|

市場調查報告書

商品編碼

2061370

農業噴霧器市場機會、成長要素、產業趨勢分析及2026-2035年預測。Agricultural Sprayers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

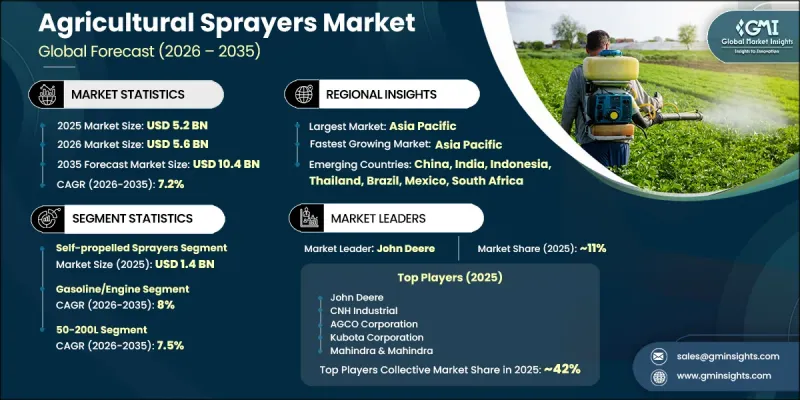

預計到 2025 年,全球農業噴霧器市場價值將達到 52 億美元,並預計以 7.2% 的複合年成長率成長,到 2035 年達到 104 億美元。

市場成長主要得益於精密農業技術的日益普及和對高效作物保護方法的日益重視。噴灑技術因其能提高噴灑精度、縮短作業時間並最大限度地減少化學藥劑浪費,在作物保護、施肥和病蟲害防治活動中廣泛應用。農業噴霧器已成為現代農業系統的重要組成部分。在非洲、亞太和拉丁美洲等開發中地區,高效作物保護對於維持農業生產力和保障糧食安全至關重要,因此農業噴霧器的重要性尤其突出。政府支持農業機械化和引進農業機械的財政獎勵措施也加速了市場擴張。此外,全球人口成長和糧食需求增加也推動了農業產量的提高。農業噴霧器在提高生產力的同時保持價格合理,為中小農戶提供了一種經濟高效的解決方案。從攜帶式噴霧器到先進的自走式噴霧系統,各種噴霧器的出現使農民能夠從人工噴灑過渡到更先進的農業技術。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 52億美元 |

| 預測市場規模 | 104億美元 |

| 複合年成長率 | 7.2% |

預計到2025年,自走式噴霧器市佔率將達到26.6%,市場規模將達到14億美元,並有望在2026年至2035年間以6.6%的複合年成長率成長。該細分市場憑藉其對大規模農業作業的適用性而佔據了穩固的地位。這些機器配備了整合式底盤系統、大容量藥箱、廣域噴桿以及精密農業技術,例如GPS導航和可變噴灑系統。與曳引機式噴霧器相比,自走式噴霧器具有更高的工作效率、更少的土壤壓實以及無需依賴其他農機即可自主運作等優點,因此備受大規模商業農場的青睞。

預計到2025年,50-200公升容量等級的噴藥機將佔據29.2%的市場佔有率,並在2026年至2035年間以7.5%的複合年成長率成長。該級別佔據主導地位的原因在於,中小農場集中在平均農場規模較小的地區,尤其是在亞太地區、非洲和拉丁美洲。手持式、背負式和緊湊型等低容量噴藥機因其價格實惠且實用而被廣泛採用。這些系統是需要高效且經濟的日常噴灑作業解決方案的農民的理想選擇。

美國農業噴霧器市場預計到2025年將達到13億美元,並在2026年至2035年間以6.9%的複合年成長率成長。市場擴張的驅動力主要來自大規模商業化農業運作、農場平均規模的擴大以及精密農業技術的積極應用。糧食、特種作物和園藝領域的需求依然強勁。農民正增加對配備先進系統(例如GPS導航、可變噴灑量技術和自動噴桿控制)的自走式噴霧器的投資。感測器和數據驅動型農業解決方案的日益普及,進一步推動了對技術先進的噴霧設備的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 價格波動和市場不可預測性

- 對品質保證和設備可靠性的擔憂

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 按產品類型和銷售量分類的平均售價

- 監理情勢

- 標準和合規要求

- 區域監理框架

- 認證標準

- 波特的分析

- PESTLE分析

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- HS編碼分類及貿易流量分析

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧正在改變傳統的噴灑方式。

- 按農場規模分類的生成式人工智慧用例和實施藍圖

- 人工智慧噴霧器的風險、限制和監管考量

- 生產能力和生產情況

- 按地區和主要生產商分類的製造能力

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 手持噴霧器

- 背包式噴霧器

- 拖曳式噴霧器

- 車載噴霧器

- 自走式噴霧機

- 空中撒佈器

- 其他

第6章 市場估算與預測:依動力來源,2022-2035年

- 電池

- 汽油/引擎

第7章 市場估計與預測:依技術分類,2022-2035年

- 油壓噴嘴

- 空氣輔助靜電式

- 超低容量(ULV)噴霧

- 精密噴塗

- 其他

第8章 市場估計與預測:依產能分類,2022-2035年

- 小於50公升

- 50~200L

- 200~500 L

- 超過500公升

第9章 市場估計與預測:依用途分類,2022-2035年

- 殺蟲劑/農藥

- 除草劑

- 消毒劑

- 肥料

第10章 市場估價與預測:依作物類型分類,2022-2035年

- 糧食

- 油籽和豆類

- 水果和花卉

- 莖和塊莖

- 其他(種植作物、林業等)

第11章 市場估價與預測:依最終用戶分類,2022-2035年

- 小規模農戶

- 中型農場

- 大型農場

- 機構和商業農場

第12章 市場估計與預測:依通路分類,2022-2035年

- 線上

- 離線

第13章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第14章:公司簡介

- Top Global Player

- John Deere

- CNH Industrial

- Kubota Corporation

- AGCO Corporation

- Mahindra &Mahindra

- Claas Group

- Bucher Industries(Kuhn Group)

- Regional Player

- Jacto

- Excel Industries

- Horsch Maschinen

- Changfa Agricultural Equipment

- TAFE Motors &Tractors

- 新興企業

- DJI Agriculture

- XAG Co., Ltd.

- Yamaha Motor Co.(Agriculture Division)

- Alamo Group

- SDF Group

- New Holland Agriculture

- Massey Ferguson

- Valtra

- YTO Group

- Lovol Heavy Industries

The Global Agricultural Sprayers Market was valued at USD 5.2 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 10.4 billion by 2035.

Market growth is supported by the rising adoption of precision agriculture practices and the increasing emphasis on efficient crop protection methods. Spraying technologies are gaining widespread acceptance as they improve application accuracy, reduce operational time, and minimize chemical wastage across crop protection, fertilization, and pest control activities. Agricultural sprayers have become an essential component of modern farming systems, particularly as efficient crop protection plays a critical role in sustaining agricultural productivity and ensuring food security across developing regions such as Africa, Asia Pacific, and Latin America. Government support programs promoting farm mechanization and financial incentives for agricultural equipment adoption are also accelerating market expansion. In addition, rising global population levels and increasing food demand are further intensifying the need for higher agricultural output. Agricultural sprayers offer cost-efficient solutions for small and medium-scale farmers by improving productivity while maintaining affordability. The availability of multiple sprayer formats, ranging from portable units to advanced self-propelled systems, is enabling farmers to transition from manual application methods to more technologically advanced farming practices.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.2 Billion |

| Forecast Value | $10.4 Billion |

| CAGR | 7.2% |

The self-propelled sprayers segment accounted for 26.6% share in 2025, reaching a value of USD 1.4 billion, and is expected to grow at a CAGR of 6.6% from 2026 to 2035. This segment holds a strong position due to its suitability for large-scale agricultural operations. These machines are equipped with integrated chassis systems, high-capacity tanks, wide spray booms, and precision farming technologies such as GPS-based navigation and variable rate application systems. Large commercial farms prefer self-propelled sprayers as they enhance operational efficiency, reduce soil compaction compared to tractor-mounted alternatives, and operate independently without reliance on additional farm machinery.

The 50-200L segment held 29.2% share in 2025 and is projected to grow at a CAGR of 7.5% from 2026 to 2035. This segment leads due to the high concentration of small and medium-scale farms globally, especially across Asia Pacific, Africa, and Latin America, where average landholding sizes remain relatively limited. Equipment within the low-volume category, including handheld, knapsack, and compact mounted sprayers, is widely adopted due to its affordability and practicality. These systems are well-suited for farmers requiring efficient yet cost-effective solutions for routine spraying operations.

U.S. Agricultural Sprayers Market reached USD 1.3 billion in 2025 and is expected to grow at a CAGR of 6.9% from 2026 to 2035. Market expansion is driven by large-scale commercial farming operations, expansive average farm sizes, and strong adoption of precision agriculture technologies. Demand remains high across grain production, specialty crops, and horticulture. Farmers are increasingly investing in self-propelled sprayers equipped with advanced systems such as GPS guidance, variable rate technology, and automated boom controls. The growing integration of sensors and data-driven farming solutions is further supporting demand for technologically advanced spraying equipment.

Major players operating in the Global Agricultural Sprayers Industry include John Deere, CNH Industrial, AGCO Corporation, Kubota Corporation, Mahindra & Mahindra, Bucher Industries (Kuhn Group), CLAAS KGaA, New Holland Agriculture, Massey Ferguson, Valtra, Horsch Maschinen, Jacto, DJI Agriculture, XAG Co., Ltd., Excel Industries, Alamo Group, SDF Group, TAFE Motors & Tractors, Changfa Agricultural Equipment, Lovol Heavy Industries, Yamaha Motor Co., and YTO Group. Companies in the agricultural sprayers market are focusing on strengthening precision agriculture capabilities by integrating GPS, sensor-based systems, and variable rate technology into their product offerings. Manufacturers are investing in automation and smart spraying solutions that enhance accuracy and reduce chemical usage. Expansion of electric and hybrid sprayer models is supporting sustainability goals and lowering operating costs. Firms are also improving durability and machine efficiency to suit diverse farm sizes and climatic conditions. Strategic collaborations with agricultural cooperatives and distribution networks are helping expand market reach. In addition, companies are emphasizing after-sales service, training programs, and digital farm management integration to enhance customer retention.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Power Source

- 2.2.4 Technology

- 2.2.5 Capacity

- 2.2.6 Usage

- 2.2.7 Crop Type

- 2.2.8 End User

- 2.2.9 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.3.1 Price volatility and market unpredictability

- 3.3.2 Quality assurance and equipment reliability concerns

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Value/Cost-plus) (Driven by Primary Research)

- 3.6.3 Average Selling Price by Product Type & Capacity

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Paid Database)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.10.3 HS Code Classification & Trade Flow Analysis

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Traditional Spraying Methods

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Farm Size

- 3.11.3 Risks, Limitations & Regulatory Considerations for AI-Enabled Sprayers

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Manufacturing Capacity by Region & Key Producer (Driven by Primary Research)

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Handheld sprayer

- 5.3 Knapsack sprayer

- 5.4 Trailed sprayer

- 5.5 Mounted sprayer

- 5.6 Self-propelled sprayer

- 5.7 Aerial sprayer

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Power Source, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Battery

- 6.3 Gasoline/Engine

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Hydraulic nozzles

- 7.3 Air-assisted electrostatic

- 7.4 Ultra-Low Volume (ULV) spraying

- 7.5 Precision spraying

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Capacity, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Below 50L

- 8.3 50-200L

- 8.4 200-500 L

- 8.5 Above 500L

Chapter 9 Market Estimates & Forecast, By Usage, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Insecticides/Pesticides

- 9.3 Herbicides

- 9.4 Fungicides

- 9.5 Fertilizers

Chapter 10 Market Estimates & Forecast, By Crop Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Cereals & Grains

- 10.3 Oilseeds & Pulses

- 10.4 Fruits & Flowers

- 10.5 Stem & Tubers

- 10.6 Other (Plantation Crops, Forestry, etc.)

Chapter 11 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Small Farmers

- 11.3 Medium Farmers

- 11.4 Large Farms

- 11.5 Institutions & Commercial Farms

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 Online

- 12.3 Offline

Chapter 13 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 Japan

- 13.4.3 India

- 13.4.4 Australia

- 13.4.5 South Korea

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 Middle East and Africa

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Top Global Player

- 14.1.1 John Deere

- 14.1.2 CNH Industrial

- 14.1.3 Kubota Corporation

- 14.1.4 AGCO Corporation

- 14.1.5 Mahindra & Mahindra

- 14.1.6 Claas Group

- 14.1.7 Bucher Industries (Kuhn Group)

- 14.2 Regional Player

- 14.2.1 Jacto

- 14.2.2 Excel Industries

- 14.2.3 Horsch Maschinen

- 14.2.4 Changfa Agricultural Equipment

- 14.2.5 TAFE Motors & Tractors

- 14.3 Emerging Players

- 14.3.1 DJI Agriculture

- 14.3.2 XAG Co., Ltd.

- 14.3.3 Yamaha Motor Co. (Agriculture Division)

- 14.3.4 Alamo Group

- 14.3.5 SDF Group

- 14.3.6 New Holland Agriculture

- 14.3.7 Massey Ferguson

- 14.3.8 Valtra

- 14.3.9 YTO Group

- 14.3.10 Lovol Heavy Industries

農業噴霧器市場:2026-2032年全球市場預測(按推進方式、類型、容量、應用、最終用戶和分銷管道分類)

農業噴霧器市場:2026-2032年全球市場預測(按推進方式、類型、容量、應用、最終用戶和分銷管道分類) 農業噴霧器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

農業噴霧器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 農業噴霧器市場:按產品類型、動力來源、應用、噴霧能力和地區分類。

農業噴霧器市場:按產品類型、動力來源、應用、噴霧能力和地區分類。 全球電池驅動背包式噴霧器市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球電池驅動背包式噴霧器市場規模、佔有率、趨勢和成長分析報告(2026-2034) 農業噴霧器市場規模、佔有率、趨勢和預測:按類型、動力來源、應用和地區分類,2026-2034年電動熱霧發生器市場:依解決方案類型、運作模式、電源、應用和最終用戶分類-全球預測,2026-2032年

農業噴霧器市場規模、佔有率、趨勢和預測:按類型、動力來源、應用和地區分類,2026-2034年電動熱霧發生器市場:依解決方案類型、運作模式、電源、應用和最終用戶分類-全球預測,2026-2032年 2026年全球霧化機市場報告2026年全球農業噴霧器市場報告熱霧發生器市場按產品類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)

2026年全球霧化機市場報告2026年全球農業噴霧器市場報告熱霧發生器市場按產品類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年) 農業噴霧器市場規模、佔有率和成長分析(按類型、農場規模、噴嘴類型、動力來源、容量、作物類型、應用和地區分類)—2026-2033年產業預測

農業噴霧器市場規模、佔有率和成長分析(按類型、農場規模、噴嘴類型、動力來源、容量、作物類型、應用和地區分類)—2026-2033年產業預測