|

市場調查報告書

商品編碼

2073234

中東農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East Agricultural Sprayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

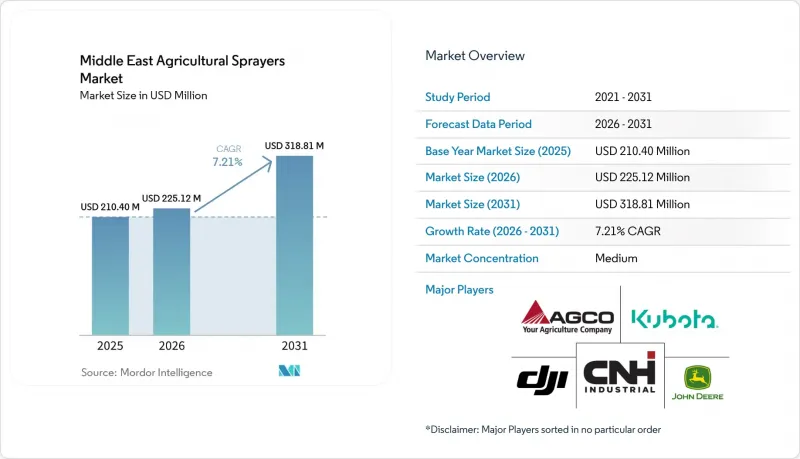

根據 Mordor Intelligence 預測,中東農業噴霧器市場規模將從 2025 年的 2.104 億美元和 2026 年的 2.2512 億美元成長到 2031 年的 3.1881 億美元,2026 年至 2031 年的複合年成長率為 7.21%。

本報告按動力來源(手動、太陽能等)、產品類型(手持式、曳引機式等)、應用領域(農地作物、果園/葡萄園等)、技術水準(傳統、精準噴灑/GPS導航等)和地區(沙烏地阿拉伯、阿拉伯聯合大公國等)進行分類。市場預測以以金額為準呈現。

中東農業噴霧器市場趨勢與洞察

在缺水農場引進精準噴灑技術

淡水資源短缺仍然是中東農業噴霧器市場最強勁的商業性促進因素之一。這是因為該地區的生產者無法將噴灑用水視為低成本投入。根據提交的草案,該地區各國面臨極端的水資源壓力,在此背景下,精準噴灑不僅是一項高階功能,更是一種切實可行的操作方案。草案指出,精密農業可以減少每個種植週期20%至30%的用水量和25%的肥料用量,從而縮短水資源緊張的農場的投資回收期。這在沙烏地阿拉伯尤其重要,因為該國的糧食自給自足目標與提高生產效率息息相關,農場面臨著透過合理管理投入來提高產量的壓力。噴灑區域的均勻性至關重要,因為在乾旱的生產系統中,由於噴灑區域重疊、徑流和漂移造成的浪費比在水資源豐富的農業區成本更高。因此,中東地區的農業噴霧器市場正從單純關注機械可靠性和補貼資格,轉向關注能夠在農場層級帶來可衡量農業效益的設備。這有利於那些能夠將噴霧器性能與投入成本節約相結合、確保作物得到持續保護並最大限度減少噴灑期間人為干預的供應商。

擴大果園和溫室作物種植面積

溫室和果園的擴張正在中東農業噴霧器市場催生獨特的需求模式,因為與大田間作物相比,這些作物需要更精準、更可控的噴灑。根據提交的草案,沙烏地阿拉伯計劃在2023年至2025年間建造100多座高科技溫室,建設資金來自高科技基礎建設農業發展基金。在商業性,封閉式種植的生產者越來越需要緊湊型系統、低漂移噴灑、冠層穿透能力以及與施肥和灌溉等作物管理方案的兼容性,而不是大型臂架式設備。阿拉伯聯合大公國(阿拉伯聯合大公國)在其糧食安全戰略下也採取了類似的策略,推廣精密農業和可控環境農業,以增強當地在惡劣氣候條件下的生產能力。這正在改變市場上的產品組合,因為溫室和果園經營者往往更重視精準性、殘留物控制和作物安全,而非僅僅關注藥罐容量。此外,氣吹式噴灑系統、機器人平台和專用噴嘴的重要性也得到了強調,它們可用於高價值的園藝應用,且不會影響作物品質。因此,此因素推動了此類設備需求量和價值的成長,因為專用園藝噴灑器的價格通常高於標準田間設備,且對維護保養的要求也更為嚴格。

噴灑高峰期電池壽命受限

電池容量的限制仍然是中東農業噴霧器市場的一大限制。這是因為高溫環境會縮小電動和無人機平台的運作舒適度。根據提交的草案,該地區夏季田間溫度在噴灑高峰期經常超過攝氏40度C,直接影響鋰離子電池系統的有效負載容量和飛行時間。草案指出,沙烏地阿拉伯的作業人員在夏季噴灑作業期間,每次更換電池都必須忍受30至45分鐘的作業中斷,導致作物保護的關鍵時期作業效率下降。即使是像大疆創新(DJI Technology)的Agras T100這樣的先進平台,儘管其有效載荷能力遠高於舊款機型,也必須運作溫度控管的限制。實際上,儘管一些農場正在試用新型電動系統,但這種限制意味著燃油驅動和曳引機式噴霧器在各種作業中仍然發揮著重要作用。因此,中東農業噴霧器市場的發展趨勢是技術混合,而不是快速單向地轉向電池驅動平台。在能量密度、充電物流和耐熱性進一步提高之前,運作時間的限制將繼續限制全部區域電動噴霧器的部署速度。

細分市場分析

到2025年,燃油動力噴霧器將佔據中東農業噴霧器市場46.2%的佔有率。這得歸功於其作業範圍廣、運作時間長、用途廣泛,使其非常適合在沙烏地阿拉伯和阿拉伯聯合大公國廣袤的農田上作業。這一主導地位表明,傳統動力系統仍然能夠很好地滿足該地區主要農業區的規模和工作量需求。電池動力、太陽能動力和手動噴霧器雖然市場佔有率較小,但在溫室、偏遠農田以及尚未完全機械化的農場等特定應用場景中仍有應用。

預計從2026年到2031年,太陽能噴霧器將以8.2%的複合年成長率高速成長,這反映出它們適用於離網園藝以及不宜使用柴油燃料的地區。中東農業噴霧器市場正在推動這一轉變,因為該地區日照充足,且乾旱地區對低能耗噴灑方式的需求量很大。在排放氣體和噪音問題更為突出的封閉迴路境中,電池驅動系統也越來越受歡迎。雖然小規模農戶仍將繼續使用手動噴霧器,但燃油驅動的噴霧器預計仍將是高效處理大面積農田的主要工具。

預計到2025年,曳引機式噴霧器將佔中東農業噴霧器市場41.4%的銷量,成為該市場中按產品類型分類的最大市場佔有率。這一主導地位反映了機械化農業在主要農業區糧食和農作物種植中持續的重要性。牽引式和自走式噴霧器廣泛應用於商業農場,因為這些農場對藥箱容量和噴桿控制要求較高;而手持式噴霧器在當地園藝和果園維護中的作用相對較小。

預計2026年至2031年間,無人機(UAV)噴灑器將以每年9.8%的速度成長,成為中東農業噴灑器市場成長最快的產品系列。大疆創新科技(DJI Technology)在2025年下半年透過推出Agras T100平台並拓展分銷網路,進一步鞏固了該品類的地位。服務車隊模式也推動了市場成長,該模式允許有組織的營運商批量採購,從而更有效率地噴灑難以到達的區域。預計曳引機式噴灑器仍將維持銷售量基礎。然而,無人機系統正在改變商業噴灑能力建構的方式。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在缺水農場引進精準噴灑技術

- 擴大果園和溫室作物種植面積

- 特種作物無人機服務機隊採用現狀

- 政府對糧食安全和機械化的誘因

- 對可變施肥量套件和 GPS 套件的改造需求。

- 高價值出口作物對低漂移噴灑的需求

- 市場限制因素

- 噴灑尖峰時段電池續航力受限

- 精密系統和無人機系統熟練操作人員短缺

- 關鍵零件高度依賴進口

- 農場間售後服務網路取得上的差異

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過動力來源

- 手動的

- 電池供電

- 太陽能

- 燃油驅動

- 依產品類型

- 手持式

- 聯結機式

- 拖著

- 自推進式

- 無人機噴灑器

- 透過使用

- 田間作物

- 果園和葡萄園

- 溫室種植的作物

- 草坪和園藝

- 按技術水準

- 傳統的

- 高精度和GPS導

- 人工智慧賦能與自主

- 按地區

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deere and Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- DJI Technology Co., Ltd.

- Yamaha Motor Co., Ltd.

- EXEL Industries

- Amazonen-Werke H. Dreyer SE and Co. KG

- Kuhn Group

- Mahindra & Mahindra Ltd.

- HORSCH

- STIHL Holding AG and Co. KG

- ISEKI & CO.,LTD.

- Ecorobotix SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east agricultural sprayers market size is projected to expand from USD 210.40 million in 2025 and USD 225.12 million in 2026 to USD 318.81 million by 2031, growing at an estimated CAGR of 7.21% during 2026-2031.

This report is Segmented by Source of Power (Manual, Solar-Powered, and More), by Product Type (Handheld, Tractor-Mounted, and More), by Application (Field Crops, Orchards and Vineyards, and More), by Technology Level (Conventional, Precision and GPS Guided, and More), and by Geography (Saudi Arabia, United Arab Emirates, and More). The Market Forecasts are Provided in Terms of Value.

Middle East Agricultural Sprayers Market Trends and Insights

Precision Spraying Adoption in Water-Scarce Farms

Freshwater scarcity remains one of the strongest commercial forces driving the Middle East agricultural sprayers market, as growers in the region cannot treat spray water as a low-cost input. The supplied draft states that countries in the region face extreme water stress, and that backdrop makes precision application a practical operating choice rather than a premium feature. The same draft notes that precision agriculture can reduce water use by 20% to 30% and fertilizer use by 25% per crop cycle, thereby improving payback periods for farms managing tight water budgets. This is especially relevant in Saudi Arabia, where food self-sufficiency targets are tied to higher production efficiency, and farms are under pressure to increase output through better input control. Uniformity of spray coverage matters because waste from overlap, runoff, and drift is more costly in arid production systems than in water-abundant agricultural zones. The Middle East agricultural sprayers market is therefore shifting toward equipment that delivers measurable agronomic returns at the farm level, not just mechanical reliability or subsidy eligibility. This benefits suppliers capable of linking sprayer performance to input savings, ensuring consistent crop protection and minimizing labor intervention during application windows.

Orchard and Greenhouse Crop Expansion

Greenhouse expansion and orchard development are creating a distinct demand pattern in the Middle East agricultural sprayers market, as these crops require more controlled, targeted spray applications than broadacre field crops. The supplied draft states that Saudi Arabia installed more than 100 high-tech greenhouses between 2023 and 2025, and that this buildout was supported by Agricultural Development Fund financing for high-tech infrastructure. The commercial meaning is that growers in confined environments increasingly need compact systems, low-drift delivery, canopy penetration, and compatibility with fertigation-linked crop programs rather than large boom equipment. The United Arab Emirates is moving along a similar path under its food security strategy, where precision agriculture and controlled-environment farming are being promoted to strengthen local production under extreme climatic limits. This changes the product mix in the market because greenhouse and orchard operators often prioritize accuracy, residue control, and crop safety over tank size alone. It also underscores the relevance of air-blast systems, robotic platforms, and specialized nozzles that can operate in high-value horticulture without compromising crop quality. As a result, this driver supports both unit demand and value growth, as specialized horticulture spraying equipment typically commands a higher selling price and more stringent service requirements than standard field units.

Limited Battery Runtime During Peak Spray Windows

Battery limitations remain a practical brake on the Middle East agricultural sprayers market because high ambient temperatures reduce the operating comfort margin for electric and drone-based platforms. The supplied draft states that summer field conditions in the region regularly exceed 40°C during peak spray windows, and that this directly affects effective payload and flight duration in lithium-ion systems. The same draft notes that operators in Saudi Arabia can experience 30 to 45 minutes of interruption per battery-swap cycle during summer applications, reducing throughput when crop-protection timing is tight. Even advanced platforms such as DJI Technology Co., Ltd.'s Agras T100 still have to operate within thermal management limits despite much higher payload capability than earlier models. In practice, the limitation keeps fuel-operated and tractor-mounted systems relevant for large-area work even as farms test newer electric formats. The Middle East agricultural sprayers market, therefore, develops as a mixed-technology market rather than a rapid one-way shift to battery platforms. Until energy density, charging logistics, and heat resilience improve further, runtime limits will continue to constrain the pace of adoption of electrified spraying across the region.

Other drivers and restraints analyzed in the detailed report include:

- Drone Service Fleet Penetration in Specialty Crops

- Government Food Security and Mechanization Incentives

- Skilled Operator Shortage for Precision and Drone Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fuel-operated sprayers held 46.2% of the Middle East agricultural sprayers market share in 2025, supported by their range, runtime, and suitability for large-field operations in Saudi Arabia and the United Arab Emirates. This leadership shows that conventional power systems still fit the scale and workload of the region's main farming belts. Battery-operated, solar-powered, and manual systems remained smaller, but they served distinct use cases in greenhouses, remote plots, and low-mechanization farms.

Solar-powered sprayers are anticipated to post the fastest 8.2% CAGR during 2026-2031, reflecting their suitability for off-grid horticulture and areas where handling diesel is less attractive. The Middle East agricultural sprayers market is supporting this shift because the region has high solar irradiance and a growing need for low-energy spraying options in arid zones. Battery systems are also gaining traction in enclosed environments where emissions and noise matter more. Manual units should persist among smallholders, while fuel-operated machines are likely to remain central for high-throughput field coverage.

Tractor-mounted sprayers accounted for 41.4% of revenue in 2025, giving them the largest share in the Middle East agricultural sprayers market across product types. Their lead reflects the continued role of mechanized cereal and row-crop farming in major agricultural zones. Trailed and self-propelled units also served commercial farms that value tank capacity and boom control, while handheld systems maintained a smaller role in localized horticulture and orchard maintenance.

Unmanned aerial vehicle sprayers are anticipated to expand at a 9.8% during 2026-2031, making them the fastest-growing product group in the Middle East agricultural sprayers market. DJI Technology Co., Ltd. strengthened this category through the Agras T100 platform and wider dealer availability in late 2025. Growth is also supported by service fleet models that enable organized operators to buy in bulk and spray hard-to-access plots more efficiently. Tractor-mounted units are estimated to continue anchoring volume. However, unmanned aerial vehicle systems are transforming the approach to building commercial spraying capacity.

Complete Report Scope:

- By Source of Power

- Manual

- Battery-Operated

- Solar-Powered

- Fuel-Operated

- By Product Type

- Handheld

- Tractor-Mounted

- Trailed

- Self-Propelled

- Unmanned Aerial Vehicle Sprayers

- By Application

- Field Crops

- Orchards and Vineyards

- Greenhouse Crops

- Turf and Gardening

- By Technology Level

- Conventional

- Precision and GPS Guided

- AI-Enabled and Autonomous

- By Geography

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

List of Companies Covered in this Report:

- Deere and Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- DJI Technology Co., Ltd.

- Yamaha Motor Co., Ltd.

- EXEL Industries

- Amazonen-Werke H. Dreyer SE and Co. KG

- Kuhn Group

- Mahindra & Mahindra Ltd.

- HORSCH

- STIHL Holding AG and Co. KG

- ISEKI & CO.,LTD.

- Ecorobotix SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision Spraying Adoption in Water-Scarce Farms

- 4.2.2 Orchard and Greenhouse Crop Expansion

- 4.2.3 Drone Service Fleet Penetration in Specialty Crops

- 4.2.4 Government Food Security and Mechanization Incentives

- 4.2.5 Retrofit Demand for Variable-Rate and GPS Kits

- 4.2.6 Demand for Low-Drift Application in High-Value Export Crops

- 4.3 Market Restraints

- 4.3.1 Limited Battery Runtime During Peak Spray Windows

- 4.3.2 Skilled Operator Shortage for Precision and Drone Systems

- 4.3.3 High Import Dependence for Core Components

- 4.3.4 Uneven Farm-Level Access to After-Sales Service Networks

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Source of Power

- 5.1.1 Manual

- 5.1.2 Battery-Operated

- 5.1.3 Solar-Powered

- 5.1.4 Fuel-Operated

- 5.2 By Product Type

- 5.2.1 Handheld

- 5.2.2 Tractor-Mounted

- 5.2.3 Trailed

- 5.2.4 Self-Propelled

- 5.2.5 Unmanned Aerial Vehicle Sprayers

- 5.3 By Application

- 5.3.1 Field Crops

- 5.3.2 Orchards and Vineyards

- 5.3.3 Greenhouse Crops

- 5.3.4 Turf and Gardening

- 5.4 By Technology Level

- 5.4.1 Conventional

- 5.4.2 Precision and GPS Guided

- 5.4.3 AI-Enabled and Autonomous

- 5.5 By Geography

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Deere and Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 DJI Technology Co., Ltd.

- 6.4.6 Yamaha Motor Co., Ltd.

- 6.4.7 EXEL Industries

- 6.4.8 Amazonen-Werke H. Dreyer SE and Co. KG

- 6.4.9 Kuhn Group

- 6.4.10 Mahindra & Mahindra Ltd.

- 6.4.11 HORSCH

- 6.4.12 STIHL Holding AG and Co. KG

- 6.4.13 ISEKI & CO.,LTD.

- 6.4.14 Ecorobotix SA

7 Market Opportunities and Future Outlook

農業噴霧器市場:2026-2032年全球市場預測(按推進方式、類型、容量、應用、最終用戶和分銷管道分類)

農業噴霧器市場:2026-2032年全球市場預測(按推進方式、類型、容量、應用、最終用戶和分銷管道分類) 德國農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)農業噴霧:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

德國農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)農業噴霧:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 農業噴霧器市場機會、成長要素、產業趨勢分析及2026-2035年預測。農業噴霧器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

農業噴霧器市場機會、成長要素、產業趨勢分析及2026-2035年預測。農業噴霧器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 農業噴霧器市場:按產品類型、動力來源、應用、噴霧能力和地區分類。

農業噴霧器市場:按產品類型、動力來源、應用、噴霧能力和地區分類。 全球電池驅動背包式噴霧器市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球電池驅動背包式噴霧器市場規模、佔有率、趨勢和成長分析報告(2026-2034) 農業噴霧器市場規模、佔有率、趨勢和預測:按類型、動力來源、應用和地區分類,2026-2034年電動熱霧發生器市場:依解決方案類型、運作模式、電源、應用和最終用戶分類-全球預測,2026-2032年

農業噴霧器市場規模、佔有率、趨勢和預測:按類型、動力來源、應用和地區分類,2026-2034年電動熱霧發生器市場:依解決方案類型、運作模式、電源、應用和最終用戶分類-全球預測,2026-2032年 2026年全球霧化機市場報告

2026年全球霧化機市場報告