|

市場調查報告書

商品編碼

1693395

西班牙密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Spain Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

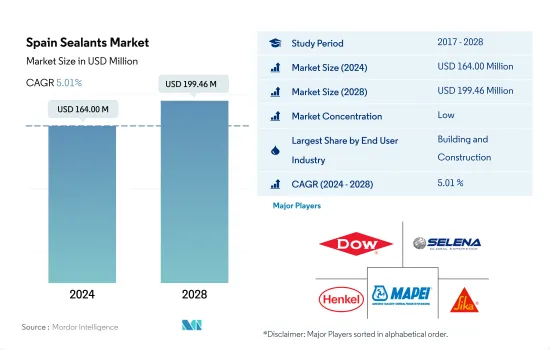

西班牙密封劑市場規模預計在 2024 年為 1.64 億美元,預計到 2028 年將達到 1.9946 億美元,預測期內(2024-2028 年)的複合年成長率為 5.01%。

新建設和基礎建設推動市場成長

- 西班牙密封劑市場主要由建設產業推動,其次是其他終端用戶行業,因為密封劑在建築和建設活動中有多種應用,例如防水、防風雨密封、裂縫密封和接縫密封。此外,建築密封劑的使用壽命很長,且易於應用於各種基材。 2019 年,西班牙建築業約佔該國 GDP 的 5.7%。在新冠疫情期間,由於該國建築投資和住宅維護活動增加,建築業產出在 2020 年下降了 19.5%,並在 2021 年持續下降。這些趨勢可能在可預見的未來持續下去,並逐漸增加對密封劑的需求。

- 電氣設備製造中使用各種密封劑進行灌封和保護應用。用於密封感測器和電纜等。由於無線電子產品的日益普及和穿戴式裝置的迅速普及,西班牙電子市場實現了強勁成長。這將推動其他終端用戶領域對密封劑的需求。此外,到 2028 年,機車和 DIY 行業中密封劑的各種應用可能會增加對必要密封劑的需求。

- 密封劑在醫療保健和汽車行業中有著廣泛的應用。密封劑用於醫療保健應用,例如組裝和密封醫療設備零件。汽車工業顯示出密封膠對各種基材的廣泛適用性,主要用於引擎和汽車墊圈。西班牙最近在這些領域取得了令人鼓舞的成長,而這種勢頭在未來幾年可能會持續下去。因此,預計到 2028 年這些趨勢將推動對密封劑的需求。

西班牙密封膠市場趨勢

國家恢復重建計劃(NRRP)等價值 10 億歐元的經濟適用住宅投資將推動建設產業

- 新冠疫情對西班牙建築業的影響是巨大的。建設產業受到重創,2020 年第一季投資下降 9.6%。 2020 年第一季,運輸和旅館業的建設活動產出下降了 11%。

- 為了重振建築市場,西班牙政府對《2018-2021年國家住宅計畫》進行了修訂,包括將計畫延長至2022年12月31日。該國還獲得了歐洲投資銀行(EIB)的資金支持,用於社會住宅的開發和建設。西班牙建築市場預計將在 2021 年強勁復甦,成長約 24.9%。截至 2021 年 6 月,歐洲投資銀行已簽署協議,支持巴塞隆納市議會投資 3,620 萬歐元,建造約 490 套新的公共租賃住宅。

- 西班牙政府根據2021-2026年國家復甦與復原力計畫(NRRP),撥款10億歐元用於興建經濟適用且節能的出租住宅。因此,預計該國建築市場在預測期內(2022-2028 年)的複合年成長率將達到 2%。

- 西班牙建設產業的前景整體樂觀。預計未來幾年歐盟資助的公共基礎設施、數位化、節能住宅重建和綠色循環經濟的投資將推動產業成長。

電動車需求的不斷成長以及價值 240 億歐元的公共和私人電動交通投資將推動汽車需求

- 西班牙是繼德國之後歐洲第二大汽車生產國。 2019 年,西班牙汽車供應商生產了價值 358.22 億歐元的商品,其中 60% 出口到歐洲國內外。

- 近年來,該國的汽車產量保持相當穩定。 2019年該國汽車產量約2,822,355輛,與2018年相比僅成長0.1%。 2020年該國汽車產量約2,268,185輛。由於新冠疫情導致供應鏈中斷,2020 年汽車產量下降了 18.6%。

- 2021年前第三季汽車產量比2020年前第三季成長4%,達到1,592,277輛。預測期內,該國汽車產業的需求可能適中。然而,2021年該國汽車產量約為2,098,133輛,較2020年下降8%。半導體晶片短缺和供應鏈限制對該國的汽車產量產生了不利影響。

- 汽車產量短缺近期進一步加劇,預計2022年將強勁復甦,產量將成長18%。西班牙的電動車市場應該會受益於下一代歐盟基金,該基金支持供應商向電動車轉型。此外,西班牙政府宣布未來三年將向公共和私人電子交通領域投資 240 億歐元。

西班牙密封劑產業概況

西班牙密封劑市場分散,前五大公司佔35.13%。該市場的主要企業為:陶氏化學、賽萊納集團、漢高股份公司、馬貝集團和西卡股份公司(按字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 法律規範

- 西班牙

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 衛生保健

- 其他最終用戶產業

- 樹脂

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽膠

- 其他樹脂

第6章 競爭格局

- 重大策略舉措

- 市場佔有率分析

- 商業狀況

- 公司簡介.

- 3M

- Dow

- Grupa Selena

- Henkel AG & Co. KGaA

- Industrias Quimicas del Adhesivo, SA-Quiadsa

- MAPEI SpA

- QS Adhesives & Sealants SL

- RPM International Inc.

- Sika AG

- Soudal Holding NV

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 全球黏合劑和密封劑產業概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 促進因素、阻礙因素和機會

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 92451

The Spain Sealants Market size is estimated at 164.00 million USD in 2024, and is expected to reach 199.46 million USD by 2028, growing at a CAGR of 5.01% during the forecast period (2024-2028).

New construction and infrastructure development to lead the market growth

- The Spain sealants market is majorly driven by the construction industry, followed by other end-user industries due to diverse applications of sealants in building and construction activities such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing. Moreover, construction sealants are designed for longevity and ease of application on different substrates. The construction industry of Spain registered around 5.7% of the country's GDP in 2019. During COVID-19, the construction output was reduced by 19.5% in 2020, sustained in 2021 owing to increasing construction investment and home maintenance activities in the country. Such trends will likely continue in the near future and gradually increase sealants demand.

- A variety of sealants are used in electrical equipment manufacturing for potting and protecting applications. They are used for sealing sensors and cables, etc. The Spanish electronics market registered significant growth, mostly due to the growing popularity of wireless electronic devices and the rapid adoption of wearable gadgets. This, in terms, will foster the demand for sealants in the other end-user segment. Moreover, a range of applications of sealants in the locomotive and DIY industries will boost the demand for required sealants by 2028.

- Sealants have diverse applications in the healthcare and automotive industries. Sealants are used in healthcare applications, such as assembling and sealing medical device parts. The automotive industry exhibits significant applicability of sealants to various substrates, mostly used for engines and car gaskets. Spain has registered promising growth in these sectors in recent times and is likely to continue in the upcoming years. Thus, such a trend will augment the demand for sealants by 2028.

Spain Sealants Market Trends

Investments including National Recovery and Resilience Plan (NRRP) worth EUR 1 billion for affordable housing to lead the construction industry

- The impact of the COVID-19 pandemic was huge on the Spanish construction sector. The construction industry pummeled and observed a decline of 9.6% in investments in the first three months of 2020. Construction activity output in the transport and hotel sector registered a decline of 11% in Q1 2020.

- To revive the construction market, the Spanish government introduced amendments to the State Housing Plan 2018-2021, including the program's extension until December 31, 2022. The country also receives financial support from the European Investment Bank (EIB) for developing and constructing social housing. The Spanish construction market was to rebound strongly in 2021 and grow about 24.9% in 2021. As of June 2021, the EIB signed an agreement to support Barcelona City Council in constructing nearly 490 new public rental homes with an investment of EUR 36.2 million.

- Under its 2021-2026 National Recovery and Resilience Plan (NRRP), the Spanish government allocated EUR 1 billion to construct affordable and energy-efficient rental housing. Thus, the construction market in the country is expected to register a 2% CAGR during the forecast period (2022-2028).

- The general outlook for the Spanish construction industry is favorable. Future industry growth is anticipated to be fueled by investments in public sector infrastructure, digitalization, energy-efficient housing renovations, and a green circular economy, all funded by the European Union.

Increasing EVs demand and government investment of public and private e-mobility investments worth EUR 24 billion to boost the automotive demand

- Spain is the second-largest automobile producer in Europe, after Germany. Spanish automotive suppliers produced EUR 35,822 million worth of products in 2019, of which 60% were exported inside and outside the European region.

- Automobile production in the country has been almost constant in the past few years. In 2019, the country produced about 28,22,355 units, registering a meager growth rate of 0.1% over 2018. The country produced about 22,68,185 units of vehicles in 2020. Automotive vehicle production contracted by 18.6% in 2020 as the COVID-19 pandemic halted the supply chain.

- In the first three quarters of 2021, automotive production increased by 4% over Q1-Q3 of 2020 and reached 1,592,277 vehicles. The country's automotive industry is likely to witness moderate demand during the forecast period. However, in 2021, the country produced about 2,098,133 vehicles, which was a decline of 8% from 2020. The semiconductor chip shortage and supply chain restrictions negatively affected the production of automotive vehicle units in the country.

- The automotive production shortfalls have recently worsened, and a strong rebound is expected in 2022, with output increasing by 18%. The Spanish electric vehicles market should benefit from the Next Generation EU fund, which supports suppliers in their shift toward e-mobility. Additionally, the Spanish government has announced public and private e-mobility investments worth EUR 24 billion over the coming three years.

Spain Sealants Industry Overview

The Spain Sealants Market is fragmented, with the top five companies occupying 35.13%. The major players in this market are Dow, Grupa Selena, Henkel AG & Co. KGaA, MAPEI S.p.A. and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Spain

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Dow

- 6.4.3 Grupa Selena

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Industrias Quimicas del Adhesivo, S.A. - Quiadsa

- 6.4.6 MAPEI S.p.A.

- 6.4.7 QS Adhesives & Sealants SL

- 6.4.8 RPM International Inc.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

建築和施工密封膠市場規模、佔有率和趨勢分析報告:按樹脂、技術、應用、功能、最終用途、分銷管道、地區和細分市場預測(2025-2033 年)

建築和施工密封膠市場規模、佔有率和趨勢分析報告:按樹脂、技術、應用、功能、最終用途、分銷管道、地區和細分市場預測(2025-2033 年) 工業密封件市場-2025-2030年預測彈性體密封劑市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)

工業密封件市場-2025-2030年預測彈性體密封劑市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年) 彈性體密封劑市場按類型、最終用途、應用、包裝和銷售管道分類-2025-2032年全球預測發泡密封膠市場按產品類型、泡棉成分、包裝類型、應用、最終用戶和銷售管道分類-2025-2032 年全球預測耐燃油密封膠市場(按樹脂類型、形式、固化機制、包裝和應用)—2025-2032 年全球預測

彈性體密封劑市場按類型、最終用途、應用、包裝和銷售管道分類-2025-2032年全球預測發泡密封膠市場按產品類型、泡棉成分、包裝類型、應用、最終用戶和銷售管道分類-2025-2032 年全球預測耐燃油密封膠市場(按樹脂類型、形式、固化機制、包裝和應用)—2025-2032 年全球預測 2025年全球預製建築密封膠市場報告

2025年全球預製建築密封膠市場報告 2032 年密封劑市場預測:按樹脂類型、應用、最終用戶和地區分類的全球分析全球密封劑市場:2025-2030 年預測

2032 年密封劑市場預測:按樹脂類型、應用、最終用戶和地區分類的全球分析全球密封劑市場:2025-2030 年預測 全球閥門密封劑市場(2025年)

全球閥門密封劑市場(2025年)

▼