|

市場調查報告書

商品編碼

2072897

東南亞農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Southeast Asia Agricultural Sprayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

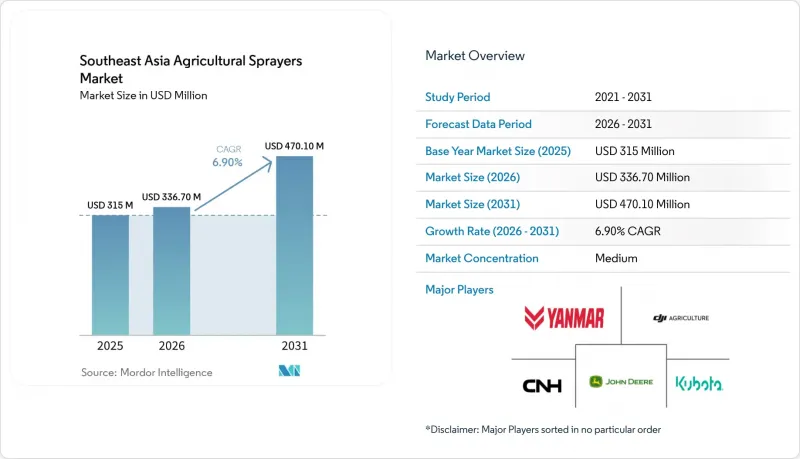

據 Mordor Intelligence 稱,東南亞農業噴霧器市場在 2025 年的價值為 3.15 億美元,預計到 2031 年將達到 4.701 億美元,而 2026 年為 3.367 億美元,預測期(2026-2031 年)的複合年成長率為 6.9%。

本報告按動力來源(例如,手動)、產品類型(例如,手持式)、應用領域(例如,田間作物)、噴灑能力(例如,超低容量系統)、技術水準(例如,傳統技術)、泵機制(例如,隔膜泵)和地區(例如,印尼、越南)進行細分。市場規模以美元(USD)計。

東南亞農業噴霧器市場趨勢與洞察

農業勞動力短缺推高了對機械化噴灑的需求。

東南亞農村勞動力遷移正從短期現象轉變為持續性變化,並改變了農場的噴灑作業方式。在一些國家,由於作物噴灑的窗口期有限,生產者越來越難以找到工人進行重複噴灑作業。手動背負式噴霧器每次噴灑作業可能需要每50公頃3至5名工人,大型農場的勞動力負擔正在迅速加重。因此,勞動力短缺正在改變人們對機械噴霧器的看法,使其不再只是為了方便而購買,而是成為業務運營的必備設備。據印尼和菲律賓的經銷商稱,在高價值作物種植系統中,動力噴霧器的投資回收期已縮短至不到18個月,加快了以往需要數年才能做出的購買決策。這推動了中型農場對曳引機式噴桿噴霧器的需求,以及在土地分散、地形崎嶇、地面交通受限的地區對無人機噴灑服務的需求。因此,東南亞農業噴霧器市場受益於與勞動力替代相關的穩定需求基礎,而不是僅僅由產量提高所驅動的需求。

政府對機械化的補助和資金籌措

公共資金支持計畫正在影響東南亞農場和合作社購買噴霧器的方式。 2025年,菲律賓農業部的「水稻無人機計畫」(Drones4Rice)以公頃為單位的代金券津貼無人機噴灑服務,並提供更廣泛的機械化資金支持精密農業的推廣。在泰國,2025年啟動的「智慧農民計畫」 (舉措)旨在促進現代化,並推廣使用GPS導航噴霧器和農業無人機等精準設備。同樣,印尼2025年啟動的「農業發展基金」(KUR Pertanian)融資計畫旨在減輕小規模農戶和合作社投資農業機械(包括機械化噴灑系統)的經濟負擔。這些計劃不僅降低了初始成本,還透過合格標準優先考慮性能卓越、效率更高、可控性更強、可追溯性更高的設備。因此,補貼和融資政策正在改變東南亞農業噴霧器市場的產品結構,增加對先進噴灑技術的需求。

無人機和動力噴霧器的初始成本很高

高昂的設備成本仍然是東南亞農業噴霧器市場的主要挑戰。有效載荷為20-30公升的商用農業無人機,根據配置、電池和配件的不同,價格在8000美元到20000美元之間。這樣的價格限制了無人機的普及,只有人工林、商業農場和資金雄厚的合作社才能負擔得起。雖然無人機即服務模式有助於降低初始投資,但操作人員仍需要承擔與設備、培訓和維護相關的巨額成本,小規模農戶需要支付高昂的服務費用。因此,儘管先進的噴灑系統在正規農業生產中得到更廣泛的應用,但手動和基礎動力噴霧器在小規模農場仍然佔據主導地位。

細分市場分析

截至2025年,手動噴霧器將佔東南亞農業噴霧器市場44%的佔有率,但預計電池驅動噴霧器將以11.3%的年複合成長率(CAGR)實現最快成長,直至2031年。手動噴霧器價格實惠,尤其是在土地面積小規模的農場,因此仍被廣泛使用。此外,由於其易於維修且所需的支援基礎設施極少,手動噴霧器在經銷商網路有限的農村地區也顯得尤為重要。這些因素意味著,即使先進產品日益普及,手動噴霧器在東南亞農業噴霧器市場的各個細分市場仍將繼續發揮重要作用。

由於鋰離子電池成本下降、運作時間延長以及多個國家農村電力供應趨於穩定,電池驅動噴霧器越來越受歡迎。這一趨勢在泰國和越南尤為明顯,兩國透過公共採購舉措和低排放農業計畫推動了電動工具的普及。同時,太陽能噴霧器正逐漸成為小規模山坡和梯田農業作業的理想解決方案。在人工林和農田作物中,由於需要更長的運作時間和更大的儲液罐容量,燃油驅動系統仍然被廣泛使用。這種多樣化的選擇表明,東南亞農業噴霧器市場並未完全拋棄傳統動力系統,而是在保留現有手動噴霧器用戶群的同時,不斷引入新的動力形式。

對於分散的農地而言,手持式噴霧器仍然是最經濟實用的選擇,推動了產品需求,預計到2025年將佔47%的市場。這一強勁勢頭反映了該地區農業仍面臨土地、資金和基礎設施的許多限制。因此,即使更先進的系統發展迅速,手持式設備的銷售量預計仍將保持穩定。由此可見,東南亞農業噴霧器市場將繼續受益於龐大且低成本的現有用戶群。

預計到2031年,無人機(UAV)噴灑器將以14.2%的複合年成長率成長,成為市場上成長最快的產品類型。這一成長主要得益於無人機即服務(Drone-as-a-Service)網路的推動,該網路降低了農場空中噴灑的高昂成本,尤其對於那些不具備自有設備成本效益的農場而言。 2026年5月,大疆創新(DJI)在曼谷舉行的2026年亞洲國際人工林機械展覽會(AGRITECHNICA Asia 2026)上推出了Agras T55和Agras T100雙電池噴灑系統,有效載荷達50升,從而將無人機的應用場景拓展至大型農場和種植園。在中大型農場,由於需要穩定的噴桿噴灑範圍和較高的日常工作效率,曳引機式、牽引式和自走式噴灑器仍然被廣泛使用。未來,隨著買家不僅比較機械的價格,還比較人事費用的降低、更快的工作速度和服務的可用性,先進地面系統和無人機(UAV)之間的重疊預計將進一步擴大。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 由於農業勞動力短缺,對機械化噴灑的需求不斷增加。

- 政府對機械化的補貼和貸款

- 精密農業和投入效率的需求

- 保護棕櫚油和水稻作物正在推動穩定的需求。

- 在低排放量水稻種植專案中,建議制定準確的噴灑計劃。

- 無人機外包服務網路的擴展

- 市場限制因素

- 無人機和動力噴霧器的初始成本很高

- 小規模農戶擁有的土地分散,限制了土地的利用。

- 適用於無人機的農藥配方仍然有限。

- 有關飛行許可和有效載荷的規定正在延誤現場作業。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 透過動力來源

- 手動輸入

- 電池供電

- 太陽能供電

- 燃油驅動

- 依產品類型

- 手持式

- 聯結機式

- 拖著

- 自推進式

- 無人機噴灑器

- 透過使用

- 田間作物

- 果園和葡萄園

- 溫室種植的作物

- 草坪和園藝

- 按噴霧量

- 超低容量系統

- 低容量系統

- 高容量系統

- 按技術水準

- 傳統的

- 高精度和GPS導

- 配備人工智慧(AI)且自主運作

- 泵浦機構

- 隔膜泵

- 活塞泵

- 離心式幫浦

- 國家

- 印尼

- 越南

- 泰國

- 菲律賓

- 馬來西亞

- 柬埔寨

- 緬甸

- 新加坡

- 東南亞其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- KUBOTA Corporation

- Deere and Company

- CNH Industrial NV

- Yanmar Holdings Co., Ltd.

- DJI Agriculture

- XAG Co., Ltd.

- Terra Drone Corporation

- STIHL Holding AG & Co. KG

- AGCO Corporation

- Jacto Inc.

- HARDI International A/S

- EXEL Industries

- Micron Sprayers Ltd.

- ASPEE Agro Equipment Pvt. Ltd.

- Goizper Group

- Yamaho Industry Co., Ltd.

- Bucher Industries AG

- Mahindra & Mahindra Ltd.

- Maruyama Mfg. Co., Inc.

- SOLO Kleinmotoren GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the southeast asia agricultural sprayers market size was valued at USD 315 million in 2025 and estimated to grow from USD 336.7 million in 2026 to reach USD 470.1 million by 2031, at a CAGR of 6.9% during the forecast period (2026-2031).

This report is Segmented by Power Source (Manual, and More), by Product Type (Handheld and More), by Application (Field Crops and More), by Spray Volume Capacity ( Ultra-Low Volume Systems, and More), by Technology Level (Conventional, and More), by Pump Mechanism (Diaphragm Pumps, and More), and Geography (Indonesia, Vietnam, and More). The Market Values are Provided in USD.

Southeast Asia Agricultural Sprayers Market Trends and Insights

Farm Labor Shortages Raise Mechanized Spraying Demand

The rural labor movement in Southeast Asia has become a lasting shift rather than a short cycle, and that is changing spraying decisions at the farm level. In several countries, growers are finding it harder to secure workers for repeated spray passes during narrow crop windows. Manual backpack spraying can require 3 to 5 workers per 50 hectares in a single application round, quickly increasing the labor burden on large farms. As a result, labor scarcity is pushing mechanized sprayers from a convenience purchase into an operating need. Dealers in Indonesia and the Philippines have reported that payback periods for powered spraying equipment are now shortening to under 18 months in higher-value crop systems, which is speeding up purchase decisions that once took years. This is lifting demand for tractor-mounted boom sprayers on medium-scale farms and for drone service contracts on fragmented or difficult terrain where ground access is limited. The Southeast Asia agricultural sprayers market is therefore benefiting from a demand base tied to labor substitution, which is more stable than demand driven only by yield improvement.

Government Mechanization Subsidies and Financing

Public financing initiatives are influencing how farms and cooperatives in Southeast Asia approach sprayer purchases. During 2025, the Philippines' Department of Agriculture's Drones4Rice program offered subsidized access to drone spraying services through hectare-based vouchers, complemented by broader mechanization funding to support the adoption of precision agriculture. In Thailand, the Smart Farmer initiatives, launched in 2025, promoted modernization and the use of precision equipment, such as GPS-guided sprayers and agricultural drones. Similarly, Indonesia's KUR Pertanian financing programs launched in 2025 aim to ease the financial burden on smallholder farmers and cooperatives investing in agricultural machinery, including mechanized spraying systems. These programs not only reduce upfront costs but also prioritize higher-performing equipment with enhanced efficiency, control, and traceability through their eligibility criteria. Consequently, subsidy and financing policies are driving changes in the product mix of the Southeast Asia agricultural sprayers market by increasing demand for advanced spraying technologies.

High Upfront Cost Of Drones And Powered Sprayers

High equipment costs continue to be a significant challenge in the Southeast Asia agricultural sprayers market. Commercial agricultural drones with payload capacities of 20-30 liters are priced between USD 8,000 and USD 20,000, depending on configuration, batteries, and accessories. This pricing restricts ownership primarily to plantations, commercial farms, and well-funded cooperatives. While drone-as-a-service models help reduce upfront investment, operators still incur substantial costs related to equipment, training, and maintenance, leading to higher service prices for small-scale growers. Consequently, advanced spraying systems are being adopted more quickly in organized farming operations, whereas manual and basic powered sprayers remain prevalent on smaller farms.

Other drivers and restraints analyzed in the detailed report include:

- Precision Agriculture and Input-Efficiency Needs

- Palm Oil and Rice Crop Protection Drives Consistent Demand

- Fragmented Smallholder Land Limits Utilization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manual sprayers accounted for 44% of the Southeast Asia agricultural sprayers market in 2025, while battery-operated sprayers are projected to grow the fastest, with a CAGR of 11.3% through 2031. Manual sprayers remain prevalent due to their affordability, particularly for farms with very small landholdings. Additionally, they are easy to repair and require minimal supporting infrastructure, which is crucial in rural areas with limited dealer networks. These factors ensure their continued relevance in various segments of the Southeast Asia agricultural sprayers market, even as advanced products gain traction.

Battery-operated sprayers are increasingly popular as lithium-ion battery costs decline, runtimes improve, and rural electrification becomes more reliable in several countries. This trend is particularly evident in Thailand and Vietnam, where public procurement initiatives and low-emission farming programs are promoting the adoption of electrified tools. Meanwhile, solar-powered sprayers are emerging as a solution for smaller hillside and terraced farming operations. Fuel-powered systems continue to serve plantation and field-crop operations, where longer runtimes and larger tank capacities are essential. This diverse mix indicates that the Southeast Asia agricultural sprayers market is not entirely transitioning away from traditional power systems but is instead incorporating new power formats alongside the established manual base.

Handheld sprayers led product demand, with a 47% share in 2025, as they remain the cheapest and most practical option for fragmented plots. Their strength reflects the reality that a large part of regional agriculture still operates under land, cash, and infrastructure constraints. That gives handheld equipment durable volume even when more advanced systems post faster growth. The Southeast Asia agricultural sprayers market, therefore, continues to be led by a large, low-cost installed base.

UAV (Unmanned Aerial Vehicle) sprayers are projected to grow at a 14.2% CAGR through 2031, making them the fastest-growing product type in the market. Much of this expansion is being driven by drone-as-a-service networks that lower the effective cost of aerial spraying for farms that cannot justify ownership. In May 2026, DJI introduced the Agras T55 with a 50-liter payload and the Agras T100 Dual Battery Spraying System at AGRITECHNICA Asia 2026 in Bangkok, extending drone capability into larger field and plantation use cases. Tractor-mounted, trailed, and self-propelled sprayers continue to serve medium and large farms that require consistent boom coverage and higher daily work rates. Over time, the overlap between advanced ground systems and Unmanned Aerial Vehicle's is likely to intensify as buyers compare not only machine price, but also labor savings, turnaround speed, and service availability.

Complete Report Scope:

- By Power Source

- Manual

- Battery-Operated

- Solar-Powered

- Fuel-Operated

- By Product Type

- Handheld

- Tractor-Mounted

- Trailed

- Self-Propelled

- Unmanned Aerial Vehicle Sprayers

- By Application

- Field Crops

- Orchards and Vineyards

- Greenhouse Crops

- Turf and Gardening

- By Spray Volume Capacity

- Ultra-Low Volume Systems

- Low-Volume Systems

- High-Volume Systems

- By Technology Level

- Conventional

- Precision and GPS-Guided

- Artificial Intelligence-Enabled and Autonomous

- By Pump Mechanism

- Diaphragm Pumps

- Piston Pumps

- Centrifugal Pumps

- By Country

- Indonesia

- Vietnam

- Thailand

- Philippines

- Malaysia

- Cambodia

- Myanmar

- Singapore

- Rest of Southeast Asia

List of Companies Covered in this Report:

- KUBOTA Corporation

- Deere and Company

- CNH Industrial N.V.

- Yanmar Holdings Co., Ltd.

- DJI Agriculture

- XAG Co., Ltd.

- Terra Drone Corporation

- STIHL Holding AG & Co. KG

- AGCO Corporation

- Jacto Inc.

- HARDI International A/S

- EXEL Industries

- Micron Sprayers Ltd.

- ASPEE Agro Equipment Pvt. Ltd.

- Goizper Group

- Yamaho Industry Co., Ltd.

- Bucher Industries AG

- Mahindra & Mahindra Ltd.

- Maruyama Mfg. Co., Inc.

- SOLO Kleinmotoren GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Farm labor shortages raise mechanized spraying demand

- 4.2.2 Government mechanization subsidies and financing

- 4.2.3 Precision agriculture and input-efficiency needs

- 4.2.4 Palm oil and rice crop protection drives consistent demand

- 4.2.5 Low-emission rice programs favor precise spray scheduling

- 4.2.6 Expansion of contract drone service networks

- 4.3 Market Restraints

- 4.3.1 High upfront cost of drones and powered sprayers

- 4.3.2 Fragmented smallholder land limits utilization

- 4.3.3 Drone-compliant pesticide formulations remain limited

- 4.3.4 Flight permits and payload rules slow field operations

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Power Source

- 5.1.1 Manual

- 5.1.2 Battery-Operated

- 5.1.3 Solar-Powered

- 5.1.4 Fuel-Operated

- 5.2 By Product Type

- 5.2.1 Handheld

- 5.2.2 Tractor-Mounted

- 5.2.3 Trailed

- 5.2.4 Self-Propelled

- 5.2.5 Unmanned Aerial Vehicle Sprayers

- 5.3 By Application

- 5.3.1 Field Crops

- 5.3.2 Orchards and Vineyards

- 5.3.3 Greenhouse Crops

- 5.3.4 Turf and Gardening

- 5.4 By Spray Volume Capacity

- 5.4.1 Ultra-Low Volume Systems

- 5.4.2 Low-Volume Systems

- 5.4.3 High-Volume Systems

- 5.5 By Technology Level

- 5.5.1 Conventional

- 5.5.2 Precision and GPS-Guided

- 5.5.3 Artificial Intelligence-Enabled and Autonomous

- 5.6 By Pump Mechanism

- 5.6.1 Diaphragm Pumps

- 5.6.2 Piston Pumps

- 5.6.3 Centrifugal Pumps

- 5.7 By Country

- 5.7.1 Indonesia

- 5.7.2 Vietnam

- 5.7.3 Thailand

- 5.7.4 Philippines

- 5.7.5 Malaysia

- 5.7.6 Cambodia

- 5.7.7 Myanmar

- 5.7.8 Singapore

- 5.7.9 Rest of Southeast Asia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 KUBOTA Corporation

- 6.4.2 Deere and Company

- 6.4.3 CNH Industrial N.V.

- 6.4.4 Yanmar Holdings Co., Ltd.

- 6.4.5 DJI Agriculture

- 6.4.6 XAG Co., Ltd.

- 6.4.7 Terra Drone Corporation

- 6.4.8 STIHL Holding AG & Co. KG

- 6.4.9 AGCO Corporation

- 6.4.10 Jacto Inc.

- 6.4.11 HARDI International A/S

- 6.4.12 EXEL Industries

- 6.4.13 Micron Sprayers Ltd.

- 6.4.14 ASPEE Agro Equipment Pvt. Ltd.

- 6.4.15 Goizper Group

- 6.4.16 Yamaho Industry Co., Ltd.

- 6.4.17 Bucher Industries AG

- 6.4.18 Mahindra & Mahindra Ltd.

- 6.4.19 Maruyama Mfg. Co., Inc.

- 6.4.20 SOLO Kleinmotoren GmbH

7 Market Opportunities and Future Outlook

中東農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中東農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 農業噴霧器市場:2026-2032年全球市場預測(按推進方式、類型、容量、應用、最終用戶和分銷管道分類)德國農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)農業噴霧:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

農業噴霧器市場:2026-2032年全球市場預測(按推進方式、類型、容量、應用、最終用戶和分銷管道分類)德國農業噴霧器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)農業噴霧:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 農業噴霧器市場機會、成長要素、產業趨勢分析及2026-2035年預測。農業噴霧器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

農業噴霧器市場機會、成長要素、產業趨勢分析及2026-2035年預測。農業噴霧器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 農業噴霧器市場:按產品類型、動力來源、應用、噴霧能力和地區分類。

農業噴霧器市場:按產品類型、動力來源、應用、噴霧能力和地區分類。 全球電池驅動背包式噴霧器市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球電池驅動背包式噴霧器市場規模、佔有率、趨勢和成長分析報告(2026-2034) 農業噴霧器市場規模、佔有率、趨勢和預測:按類型、動力來源、應用和地區分類,2026-2034年電動熱霧發生器市場:依解決方案類型、運作模式、電源、應用和最終用戶分類-全球預測,2026-2032年

農業噴霧器市場規模、佔有率、趨勢和預測:按類型、動力來源、應用和地區分類,2026-2034年電動熱霧發生器市場:依解決方案類型、運作模式、電源、應用和最終用戶分類-全球預測,2026-2032年