market Forecasts are Provided in Terms of Value (USD).

France Freight Brokerage Services Market Trends and Insights

Supply-Chain-Visibility Mandates Under CSRD Drive Broker Adoption

CSRD obliges around 50,000 companies to disclose Scope 3 transport emissions from January 2025, pushing shippers to partner with providers that deliver ISO 14083-aligned carbon data and real-time tracking. Compliance penalties and average annual reporting costs of EUR 1.2 million (USD 1.42 million) encourage outsourcing to brokers with automated dashboards. French multinationals now rank environmental reporting among their three top procurement criteria, expanding the France freight brokerage services market as brokers translate complex audit rules into simple shipper interfaces. The directive's extraterritorial reach draws non-EU suppliers into the same reporting net, enlarging cross-border brokerage demand. Early adopters differentiate through blockchain proofs of emission calculations and API connectivity with enterprise resource planning systems.

Expansion of Urban Consolidation Hubs Boosts Cross-Docking Brokerage

Fifteen micro-hubs in Paris and eight in Lyon feed zero-emission delivery zones by 2026, letting brokers aggregate palletized loads from multiple shippers and raise truck fill rates to 80-85%. Municipal rules already bar Euro 5 diesel above 3.5 tons from key downtown districts, so brokers charge premiums for value-added cross-docking and time-window services. Consolidation centers also shorten courier routes, lowering last-mile travel time by 30-40% and supporting same-day e-commerce commitments. Public grants from the European Investment Bank and local authorities de-risk private hub investment, further lifting urban LTL brokerage volumes.

Antitrust Scrutiny on Broker Fee Transparency Raises Compliance Costs

EU competition authorities probe hidden margins of 12-25% on spot loads, pressing brokers to unbundle carrier pay from service fees. The French Competition Authority now requires itemized invoices, forcing IT upgrades, legal reviews, and customer re-education that together trim EBITDA for mid-sized firms. Potential fines of up to 10% of revenue heighten risk, slowing geographic expansion and technology spending in the France freight brokerage services market.

Other drivers and restraints analyzed in the detailed report include:

- Hydrogen-Truck Subsidy Scheme Enlarges Green Capacity Pools

- Post-Brexit Digital Customs Clearance Stimulates Cross-Channel Brokerage Volumes

- Volatile Rail and EV-Truck Electricity Prices Erode Multimodal Cost Parity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Less-than-truckload accounted for a rising slice of the France freight brokerage services market size as its revenue grows at 8.06% CAGR to 2031, while full-truckload still commands 57.53% share in 2025. Consolidation hubs inside Paris and Lyon lift LTL truck utilization and support same-day delivery promises that attract e-commerce merchants. In contrast, FTL serves steady factory-to-warehouse corridors but is pressured by driver shortages and higher insurance.

Improved load pooling through AI cuts LTL pairing time to three hours, enhancing on-time performance. Hybrid solutions that stitch an FTL trunk with LTL urban legs blur segment lines, enabling brokers to upsell bundled services. Specialized offerings for hazardous and oversized cargo remain niche but stable, anchored by construction and chemical demand.

Dry vans delivered 40.68% of the France freight brokerage services market size, yet refrigerated units expand at 8.68% CAGR as vaccine and biologic volumes climb. Temperature-controlled capacity shortages during Q1 health campaigns allowed brokers to charge 15-20% premiums, boosting the France freight brokerage services market. IoT probes in trailers now alert on compressor faults, cutting spoilage and raising carrier service levels.

GDP compliance and end-to-end serialization for medicines intensify demand for visibility, prompting brokers to invest in blockchain logs that verify temperature integrity. Flatbeds and tankers keep a steady share tied to construction and chemical shipments, while their growth lags the headline market due to cyclical exposure.

List of Companies Covered in this Report:

- DHL Group

- DSV

- Geodis

- C.H Robinson

- Kuehne + Nagel

- Sennder

- Upply

- FM Logistic

- Clicktrans

- Emo Trans

- Carmovia

- Alpega Teleroute

- Groupe CAT

- Transporeon

- B2PWeb

- Cocolis

- Fretlink

- Chronotruck

- FretBay

- Waygoo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Supply-chain-visibility mandates under CSRD drive broker adoption

- 4.2.2 Expansion of urban consolidation hubs boosts cross-docking brokerage

- 4.2.3 Hydrogen-truck subsidy scheme ("H2 Mobility France") enlarges green capacity pools

- 4.2.4 Post-Brexit digital customs clearance stimulates cross-Channel brokerage volumes

- 4.2.5 AI-enabled dynamic-pricing engines improve load-matching efficiency

- 4.2.6 Circular-economy reverse-logistics flows create profitable backhaul lanes

- 4.3 Market Restraints

- 4.3.1 Antitrust scrutiny on broker fee transparency raises compliance costs

- 4.3.2 Volatile rail & EV-truck electricity prices erode multimodal cost parity

- 4.3.3 Escalating cyber-attacks on freight platforms dampen shipper trust

- 4.3.4 Spike in carrier insurance premiums tightens independent-haulage capacity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service

- 5.1.1 Full-Truckload (FTL)

- 5.1.2 Less-than-Truckload (LTL)

- 5.1.3 Others

- 5.2 By Equipment / Trailer Type

- 5.2.1 Dry Van

- 5.2.2 Refrigerated Van

- 5.2.3 Flatbed / Step-Deck

- 5.2.4 Tanker (Bulk Liquid & Chemical)

- 5.2.5 Others

- 5.3 By Haul Length

- 5.3.1 Long-Haul (More than 500 miles)

- 5.3.2 Regional (100-500 miles)

- 5.3.3 Local (Less than 100 miles)

- 5.4 By Business Model

- 5.4.1 Traditional Freight Brokerage

- 5.4.2 Asset-Based Freight Brokerage

- 5.4.3 Agent Model Freight Brokerage

- 5.4.4 Digital Freight Brokerage

- 5.5 By End-User Industry

- 5.5.1 Manufacturing & Automotive

- 5.5.2 Construction & Infrastructure Projects

- 5.5.3 Oil, Gas, Mining & Chemicals

- 5.5.4 Agriculture & Food / Beverage

- 5.5.5 Retail, FMCG & Wholesale Distribution

- 5.5.6 Healthcare & Pharmaceuticals

- 5.5.7 E-commerce & 3PL Fulfilment

- 5.5.8 Other End-User Industry

- 5.6 By Customer Size

- 5.6.1 Large Enterprise Shippers (More than USD 100 M)

- 5.6.2 Mid-Market Shippers (USD 10-100 M)

- 5.6.3 Small Businesses (Less than USD 10 M)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 DHL Group

- 6.4.2 DSV

- 6.4.3 Geodis

- 6.4.4 C.H Robinson

- 6.4.5 Kuehne + Nagel

- 6.4.6 Sennder

- 6.4.7 Upply

- 6.4.8 FM Logistic

- 6.4.9 Clicktrans

- 6.4.10 Emo Trans

- 6.4.11 Carmovia

- 6.4.12 Alpega Teleroute

- 6.4.13 Groupe CAT

- 6.4.14 Transporeon

- 6.4.15 B2PWeb

- 6.4.16 Cocolis

- 6.4.17 Fretlink

- 6.4.18 Chronotruck

- 6.4.19 FretBay

- 6.4.20 Waygoo

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年全球仲介業者轉運板市場報告

2026年全球仲介業者轉運板市場報告 歐洲貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)西班牙貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)貨運代理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)東協貨運代理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)北美貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

歐洲貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)西班牙貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)貨運代理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)東協貨運代理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)北美貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 貨運代理服務市場:依服務類型、運輸方式、客戶規模、貨物類型、技術應用及最終用戶產業分類-2026-2032年全球市場預測美國整車貨運經紀市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

貨運代理服務市場:依服務類型、運輸方式、客戶規模、貨物類型、技術應用及最終用戶產業分類-2026-2032年全球市場預測美國整車貨運經紀市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 全球貨運仲介市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球貨運仲介市場規模、佔有率、趨勢和成長分析報告(2026-2034)