|

市場調查報告書

商品編碼

2063309

西班牙貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Spain Freight Brokerage Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

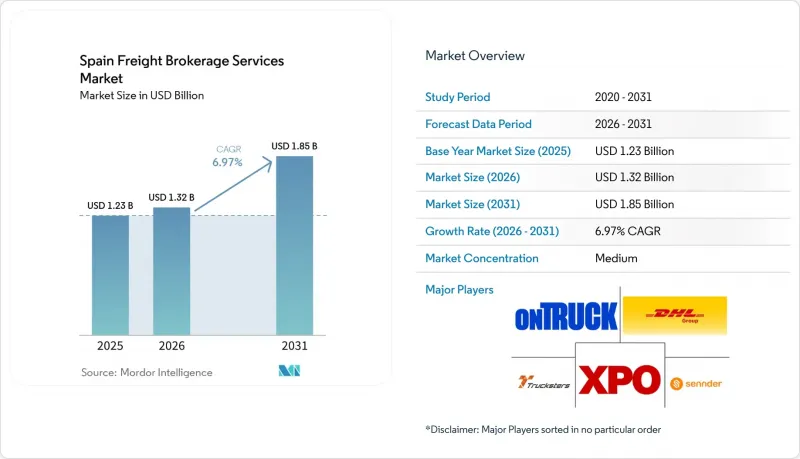

據 Mordor Intelligence 稱,西班牙貨運代理服務市場在 2025 年的價值為 12.3 億美元,預計到 2031 年將從 2026 年的 13.2 億美元成長到 18.5 億美元,在預測期(2026-2031 年)內的複合成長率為 6.97%。

電子文件的強制實施、自動化倉庫的普及以及沿海路線的擴張正在重塑競爭格局,採用API工作流程和即時運力匹配的仲介正獲得優勢。本報告按服務類型(整車運輸、小包裹運輸及其他)、車輛/拖車類型(乾貨車、冷藏車及其他)、運輸距離(長途、區域、近距離)、經營模式(傳統模式及其他)、終端用戶行業(製造業及其他)和客戶規模(大型企業及其他)進行細分。市場預測以美元計價。

西班牙貨運代理服務市場的趨勢與洞察

倉儲自動化領域的競爭正在加速西班牙對當日送達服務的需求。

自動化倉庫系統將貨物停留時間從數天縮短至數小時,迫使托運人必須在30時限內安排運輸車輛。數位仲介透過API取得倉庫管理訊號並即時安排承運商,從而從這種速度中獲利。機器人技術的部署主要集中在薩拉戈薩的PLAZA樞紐和巴塞隆納的自由貿易區,即使是超過300公斤的貨物也能實現當日送達,以實現盈利。隨著托運人轉向提供電子交貨證明和自動計費的平台,傳統客服中心仲介的市佔率正在下降。當天送達的需求正在零售、製藥和高科技產業蔓延,推動了指定時間送達路線訂單的兩位數成長。

強制性電子貨物單證將加速平台的普及應用。

西班牙的「Ley Crea y Crece」法案強制要求企業間交易使用電子帳單,歐盟的eCMR框架則實現了跨境運輸貨運標籤的數位化。平台仲介正在將這兩項要求整合到各自的系統中,使托運人能夠在運輸管理系統(TMS)內自動產生合規單據。在法國和葡萄牙的航線上,超過40%的承運商貨運已開始實施數位化,但在純國內航線上,這一比例僅15%。合規的便利性正促使中型出口商轉向數位化供應商,其採用率每年都維持著三位數的成長。而紙本業者則面臨整合成本,這會擠壓利潤空間並延長結算週期,進而進一步擴大績效差距。

NIS-2 網路安全法規正在推高數位仲介的營運成本。

到2024年10月,被列為關鍵型數位貨運平台的平台將被要求在24小時內提交違規報告,並接受年度審計。不遵守規定者將面臨最高1000萬歐元(1170萬美元)的罰款。中型仲介每年需要撥出20萬至50萬歐元(23508至58770美元)用於安全營運中心(SOC)工具、穿透測試和員工培訓。這些支出正在加速產業重組,小規模的參與企業正將其業務組合出售給資金較雄厚的競爭對手。傳統的電話貨運公司目前仍不受此指令的約束,但它們正在流失那些要求全面數位化視覺性的客戶。因此,合規負擔在重塑市場的同時,也減緩了整體成長。

細分市場分析

2025年,整車運輸(FTL)將主導西班牙貨運代理服務市場,佔63.29%的市場。這是因為大規模出口商仍傾向選擇能夠簡化跨境流程的點對點直達運輸。同時,零擔運輸(LTL)的貨運量正以8.76%的複合年成長率成長,這得益於倉儲自動化和全通路零售將訂單拆分成小於托盤尺寸的貨物。數位化路線規劃引擎正在降低單次停靠成本,從而在馬德里-巴塞隆納和瓦倫西亞等交通繁忙的路線上實現多點配送。

零擔貨運 (LTL) 服務的快速發展正在使西班牙的貨運市場多元化。能夠將零散貨物組裝成整車的仲介業者提高了每英里的收入,同時也為托運人提供了更節能的運輸選擇。同時,整車貨運 (FTL)仲介業者推出混合服務模糊了傳統貨運細分市場的界限,這些服務既能確保基礎車廂的可用性,又能透過現貨交付將閒置的裝載空間變現。

到2025年,冷藏車將佔西班牙貨運代理服務市場的48.39%,預計年複合成長率將達到9.60%,主要得益於西班牙水果、蔬菜和疫苗出口對溫度控制的嚴格要求。 2025年推出的電動自充電式冷藏車,由於減少了柴油發電機的使用,並使其能夠進入都市區低排放氣體區,因此吸引了來自製藥公司和食品供應鏈的高價值貨物運輸。乾貨車是運輸日常消費品的必需品,但成長速度較慢。同時,罐車和平板車的需求會隨著化學產品和建築材料的生產趨勢而波動。

在西班牙貨運代理服務市場,低溫運輸運輸路線的價格彈性最低,這使得仲介業者能夠在不損失市場佔有率的情況下轉嫁燃油額外費用。透過增加溫度偏差分析能力,管理具有保值儲存等級(GDP)路線的貨運代理商正在與生命科學領域的客戶建立牢固的合作關係。為了應對農產品季節性波動,仲介業者正在重新分配冷藏集裝箱,用於運輸冷凍水產品和糖果甜點,從而全年保持資產利用率的平衡。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 倉儲自動化領域的競爭正在擴大西班牙境內對當日送達服務的需求。

- 強制性電子貨物單據(ECMR 和“Ley Crea Y Crece”電子帳單)正在加速該平台的普及。

- ETS-2 對道路運輸的碳定價正在推動對貨物聚合演算法的需求。

- 西班牙與馬格里布之間沿海路線的成長,為首末一公里運輸經紀業務創造了新的成長機會。

- 氫能走廊(地中海氫能走廊和西班牙氫能山谷)正在促進早期綠色通道經紀產品的開發。

- 利用人工智慧技術,透過公私合營物流資料空間實現即時、多模態預訂API。

- 市場限制因素

- NIS-2網路安全合規性正在推高數位仲介的營運成本。

- 關於2026-2027年全國道路使用者收費的討論,為收費標準的製定帶來了不確定性。

- 現貨貨運量減少,分為 OEM 專用物流及零售商內部資源。

- 伊比利半島各港口設施不平衡的狀況依然存在,阻礙了回程傳輸。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按服務

- 全軌道公路(FTL)

- 低於100%的運費(零擔運輸)

- 其他

- 車輛/拖車類型

- 乾燒

- 冷藏車

- 平板/階梯式平板車

- 油輪(散裝液體和化學品)

- 其他

- 按運輸距離

- 長途(500英里或以上)

- 該區域內(100-500英里)

- 近距離(100英里以內)

- 按經營模式

- 傳統的

- 資產持有類型

- 基於代理的

- 數位的

- 按最終用戶行業分類

- 製造業/汽車

- 基礎建設項目

- 石油、天然氣、採礦和化工

- 農業/食品/飲料

- 零售、快速消費品和批發分銷

- 醫療和藥品

- 電子商務與第三方物流履約

- 其他

- 按客戶規模

- 大型企業(年營業額超過1億美元)

- 中型企業(年營業額1000萬美元至1億美元)

- 中小企業(營業額低於1000萬美元)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Ontruck

- Trucksters

- Sennder

- DHL Group

- XPO Inc.

- Kuehne+Nagel

- DSV A/S

- Clicktrans

- Emo Trans

- Carmovia

- Logista Freight

- Arola Logistics

- Noatum Logistics

- GEODIS

- Rhenus Logistics

- Cargobot

- NYK航運公司(含郵船物流)

- Scan Global Logistics

- Grupo Moldtrans

- Tennders

第7章 市場機會與未來展望

According to Mordor Intelligence, the spain freight brokerage services market size was valued at USD 1.23 billion in 2025 and estimated to grow from USD 1.32 billion in 2026 to reach USD 1.85 billion by 2031, at a CAGR of 6.97% during the forecast period (2026-2031).

Digital-document mandates, automated warehouses, and expanding short-sea loops are reshaping competition, rewarding brokers that embed API-ready workflows and real-time capacity matching. This report is Segmented by Service (Full-Truckload, Less-Than-Truckload, Others), by Equipment/Trailer Type (Dry Van, Refrigerated Van, and More), by Haul Length (Long-Haul, Regional, Local), by Business Model (Traditional, and More), by End-User Industry (Manufacturing and More), and by Customer Size (Large Enterprise, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Freight Brokerage Services Market Trends and Insights

Warehouse-Automation Race Amplifying Intra-Spain Same-Day Freight Needs

Automated storage and retrieval systems now shrink dwell time from days to hours, forcing shippers to secure outbound trucks inside 30-minute windows. Digital brokers that ingest warehouse-management signals via API and dispatch carriers in real time monetize this velocity premium. Zaragoza's PLAZA hub and Barcelona's Zona Franca concentrate robotics deployments, enabling profitable same-day moves for loads above 300 kg. Traditional call-center brokers lose share as shippers pivot toward platforms offering electronic proof-of-delivery and auto-billing. Same-day expectations ripple across retail, pharma, and high-tech verticals, driving double-digit order growth for time-definite lanes.

Mandatory E-Freight Documents Accelerating Platform Uptake

Spain's "Ley Crea y Crece" enforces e-invoices in B2B trade, and the EU eCMR framework digitizes consignment notes for cross-border trips. Platform brokers hard-wire both requirements, letting shippers auto-generate compliant paperwork inside their TMS. Adoption already tops 40% of carrier trips on France and Portugal corridors, versus 15% on purely domestic lanes. Compliance convenience is tipping mid-market exporters toward digital vendors, boosting onboarding rates by triple digits year over year. Paper-based operators face integration costs that erode margins and delay invoice cycles, widening the performance gap.

NIS-2 Cybersecurity Compliance Raising Operating Costs for Digital Brokers

By October 2024, digital freight platforms classified as essential will file 24-hour breach reports and undergo yearly audits or risk fines of up to EUR 10 million (USD 11.7 million). Mid-size brokers must allocate EUR 200,000-500,000 (USD 23,508-58,770) annually for SOC tools, penetration testing, and staff training. These outlays accelerate consolidation as smaller entrants sell portfolios to capital-rich rivals. Traditional phone-based firms stay outside the directive's scope yet lose customers seeking full digital visibility. The compliance burden, therefore, reshapes market structure even while slowing overall growth.

Other drivers and restraints analyzed in the detailed report include:

- EU Green-Logistics and Digital-Corridor Funding

- Growth of Spain-Maghreb Short-Sea Loops Creating First/Last-Mile Brokerage Opportunities

- Pending 2026-2027 National Road-User Charge Debate Creating Tariff Uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full-truckload shipments dominated with 63.29% of the Spain freight brokerage services market share in 2025, as large exporters still prefer direct point-to-point moves that simplify border transit. At the same time, less-than-truckload volumes are growing at an 8.76% CAGR because warehouse automation and omnichannel retail break orders into sub-pallet consignments. Digital route-building engines lower per-stop costs, making multi-drop tours viable on dense Madrid-Barcelona-Valencia lanes.

Rapid LTL uptake is diversifying the Spain freight brokerage services market. Brokers able to merge partial loads into full trailers capture higher revenue per mile while offering shippers carbon-efficient options. FTL brokers respond by launching hybrid services that guarantee a base trailer but monetize unused floor space through spot inserts, blurring traditional segment boundaries.

Refrigerated vans held 48.39% of the Spain freight brokerage services market size in 2025, and will expand at a 9.60% CAGR as Spain's fruit, veg, and vaccine exports require tight temperature control. Electric self-charging reefers introduced in 2025 cut diesel genset use and unlock urban low-emission zones, attracting premium payloads from pharma and grocery chains. Dry-van boxes remain essential for consumer staples but grow more slowly, while tankers and flatbeds cycle with chemicals and construction output.

Within the Spain freight brokerage services market size, cold-chain lanes exhibit the lowest price elasticity, letting brokers pass on fuel surcharges without losing share. Those managing validated GDP lanes add analytics on temperature excursions, creating stickiness with life-science customers. As produce seasonality shifts, brokers redeploy reefers into frozen seafood and confectionery, smoothing asset utilization year-round.

List of Companies Covered in this Report:

- Ontruck

- Trucksters

- Sennder

- DHL Group

- XPO Inc.

- Kuehne+Nagel

- DSV A/S

- Clicktrans

- Emo Trans

- Carmovia

- Logista Freight

- Arola Logistics

- Noatum Logistics

- GEODIS

- Rhenus Logistics

- Cargobot

- NYK Line (Including Yusen Logistics)

- Scan Global Logistics

- Grupo Moldtrans

- Tennders

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Warehouse-Automation Race Amplifying Intra-Spain Same-Day Freight Needs

- 4.2.2 Mandatory E-Freight Documents (Ecmr and "Ley Crea Y Crece" E-Invoice) Accelerating Platform Uptake

- 4.2.3 ETS-2 Carbon Pricing on Road Transport Boosting Demand for Load-Consolidation Algorithms

- 4.2.4 Growth of Spain-Maghreb Short-Sea Loops Creating First/Last-Mile Brokerage Opportunities

- 4.2.5 Hydrogen Corridor (H2Med and Spanish H2-Valleys) Spurring Early Green-Lane Brokerage Products

- 4.2.6 AI-Driven Public-Private Logistics Data Space Enabling Real-Time Multimodal Booking APIs

- 4.3 Market Restraints

- 4.3.1 NIS-2 Cyber-Security Compliance Raising Operating Costs for Digital Brokers

- 4.3.2 Pending 2026-2027 National Road-User Charge Debate Creating Tariff Uncertainty

- 4.3.3 OEM-Captive Logistics and Retailer Insourcing Shrinking Accessible Spot Volumes

- 4.3.4 Persistent Equipment Imbalance at Iberian Ports Disrupting Back-Haul Availability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Service

- 5.1.1 Full-Truckload (FTL)

- 5.1.2 Less-than-Truckload (LTL)

- 5.1.3 Others

- 5.2 By Equipment / Trailer Type

- 5.2.1 Dry Van

- 5.2.2 Refrigerated Van

- 5.2.3 Flatbed / Step-Deck

- 5.2.4 Tanker (Bulk Liquid and Chemical)

- 5.2.5 Others

- 5.3 By Haul Length

- 5.3.1 Long-Haul (More than 500 miles)

- 5.3.2 Regional (100-500 miles)

- 5.3.3 Local (Less than 100 miles)

- 5.4 By Business Model

- 5.4.1 Traditional Freight Brokerage

- 5.4.2 Asset-Based Freight Brokerage

- 5.4.3 Agent Model Freight Brokerage

- 5.4.4 Digital Freight Brokerage

- 5.5 By End-User Industry

- 5.5.1 Manufacturing and Automotive

- 5.5.2 Construction and Infrastructure Projects

- 5.5.3 Oil, Gas, Mining and Chemicals

- 5.5.4 Agriculture and Food / Beverage

- 5.5.5 Retail, FMCG and Wholesale Distribution

- 5.5.6 Healthcare and Pharmaceuticals

- 5.5.7 E-commerce and 3PL Fulfilment

- 5.5.8 Others

- 5.6 By Customer Size

- 5.6.1 Large Enterprise Shippers (More than USD 100 M)

- 5.6.2 Mid-Market Shippers (USD 10-100 M)

- 5.6.3 Small Businesses (Less than USD 10 M)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Ontruck

- 6.4.2 Trucksters

- 6.4.3 Sennder

- 6.4.4 DHL Group

- 6.4.5 XPO Inc.

- 6.4.6 Kuehne+Nagel

- 6.4.7 DSV A/S

- 6.4.8 Clicktrans

- 6.4.9 Emo Trans

- 6.4.10 Carmovia

- 6.4.11 Logista Freight

- 6.4.12 Arola Logistics

- 6.4.13 Noatum Logistics

- 6.4.14 GEODIS

- 6.4.15 Rhenus Logistics

- 6.4.16 Cargobot

- 6.4.17 NYK Line (Including Yusen Logistics)

- 6.4.18 Scan Global Logistics

- 6.4.19 Grupo Moldtrans

- 6.4.20 Tennders

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

2026年全球仲介業者轉運板市場報告

2026年全球仲介業者轉運板市場報告 歐洲貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)法國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)貨運代理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)東協貨運代理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)北美貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

歐洲貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)法國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)貨運代理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)東協貨運代理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)北美貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國貨運代理服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 貨運代理服務市場:依服務類型、運輸方式、客戶規模、貨物類型、技術應用及最終用戶產業分類-2026-2032年全球市場預測美國整車貨運經紀市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

貨運代理服務市場:依服務類型、運輸方式、客戶規模、貨物類型、技術應用及最終用戶產業分類-2026-2032年全球市場預測美國整車貨運經紀市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 全球貨運仲介市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球貨運仲介市場規模、佔有率、趨勢和成長分析報告(2026-2034)