|

市場調查報告書

商品編碼

1876545

植物性乳製品替代品市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Plant-Based Dairy Alternatives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

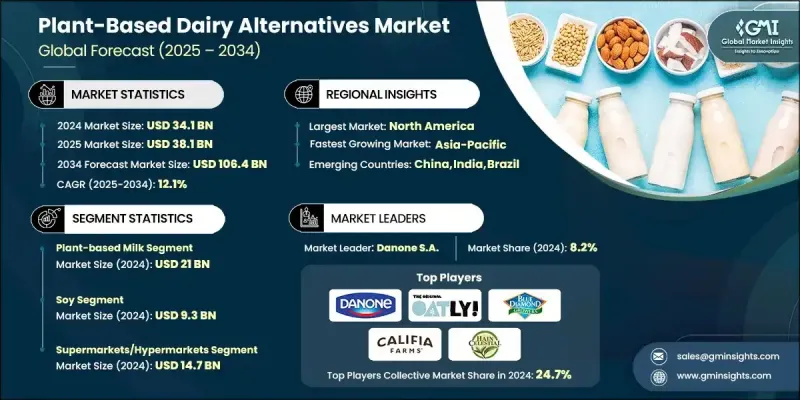

2024 年全球植物性乳製品替代品市場價值為 341 億美元,預計到 2034 年將以 12.1% 的複合年成長率成長至 1064 億美元。

隨著消費者日益尋求永續、營養且符合倫理道德的傳統乳製品替代品,市場正經歷快速成長。對無乳糖和純素食產品的需求不斷成長,加上配料技術的進步,正推動著該行業向前發展。儘管植物性起起司和優格目前在市佔率中佔比較小,但其成長速度強勁,達到兩位數,這得益於創新配方能夠複製乳製品的質地、風味和功能。大量資本投資正湧入該領域,成熟的乳製品生產商正在對其設施進行現代化改造,以加工燕麥、豌豆和杏仁等原料。鼓勵植物性蛋白質消費的政策變化以及將植物性飲料納入學校營養計劃,進一步刺激了市場需求。展望未來,監管政策的清晰度、價格平衡以及碳排放責任等因素將影響該行業的發展軌跡,這些因素將共同影響北美和歐洲主要市場的產品創新和原料採購。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 341億美元 |

| 預測值 | 1064億美元 |

| 複合年成長率 | 12.1% |

2024年,植物奶市場規模達到210億美元,預計2025年至2034年間將以12.1%的複合年成長率成長。目前,燕麥奶飲料在該市場佔據主導地位,因其口感溫和、用途廣泛且具有良好的永續性而備受青睞。隨著消費者探索豆奶和杏仁奶以外的其他選擇,大麻籽、椰子和蠶豆等原料正被添加到新的產品線中,以豐富產品種類並提升營養價值。各大品牌持續加大研發投入,致力於改善植物奶的口感、質地與營養密度,力求達到甚至超越乳製品。這個細分市場的蓬勃發展正推動整個植物奶產業的創新,提升消費者接受度並豐富產品種類。

2024年,超市和大賣場市場規模達147億美元,預計2025年至2034年將以11.1%的複合年成長率成長,佔市場總佔有率的43.2%。這些零售據點憑藉其寬敞的貨架空間和醒目的陳列位置,在分銷通路中佔據主導地位,助力植物性產品觸達主流消費者。同時,專賣店和健康食品零售商在測試和推出新產品方面繼續發揮至關重要的作用。隨著植物性乳製品日益普及,自有品牌也不斷擴張,提供價格更具競爭力的替代產品。便利商店也拓展產品種類,以滿足消費者在日常購物環境中對便利植物性產品的需求。

2024年,德國植物性乳製品替代品市場規模達19億美元,預計到2034年將以11.7%的複合年成長率成長。德國在歐洲處於領先地位,這得益於其強大的環保意識、杏仁和燕麥基乳製品替代品的廣泛應用,以及消費者對永續和本地採購產品的日益成長的偏好。國內品牌和連鎖超市之間的激烈競爭推動了自有品牌的發展,並擴大了消費者的試用範圍,進一步加速了市場擴張。

全球植物性乳製品替代品市場的主要參與者包括Hain Celestial Group、Blue Diamond Growers、Oatly Group AB、Califia Farms和達能集團(Danone SA)。這些領導企業正致力於創新、擴張和合作,以鞏固其市場地位。他們大力投資產品研發,力求透過先進的加工技術和原料最佳化,複製乳製品的質地和營養成分。與零售商和餐飲連鎖店建立策略合作夥伴關係,有助於提升產品的知名度和可及性。此外,各公司也正在擴大產能,並進軍新的區域市場,以滿足不斷成長的全球需求。多元化發展,例如採用燕麥、大麻籽和蠶豆等替代蛋白來源,有助於增強供應鏈的韌性,並實現永續發展目標。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預測模型

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(註:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2025-2034年

- 主要趨勢

- 植物奶

- 常溫保存

- 冷藏

- 植物優格

- 可舀取

- 飲用

- 植株起司

- 塊和輪

- 切絲和磨碎

- 切片

- 奶油乳酪和塗抹醬

- 餐飲服務類似物

- 植物性冰淇淋和冷凍甜點

- 品脫裝和桶裝

- 新奇

- 植物奶油和塗抹醬

- 棍棒/方塊

- 軟桶塗抹

- 奶油

- 冷藏液體

- 常溫保存液體

- 粉狀

- 其他

第6章:市場估算與預測:依來源分類,2025-2034年

- 主要趨勢

- 大豆

- 杏仁

- 燕麥

- 椰子

- 麻

- 混合/調和基底

- 新型蛋白質

- 蠶豆

- 亞麻籽

- 藜麥

- 其他蛋白質

第7章:市場估算與預測:依配銷通路分類,2025-2034年

- 主要趨勢

- 超市和大型超市

- 便利商店和雜貨店

- 特色食品店和健康食品店

- 線上零售/DTC

- 餐飲服務

- 工業/B2B原料

第8章:市場估算與預測:依地區分類,2025-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Blue Diamond Growers

- Califia Farms

- Danone SA

- Earth's Own Food Company Inc.

- Eden Foods, Inc.

- Elmhurst 1925

- Good Karma Foods

- Happy Planet Foods

- Hain Celestial Group

- Nestle SA

- Oatly Group AB

- Pacific Foods of Oregon, LLC

- Ripple Foods

- SunOpta Inc.

- The Coca-Cola Company (Fairlife/Simply platforms)

- The Hain Celestial Group

- The Hershey Company (via SOFIT)

- TurtleTree

- Valio Ltd

- Yili Group

The Global Plant-Based Dairy Alternatives Market was valued at USD 34.1 billion in 2024 and is estimated to grow at a CAGR of 12.1% to reach USD 106.4 billion by 2034.

The market is experiencing rapid growth as consumers increasingly seek sustainable, nutritious, and ethical alternatives to traditional dairy products. Rising demand for lactose-free and vegan options, combined with advancements in ingredient technology, is propelling the industry forward. Although plant-based cheese and yogurt currently represent smaller portions of the market, they are growing at strong double-digit rates, supported by innovative formulations that replicate the texture, flavor, and functionality of dairy. Significant capital investments are flowing into the sector, with established dairy producers modernizing their facilities to process ingredients such as oats, peas, and almonds. Policy changes encouraging plant protein consumption and school nutrition programs that incorporate plant-based beverages are further stimulating demand. Looking ahead, the industry's trajectory will be shaped by factors such as regulatory clarity, balanced pricing, and accountability for carbon emissions, which together will influence product innovation and raw material sourcing in key markets across North America and Europe.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.1 Billion |

| Forecast Value | $106.4 Billion |

| CAGR | 12.1% |

The plant-based milk segment generated USD 21 billion in 2024 and is anticipated to grow at a CAGR of 12.1% between 2025 and 2034. Oat-based beverages currently dominate this segment, appreciated for their mild taste, versatility, and favorable sustainability profile. As consumers explore alternatives beyond soy and almond, ingredients like hemp, coconut, and fava beans are being incorporated into new product lines to expand variety and nutritional value. Brands continue to invest in research and development aimed at improving taste, mouthfeel, and nutrient density to match or surpass dairy equivalents. The evolution of this segment is driving innovation across the wider plant-based dairy industry, enhancing both consumer acceptance and product diversity.

The supermarkets and hypermarkets segment was valued at USD 14.7 billion in 2024 and is expected to grow at a CAGR of 11.1% from 2025 to 2034, representing 43.2% share. These retail outlets dominate distribution due to extensive shelf space and visibility, helping plant-based products reach mainstream consumers. At the same time, specialty and health-food retailers continue to play a crucial role in testing and launching new product formats. As plant-based dairy becomes increasingly normalized, private-label brands are expanding, offering competitively priced alternatives. Convenience stores are also broadening their offerings to meet the growing consumer preference for accessible plant-based options in everyday shopping environments.

Germany Plant-Based Dairy Alternatives Market was valued at USD 1.9 billion in 2024 and is projected to grow at a CAGR of 11.7% through 2034. The country leads in Europe due to strong environmental awareness, widespread adoption of almond and oat-based dairy substitutes, and growing consumer preference for sustainable and locally sourced products. Intense competition among domestic brands and supermarket chains has spurred private-label development and broadened consumer trials, further accelerating market expansion.

Key players operating in the Global Plant-Based Dairy Alternatives Market include Hain Celestial Group, Blue Diamond Growers, Oatly Group AB, Califia Farms, and Danone S.A. Leading companies in the plant-based dairy alternatives market are pursuing innovation, expansion, and collaboration to strengthen their market foothold. They are investing heavily in product research to replicate the texture and nutritional profile of dairy through advanced processing and ingredient optimization. Strategic partnerships with retailers and foodservice chains are helping enhance product visibility and accessibility. Companies are also expanding production capacity and entering new regional markets to meet rising global demand. Diversification into alternative protein sources such as oats, hemp, and fava beans supports supply chain resilience and sustainability goals.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Source

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2025 - 2034 (USD Million, Kilo Tons)

- 5.1 Key trends

- 5.2 Plant-based milk

- 5.2.1 Shelf-stable

- 5.2.2 Refrigerated

- 5.3 Plant-based yogurt

- 5.3.1 Spoonable

- 5.3.2 Drinkable

- 5.4 Plant-based cheese

- 5.4.1 Block & wheel

- 5.4.2 Shredded & grated

- 5.4.3 Sliced

- 5.4.4 Cream-cheese & spreads

- 5.4.5 Food-service analogues

- 5.5 Plant-based ice cream & frozen dessert

- 5.5.1 Pints & tubs

- 5.5.2 Novelties

- 5.6 Plant-based butter & spreads

- 5.6.1 Stick / block

- 5.6.2 Soft-tub spreads

- 5.7 Creamers

- 5.7.1 Refrigerated liquid

- 5.7.2 Shelf-stable liquid

- 5.7.3 Powdered

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Source, 2025 - 2034 (USD Million, Kilo Tons)

- 6.1 Key trends

- 6.2 Soy

- 6.3 Almond

- 6.4 Oat

- 6.5 Coconut

- 6.6 Hemp

- 6.7 Mixed / blended bases

- 6.8 Novel proteins

- 6.8.1 Faba bean

- 6.8.2 Flaxseed

- 6.8.3 Quinoa

- 6.8.4 Other proteins

Chapter 7 Market Estimates and Forecast, By Distribution channel, 2025 - 2034 (USD Million, Kilo Tons)

- 7.1 Key trends

- 7.2 Supermarkets & hypermarkets

- 7.3 Convenience & grocery stores

- 7.4 Specialty & health-food stores

- 7.5 Online retail / DTC

- 7.6 Food-service

- 7.7 Industrial / B2B ingredients

Chapter 8 Market Estimates and Forecast, By Region, 2025 - 2034 (USD Million, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Blue Diamond Growers

- 9.2 Califia Farms

- 9.3 Danone S.A.

- 9.4 Earth’s Own Food Company Inc.

- 9.5 Eden Foods, Inc.

- 9.6 Elmhurst 1925

- 9.7 Good Karma Foods

- 9.8 Happy Planet Foods

- 9.9 Hain Celestial Group

- 9.10 Nestle S.A.

- 9.11 Oatly Group AB

- 9.12 Pacific Foods of Oregon, LLC

- 9.13 Ripple Foods

- 9.14 SunOpta Inc.

- 9.15 The Coca-Cola Company (Fairlife/Simply platforms)

- 9.16 The Hain Celestial Group

- 9.17 The Hershey Company (via SOFIT)

- 9.18 TurtleTree

- 9.19 Valio Ltd

- 9.20 Yili Group

乳製品替代品市場規模、佔有率、成長率和全球市場分析:按類型、應用和地區分類,並提供 2026-2034 年的洞察和預測全球乳製品替代品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

乳製品替代品市場規模、佔有率、成長率和全球市場分析:按類型、應用和地區分類,並提供 2026-2034 年的洞察和預測全球乳製品替代品市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 乳製品替代品市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)

乳製品替代品市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年) 乳製品替代品和植物來源乳製品市場預測至2032年:按產品類型、成分、配方、分銷管道、應用和地區分類的全球分析乳製品替代品和純素產品市場預測至2032年:按產品、成分、價格分佈、配方類型、分銷管道、最終用戶和地區分類的全球分析大豆基乳製品替代品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2024-2032)全球植物性發酵乳製品市場:預測至2032年-按產品類型、配料、發酵類型、包裝、分銷管道、最終用戶和地區進行分析2032 年富含益生菌的乳製品替代品市場預測:按產品、菌株類型、來源、應用、最終用戶和地區進行的全球分析2032 年植物性乳製品替代品市場預測:按產品類型、來源、配方、性質、分銷管道、應用、最終用戶和地區進行的全球分析乳製品替代品市場:2025-2030 年預測

乳製品替代品和植物來源乳製品市場預測至2032年:按產品類型、成分、配方、分銷管道、應用和地區分類的全球分析乳製品替代品和純素產品市場預測至2032年:按產品、成分、價格分佈、配方類型、分銷管道、最終用戶和地區分類的全球分析大豆基乳製品替代品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2024-2032)全球植物性發酵乳製品市場:預測至2032年-按產品類型、配料、發酵類型、包裝、分銷管道、最終用戶和地區進行分析2032 年富含益生菌的乳製品替代品市場預測:按產品、菌株類型、來源、應用、最終用戶和地區進行的全球分析2032 年植物性乳製品替代品市場預測:按產品類型、來源、配方、性質、分銷管道、應用、最終用戶和地區進行的全球分析乳製品替代品市場:2025-2030 年預測