|

市場調查報告書

商品編碼

1693396

中國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)China Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

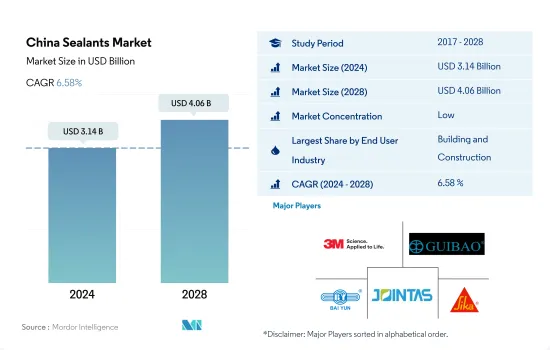

預計 2024 年中國密封劑市場規模為 31.4 億美元,到 2028 年將達到 40.6 億美元,預測期內(2024-2028 年)的複合年成長率為 6.58%。

建築密封膠增強了防水、裂縫密封、接縫密封應用的密封膠

- 中國的密封劑市場主要由建設產業推動,其次是其他終端用戶產業,因為密封劑在建築和建設活動中的應用多種多樣,例如防水、裂縫密封和接縫密封。此外,建築密封劑的使用壽命很長,且易於應用於各種基材。儘管受新冠疫情影響導致供應鏈中斷、生產停頓,但建築業在 2020 年仍實現了 6.9% 的 GDP 成長。

- 電氣設備製造中使用各種密封劑進行灌封和保護應用。它們用於密封感測器、電纜等。中國電子產品市場在 2020 年佔據了全球 41% 的市場佔有率,由於擁有廣泛的製造生態系統和龐大的勞動力,預計未來幾年將持續成長。預計這將推動其他終端用戶領域對密封劑的需求。此外,中國擁有全球機車和船舶工業的龐大生產能力,推動了對必要密封劑的需求。

- 密封劑在醫療保健和汽車行業中有著廣泛的應用。密封劑用於醫療保健應用,例如組裝和密封醫療設備零件。在汽車工業中,密封劑用於各種基材,主要用於引擎和車輛墊圈。近年來,中國在這些領域,尤其是汽車產業取得了可喜的成長,預計未來幾年這一趨勢將持續下去,從而推動到 2028 年對密封膠的需求。

中國密封膠市場趨勢

中國政府建設計畫醫療保健、醫院和醫療設施,推動中國建設

- 中國經濟成長的動力主要來自住宅和商業建築業的蓬勃發展。中國正處於持續都市化進程中,目標是2030年都市化率達到70%。在都市化過程中,都市區生活空間需求的增加以及城市都市區居民對改善居住條件的渴望將對住宅市場產生重大影響,可能導致中國住宅的增加。

- 非住宅基礎設施可能會大幅擴張。中國人口老化將需要更多的醫療設施和醫院。 2019年,中國政府核准了26個基礎建設計劃,總價值約1420億美元,預計2023年完工。中國是全球最大的建築市場,佔全球建築投資的20%。

- 在中國,香港住宅委員會已推出多項舉措,推動經濟適用住宅建設。當局的目標是到 2030 年提供 301,000 套公共住宅。家庭收入水準的提高加上農村人口向都市區的遷移預計將繼續刺激該國住宅建築業的需求。到2030年,預計該國在建設上的支出將超過13兆美元。因此,預計預測期內(2022-2028 年)建築市場的複合年成長率為 4.48%。

政府政策可能會刺激中國對電動車的需求,並促進汽車生產

- 2021年,中國乘用車市場保有量將達2,141萬輛,超過日本、美國、德國等全球主要汽車市場,成為全球最大乘用車市場。中國電動車製造商比亞迪佔全球電動車產量的8.84%。

- 中國作為新冠疫情的重災區,全國範圍內的停工停產、供應鏈中斷、人才短缺等問題,導致2020年汽車行業遭受巨大損失,導致2020年中國與前一年同期比較產銷同比出現負成長。

- 中國政府對電動車車主的限時購買補貼、交通豁免、充電回饋等政策促進了中國電動車的銷售和需求。預計2027年電動車銷量將達752.6萬輛。中國電動車產量預計將從2019年的100萬輛增加到2021年的350萬輛,預測期間(2022-2028年)的複合年成長率為15.07%。

- 上海工業Group Limited是中國產量最大的汽車製造商。上汽集團生產的乘用車和商用車數量大幅成長,從2019年的約200萬輛增加到2021年的700萬輛。這一成長趨勢表明,預計中國汽車市場在預測期內將穩定成長。

中國密封膠產業概況

中國密封膠市場較為分散,前五大企業市佔率合計為20.34%。市場的主要企業有:3M、成都矽寶科技、廣州白雲化工、廣州集泰化工和西卡股份公司(依字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 法律規範

- 中國

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 衛生保健

- 其他最終用戶產業

- 樹脂

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽膠

- 其他樹脂

第6章 競爭格局

- 重大策略舉措

- 市場佔有率分析

- 商業狀況

- 公司簡介.

- 3M

- Arkema Group

- Chengdu Guibao Science and Technology Co., Ltd.

- Dow

- Guangzhou Baiyun Chemical Industry Co.,ltd.

- Guangzhou Jointas Chemical Co.,Ltd.

- HB Fuller Company

- Hangzhou Zhijiang Advanced Material Co., ltd.

- Henkel AG & Co. KGaA

- Sika AG

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 全球黏合劑和密封劑產業概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 促進因素、阻礙因素和機會

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 92452

The China Sealants Market size is estimated at 3.14 billion USD in 2024, and is expected to reach 4.06 billion USD by 2028, growing at a CAGR of 6.58% during the forecast period (2024-2028).

Construction sealants to boost the sealants, owing to waterproofing, cracks-sealing, and joint-sealing applications

- The China sealants market is majorly driven by the construction industry, followed by other end-user industries due to diverse applications of sealants in building and construction activities, such as waterproofing, cracks-sealing, and joint-sealing. Moreover, construction sealants are designed for longevity and ease of application on different substrates. The construction sector achieved a GDP of 6.9% in 2020 despite supply chain disruption and production suspension due to COVID-19 impacts.

- A variety of sealants are used in electrical equipment manufacturing for potting and protecting applications. They are used for sealing sensors and cables, etc. The Chinese electronics market registered a market share of 41% globally in 2020 and is likely to have sustainable growth in the upcoming years due to the extensive presence of the manufacturing ecosystem with a huge labor force. This, in terms, will foster the demand for sealants in the other end-user segment. Moreover, China has a massive production capacity for locomotive and marine industries in the world, boosting the demand for required sealants.

- Sealants have diverse applications in the healthcare and automotive industries. Sealants are used in healthcare applications such as assembling and sealing medical device parts. The automotive industry exhibits significant applicability of sealants to various substrates, mostly used for engines and car gaskets. China registered promising growth in these sectors, specifically in automotive, in recent times and is likely to continue in the upcoming years, which will augment the demand for sealants by 2028.

China Sealants Market Trends

Housing, hospitals, and healthcare facilities schemes by the Chinese government to lead the construction in the country

- China has been majorly driven by the ample developments in the residential and commercial construction sectors and supported by the growing economy. China is promoting and undergoing a process of continuous urbanization, with a target rate of 70% for 2030. The increased living spaces required in the urban areas resulting from urbanization and the desire of middle-class urban residents to improve their living conditions may have a profound effect on the housing market and thereby increase the residential construction in the country.

- Non-residential infrastructure is likely to expand significantly. The country's aging population necessitates the construction of additional healthcare facilities and hospitals. The Chinese government approved 26 infrastructure projects worth approximately USD 142 billion in 2019, with completion due in 2023. The country boasts the world's largest construction market, accounting for 20% of all worldwide construction investments.

- In China, the housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units by 2030. The rising household income levels, combined with the population migrating from rural to urban areas, are expected to continue to drive the demand for the residential construction sector in the country. By 2030, the country is estimated to spend over USD 13 trillion on construction. Thus, the construction market is expected to register a 4.48% CAGR during the forecast period (2022-2028).

Owing to government policies, EVs demand in China is rising and is likely to propel the automotive production

- China's automotive market for passenger vehicles is the largest in the world, as it accounted for 21.41 million units in 2021 compared to other major global players such as Japan, the United States, and Germany. This number is expected to grow at the same pace because of the increasing production capacity of automotive companies post-pandemic in China, as BYD, which is a local electric vehicle manufacturer in China, holds 8.84% of total electric vehicle production in the world.

- China, being the epicenter of the COVID-19 pandemic, witnessed huge losses in the automotive industry in 2020 as it led to nationwide lockdowns, supply chain disruptions, lack of human resources availability, etc. This was the reason for the negative Y-o-Y growth rate in China in 2020.

- The Chinese government's policies for electric vehicle owners, such as time-limited purchase subsidies, traffic regulations waivers, and charging rebates for EV owners, have encouraged the sale and demand for EVs in China. The sales of electric vehicles are expected to reach 7,526 thousand in 2027. EV production in China increased from 1 million units in 2019 to 3.5 million units in 2021, and it is expected to record a 15.07% CAGR in the forecast period (2022-2028).

- Shanghai Automotive Industry Corporation is China's largest automotive company in terms of production. The growth in the number of both passenger and commercial vehicles manufactured by SAIC is significant, as it increased from nearly 2 million units in 2019 to 7 million units in 2021. This growth trend shows that the Chinese automotive market is expected to grow steadily during the forecast period.

China Sealants Industry Overview

The China Sealants Market is fragmented, with the top five companies occupying 20.34%. The major players in this market are 3M, Chengdu Guibao Science and Technology Co., Ltd., Guangzhou Baiyun Chemical Industry Co.,ltd., Guangzhou Jointas Chemical Co.,Ltd. and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 China

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Chengdu Guibao Science and Technology Co., Ltd.

- 6.4.4 Dow

- 6.4.5 Guangzhou Baiyun Chemical Industry Co.,ltd.

- 6.4.6 Guangzhou Jointas Chemical Co.,Ltd.

- 6.4.7 H.B. Fuller Company

- 6.4.8 Hangzhou Zhijiang Advanced Material Co., ltd.

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

全球隔熱密封劑市場報告(2026 年)

全球隔熱密封劑市場報告(2026 年) CIPG/FIPG液體墊片市場:按產品類型、包裝、黏度、應用、最終用戶、銷售管道分類 - 全球預測(2026-2032年)聲學密封膠和黏合劑市場:按產品、技術、類型、應用和分銷管道分類,全球預測(2026-2032年)重型密封蠟市場按產品類型、配方、應用方法、銷售管道、應用領域和最終用途產業分類-2026-2032年全球預測

CIPG/FIPG液體墊片市場:按產品類型、包裝、黏度、應用、最終用戶、銷售管道分類 - 全球預測(2026-2032年)聲學密封膠和黏合劑市場:按產品、技術、類型、應用和分銷管道分類,全球預測(2026-2032年)重型密封蠟市場按產品類型、配方、應用方法、銷售管道、應用領域和最終用途產業分類-2026-2032年全球預測 工業密封件市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034)

工業密封件市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034) 日本密封膠市場報告(按最終用戶產業(航太、汽車、建築、醫療保健及其他)、樹脂(丙烯酸、環氧樹脂、聚氨酯、矽酮及其他)和地區分類,2026-2034年)

日本密封膠市場報告(按最終用戶產業(航太、汽車、建築、醫療保健及其他)、樹脂(丙烯酸、環氧樹脂、聚氨酯、矽酮及其他)和地區分類,2026-2034年) 工業密封件市場規模、佔有率及成長分析(按類型、材質、產業及地區分類)-2026-2033年產業預測

工業密封件市場規模、佔有率及成長分析(按類型、材質、產業及地區分類)-2026-2033年產業預測 彈性密封劑市場規模、佔有率及成長分析(按產品類型、最終用途及地區分類)-2026-2033年產業預測

彈性密封劑市場規模、佔有率及成長分析(按產品類型、最終用途及地區分類)-2026-2033年產業預測 建築和施工密封膠市場規模、佔有率和趨勢分析報告:按樹脂、技術、應用、功能、最終用途、分銷管道、地區和細分市場預測(2025-2033 年)工業密封件市場-2025-2030年預測

建築和施工密封膠市場規模、佔有率和趨勢分析報告:按樹脂、技術、應用、功能、最終用途、分銷管道、地區和細分市場預測(2025-2033 年)工業密封件市場-2025-2030年預測

▼