|

市場調查報告書

商品編碼

1693801

南美資料中心市場佔有率分析、產業趨勢和成長預測(2025-2030 年)South America Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

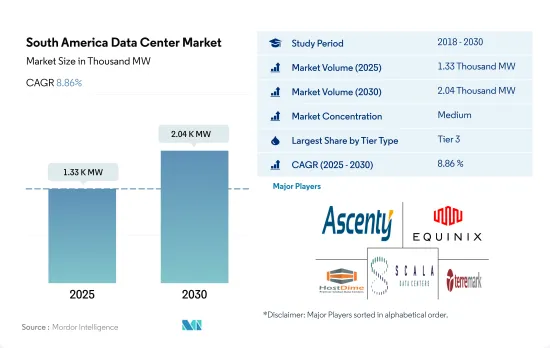

南美資料中心市場規模預計在 2025 年達到 1,330 兆瓦,預計到 2030 年將達到 2,040 兆瓦,複合年成長率為 8.86%。

預計 2025 年主機託管收益將達到 50.091 億美元,2030 年將達到 85.247 億美元,預測期內(2025-2030 年)的複合年成長率為 11.22%。

2023 年,Tier 3 資料中心將佔據大部分市場佔有率,但 Tier 4 資料中心在預測期內將快速成長

- 在南美市場,Tier 3 細分市場目前憑藉其顯著的功能優勢佔據了大部分佔有率。此層類型高度冗餘,具有多個電源和冷卻路徑。這些資料中心的運轉率約為 99.982%,每年的停機時間為 1.6 小時。隨著邊緣和雲端連接的日益普及,Tier 3 細分市場的成長預計將進一步加速。

- 巴西擁有該地區最多的 Tier 3 資料中心。 2022年,巴西的58個資料中心將獲得Tier 3認證。 2022 年,聖保羅將擁有全國最多的 Tier 3 資料中心,佔 77.9%,里約熱內盧將擁有 27.2%。其他熱點地區(塞阿拉、卡斯卡維爾、庫里蒂巴和里貝朗普雷圖等)的佔有率為 14.8%。預計 Tier 3 部分將從 2023 年的 649 兆瓦成長到 2029 年的 987.67 兆瓦,複合年成長率為 7.25%。

- 預計在預測期內,Tier 4 部分的最高複合年成長率將達到 20.94%。巴西等多個已開發國家正致力於採用 Tier 4 認證,該認證具有所有組件的完全容錯和冗餘功能。這也是發展中地區也採用 Tier 4 類型的主要原因。預計市場的主要企業將在預測期內擴大其設施,包括擁有 17 個設施的 Scala 資料中心(366 MW)和擁有 1 個設施的 ODATA(24 MW)。

- 預計一線和二線市場將在 GDP 成長較低且成本較高的低度開發國家開發中國家和發展中國家實現顯著成長。這些國家包括玻利維亞、巴拉圭、蘇利南和厄瓜多爾,其中大多數是由無法負擔三級和四級設施的中小型企業組成。

巴西佔據主要佔有率,預計在調查期間將繼續佔據主導地位

- 巴西和智利佔據南美洲資料中心市場的最大佔有率。巴西政府透過國家寬頻計畫(REPNBL)提供獎勵,其中包括購買基礎設施的獎勵。巴西的絕對投資金額較 2021 年成長了 40%,這得益於 Ascenty、Scala Data Centers 和 ODATA 等主機託管服務提供商以及 GlobeNet Telecom、Ava Telecom 和 Embratel 等通訊業者的投資。聖保羅是巴西主要的金融城市,也是資料中心的主要樞紐。里約熱內盧和福塔萊薩等其他城市也是巴西的主要投資中心。

- 智利的能源價格具有競爭力,這在很大程度上歸功於可再生能源發電潛力的計劃。能源成本已降至五年前的三分之一,這主要歸功於可再生能源目前佔總發電量的 46%。智利傳統上擁有該地區最好的通訊基礎設施之一,目前有兩個主要的光纖計劃正在進行中,以確保完全冗餘的光纖主幹網路。其中包括國營的 Fibra Optica Austral (FOA) 海底電纜,該電纜將澳洲南部與 Gtd(一條 3,500 公里的南北海底電纜)連接起來。 2022年,Scala Data Centers、ODATA、Ascenty(Digital Realty)和EdgeConneX等主機代管業者成為智利資料中心市場的主要投資者。

- 在阿根廷,布宜諾斯艾利斯是一個重要的投資地點,該市已確定的第三方設施貢獻了現有電力容量的 90% 以上。現有的資料中心大多是在有限空間內建造的小型設施。根據國際可再生能源機構(IRENA)的數據,2020年可再生能源佔阿根廷總電力供應的約33%,阿根廷的目標是到2025年可再生能源發電量佔比達到20%,並計劃在未來成為全球最大的資料中心樞紐之一。

南美洲資料中心市場的趨勢

各行各業對網際網路和智慧型手機技術的廣泛採用以及全部區域數位化使用率的不斷成長正在推動市場需求

- 2020年,行動科技和服務佔拉丁美洲地區GDP的7.1%,經濟增加值貢獻超過3,400億美元。行動生態系統也支持超過 160 萬個就業機會(直接和間接)。到 2025 年,隨著拉丁美洲各國擴大受益於行動服務日益普及所帶來的生產力和效率的提高,拉丁美洲行動生態系統的經濟貢獻預計將成長到 300 億美元以上。

- 巴西的數位應用正在迅速成長。各公司對網路和智慧型手機的廣泛使用影響了消費者的行為。日本越來越多的人能夠購買智慧型手機,導致智慧型手機用戶數量增加。 2020年5月,拉丁美洲下載的購物應用程式大部分來自巴西,巴西以約4,400萬次下載量位居榜首。

- 智利的電子商務正在穩步擴張。 2020年智利每位付費用戶平均年收入達913美元,智利消費者的跨國電商購買量達69%。這導致了大量數據的產生,增加了全國對資料中心的需求。受新網路持續推出、設備生態系統不斷擴大以及針對消費者和企業的新應用開發的推動,南美洲正在快速向 5G 轉型。

由於銀行、商業和通訊服務對網際網路的依賴性不斷增強,該地區的 FTTH用戶正在增加,從而推動了市場成長。

- 在拉丁美洲和加勒比地區,只有不到 50% 的人口可以使用固定寬頻網際網路,只有 9.9% 的人口可以使用光纖網際網路。許多農村地區由於網路設備價格昂貴,網路覆蓋不完善。智利在固定寬頻領域為其他國家樹立了標準。智利擁有拉丁美洲最快的數據下載速度。智利的平均網路下載速度為 219Mbps,遠遠領先該地區最大的經濟體巴西,巴西的平均網路下載速度為 95.95Mbps。

- 在新冠疫情期間,巴西人越來越依賴網路進行銀行業務、商業、通訊和休閒。然而,截至2021年4月,巴西固定通訊速度全球排名第49位,通訊速度排名第74位。這意味著網路存取和寬頻速度正在快速成長,這意味著資料中心將受益於更快的資料傳輸、更高的儲存率和更低的延遲。

- 預計到 2022 年拉丁美洲光纖到府 (FTTH) 市場將擁有約 1.05 億個光纖連接家庭,比 2021 年底成長 36%,即新增 2,800 萬個光纖連接家庭。目前拉丁美洲的光纖普及率已接近61%。在投資方面,智利行動電話營運商 WOM 已與數位支援和收益管理軟體公司 Aleppo 合作,計劃於 2021 年進軍固定寬頻 (FTTH) 市場。

南美洲資料中心產業概況

南美洲資料中心市場適度整合,前五大公司佔50.76%的市場。該市場的主要企業包括 Ascenty(Digital Realty Trust Inc.)、Equinix Inc.、HostDime Global Corp.、Scala Data Centers 和 Terremark(Verizon)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 市場展望

- 負載能力

- 占地面積

- 主機代管收入

- 安裝機架數量

- 機架空間利用率

- 海底電纜

第5章 產業主要趨勢

- 智慧型手機用戶數量

- 每部智慧型手機的數據流量

- 行動數據速度

- 寬頻數據速度

- 光纖連接網路

- 法律規範

- 巴西

- 智利

- 價值鍊和通路分析

第6章市場區隔

- 資料中心規模

- 大規模

- 超大規模

- 中等規模

- 超大規模

- 小規模

- 等級類型

- 1級和2級

- 第 3 層

- 第 4 層

- 吸收量

- 未使用

- 使用

- 按主機託管類型

- 超大規模

- 零售

- 批發的

- 按最終用戶

- BFSI

- 雲

- 電子商務

- 政府

- 製造業

- 媒體與娛樂

- 電信

- 其他

- 國家

- 巴西

- 智利

- 南美洲其他地區

第7章競爭格局

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Ascenty(Digital Realty Trust Inc.)

- EdgeUno Inc.

- Equinix Inc.

- GTD Grupo Teleductos SA

- HostDime Global Corp.

- Lumen Technologies Inc.

- NABIAX

- ODATA(Patria Investments Ltd)

- Quantico Data Center

- Scala Data Centers

- SONDA SA

- Terremark(Verizon)

第8章:CEO面臨的關鍵策略問題

第9章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 全球市場規模和DRO

- 資訊來源及延伸閱讀

- 圖表清單

- 關鍵見解

- 數據包

- 詞彙表

The South America Data Center Market size is estimated at 1.33 thousand MW in 2025, and is expected to reach 2.04 thousand MW by 2030, growing at a CAGR of 8.86%. Further, the market is expected to generate colocation revenue of USD 5,009.1 Million in 2025 and is projected to reach USD 8,524.7 Million by 2030, growing at a CAGR of 11.22% during the forecast period (2025-2030).

Tier 3 data centers accounts for majority market share in 2023, Tier-4 is the fastest growing in forecasted period

- The Tier 3 segment currently has a majority share in the South American market due to the major advantage of its features. This tier type has a high redundancy level and multiple paths for power and cooling. These data centers have an uptime of around 99.982%, translating into a downtime of 1.6 hours per year. With the increasing adoption of edge and cloud connectivity, the growth in the Tier 3 segment is expected to increase further.

- Brazil hosts the maximum number of Tier 3 data centers in the region. In 2022, 58 data centers in Brazil had Tier 3 certification. In 2022, Sao Paulo hosted the maximum number of Tier 3 data centers in the country, with a market share of 77.9% and Rio de Janeiro with 27.2%. Among other hotspots (Ceara, Cascavel, Curitiba, Ribeirao Preto, and others), the share was 14.8%. The Tier 3 segment is expected to grow from 649 MW in 2023 to 987.67 MW in 2029, at a projected CAGR of 7.25%.

- The Tier 4 segment is expected to record the highest CAGR of 20.94% during the forecast period. Various developed countries, such as Brazil, are focusing on adopting the Tier 4 certification to be completely fault-tolerant and redundant for every component. This is the major reason why even the developing regions are adopting the Tier 4 type. Major players in the market are expected to expand their facilities, which include Scala Data Centers (366 MW) with 17 facilities and ODATA (24 MW) with one facility during the forecast period.

- The Tier 1 & 2 segment is expected to showcase significant growth in developing countries, with a low GDP rate index in under-developed countries with a high expense burden. These countries include Bolivia, Paraguay, Suriname, and Ecuador, which have the majority of SMEs that cannot afford Tier 3 and 4 facilities.

Brazil holds the major share and expected to continue the dominance during the study period

- Brazil and Chile hold the largest shares in the South American data center market. The Brazilian government provides incentives through the Regime Especial de Tributacao do Programa Nacional de Banda Larga (REPNBL) program, which includes incentives for purchasing infrastructure that help improve colocation services in the country. Brazil has witnessed an absolute growth of 40% in investments from the 2021 values due to investments from colocation providers such as Ascenty, Scala Data Centers, and ODATA and telecom operators such as GlobeNet Telecom, Ava Telecom, and Embratel. Sao Paulo, Brazil's significant financial capital, serves as the primary data center hub. Other cities, such as Rio de Janeiro and Fortaleza, are major investment locations in Brazil.

- Chile has competitive energy prices, primarily fueled by plans to take advantage of its natural renewable energy generation potential over the coming years. Energy costs have dropped to one-third of what they were five years ago, mainly based on renewable energy that now makes up 46% of the total produced. Chile traditionally has some of the region's best telecommunications infrastructure, and two major fiber projects are underway to ensure it will have a fully redundant fiber backbone. These include the state-funded Fibra Optica Austral (FOA) submarine cable connecting the deep south and Gtd's 3,500 km north-south submarine cable. In 2022, colocation operators, such as Scala Data Centers, ODATA, Ascenty (Digital Realty), and EdgeConneX, were the major investors in the Chilean data center market.

- In Argentina, Buenos Aires is the major investment destination, with the identified third-party facilities in the city contributing to over 90% of the existing power capacity. Most existing data centers are smaller facilities built over a limited area. The International Renewable Energy Agency (IRENA) stated that renewable energy contributed to around 33% of the overall electricity capacity in 2020 in Argentina, and the country aims to generate 20% of the electricity via renewable sources by 2025. The country aims to be one of the largest data center hubs in the coming time period.

South America Data Center Market Trends

The high internet and smartphone technology adoption by various businesses and growing digital usage across the region drives the market demand

- In 2020, mobile technologies and services accounted for 7.1% of GDP in Latin America - a contribution that amounted to more than USD 340 billion of economic value added. The mobile ecosystem also supported more than 1.6 million jobs (directly and indirectly). By 2025, the economic contribution of the Latin American mobile ecosystem will grow by more than USD 30 billion as countries in the region increasingly benefit from the improvements in productivity and efficiency brought about by the increased take-up of mobile services.

- Digital usage is expanding rapidly in Brazil. The high internet and smartphone technology adoption by various businesses has impacted consumer behavior. More people in the country can now purchase smartphones, leading to a growing number of smartphone users. In May 2020, most shopping apps downloaded in South America were developed in Brazil, which stood out with approximately 44 million app downloads in this category.

- In Chile, e-commerce is expanding steadily. Chile's average annual revenue per paying user amounted to USD 913 in 2020. Most cross-border e-commerce purchases by Chilean shoppers stand at 69%. As a result, vast amounts of data have been created, increasing the demand for data centers nationwide. In South America, the transition to 5G is progressing rapidly, driven by the continued rollout of new networks, the expansion of the device ecosystem, and the development of new applications for consumers and enterprises.

People across the region increasingly reliant on the internet for banking, business, & telecommunication services and increasing FTTH subscribers across the region drives the market growth

- In South America and the Caribbean, less than 50% of the population has access to fixed broadband internet, and only 9.9% has fiber internet access. Many rural areas have patchy network coverage due to expensive network equipment. Chile has set the standard for other countries to follow in fixed broadband. Chile has the fastest data download speeds in Latin America. With an average rate of 219 Mbps, Chile is well ahead of the region's largest economy, Brazil, where internet download speeds average 95.95 Mbps.

- The Brazilian population became increasingly reliant on the internet for banking, business, telecommunication, and leisure during the COVID-19 pandemic. However, the country ranked 49th globally for fixed broadband speed and 74th for mobile speed as of April 2021. This shows that access to the internet and broadband speed are growing rapidly, meaning data centers will benefit from faster data transfer, higher storage rates, and lower latency.

- Latin America's fiber-to-the-home (FTTH) market was set to register approximately 105 million homes with fiber in 2022, an increase of 36%, or 28 million new premises, compared with the end of 2021. Latin America now has a fiber penetration rate of nearly 61%. In terms of investment, in 2021, to penetrate the fixed broadband (FTTH) market, Chilean mobile operator WOM teamed with digital enablement and revenue management software company Aleppo.

South America Data Center Industry Overview

The South America Data Center Market is moderately consolidated, with the top five companies occupying 50.76%. The major players in this market are Ascenty (Digital Realty Trust Inc.), Equinix Inc., HostDime Global Corp., Scala Data Centers and Terremark (Verizon) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 It Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 Key Industry Trends

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.6.1 Brazil

- 5.6.2 Chile

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

- 6.1 Data Center Size

- 6.1.1 Large

- 6.1.2 Massive

- 6.1.3 Medium

- 6.1.4 Mega

- 6.1.5 Small

- 6.2 Tier Type

- 6.2.1 Tier 1 and 2

- 6.2.2 Tier 3

- 6.2.3 Tier 4

- 6.3 Absorption

- 6.3.1 Non-Utilized

- 6.3.2 Utilized

- 6.3.2.1 By Colocation Type

- 6.3.2.1.1 Hyperscale

- 6.3.2.1.2 Retail

- 6.3.2.1.3 Wholesale

- 6.3.2.2 By End User

- 6.3.2.2.1 BFSI

- 6.3.2.2.2 Cloud

- 6.3.2.2.3 E-Commerce

- 6.3.2.2.4 Government

- 6.3.2.2.5 Manufacturing

- 6.3.2.2.6 Media & Entertainment

- 6.3.2.2.7 Telecom

- 6.3.2.2.8 Other End User

- 6.4 Country

- 6.4.1 Brazil

- 6.4.2 Chile

- 6.4.3 Rest of South America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.3.1 Ascenty (Digital Realty Trust Inc.)

- 7.3.2 EdgeUno Inc.

- 7.3.3 Equinix Inc.

- 7.3.4 GTD Grupo Teleductos SA

- 7.3.5 HostDime Global Corp.

- 7.3.6 Lumen Technologies Inc.

- 7.3.7 NABIAX

- 7.3.8 ODATA (Patria Investments Ltd)

- 7.3.9 Quantico Data Center

- 7.3.10 Scala Data Centers

- 7.3.11 SONDA SA

- 7.3.12 Terremark (Verizon)

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms

2026年全球智慧客戶資料中心市場報告2026年全球網路資料中心(IDC)市場報告2026年全球資料中心房地產市場報告

2026年全球智慧客戶資料中心市場報告2026年全球網路資料中心(IDC)市場報告2026年全球資料中心房地產市場報告 資料中心市場:按組件、資料中心類型、層級、冷卻方式、電源、最終用戶和組織規模分類-2026年至2032年全球市場預測

資料中心市場:按組件、資料中心類型、層級、冷卻方式、電源、最終用戶和組織規模分類-2026年至2032年全球市場預測 全球在軌資料中心市場預測(至2034年)-按平台、組件、系統、連接類型、應用、最終用戶和地區分類的分析

全球在軌資料中心市場預測(至2034年)-按平台、組件、系統、連接類型、應用、最終用戶和地區分類的分析 資料中心匯流排市場規模、佔有率和成長分析:按導體材料、絕緣類型、額定功率、安裝/整合方法、資料中心類型和地區分類-2026-2033年產業預測2026年全球客製化資料中心市場報告

資料中心匯流排市場規模、佔有率和成長分析:按導體材料、絕緣類型、額定功率、安裝/整合方法、資料中心類型和地區分類-2026-2033年產業預測2026年全球客製化資料中心市場報告 資料中心能源概況 - Oracle:自 2019 年以來,能源使用量以 24% 的複合年成長率成長,由於可再生能源的使用,排放保持穩定,但 Stargate 專案可能會大幅增加碳足跡。

資料中心能源概況 - Oracle:自 2019 年以來,能源使用量以 24% 的複合年成長率成長,由於可再生能源的使用,排放保持穩定,但 Stargate 專案可能會大幅增加碳足跡。 氫動力資料中心市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能、安裝模式資料中心市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案

氫動力資料中心市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能、安裝模式資料中心市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案