|

市場調查報告書

商品編碼

2072817

農業噴霧:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Agricultural Fogging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

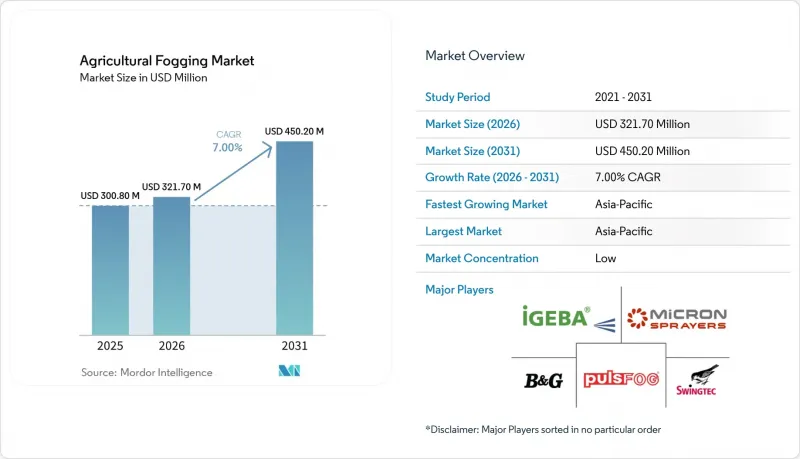

據 Mordor Intelligence 稱,2025 年農業噴霧市場價值為 3.008 億美元,預計將從 2026 年的 3.217 億美元成長到 2031 年的 4.502 億美元,在 2026 年至 2031 年的預測期內,複合年成長率將達到 7.0%。

本報告按機器類型(例如,熱噴霧器)、動力來源(燃油動力、有線動力、電池動力)、應用領域(例如,作物保護和病害控制、溫室和苗圃衛生管理)以及地區(北美、南美、歐洲、亞太地區、中東和非洲)進行細分。市場預測以美元(USD)計價。

全球農業噴霧市場趨勢及洞察

對精準病蟲害防治的需求

由於對精準病蟲害防治的需求不斷成長,農業噴灑市場正在蓬勃發展。噴灑覆蓋的品質顯著影響莓果、保護地蔬菜、柑橘類水果和觀賞植物等作物的防治效果。 2024年發表於國際農業與生物科學中心(CABI)期刊《農業與生物科學》的一項研究表明,在相同的操作條件下,靜電噴霧在葉片上表面的附著率達到327個沉積物/平方厘米,而傳統噴霧系統僅為102個沉積物/平方厘米。這種高附著效率正推動靜電噴霧和冷霧系統在綜合蟲害管理方案中的應用,因為種植者希望提高藥效穿透冠層的能力,減少農藥浪費,並獲得更穩定的噴灑效果。

擴大溫室和保護性栽培

保護性栽培是農業噴霧市場的主要驅動力。這是因為溫室栽培在每個生長週期都需要定期消毒、作物處理和環境控制。根據《國際農學研究雜誌》2025年發表的綜述,中國將引領保護性栽培面積的發展,預計2024年將達到276萬公頃。隨著溫室基礎設施的擴張,用於作物保護、濕度控制和病害防治的噴霧系統需求顯著成長。擁有全面產品系列且專注於溫室領域的供應商正受益於保護性栽培的加強以及商業園藝企業生產週期的增加。

商用系統的初始成本和維護成本都很高。

高昂的初始成本和維護費用仍是農業噴灑市場推廣應用的主要障礙,尤其對面臨資金限制的中小型農場而言,更構成重大挑戰。根據美國農業部經濟研究局預測,農業部門的總生產成本預計將從2025年的4,731億美元增加到2026年的4,777億美元。不斷上漲的營運成本限制了生產者投資先進噴灑系統的能力,而這些系統需要額外的燃料、維護、備件和化學品處理基礎設施的支出。因此,對成本較為敏感的農場正在經歷設備更換週期延長的困境。

細分市場分析

到2025年,熱噴灑器將佔據農業噴灑市場最大的佔有率,達到38.5%。由於其在露天作物病蟲害防治、牲畜棚舍和倉儲設施的衛生管理以及需要高密度霧化滲透和廣域覆蓋的大規模應用,這些系統的需求仍然強勁。成熟的供應鏈、操作人員的熟悉程度以及相對較低的設備成本正在推動其普及,尤其是在農業發展中國家。燃油動力熱噴灑系統尤其適用於對移動性和處理速度要求極高的戶外和大批量作業。此類別產品也因其在傳統農業病蟲害防治實踐中的廣泛應用而持續受益。

在農業噴灑市場中,低溫噴霧器市場預計將以最高的複合年成長率(CAGR)成長,2026年至2031年間將達到8.1%。由於低溫噴霧器系統與水性配方和生物來源農作物保護產品相容,且能夠精確控制液滴分佈,因此其應用日益廣泛,尤其是在溫室和園藝領域。種植者青睞低溫噴霧器,因為它能夠確保精準的附著力,最大限度地減少化學廢料,並有效管理殘留物。此外,靜電噴霧技術透過提高冠層穿透性和噴霧均勻性,正在加速其在精準農業環境中的應用。向永續作物保護方案的轉變以及對生物來源材料相容性的日益成長的需求,將繼續推動商業農業對先進低溫噴霧系統的需求。

區域分析

預計到2025年,亞太地區將佔據農業噴灑市場42.3%的佔有率,並將在2026年至2031年間以7.5%的複合年成長率保持最高增速。該地區持續推動市場需求,主要得益於中國、印度和東南亞地區溫室和機械化作物保護技術的快速發展。隨著溫室基礎設施的不斷完善,整個商業園藝產業對用於作物保護、衛生管理和環境管理的農業噴灑系統的需求也不斷成長。

北美和歐洲在農業噴灑系統方面仍處於技術領先地位,種植者越來越重視精準噴灑和殘留控制。這些地區的商業溫室經營者和特種作物種植者持續採用先進的噴灑系統,這些系統支援可控液滴噴灑並與生物藥品相容。此外,更嚴格的農藥施用方法和工人安全要求法律規範也促進了這些地區使用具有更佳操作控制的校準噴灑技術。

歐洲是農業噴灑系統的主要成長區域,這主要得益於溫室種植的持續擴張以及生物防治技術在商業園藝中的應用。根據荷蘭統計局預測,到2024年,荷蘭94.4%的溫室種植面積將使用生物防治劑。隨著生物防治的日益普及,對能夠控制液滴分佈並確保溫室蔬菜、花卉和育苗系統均勻噴灑的精準噴灑系統的需求也日益成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對精準病蟲害防治的需求

- 擴大溫室和大棚種植

- 機械化可以彌補農業勞動力短缺的問題。

- 需要減少農藥的使用量,並提高噴灑的均勻性。

- 遠端操作和自動噴灑在遵守重新進入間隔和工人接觸限制方面具有優勢。

- 擴大生物農藥和水性製劑在高附加價值園藝領域的應用。

- 市場限制因素

- 專業系統的初始成本和維護成本都很高。

- 加強對農藥使用和殘留的監管

- 由於與熱源和配方不相容,某些活性成分在熱激活產品中的使用受到限制。

- 溫室對氣密性、通風和水滴控制的要求,增加了小規模生產者破產的風險。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按機器類型

- 熱噴塗機

- 低溫噴塗機

- 靜電噴霧器

- 透過動力來源

- 燃油驅動

- 有線電氣

- 電池供電

- 透過使用

- 作物保護與病害管理

- 溫室和育苗設施的衛生管理

- 儲存和採後保護

- 畜禽舍的衛生管理

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 法國

- 義大利

- 西班牙

- 英國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 印尼

- 泰國

- 其他亞太國家

- 中東

- 土耳其

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 摩洛哥

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IGEBA Geratebau GmbH

- B&G Equipment Company, Inc.(Pelsis Group)

- pulsFOG Dr. Stahl & Sohn GmbH

- Swingtec GmbH

- Micron Sprayers Limited(Goizper Group)

- VectorFog Electronic Corporation

- Martignani Srl

- TIFONE Srl

- Shouguang Jiafu Agricultural Machinery Co., Ltd.

- UNA Corporation

- HARDI INTERNATIONAL A/S

- Vectorfog(Vectornate Inc.)

- Shenzhen Longray Technology Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the agricultural fogging market size was valued at USD 300.80 million in 2025 and is projected to grow from USD 321.70 million in 2026 to USD 450.20 million by 2031, registering a CAGR of 7.0% during the forecast period from 2026 to 2031.

This report is Segmented by Machine Type (Thermal Fogging Machines and More), by Power Source (Fuel-Powered, Electric Corded, and Battery-Powered), by Application (Crop Protection and Disease Management, Greenhouse and Nursery Sanitation, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Agricultural Fogging Market Trends and Insights

Precision Pest and Disease Control Demand

The agricultural fogging market is experiencing growth due to the rising demand for precision pest and disease control in crops such as berries, protected vegetables, citrus, and ornamental plants, where the quality of spray coverage significantly impacts treatment effectiveness. A 2024 study published in the Centre for Agriculture and Bioscience International (CABI) Agriculture and Bioscience journal highlighted that electrostatic spraying achieved 327 deposits/cm2 on adaxial leaf surfaces, compared to 102 deposits/cm2 with conventional spraying systems under identical operating conditions. This higher deposition efficiency is driving the adoption of electrostatic and cold fogging systems, as growers aim for improved canopy penetration, reduced chemical wastage, and more consistent application performance within integrated pest management programs.

Expansion of Greenhouse and Protected Cultivation

Protected cultivation is a key driver for the agricultural fogging market, as greenhouse production necessitates regular sanitation, crop treatment, and environmental control during each growing cycle. According to a 2025 review published in the International Journal of Research in Agronomy, China led the protected cultivation area, reaching 2.76 million hectares in 2024. The expansion of greenhouse infrastructure has significantly increased the demand for fogging systems used in crop protection, humidity management, and disease control. Suppliers with robust greenhouse-focused product portfolios are benefiting from the growing intensity of protected cultivation and the rising frequency of production cycles in commercial horticulture operations.

High Upfront and Maintenance Costs for Professional Systems

High upfront and maintenance costs remain a significant barrier to adoption in the agricultural fogging market, particularly for small- and medium-scale farming operations facing financial constraints. According to the United States Department of Agriculture Economic Research Service, total farm sector production expenses are projected to rise from USD 473.1 billion in 2025 to USD 477.7 billion in 2026. Increasing operating costs are limiting growers' capacity to invest in advanced fogging systems, which require additional expenditures on fuel, maintenance, spare parts, and chemical handling infrastructure. Consequently, equipment replacement cycles are slower in cost-sensitive agricultural operations.

Other drivers and restraints analyzed in the detailed report include:

- Mechanization to Offset Farm Labor Shortages

- Need to Reduce Chemical Volume and Improve Coverage Consistency

- Tightening Pesticide-Use and Residue Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The agricultural fogging market share for thermal fogging machines held the largest 38.5% in 2025. These systems maintain strong demand due to their extensive use in open-field crop protection, livestock buildings, storage sanitation, and large-scale agricultural treatments requiring dense fog penetration and broad-area coverage. Factors such as an established supply chain, operator familiarity, and relatively lower equipment costs support their adoption, particularly in developing agricultural economies. Fuel-based thermal systems are especially suitable for outdoor and high-throughput applications where mobility and treatment speed are critical. This category continues to benefit from its widespread application in conventional agricultural pest and disease management practices.

The agricultural fogging market size for cold fogging machines is projected to advance at the fastest 8.1% CAGR from 2026 to 2031. These systems are increasingly adopted due to their compatibility with water-based formulations, biological crop protection products, and controlled droplet application, particularly in greenhouse and horticulture operations. Growers favor cold fogging machines for their ability to ensure precise deposition, minimize chemical wastage, and manage residues effectively. Additionally, electrostatic fogging technologies are driving adoption in precise cultivation environments by enhancing canopy penetration and application consistency. The shift toward sustainable crop protection programs and the need for biological-input compatibility continue to drive demand for advanced cold fogging equipment in commercial agriculture.

Complete Report Scope:

- By Machine Type

- Thermal Fogging Machines

- Cold Fogging Machines

- Electrostatic Fogging Machines

- By Power Source

- Fuel-powered

- Electric corded

- Battery-powered

- By Application

- Crop Protection and Disease Management

- Greenhouse and Nursery Sanitation

- Storage and Post-harvest Protection

- Livestock and Poultry House Hygiene

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- France

- Italy

- Spain

- United Kingdom

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- Thailand

- Rest of Asia-Pacific

- Middle East

- Turkey

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Morocco

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific accounted for the largest 42.3% of the agricultural fogging market share in 2025 and is projected to grow at the fastest CAGR of 7.5% from 2026 to 2031. The region continues to lead demand because greenhouse expansion and mechanized crop protection practices are increasing rapidly across China, India, and Southeast Asia. The expanding greenhouse base is strengthening demand for agricultural fogging systems used in crop protection, sanitation, and environmental management across commercial horticulture operations.

North America and Europe continue to represent technologically advanced regions for agricultural fogging systems, where growers increasingly prioritize precision application and residue management. Commercial greenhouse operators and specialty crop growers across these regions continue adopting advanced fogging systems capable of supporting controlled droplet application and biological-input compatibility. The regions also benefit from stronger regulatory oversight related to pesticide application practices and worker-safety requirements, encouraging use of calibrated fogging technologies with improved operational control.

Europe is a key growth region for agricultural fogging systems due to the ongoing expansion of greenhouse cultivation and the adoption of biological crop protection in commercial horticulture. According to Statistics Netherlands, biological pest control agents were utilized in 94.4% of the greenhouse-cultivated area in the Netherlands in 2024. The growing reliance on biological crop protection is driving demand for precision fogging systems that enable controlled droplet application and uniform treatment coverage across greenhouse vegetables, floriculture, and nursery cultivation systems.

- IGEBA Geratebau GmbH

- B&G Equipment Company, Inc. (Pelsis Group)

- pulsFOG Dr. Stahl & Sohn GmbH

- Swingtec GmbH

- Micron Sprayers Limited (Goizper Group)

- VectorFog Electronic Corporation

- Martignani S.r.l.

- TIFONE S.r.l.

- Shouguang Jiafu Agricultural Machinery Co., Ltd.

- UNA Corporation

- HARDI INTERNATIONAL A/S

- Vectorfog (Vectornate Inc.)

- Shenzhen Longray Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision pest and disease control demand

- 4.2.2 Expansion of greenhouse and protected cultivation

- 4.2.3 Mechanization to offset farm labor shortages

- 4.2.4 Need to reduce chemical volume and improve coverage consistency

- 4.2.5 Re-entry interval and worker-exposure compliance favor remote and automated fogging

- 4.2.6 Rising adoption of biopesticides and water-based formulations in high-value horticulture

- 4.3 Market Restraints

- 4.3.1 High upfront and maintenance costs for professional systems

- 4.3.2 Tightening pesticide-use and residue compliance

- 4.3.3 Heat and formulation incompatibility limits some active ingredients in thermal systems

- 4.3.4 Greenhouse sealing, ventilation, and droplet-calibration demands raise failure risk for smaller growers

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Machine Type

- 5.1.1 Thermal Fogging Machines

- 5.1.2 Cold Fogging Machines

- 5.1.3 Electrostatic Fogging Machines

- 5.2 By Power Source

- 5.2.1 Fuel-powered

- 5.2.2 Electric corded

- 5.2.3 Battery-powered

- 5.3 By Application

- 5.3.1 Crop Protection and Disease Management

- 5.3.2 Greenhouse and Nursery Sanitation

- 5.3.3 Storage and Post-harvest Protection

- 5.3.4 Livestock and Poultry House Hygiene

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 Italy

- 5.4.3.4 Spain

- 5.4.3.5 United Kingdom

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 Indonesia

- 5.4.4.6 Thailand

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Turkey

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Morocco

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 IGEBA Geratebau GmbH

- 6.4.2 B&G Equipment Company, Inc. (Pelsis Group)

- 6.4.3 pulsFOG Dr. Stahl & Sohn GmbH

- 6.4.4 Swingtec GmbH

- 6.4.5 Micron Sprayers Limited (Goizper Group)

- 6.4.6 VectorFog Electronic Corporation

- 6.4.7 Martignani S.r.l.

- 6.4.8 TIFONE S.r.l.

- 6.4.9 Shouguang Jiafu Agricultural Machinery Co., Ltd.

- 6.4.10 UNA Corporation

- 6.4.11 HARDI INTERNATIONAL A/S

- 6.4.12 Vectorfog (Vectornate Inc.)

- 6.4.13 Shenzhen Longray Technology Co., Ltd.

7 Market Opportunities and Future Outlook

中東農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中東農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 農業噴霧器市場:2026-2032年全球市場預測(按推進方式、類型、容量、應用、最終用戶和分銷管道分類)德國農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

農業噴霧器市場:2026-2032年全球市場預測(按推進方式、類型、容量、應用、最終用戶和分銷管道分類)德國農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 農業噴霧器市場機會、成長要素、產業趨勢分析及2026-2035年預測。農業噴霧器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

農業噴霧器市場機會、成長要素、產業趨勢分析及2026-2035年預測。農業噴霧器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 農業噴霧器市場:按產品類型、動力來源、應用、噴霧能力和地區分類。

農業噴霧器市場:按產品類型、動力來源、應用、噴霧能力和地區分類。 全球電池驅動背包式噴霧器市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球電池驅動背包式噴霧器市場規模、佔有率、趨勢和成長分析報告(2026-2034) 農業噴霧器市場規模、佔有率、趨勢和預測:按類型、動力來源、應用和地區分類,2026-2034年電動熱霧發生器市場:依解決方案類型、運作模式、電源、應用和最終用戶分類-全球預測,2026-2032年

農業噴霧器市場規模、佔有率、趨勢和預測:按類型、動力來源、應用和地區分類,2026-2034年電動熱霧發生器市場:依解決方案類型、運作模式、電源、應用和最終用戶分類-全球預測,2026-2032年 2026年全球霧化機市場報告

2026年全球霧化機市場報告