|

市場調查報告書

商品編碼

2072713

中東歐屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Central and Eastern Europe Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

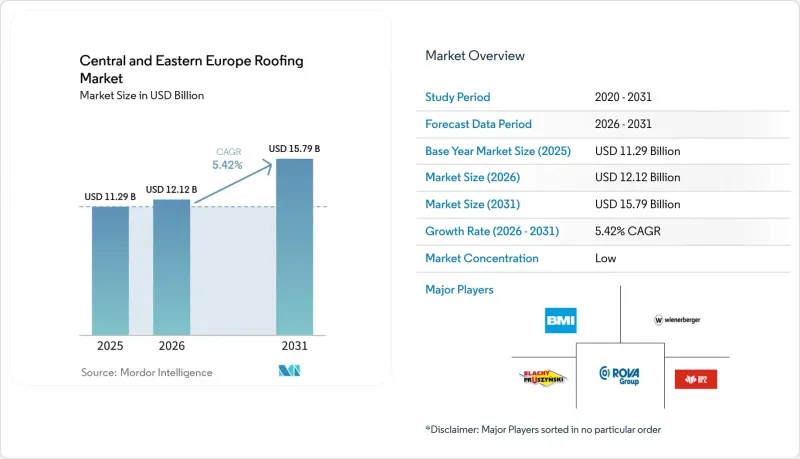

根據 Mordor Intelligence 預測,中東歐屋頂材料市場規模預計在 2025 年達到 112.9 億美元,2026 年達到 121.2 億美元,2031 年達到 157.9 億美元,2026 年至 2031 年的複合年成長率為 5.42%。

本報告按材料類型(瀝青瓦、粘土/混凝土瓦、金屬屋頂、瀝青/改性瀝青卷材等)、施工類型(新建、屋頂翻新)、應用領域(住宅等)和地區(波蘭、羅馬尼亞、捷克、匈牙利及其他歐洲國家)進行分類。市場預測以美元計價。

中東歐屋頂材料市場趨勢及洞察

強制執行EPBD維修將創造一個有政策支援的、永續的需求管道。

中東歐地區的屋頂市場正因《建築能源性能指令》(EPBD) 的修訂而重組。該指令是預測期內影響屋頂維修決策的最重要政策因素之一。該指令規定,到2030年,能源效率最低的非住宅建築中,16%必須維修;到2033年,這一比例將達到26%。此外,該指令還旨在2030年將住宅建築的平均初級能源消耗降低16%。這在中東歐地區尤其重要,因為該地區超過50%的建築不符合現行的性能標準,而且大部分住宅存量建於1990年之前。實際上,許多房屋僅靠小規模修小補無法達到標準,因此,屋頂更換、隔熱升級以及相關的外部工程將擴大以打包形式進行。這種打包方式將降低屋頂工程需求的自願性,使其與強制合規計畫更加緊密地連結起來。這將使服務中東歐屋頂市場的供應商和承包商更容易預測需求。此外,經過技術認證的系統價值也隨之提升,因為買家現在需要證明完工後的屋頂不僅能恢復其耐候性,還能達到能源性能目標。

隔熱維修補貼計畫正在刺激大規模的住宅屋頂更換。

針對普通家庭的補貼計畫正在擴大維修的範圍,使中東歐的屋頂市場更能抵禦短期價格壓力。波蘭的「Czyste Powietrze」(意為「節能改造」)計劃於2025年3月從歐盟現代化基金獲得了100億波幣(約25億美元)的資金。這筆資金用於支持屋頂隔熱,作為更廣泛的家庭節能維修計畫的一部分。在捷克共和國,「新綠色節能計畫」直接支持獨棟住宅和多用戶住宅的屋頂和天花板隔熱工程,將政策需求轉化為實際的屋頂更換工作。這種效果在低收入族群中特別顯著,高額津貼降低了維修決策對金屬和瀝青價格波動的敏感度。這使得屋頂更換訂單的前景比沒有補貼的純粹消費市場更穩定,尤其是在住宅存量老舊、供暖效率較低的國家。因此,在中歐和東歐的住宅市場,日益成長的趨勢是,專案應在一個決策過程中同時解決隔熱、屋頂更換和未來太陽能發電裝置等問題,而不是分階段進行。

鋼鐵、瀝青和能源投入成本的波動

鋼鐵和瀝青價格的波動持續對中東歐的屋頂材料市場構成直接阻力,尤其對那些依賴進口原料或需要高能耗生產製程的產品線影響更大。根據歐洲金屬冶金聯合會(EUROMETAL)的報告,2026年5月下旬熱軋鋼卷價格為每噸700至770歐元(相當於每噸756至831.6美元),但預計2026年7月保障措施的變化將使鋼鐵產品的價格走勢保持不確定性。這種不確定性正在影響金屬屋頂材料的製造商、加工商和經銷商,導致他們難以製定估算時間表和管理採購進度。對於平屋頂系統而言,與瀝青相關的壓力也是一個重要因素,因為原料供應中斷可能會延誤專案進度並擠壓利潤空間。此外,能源成本也給依賴穩定工廠運作的陶瓦、防水油布和其他屋頂材料製造商帶來了額外的負擔。這種負擔對當地中小企業來說尤其沉重,這可能會加速擁有廣泛採購選擇和雄厚財力的大公司擴大市場佔有率。

細分市場分析

到2025年,陶瓦和混凝土瓦將佔據36.20%的市場佔有率,成為中東歐屋頂材料市場中最大的類別。這一主導地位反映了人們對坡屋頂的長期偏好,因為在波蘭、匈牙利和捷克共和國,瓦屋頂仍然與住宅建築緊密相連。此外,由於許多正在翻新的住宅最初建造時就採用了適合瓦片系統的坡屋頂,因此該類別也受益於重建需求的成長。從實際角度來看,儘管人們對維修的期望不斷提高,但瓦片憑藉其良好的口碑仍然非常重要。 2025年底的投資趨勢也表明,製造商仍然將這個類別作為戰略重點。例如,維納伯格(Wienerberger)在匈牙利開設了一家新的混凝土瓦運作,年產能為300萬平方公尺,投資額達3,000萬歐元(3,240萬美元)。這項決定進一步印證了規模、產品連續性和區域供應鏈在中東歐屋頂產業中仍然至關重要的觀點。

因此,在現有屋頂框架難以支撐重型更換系統的維修工程中,金屬屋頂尤其具有吸引力。鑑於合格技術純熟勞工數量有限,對於需要在較少工時內覆蓋更大面積的項目,金屬屋頂也同樣適用。對於平屋頂商業建築而言,瀝青和改質瀝青防水卷材仍然必不可少,但由於成本和供應波動,採購計畫可能較為複雜。單層防水卷材因其適用於排水設計並可與屋頂太陽能發電系統整合,在大規模工業應用中市場佔有率不斷成長。另一方面,瀝青瓦仍然佔據著一定的市場地位,而木材主要用於歷史建築和高階項目。在中東歐的屋頂產業,隨著業主越來越重視合規性、使用壽命和整合性,而不僅僅是用低成本的替代方案替換材料,轉向認證系統解決方案的趨勢日益明顯。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 根據能源性能指令 (EPBD) 對能源效率最低的建築物進行重大維修

- 為滿足屋頂更換需求,提供隔熱維修補貼。

- 倉庫和輕工業屋頂擴建工程透過近岸運輸進行拖運

- 在維修工程中改用金屬屋頂,目的是減輕重量並縮短施工時間。

- 「太陽能就緒」認證和屋頂太陽能發電系統的獲批,正在推動屋頂系統升級的增加。

- 冰雹和對流風暴造成的破壞正在加速屋頂更換的週期。

- 市場限制因素

- 鋼材、瀝青和能源投入成本波動很大

- 熟練屋頂工短缺和勞動力老化

- 維修工程效果不佳,且建築層面的執行管理不善。

- 建築承包商素質參差不齊,建築規範執行不符。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 成本結構分析

- 屋頂更換的趨勢和影響

- 波特五力模型

第5章 市場規模與成長預測

- 材料類型

- 瀝青瓦

- 粘土磚和水泥瓦

- 金屬屋頂

- 瀝青基/改質瀝青基防水卷材

- 單層薄膜(TPO、EPDM、PVC)

- 樹

- 其他

- 依建築類型

- 新建工程

- 屋頂更換和維修

- 透過使用

- 住宅

- 商業

- 產業

- 公共設施

- 其他

- 按地區

- 波蘭

- 羅馬尼亞

- 捷克共和國

- 匈牙利

- 其他中歐和東歐國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BMI Group

- Wienerberger

- Pruszynski

- BP2

- ROVA Group

- Lindab

- Ruukki Construction

- Kingspan Group

- Soprema

- Bilka

- Metigla

- Wetterbest

- Balex Metal

- swissporTON

- Terran Group

- Onduline Group

- PREFA Aluminiumprodukte

- Gerard Roofing System

- Nelskamp

- Bauder

第7章 市場機會與未來展望

According to Mordor Intelligence, the central and eastern europe roofing market size is projected to be USD 11.29 billion in 2025, USD 12.12 billion in 2026, and reach USD 15.79 billion by 2031, growing at a CAGR of 5.42% from 2026 to 2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, and More), Construction Type (New Construction, Reroofing), Application (Residential, and More), and Geography (Poland, Romania, Czech Republic, Hungary, and Rest of Central and Eastern Europe). The Market Forecasts are Provided in Terms of Value (USD).

Central and Eastern Europe Roofing Market Trends and Insights

EPBD Renovation Mandates Create a Durable, Policy-Anchored Demand Pipeline

The Central and Eastern Europe roofing market is being reshaped by the recast of the Energy Performance of Buildings Directive (EPBD), which is one of the strongest policy drivers influencing roof renovation decisions over the forecast period. The directive requires renovating the 16% worst-performing non-residential buildings by 2030 and 26% by 2033, while also targeting a 16% reduction in average primary energy use in residential buildings by 2030. This matters more in Central and Eastern Europe because more than 50% of the building stock does not meet current performance expectations, and much of the residential base predates 1990. In practice, many properties will not be able to comply solely through minor repairs, so roof replacement, insulation upgrades, and related envelope work will increasingly be specified together. That bundling effect makes roofing demand less discretionary and more tied to mandatory compliance schedules, which improves visibility for suppliers and installers serving the Central and Eastern Europe roofing market. It also raises the value of technically certified systems, because buyers now need proof that the finished roof meets energy performance targets rather than just restoring weather protection.

Thermal Modernization Subsidy Programs Activate Household Reroofing at Scale

Household subsidy programs are expanding the addressable base for renovation work and making the Central and Eastern European roofing market more resilient to short-term price pressure. Poland's Czyste Powietrze program secured PLN 10 billion (USD 2.5 billion) from the European Union (EU) Modernization Fund in March 2025, including support for roof insulation as part of wider household energy upgrades. In the Czech Republic, the New Green Savings Programme directly supports roof and ceiling insulation for family houses and apartment buildings, which helps convert policy demand into actual roof replacement activity. The effect is especially strong at the lower-income end, where high grant coverage reduces the sensitivity of repair decisions to movements in metal or bitumen prices. That keeps reroofing pipelines more stable than they would be in a purely unsubsidized consumer market, particularly in countries with older housing stock and low heating efficiency. As a result, the Central and Eastern Europe roofing market is seeing more projects where insulation, covering replacement, and future solar compatibility are considered in a single homeowner decision rather than in separate phases.

Volatile Steel, Bitumen, and Energy Input Costs

Steel and bitumen price volatility remains a direct headwind for the Central and Eastern Europe roofing market, particularly in product groups that depend on imported feedstock or energy-intensive production. EUROMETAL reported late May 2026 hot-rolled coil prices at EUR 700 to EUR 770 per tonne, equivalent to USD 756 to USD 831.6 per tonne, while the July 2026 safeguard changes are expected to keep pricing for steel-based products uncertain. That uncertainty affects metal roofing manufacturers, fabricators, and distributors because quoting windows and procurement timing become harder to manage. Bitumen-related pressure also matters for flat roofing systems, as disruptions in raw material availability can delay project schedules and compress margins. Energy costs add another layer of strain on clay tile, membrane, and other manufactured roofing products that depend on stable plant economics. The burden falls more heavily on smaller regional players, which may accelerate share gains for larger businesses with broader sourcing options and stronger balance sheets.

Other drivers and restraints analyzed in the detailed report include:

- Nearshoring Industrial Construction Sustains Single-Ply and Panel Roofing Demand

- Metal Roofing Substitution in Renovation for Lightweight, Faster Installation

- Skilled Roofer Shortages and Ageing Installer Base

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clay & Concrete Tiles held a 36.20% market share in 2025, making them the largest material category in the Central and Eastern Europe roofing market. This leading position reflects long-established preferences for pitched roofs across Poland, Hungary, and the Czech Republic, where tile roofs remain closely tied to mainstream residential construction. The category also benefits from replacement demand, as many renovated homes were originally built with pitched roofs that are well-suited to tile systems. In practical terms, that installed base keeps tile relevant even as performance expectations rise. End-2025 investment also showed that manufacturers still view this category as strategically important, with Wienerberger commissioning a new concrete roof tile plant in Hungary with an annual capacity of 3 million square meters and an investment of EUR 30 million (USD 32.4 million). The decision supports the view that scale, product continuity, and regional supply remain important in the Central and Eastern Europe roofing industry.

Metal Roofing is the fastest-growing material segment, with the Central and Eastern Europe roofing market size for this category projected to expand at a 6.40% CAGR from 2026 to 2031. Its growth is tied to two practical advantages that matter more each year: lighter structural loading on older buildings and faster installation under tight labor conditions. That makes metal especially attractive in renovation projects where legacy roof frames cannot easily support heavier replacement systems. It also fits projects where installers need to complete more area in fewer site days because certified labor is limited. Bituminous and modified bitumen membranes remain essential for flat commercial roofs, although cost and supply volatility can complicate procurement planning. Single-ply membranes are gaining ground in large industrial applications due to their compatibility with drainage design and rooftop solar integration. At the same time, asphalt shingles retain a niche role, and wood remains concentrated in heritage and premium uses. Across the Central and Eastern Europe roofing industry, the shift toward certified system solutions is becoming clearer as owners place more value on compliance, service life, and integration than on low-end material substitution alone.

Complete Report Scope:

- By Material Type

- Asphalt Shingles

- Clay & Concrete Tiles

- Metal Roofing

- Bituminous / Modified Bitumen Membranes

- Single-Ply Membranes (TPO, EPDM, and PVC)

- Wood

- Others

- By Construction Type

- New Construction

- Reroofing and Replacement

- By Application

- Residential

- Commercial

- Industrial

- Institutional

- Others

- By Geography

- Poland

- Romania

- Czech Republic

- Hungary

- Rest of Central and Eastern Europe

List of Companies Covered in this Report:

- BMI Group

- Wienerberger

- Pruszynski

- BP2

- ROVA Group

- Lindab

- Ruukki Construction

- Kingspan Group

- Soprema

- Bilka

- Metigla

- Wetterbest

- Balex Metal

- swissporTON

- Terran Group

- Onduline Group

- PREFA Aluminiumprodukte

- Gerard Roofing System

- Nelskamp

- Bauder

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EPBD-Led Deep Renovation of Worst-Performing Buildings

- 4.2.2 Thermal Modernization Subsidies Supporting Reroofing Demand

- 4.2.3 Nearshoring-Led Warehouse and Light-Industrial Roof Build-Out

- 4.2.4 Metal Roofing Substitution in Renovation for Lightweight, Faster Installation

- 4.2.5 Solar-Ready and Rooftop PV Permit Triggers Increasing Roof-System Upgrades

- 4.2.6 Hail and Convective Storm Damage Accelerating Reroofing Cycles

- 4.3 Market Restraints

- 4.3.1 Volatile Steel, Bitumen, and Energy Input Costs

- 4.3.2 Skilled Roofer Shortages and Ageing Installer Base

- 4.3.3 Renovation Underperformance and Weak Building-Level Execution Controls

- 4.3.4 Fragmented Installer Quality and Uneven Code Enforcement

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Cost Structure Analysis

- 4.8 Trend and Impacts of Roofing Replacements

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay & Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes (TPO, EPDM, and PVC)

- 5.1.6 Wood

- 5.1.7 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 Poland

- 5.4.2 Romania

- 5.4.3 Czech Republic

- 5.4.4 Hungary

- 5.4.5 Rest of Central and Eastern Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 BMI Group

- 6.4.2 Wienerberger

- 6.4.3 Pruszynski

- 6.4.4 BP2

- 6.4.5 ROVA Group

- 6.4.6 Lindab

- 6.4.7 Ruukki Construction

- 6.4.8 Kingspan Group

- 6.4.9 Soprema

- 6.4.10 Bilka

- 6.4.11 Metigla

- 6.4.12 Wetterbest

- 6.4.13 Balex Metal

- 6.4.14 swissporTON

- 6.4.15 Terran Group

- 6.4.16 Onduline Group

- 6.4.17 PREFA Aluminiumprodukte

- 6.4.18 Gerard Roofing System

- 6.4.19 Nelskamp

- 6.4.20 Bauder

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類)

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類) 中東和北非屋頂材料市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲屋頂材料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)東協屋頂材料市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和北非屋頂材料市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲屋頂材料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)東協屋頂材料市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告

2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告