|

市場調查報告書

商品編碼

1910843

德國資料中心市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Germany Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

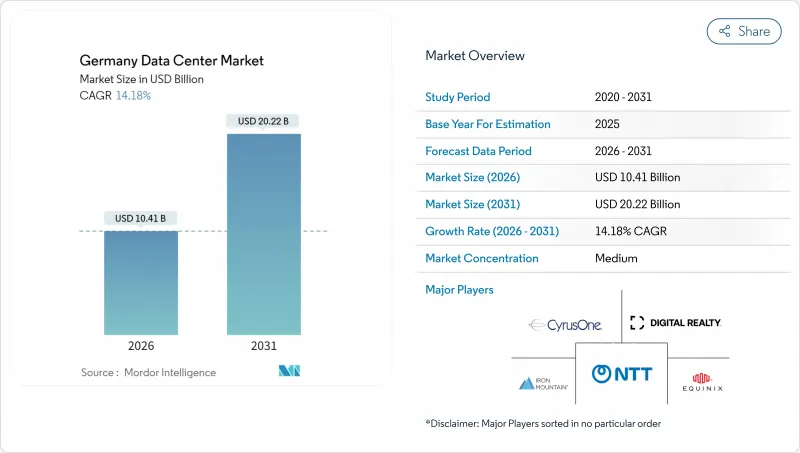

德國資料中心市場預計到 2026 年將達到 104.1 億美元,高於 2025 年的 91.2 億美元。

預計到 2031 年將達到 202.2 億美元,2026 年至 2031 年的複合年成長率為 14.18%。

就IT負載容量而言,市場預計將從2025年的3,440兆瓦成長到2030年的6,230兆瓦,在預測期(2025-2030年)內複合年成長率(CAGR)為12.60%。市場佔有率和估計值均以兆瓦為單位計算和報告。成長的主要驅動力是人工智慧(AI)工作負載的快速成長、超大規模資料中心業者營運商持續的資本支出以及鼓勵建造現代化高密度設施的監管要求。該市場在歐洲已位居第二,在法蘭克福,超大規模資料中心業者營運商的預租承諾吸收速度超過了新增供給能力的吸收速度。此外,5G賦能的邊緣配置正使主要都會區以外的需求多元化。機架密度的提升和液冷技術的應用正在縮小雲端環境和本地環境之間的效能差距,促使企業擺脫傳統的伺服器機房。最後,政府對自主人工智慧基礎設施和廢熱再利用的激勵措施正在創造新的收入來源,並加強對新計畫的投資決策。

德國資料中心市場趨勢與洞察

人工智慧、雲端運算和5G推動工作負載快速成長

基於GPU的推理和訓練的擴展正推動機架密度達到30-100kW,與傳統企業環境相比實現了五倍的飛躍。微軟斥資32億歐元,計畫在2026年將國內人工智慧容量加倍,凸顯了這種規模的變革;而德國電信的目標是到2030年部署1萬個邊緣節點,以支援5G低延遲應用場景。目前,法蘭克福超大規模資料中心的平均運轉率超過85%,造成了供應緊張,迫使新進業者選擇備用場地。由於風冷系統已無法應對高密度GPU叢集的熱負荷,液冷技術的應用正在加速。這些技術現實共同推動了電力和占地面積的需求,直接為德國資料中心市場中那些嚴格遵守能源效率標準的營運商創造了更多商機。

法蘭克福超大規模資料中心業者擴張計劃

亞馬遜網路服務(AWS)計劃在2040年投資94.4億美元,這將是德國有史以來規模最大的私營部門基礎設施投資,鞏固了法蘭克福作為德國領先人工智慧中心的地位。如此規模的投資吸引了重視雲端連接接近性的企業租戶,但也推高了地價,加劇了電網瓶頸。開發商目前正在模擬分階段建設,利用中間柴油發電機作為過渡方案,等待最終高壓供電線路的建成。儘管存在集中風險,但由於主要租戶通常會簽訂10至15年的電力契約,因此近期收益前景正在改善。

法蘭克福都會區電網連接限制

由於區域變電站接近飽和,聯邦網路管理局目前採用候補名單系統分配新的大容量饋線。開發商表示,50兆瓦及以上的併網工程面臨18至24個月的延誤,迫使他們分階段運作或將工程遷至鄰近的萊茵蘭地區。一項耗資7.5億歐元的電網強化計畫有望緩解這一壓力,但預計要到2033年才能全面生效。因此,一些計劃提前購買電池儲能設備,以便在啟動運作自主滿足關鍵負載需求,這增加了資本預算,也使資金籌措更加複雜。

細分市場分析

截至2025年,大型機房在德國資料中心市場佔據33.62%的佔有率,主要得益於超大規模資料中心業者資料中心的規模經濟效應。同時,邊緣站點雖然規模較小,但隨著5G的普及加速本地處理,其複合年成長率(CAGR)仍維持在12.97%。儘管目前邊緣資料中心在德國資料中心市場的佔有率仍然小規模,但像德國電信這樣的業者計劃在2030年部署1萬個節點,這條藍圖可能會增加區域接入點(PoP)的數量。邊緣節點通常安裝在維修的電信交換機房中,從而降低土地成本並縮短核准流程。即使在微型站點中,液冷系統維修也正成為常態,因為人工智慧推理處理需要類似於核心園區的高密度機架。

容量在 5 至 25 兆瓦之間的中型資料中心,對於那些已超出其本地部署環境容量但尚未準備好遷移到超大規模資料中心的公司而言,是一個理想的過渡方案。法蘭克福正在建造多個容量超過 100 兆瓦的大型資料中心園區,但由於電網壓力,這些園區不得不分階段投入運作。因此,德國資料中心市場呈現出大規模集中式資料中心與不斷擴展的邊緣資料中心並存的趨勢,在不犧牲雲間互聯性的前提下,將運算資源更靠近使用者。

到2025年,三級資料中心將佔德國資料中心裝置容量的59.25%,反映出企業對可控價格下並行維護性的重視。四級資料中心容量是德國資料中心市場成長最快的細分市場,複合年成長率達13.62%。這主要歸功於銀行、金融和保險(BFSI)以及人工智慧訓練,這些行業在長時間模型運行週期中無法容忍停機。法蘭克福的金融公司通常需要可用性超過99.995%的高彈性設計。雖然邊緣資料中心目前主要採用二級資料中心等級的設計,但它們擴大採用N+1液冷迴路,從而有效地提升了彈性等級。

當工作負載需要極高的正常運作時,超大規模資料中心業者資金籌措Tier 4 級資料中心;而對於 Tier 3 級資料中心,自動擴展的消費級雲端執行個體即可滿足需求。目前,德國所有新建設資料中心都必須通過 EN 50600-3 標準認證。展望未來,混合架構將融合 Tier 4 級核心資料中心和高彈性邊緣資料中心,根據工作負載的關鍵性,為德國資料中心市場帶來多層拓撲結構。

德國資料中心市場報告按資料中心規模(大型、超大型、中型、巨型、小規模)、等級(Tier 1-2、Tier 3、Tier 4)、資料中心類型(超大規模/自建、企業/邊緣、託管)、最終用戶(銀行、金融服務和保險 (BFSI)、IT 和 ITES、電子商務、政府、電信製造業、媒體和娛樂、金融服務和保險 (BFSI)、IT 和 ITES、電子商務、政府、電信製造業、媒體和娛樂、金融服務和保險 (BFSI)、IT 和 ITES、電子商務、政府、電信製造業、媒體和娛樂、金融服務和保險 (BFSI)、IT 和 ITES、電子商務、政府、電信製造業、媒體和娛樂、金融服務和保險 (BFSI)、IT 和 ITES、電子商務、政府、電信製造業、媒體和娛樂、金融服務和保險 (BFSI)、IT 和 ITES、電子商務、政府、電信製造業、媒體和娛樂、金融服務和保險 (BFSI)、IT 和 ITES、電子商務、政府、電信製造業、媒體和娛樂、金融服務和保險 (BFSI)、IT 和 ITES、電子商務、政府、電信製造業、媒體和娛樂、金融服務和保險 (BFSI)、IT 和 ITES、電子商務、政府、電信製造業、市場預測以 IT 負載容量(兆瓦,MW)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 人工智慧、雲端運算和 5G 推動工作負載爆炸性成長

- 法蘭克福超大規模資料中心業者擴張計劃

- 透過 DE-CIX 實現強大的光纖和海底光纜連接

- 企業數位轉型和GDPR推動了對託管服務的需求。

- 政府支持的人工智慧超級工廠計劃促進新建設

- 透過強制利用廢熱創造二次收入來源

- 市場限制

- 法蘭克福都會區電網連接受限和電力短缺

- 與其他歐盟國家相比,電力成本較高

- EnEfG 合規成本涉及可再生能源採購義務和 PUE 限制

- 高密度液體冷卻操作領域技術純熟勞工短缺

- 市場展望

- IT負載能力

- 高架樓層面積

- 託管收入

- 預裝機架

- 機架空間利用率

- 海底電纜

- 主要行業趨勢

- 智慧型手機用戶數量

- 每部智慧型手機的數據流量

- 行動資料通訊速度

- 寬頻資料通訊速度

- 光纖連接網路

- 法律規範

- 價值鍊和通路分析

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(兆瓦)

- 按資料中心規模

- 大規模

- 巨大的

- 中號

- 百萬

- 小規模

- 依層級類型

- 一級和二級

- 三級

- 第四級

- 依資料中心類型

- 超大規模/內部建設

- 企業/邊緣運算

- 搭配

- 未使用的

- 運作中

- 零售共址

- 批發託管

- 最終用戶

- BFSI

- 資訊科技/資訊科技服務

- 電子商務

- 政府機構

- 製造業

- 媒體與娛樂

- 溝通

- 其他最終用戶

- 透過熱點

- 法蘭克福

- 漢堡

- 德國其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Equinix, Inc.

- NTT Corporation

- Digital Realty Trust Inc.

- Vantage Data Centers, LLC

- Leaseweb Global BV

- CloudHQ, LLC

- Goodman Group

- noris network AG

- euNetworks Group Limited

- Global Switch Holdings Limited

- Telehouse International Corporation of Europe Ltd.

- AtlasEdge Data Centres Ltd.

- ITENOS GmbH

- STACK Infrastructure, Inc.

- GlobalConnect A/S

- maincubes one Services GmbH

- CyrusOne Inc.

- Iron Mountain Inc.

- EdgeConneX, Inc.

- Data4 Group

第7章 市場機會與未來展望

Germany Data Center market size in 2026 is estimated at USD 10.41 billion, growing from 2025 value of USD 9.12 billion with 2031 projections showing USD 20.22 billion, growing at 14.18% CAGR over 2026-2031.

In terms of IT load capacity, the market is expected to grow from 3.44 thousand megawatts in 2025 to 6.23 thousand megawatts by 2030, at a CAGR of 12.60% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. Growth is driven by the surge in artificial intelligence (AI) workloads, sustained hyperscaler capital expenditures, and regulatory requirements that favor modern, high-density facilities. The market already ranks as Europe's second-largest hub; hyperscaler pre-leasing in Frankfurt is absorbing new capacity faster than it can be delivered, while 5G-enabled edge deployments diversify demand beyond the main metro. Rising rack densities and the adoption of liquid cooling are narrowing the performance gap between cloud and on-premise environments, encouraging enterprises to abandon legacy server rooms. Finally, government incentives for sovereign AI infrastructure and waste-heat reuse create incremental revenue streams that strengthen the investment case for new projects.

Germany Data Center Market Trends and Insights

AI, Cloud and 5G-Driven Workload Surge

Ramp-up of GPU-powered inference and training is pushing rack densities to 30-100 kW, a five-fold leap from traditional enterprise footprints. Microsoft's EUR 3.2 billion program to double national AI capacity by 2026 highlights the scale shift, while Deutsche Telekom targets 10,000 edge nodes by 2030 to support 5G low-latency use cases. Average hyperscale utilization in Frankfurt now exceeds 85%, tightening available supply and pushing new entrants toward secondary sites. Liquid-cooling adoption is gaining momentum as air systems can no longer evacuate the thermal load of dense GPU clusters. These technical realities collectively amplify power and floor-space demand, directly lifting revenue opportunities for operators adhering to the Germany data center market's stringent efficiency codes.

Hyperscaler Expansion Commitments to Frankfurt

Amazon Web Services' USD 9.44 billion pledge through 2040 represents the largest single private-sector infrastructure investment in Germany to date, cementing Frankfurt as the country's AI nucleus. Such scale attracts enterprise tenants who value latency adjacency to cloud on-ramps, but the same clustering inflates land prices and exacerbates grid bottlenecks. Operators now model multi-phase builds with interim diesel-generator bridging while waiting for final high-voltage feeds. Although risk is concentrated, near-term revenue visibility improves because anchor tenants typically lock in 10- to 15-year power contracts.

Grid Connection Constraints in Frankfurt Metro

Bundesnetzagentur now allocates new high-capacity feeds via a queueing mechanism as local substations approach saturation. Developers report 18-24-month delays for >=50 MW connections, forcing staged commissioning or relocation to nearby Rhineland plots. A EUR 750 million reinforcement program will ease pressure, but full impact is unlikely before 2033. Consequently, some projects pre-purchase battery storage to self-sustain critical loads during ramp-up, inflating capital budgets and complicating financing.

Other drivers and restraints analyzed in the detailed report include:

- Strong Fiber and Submarine Connectivity via DE-CIX

- Corporate Digital Transformation and GDPR-Driven Colocation Demand

- High Electricity Costs Relative to EU Peers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large halls retained 33.62% of the Germany data center market share in 2025 thanks to hyperscaler economies of scale. Yet edge sites, while smaller, are on track for 12.97% CAGR as 5G adoption accelerates localized processing. The Germany data center market size allocated to edge remains modest today, but operators such as Deutsche Telekom plan 10,000 nodes by 2030, a roadmap that will multiply regional PoP counts. Edge units frequently occupy refurbished telecom exchanges, lowering land costs and shortening permitting cycles. Liquid-cooling retrofits are becoming standard even at micro sites because AI inferences require high-density racks similar to core campuses.

Medium facilities often 5-25 MW provide a bridging option for enterprises that outgrow on-premise rooms but are not yet ready for hyperscale footprints. In Frankfurt, mega campuses exceeding 100 MW continue to break ground, though grid scarcity forces phased energization. The Germany data center market thus combines massive centralized developments with a proliferating edge rim, bringing compute closer to users without sacrificing cloud interconnectivity.

Tier 3 halls comprised 59.25% of installed power in 2025, reflecting enterprises' preference for concurrent maintainability at a manageable price point. The Germany data center market size allocated to Tier 4 grows the fastest, 13.62% CAGR, because BFSI and AI training cannot tolerate downtime during long model-run cycles. Financial firms in Frankfurt routinely specify fault-tolerant designs delivering >=99.995% availability. Edge locations tend toward Tier 2 equivalents but increasingly add N+1 liquid-cooling loops, effectively moving up the resilience ladder.

Hyperscalers finance Tier 4 builds where workloads justify premium uptime, while auto-scaling consumer cloud instances remain content with Tier 3. Certification to the EN 50600-3 standard is now a baseline across all new German builds. Over time, hybrid architectures will mesh Tier 4 cores with resilient edge outposts, giving the Germany data center market a multi-tier topology aligned to workload criticality.

The Germany Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-built, Enterprise/Edge, and Colocation), End User (BFSI, IT and ITES, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and More), and Hotspot. The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

List of Companies Covered in this Report:

- Equinix, Inc.

- NTT Corporation

- Digital Realty Trust Inc.

- Vantage Data Centers, LLC

- Leaseweb Global B.V.

- CloudHQ, LLC

- Goodman Group

- noris network AG

- euNetworks Group Limited

- Global Switch Holdings Limited

- Telehouse International Corporation of Europe Ltd.

- AtlasEdge Data Centres Ltd.

- ITENOS GmbH

- STACK Infrastructure, Inc.

- GlobalConnect A/S

- maincubes one Services GmbH

- CyrusOne Inc.

- Iron Mountain Inc.

- EdgeConneX, Inc.

- Data4 Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI, Cloud and 5G-Driven Workload Surge

- 4.2.2 Hyperscaler Expansion Commitments to Frankfurt

- 4.2.3 Strong Fiber and Submarine Cable Connectivity via DE-CIX

- 4.2.4 Corporate Digital Transformation and GDPR-Driven Colocation Demand

- 4.2.5 Government-Backed AI Gigafactory Initiatives Incentivizing New Build

- 4.2.6 Waste Heat Utilization Mandates Creating Secondary Revenue Streams

- 4.3 Market Restraints

- 4.3.1 Grid Connection Constraints and Power Scarcity in Frankfurt Metro

- 4.3.2 High Electricity Costs Relative to Other EU Peers

- 4.3.3 EnEfG Compliance Costs for Mandatory Renewable Sourcing and PUE Limits

- 4.3.4 Skilled Labor Shortage in High-Density Liquid Cooling Operations

- 4.4 Market Outlook

- 4.4.1 IT Load Capacity

- 4.4.2 Raised Floor Space

- 4.4.3 Colocation Revenue

- 4.4.4 Installed Racks

- 4.4.5 Rack Space Utilization

- 4.4.6 Submarine Cable

- 4.5 Key Industry Trends

- 4.5.1 Smartphone Users

- 4.5.2 Data Traffic Per Smartphone

- 4.5.3 Mobile Data Speed

- 4.5.4 Broadband Data Speed

- 4.5.5 Fiber Connectivity Network

- 4.5.6 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MEGAWATT)

- 5.1 By Data Center Size

- 5.1.1 Large

- 5.1.2 Massive

- 5.1.3 Medium

- 5.1.4 Mega

- 5.1.5 Small

- 5.2 By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale / Self-built

- 5.3.2 Enterprise / Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End User

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Hotspot

- 5.5.1 Frankfurt

- 5.5.2 Hamburg

- 5.5.3 Rest of Germany

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Equinix, Inc.

- 6.4.2 NTT Corporation

- 6.4.3 Digital Realty Trust Inc.

- 6.4.4 Vantage Data Centers, LLC

- 6.4.5 Leaseweb Global B.V.

- 6.4.6 CloudHQ, LLC

- 6.4.7 Goodman Group

- 6.4.8 noris network AG

- 6.4.9 euNetworks Group Limited

- 6.4.10 Global Switch Holdings Limited

- 6.4.11 Telehouse International Corporation of Europe Ltd.

- 6.4.12 AtlasEdge Data Centres Ltd.

- 6.4.13 ITENOS GmbH

- 6.4.14 STACK Infrastructure, Inc.

- 6.4.15 GlobalConnect A/S

- 6.4.16 maincubes one Services GmbH

- 6.4.17 CyrusOne Inc.

- 6.4.18 Iron Mountain Inc.

- 6.4.19 EdgeConneX, Inc.

- 6.4.20 Data4 Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球智慧客戶資料中心市場報告2026年全球網路資料中心(IDC)市場報告2026年全球資料中心房地產市場報告

2026年全球智慧客戶資料中心市場報告2026年全球網路資料中心(IDC)市場報告2026年全球資料中心房地產市場報告 資料中心市場:按組件、資料中心類型、層級、冷卻方式、電源、最終用戶和組織規模分類-2026年至2032年全球市場預測

資料中心市場:按組件、資料中心類型、層級、冷卻方式、電源、最終用戶和組織規模分類-2026年至2032年全球市場預測 全球在軌資料中心市場預測(至2034年)-按平台、組件、系統、連接類型、應用、最終用戶和地區分類的分析

全球在軌資料中心市場預測(至2034年)-按平台、組件、系統、連接類型、應用、最終用戶和地區分類的分析 資料中心匯流排市場規模、佔有率和成長分析:按導體材料、絕緣類型、額定功率、安裝/整合方法、資料中心類型和地區分類-2026-2033年產業預測2026年全球客製化資料中心市場報告

資料中心匯流排市場規模、佔有率和成長分析:按導體材料、絕緣類型、額定功率、安裝/整合方法、資料中心類型和地區分類-2026-2033年產業預測2026年全球客製化資料中心市場報告 資料中心能源概況 - Oracle:自 2019 年以來,能源使用量以 24% 的複合年成長率成長,由於可再生能源的使用,排放保持穩定,但 Stargate 專案可能會大幅增加碳足跡。

資料中心能源概況 - Oracle:自 2019 年以來,能源使用量以 24% 的複合年成長率成長,由於可再生能源的使用,排放保持穩定,但 Stargate 專案可能會大幅增加碳足跡。 氫動力資料中心市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能、安裝模式資料中心市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案

氫動力資料中心市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能、安裝模式資料中心市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案