|

市場調查報告書

商品編碼

2066484

農業噴霧器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Agriculture Sprayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

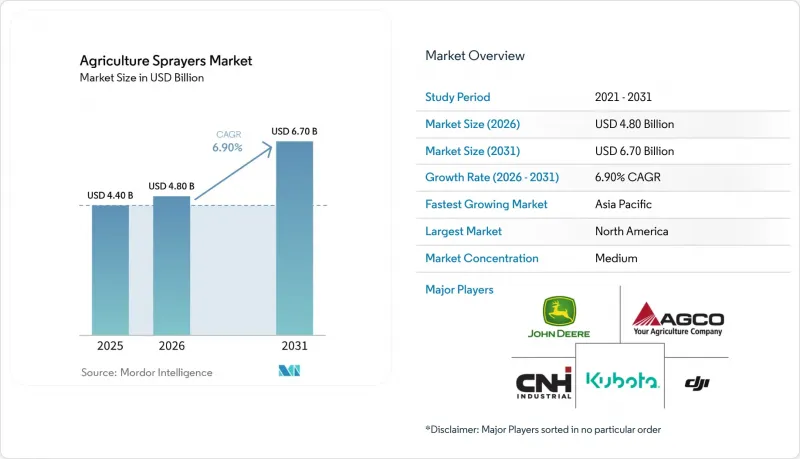

根據 Mordor Intelligence 預測,農業噴霧器市場規模將從 2025 年的 44 億美元成長到 2026 年的 48 億美元,到 2031 年將達到 67 億美元,2026 年至 2031 年的複合年成長率為 6.9%。

本報告按動力來源(手動、太陽能等)、產品類型(曳引機式等)、應用領域(田間作物等)、噴灑能力(低容量等)、技術水準(傳統等)、泵機制(隔膜泵等)和地區(北美、非洲等)進行分類。市場預測以美元計價。

全球農業噴霧器市場趨勢及洞察

農藥使用量增加

農藥施用頻率的不斷增加持續推動農業噴霧器市場對基礎設備的需求。根據美國農業部經濟研究局(USDA ERS)預測,到2024年和2025年,面積面積中將有96%為抗除草劑大豆,凸顯了大規模農業系統對作物保護化學品的持續依賴。大面積作物噴灑頻率的增加導致設備運作時間延長,噴嘴、幫浦、軟管和噴桿組件等零件的磨損也隨之加快。這一趨勢支撐著農業噴霧器及其售後耗材的穩定更換需求,尤其是在生長季多次噴灑農藥的密集種植區。

升級為使用感測器的精密噴塗

感測器驅動的升級正在拓展農業噴霧器市場的機遇,許多種植者無需更換整機,即可對現有設備進行改造升級。迪爾公司宣佈為其2026年及更早的機型提供更多升級選項和噴桿配置,這表明改造升級正成為一種重要的普及途徑,而非小眾解決方案。隨著感測精度的提高和實施成本的降低,精準噴灑正從一項高階功能轉變為商業農業中提昇生產力的標準工具。

高昂的初始投資和資金籌措障礙

對於農業噴霧器市場而言,資本成本仍然是一項重大挑戰,尤其是對於那些無法在兩到三個種植季節內收回先進設備投資的農場而言。 EXEL Industries報告稱,2024-2025會計年度上半年農業噴霧器相關產品的銷售額下降了15.7%,並將北美市場表現疲軟歸因於農民因經濟前景不明朗而採取的謹慎態度。在人工智慧和自動駕駛設備領域,這項挑戰更為突出,因為購買決策通常需要考慮硬體、軟體和服務成本的綜合因素,而不僅僅是機器本身的成本。因此,即使升級的技術優勢顯而易見,一些生產商也傾向於選擇改造現有設備、延遲設備更換或依賴外部服務供應商。除非融資條件放寬且租賃模式得到更廣泛的應用,否則幾個主要農業地區的先進技術普及率可能仍將低於其應有的水平。

細分市場分析

到2025年,燃油驅動型噴霧器將佔據農業噴霧器市場36.0%的最大佔有率。這些噴霧器之所以能保持其主導地位,是因為它們運作時間長,並且適用於在廣袤的農田上進行大規模噴桿式和自走式作業。在北美、南美和歐洲等農田面積廣闊、需要在有限的噴灑期內不間斷噴灑的地區,燃油驅動型噴霧器備受青睞。手動和太陽能驅動型噴霧器則繼續在小規模農民和溫室種植領域發揮重要作用。主要農業經濟體中完善的分銷網路、熟練的維護技術以及現有的燃料基礎設施,進一步鞏固了這一細分市場的穩定性。

在農業噴霧器市場中,電池動力噴霧器預計將以最高的複合年成長率(CAGR)成長,從2026年到2031年達到12.1%。這一成長主要得益於無人機和輕型自主平台的日益普及,以及鋰離子電池效率的提升。電池動力系統因其低噪音和低排放氣體等主要優勢,越來越適用於果園噴灑、溫室作業和小型田間作業。製造商還在電池動力平台上整合數位監控和自動噴灑系統,以提高噴灑精度和性能。儘管電池動力噴霧器市場成長迅速,但在需要長時間運作以維持生產力的大型作物保護作業中,燃油動力系統仍然至關重要。

到2025年,曳引機式噴霧系統將佔據最大的市場佔有率,達到41.4%。這些噴霧器之所以能保持強勁的市場地位,是因為它們能夠與現有曳引機車隊無縫整合,並且在實施精準噴灑技術方面具有成本效益。它們在北美和歐洲廣泛應用,完善的農業機械基礎設施支撐著穩定的更換需求。此外,牽引式和自走式噴霧器在大規模田間作業中繼續發揮至關重要的作用,這些作業需要更大的藥箱容量和更寬的噴桿噴灑範圍。該細分市場具有許多優勢,例如強大的售後支援、易於維護,以及與商業農業中常用的導航和改造技術的兼容性。

預計無人機噴灑器將以最快的速度成長,2026年至2031年的複合年成長率將達到28.1%。這一成長主要受勞動力短缺加劇、精準噴灑需求增加以及果園、稻田和特種作物中空中噴灑技術日益普及等因素驅動。無人機具有許多優勢,例如適應地形、減少對勞動力的依賴以及在噴灑季節短暫的情況下能夠快速部署。製造商正透過提供培訓支援、機隊管理軟體和自主路徑規劃系統來促進商業性應用。雖然地面噴灑器在全球噴灑作業中仍佔據很大比例,但在那些速度、目標精度和作業效率能夠為農民帶來顯著經濟價值的領域,無人機系統的應用正在不斷成長。

區域分析

到2025年,北美將佔據最大的市場佔有率,達到32.0%。這一主導地位主要歸功於玉米、大豆、小麥和菜籽等作物的大規模生產系統,這些作物需要大量的噴灑作業。在美國,自走式噴霧器、精準噴灑技術和數位化農場管理系統的廣泛應用推動了區域需求的成長。加拿大也做出了重要貢獻,能夠覆蓋大片田地的先進噴灑設備對於大規模商業糧食生產至關重要。完善的經銷商網路、定期的設備更新周期以及對精密農業技術的積極應用等因素,持續支撐著該地區大型商業農業企業對先進農業噴灑平台的穩定需求。

預計亞太地區將呈現最高成長率,2026年至2031年的複合年成長率將達到8.5%。這一成長主要得益於農業機械化的進步、農業無人機的日益普及以及政府對精密農業技術的持續支持。中國正透過補貼計畫推動農業機械現代化,這些計畫旨在推廣植物保護無人機和智慧農業技術。在印度、日本和澳大利亞,隨著人手不足和地形崎嶇等因素的加劇,空中噴灑的經濟價值日益凸顯,無人機噴灑系統的應用也不斷推進。區域製造商正致力於操作員培訓、經銷商支援以及拓展數位化噴灑生態系統,從而鞏固亞太地區作為全球先進農業噴灑解決方案生產和研發中心的地位。

歐洲市場仍然成熟,受法律規範的約束,合規要求和噴灑控制的改進推動設備的定期升級。歐盟委員會提出的2025年12月監管簡化計畫表明,在特定風險條件下,可能會對無人機引入一般豁免,預計將從2026年起擴大無人機噴灑市場。南美洲佔據重要地位,這得益於巴西龐大的商業農業基礎以及對曳引機式和自主式設備的強勁需求。同時,中東和非洲仍處於發展初期,但隨著糧食安全目標和出口殘留物標準的推動,選擇性的改進升級正在日益重要。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 農藥使用量增加

- 利用感測器提高噴塗精度

- 人事費用上升和操作人員短缺

- 政府對機械化和智慧農業的補貼

- 利用人工智慧 (AI) 進行定點噴灑的經濟效益可以縮短農藥使用的投資回收期。

- 用於果園噴灑服務的專用無人機和飛機數量增加

- 市場限制因素

- 前期資本投入龐大,且資金籌措存在諸多障礙。

- 操作人員和農業部門缺乏數據利用技能

- 混合車輛車隊中軟體和控制系統的互通性差距

- 噴灑高峰期對電池壽命、充電和運作時間的限制

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過動力來源

- 手動的

- 電池供電

- 太陽能

- 燃油驅動

- 依產品類型

- 手持式

- 聯結機式

- 拖著

- 自推進式

- 無人機噴灑器

- 透過使用

- 田間作物

- 果園和葡萄園

- 溫室種植的作物

- 草坪和園藝

- 按噴霧量

- 超微量噴霧

- 低容量

- 高容量

- 按技術水準

- 傳統的

- 高精度和GPS導

- 配備人工智慧(AI)且自主運作

- 泵浦機構

- 隔膜泵

- 活塞泵

- 離心式幫浦

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Limited

- SZ DJI Technology Co., Ltd.

- EXEL Industries

- Maquinas Agricolas Jacto SA

- AMAZONEN-WERKE H. DREYER SE & Co. KG

- Bucher Industries AG

- Yamaha Motor Co., Ltd.

- XAG Co., Ltd.

- HORSCH Maschinen GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the agriculture sprayers market size is projected to grow from USD 4.4 billion in 2025 to USD 4.8 billion in 2026 and USD 6.7 billion by 2031, registering a CAGR of 6.9% from 2026 to 2031.

This report is Segmented by Source of Power (Manual, Solar-Powered, and More), by Product Type (Tractor-Mounted, and More), by Application (Field Crops And, More), by Spray Volume (Low Volume and More), by Technology Level (Conventional and More), by Pump Mechanism (Diaphragm Pumps and More), and by Geography (North America, Africa and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Agriculture Sprayers Market Trends and Insights

Growth in Agrochemical Usage

Increasing pesticide application intensity continues to drive baseline equipment demand in the agriculture sprayers market. According to the United States Department of Agriculture Economic Research Service (USDA, ERS), herbicide-tolerant soybean acreage in the United States accounted for 96% of the planted area in 2024 and 2025, highlighting the ongoing reliance on crop protection chemical applications in large-scale farming systems. Higher spraying frequency in broadacre crops leads to increased equipment operating hours and accelerates wear on components such as nozzles, pumps, hoses, and boom assemblies. This trend supports consistent replacement demand for agricultural sprayers and aftermarket consumable components, particularly in intensive row-crop production regions where multiple spray applications are standard during the growing season.

Precision Spraying Upgrades Using Sensors

Sensor-based upgrades are expanding opportunities in the agriculture sprayers market, as many growers can retrofit their existing equipment instead of replacing entire machines. Deere & Company has introduced expanded upgrade options and boom configurations for Model Year 2026 equipment and earlier models, indicating that retrofitting is becoming a significant adoption pathway rather than a niche solution. As sensing accuracy improves and installation costs become more justifiable, precision spraying is transitioning from a premium feature to a standard productivity tool for commercial farming operations.

High Upfront Capital Expenditure and Financing Hurdles

Capital costs continue to pose a significant challenge for the agriculture sprayers market, particularly for farms unable to recoup the investment in advanced equipment within two to three seasons. EXEL Industries reported a 15.7% decline in agricultural spraying revenue during the first half of the fiscal year 2024-2025, attributing the weakness in North America to farmers adopting a cautious approach due to limited economic visibility. The challenge is more pronounced in the segment of AI-enabled and autonomous equipment, where purchase decisions often encompass hardware, software, and service costs rather than a single machine expense. This has led some growers to opt for retrofits, delay equipment replacement, or rely on external service providers, even when the technical benefits of upgrading are evident. Without an easing of credit conditions or broader adoption of leasing models, the uptake of advanced technologies is likely to remain below its potential in several established farming regions.

Other drivers and restraints analyzed in the detailed report include:

- Rising Labor Costs and Operator Shortages

- Government Mechanization and Smart-Farming Subsidies

- Limited Operator and Agronomy Data Skills

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The agriculture sprayers market share for the fuel-operated segment held the largest 36.0% in 2025. These sprayers maintain their dominance due to their longer operating endurance and suitability for large boom and self-propelled applications in broadacre farming systems. They are widely preferred in regions such as North America, South America, and Europe, where large field sizes necessitate uninterrupted spraying during narrow application windows. Manual and solar-assisted systems continue to serve niche roles in smallholder agriculture and greenhouse production. The segment's stability is further supported by established dealer networks, maintenance familiarity, and existing fuel infrastructure in major agricultural economies.

The agriculture sprayers market size for the battery-operated segment is forecasted to grow at the fastest 12.1% CAGR from 2026 to 2031. This growth is driven by increasing adoption of drones, lightweight autonomous platforms, and advancements in lithium-ion battery efficiency. Battery-powered systems are becoming increasingly suitable for orchard spraying, greenhouse operations, and compact field applications, where their lower operating noise and reduced emissions offer significant advantages. Manufacturers are also incorporating digital monitoring and automated application systems into battery-operated platforms to enhance precision and performance. Despite this growth, fuel-operated systems remain essential for high-capacity crop protection applications, where extended operating hours are critical for maintaining productivity.

Tractor-mounted systems accounted for the largest 41.4% share in 2025. These sprayers maintain a strong position due to their seamless integration with existing tractor fleets and their cost-effective approach to adopting precision spraying technologies. They are widely used in North America and Europe, where established agricultural machinery infrastructure supports consistent replacement demand. Additionally, trailed and self-propelled sprayers remain relevant for large-scale field operations that require higher tank capacities and wider boom coverage. This segment benefits from robust aftermarket support, easier maintenance, and compatibility with guidance and retrofit technologies commonly used in commercial farming operations.

Unmanned aerial vehicle sprayers are forecasted to expand at the fastest 28.1% CAGR from 2026 to 2031. This growth is driven by increasing labor shortages, rising demand for precision application, and the expanding adoption of aerial spraying in orchards, rice fields, and specialty crops. Unmanned aerial vehicle (UAV) sprayers offer advantages such as terrain adaptability, reduced reliance on labor, and rapid deployment during narrow treatment windows. Manufacturers are enhancing commercial adoption by providing training support, fleet management software, and autonomous route-planning systems. While ground-based sprayers continue to dominate global installed capacity, drone systems are increasingly being adopted for applications where speed, targeted spraying accuracy, and operational efficiency deliver greater economic value to agricultural operators.

Geography Analysis

North America held the largest 32.0% share in 2025. This leadership is attributed to extensive production systems for crops such as corn, soybean, wheat, and canola, which require high-capacity spraying operations. The United States drives regional demand through the widespread adoption of self-propelled sprayers, precision application technologies, and digital farm management systems. Canada also contributes significantly, with large commercial grain operations necessitating advanced spraying equipment capable of high field coverage. Factors such as an established dealer network, recurring equipment replacement cycles, and strong adoption of precision agriculture technologies continue to support stable demand for advanced agricultural spraying platforms across large-scale commercial farming operations in the region.

Asia-Pacific is forecast to grow at the fastest 8.5% CAGR from 2026 to 2031. This growth is driven by increasing farm mechanization, rising deployment of agricultural drones, and expanding government support for precision agriculture technologies. China is advancing agricultural equipment modernization through subsidy programs that promote plant protection drones and smart farming technologies. India, Japan, and Australia are also increasing the adoption of Unmanned Aerial Vehicle (UAV) spraying systems, as labor shortages and challenging terrain enhance the economic value of aerial spraying. Regional manufacturers are focusing on expanding operator training, dealer support, and digital spraying ecosystems, solidifying Asia-Pacific's position as a growing hub for the production and development of advanced agricultural spraying solutions globally.

Europe remains a mature market influenced by regulatory frameworks, where recurring equipment renewal is driven by compliance requirements and improved application control. The European Commission's December 2025 simplification proposal has introduced the possibility of general drone derogations under specific risk conditions, potentially expanding the market for Unmanned Aerial Vehicle (UAV) spraying after 2026. In South America, Brazil's extensive commercial farming base and strong demand for tractor-mounted and self-propelled equipment make the region significant. Meanwhile, the Middle East and Africa, though at an earlier stage, are becoming increasingly relevant as food security objectives and export residue standards encourage selective precision upgrades.

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Limited

- SZ DJI Technology Co., Ltd.

- EXEL Industries

- Maquinas Agricolas Jacto S.A.

- AMAZONEN-WERKE H. DREYER SE & Co. KG

- Bucher Industries AG

- Yamaha Motor Co., Ltd.

- XAG Co., Ltd.

- HORSCH Maschinen GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in agrochemical usage

- 4.2.2 Precision spraying upgrades using sensors

- 4.2.3 Rising labor costs and operator shortages

- 4.2.4 Government mechanization and smart-farming subsidies

- 4.2.5 Artificial Intelligence (AI) spot-spraying economics improve chemical-use payback

- 4.2.6 Growth of specialized drone and orchard spray-service fleets

- 4.3 Market Restraints

- 4.3.1 High upfront capital expenditure and financing hurdles

- 4.3.2 Limited operator and agronomy data skills

- 4.3.3 Mixed-fleet software and control-system interoperability gaps

- 4.3.4 Battery lifecycle, charging, and uptime constraints in peak spray windows

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Source of Power

- 5.1.1 Manual

- 5.1.2 Battery-Operated

- 5.1.3 Solar-Powered

- 5.1.4 Fuel-Operated

- 5.2 By Product Type

- 5.2.1 Handheld

- 5.2.2 Tractor-Mounted

- 5.2.3 Trailed

- 5.2.4 Self-Propelled

- 5.2.5 Unmanned Aerial Vehicle Sprayers

- 5.3 By Application

- 5.3.1 Field Crops

- 5.3.2 Orchards and Vineyards

- 5.3.3 Greenhouse Crops

- 5.3.4 Turf and Gardening

- 5.4 By Spray Volume Capacity

- 5.4.1 Ultra-Low Volume

- 5.4.2 Low Volume

- 5.4.3 High Volume

- 5.5 By Technology Level

- 5.5.1 Conventional

- 5.5.2 Precision and GPS-Guided

- 5.5.3 Artificial Intelligence-Enabled and Autonomous

- 5.6 By Pump Mechanism

- 5.6.1 Diaphragm Pumps

- 5.6.2 Piston Pumps

- 5.6.3 Centrifugal Pumps

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.1.4 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 Australia

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Rest of Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 Mahindra & Mahindra Limited

- 6.4.6 SZ DJI Technology Co., Ltd.

- 6.4.7 EXEL Industries

- 6.4.8 Maquinas Agricolas Jacto S.A.

- 6.4.9 AMAZONEN-WERKE H. DREYER SE & Co. KG

- 6.4.10 Bucher Industries AG

- 6.4.11 Yamaha Motor Co., Ltd.

- 6.4.12 XAG Co., Ltd.

- 6.4.13 HORSCH Maschinen GmbH

7 Market Opportunities and Future Outlook

農業噴霧器市場:2026-2032年全球市場預測(按推進方式、類型、容量、應用、最終用戶和分銷管道分類)

農業噴霧器市場:2026-2032年全球市場預測(按推進方式、類型、容量、應用、最終用戶和分銷管道分類) 農業噴霧器市場機會、成長要素、產業趨勢分析及2026-2035年預測。

農業噴霧器市場機會、成長要素、產業趨勢分析及2026-2035年預測。 農業噴霧器市場:按產品類型、動力來源、應用、噴霧能力和地區分類。

農業噴霧器市場:按產品類型、動力來源、應用、噴霧能力和地區分類。 全球電池驅動背包式噴霧器市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球電池驅動背包式噴霧器市場規模、佔有率、趨勢和成長分析報告(2026-2034) 農業噴霧器市場規模、佔有率、趨勢和預測:按類型、動力來源、應用和地區分類,2026-2034年電動熱霧發生器市場:依解決方案類型、運作模式、電源、應用和最終用戶分類-全球預測,2026-2032年

農業噴霧器市場規模、佔有率、趨勢和預測:按類型、動力來源、應用和地區分類,2026-2034年電動熱霧發生器市場:依解決方案類型、運作模式、電源、應用和最終用戶分類-全球預測,2026-2032年 2026年全球霧化機市場報告2026年全球農業噴霧器市場報告熱霧發生器市場按產品類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)

2026年全球霧化機市場報告2026年全球農業噴霧器市場報告熱霧發生器市場按產品類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年) 農業噴霧器市場規模、佔有率和成長分析(按類型、農場規模、噴嘴類型、動力來源、容量、作物類型、應用和地區分類)—2026-2033年產業預測

農業噴霧器市場規模、佔有率和成長分析(按類型、農場規模、噴嘴類型、動力來源、容量、作物類型、應用和地區分類)—2026-2033年產業預測