|

市場調查報告書

商品編碼

2072712

東協屋頂材料市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)ASEAN Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

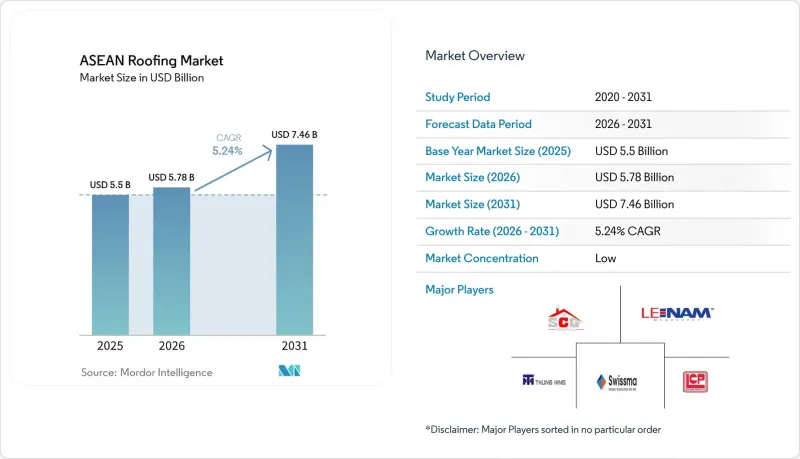

根據 Mordor Intelligence 預測,東協屋頂材料市場規模預計將在 2025 年達到 55 億美元,2026 年達到 57.8 億美元,到 2031 年達到 74.6 億美元,2026 年至 2031 年的複合年成長率為 5.24%。

本報告按材料類型(瀝青瓦、粘土/混凝土瓦、金屬屋頂材料、瀝青/改性瀝青防水卷材、單層防水卷材、木材及其他)、施工類型(新建、屋頂更換/翻新)、應用領域(住宅、商業、工業及其他)和地區(印度尼西亞、越南、泰國及其他)進行細分。市場預測以美元計價。

東協屋頂材料市場趨勢與洞察

政府主導的住宅和基礎設施項目正在擴大對屋頂材料的需求。

儘管私人建築的進展並不均衡,但政府主導的住宅計畫為東協屋頂材料市場提供了堅實的支撐。在印度尼西亞,一項預算為43.6兆印尼幣(約26.5億美元)的計劃,旨在到2025年底維修200萬套不達標住宅,直接推動了西爪哇、萬丹和中爪哇等住宅嚴重短缺省份對屋頂更換的需求。在越南,2025年完工的社會住宅,超過了年度目標。由於公共投資的增加,2026年的目標已提高到158,723萬套。這些項目至關重要,因為它們不僅能在私人住宅開工放緩的情況下維持對屋頂材料的需求,還能為製造商和承包商提供更清晰的訂單預測。此外,推廣在大規模住宅中使用經過認證和標準化的材料,將逐步減少假冒和回收屋頂材料的作用,從而擴大東協屋頂材料市場的合法和可銷售基本客群。

由於綠建築和隔熱性能法規的要求,屋頂結構規範更加嚴格。

東協屋頂材料市場的產品選擇正隨著建築圍護結構性能相關法規的不斷改進而穩步變化。國際能源總署(IEA)發布的東協節能建築藍圖指出,屋頂是熱帶氣候下重要的熱邊界。藍圖強調,冷屋頂、綠色屋頂和被動式通風是降低冷氣需求的實際可行的措施。東協能源中心(ACE)和聯合國環境規劃署(UNEP)於2026年4月聯合發布的《被動式冷卻藍圖》更進一步,建議將被動式冷卻要求強制納入國家建築規範,並將反射屋頂定位為一項關鍵措施。隨著綠色認證體系逐漸成為專案融資和公共採購的必要條件,買家將越來越傾向於選擇符合標準的完整屋頂系統,而不是單一低成本組件。這一趨勢將推動反射型、隔熱型和一體化屋頂系統的發展,使東協屋頂市場不再局限於公共和商業項目中的商品採購。

原物料價格波動對專案的獲利能力和供應商的利潤率帶來了壓力。

投入成本波動仍然是東協屋頂材料市場面臨的最明顯阻力之一。瀝青、聚氯乙烯(PVC)樹脂、熱塑性聚烯(TPO)化合物和鋼捲均易受全球大宗商品週期的影響,而這些週期往往與當地的施工進度和競標時間表相衝突。根據經濟合作暨發展組織(OECD)發布的《2025年鋼鐵展望》,產能提升和鋼帶及鋼捲(對東協金屬屋頂材料製造商至關重要)買家需求成長不均衡都可能導致價格波動。在2024年和2025年,這些價格波動擠壓了供應商的利潤空間,使其難以獲得競標價格,迫使一些承包商選擇品質較低的材料。在東協屋頂材料的長期專案週期中,缺乏避險能力、長期採購合約或一定程度原物料整合能力的製造商仍面臨巨大的風險。

細分市場分析

到2025年,金屬屋頂材料將佔東協屋頂市場38%的佔有率,成為該全部區域最大的屋頂材料類別。這一地位主要得益於其在工業倉庫、郊區住宅和公共工程中的廣泛應用,在這些項目中,安裝速度和每平方公尺成本仍然是關鍵的採購考量。此外,該地區完善的製造業和物流基礎設施也為金屬屋頂材料的發展提供了有利條件,模壓金屬板常用於大跨度、緩坡屋頂,有時還會與隔熱複合材料結合使用。經合組織發布的《2025年鋼鐵展望》指出,東協是少數預計到2030年鋼鐵需求將保持強勁成長的地區之一,這進一步印證了上述趨勢。在東協屋頂市場,這將使金屬屋頂製造商即使在價格波動的情況下也能確保重要的戰略材料供應基礎。

在東協屋頂材料市場,單層防水卷材預計到2031年將以6.4%的複合年成長率成長,成為預測期內成長最快的建築材料類別。這項需求主要由新加坡、雅加達和胡志明市的資料中心和高階商業屋頂推動,這些地區由於熱熔焊接系統接縫失效風險較低且更換運作較短,因此更受青睞。在泰國和越南的住宅中,粘土瓦和混凝土瓦仍然具有重要的文化和建築價值。然而,在多層建築中,它們面臨著被更輕的纖維水泥和金屬建築材料取代的壓力。瀝青瓦仍主要集中在泰國、馬來西亞和菲律賓的高檔住宅。同時,由於承包商基礎穩固且與焊接系統相比所需設備較少,瀝青防水卷材在平屋頂的商業和工業設施中仍被廣泛應用。雖然木質屋頂材料的受歡迎程度正在下降,但聚碳酸酯、uPVC 和纖維水泥板在經濟型住宅翻新中卻越來越受歡迎。在那些經認證的隔熱且易於維護的產品符合政府主導的翻新需求的地區,這種趨勢尤其明顯。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府住宅和基礎設施建設計劃正在擴大對屋頂材料的需求。

- 綠色建築和熱工性能法規支援冷屋頂和保溫屋頂

- 工業、物流、低溫運輸和資料中心建設的擴張增加了對保溫板和膜材料的需求。

- 熱帶地區的濕度、季風的影響以及漏水的風險增加了防水工程的頻率。

- 透過綠色屋頂、虹吸式排水和雨水管理系統創造附加價值。

- 減少東協地區的貿易壁壘改善了優質屋頂材料的採購環境。

- 市場限制因素

- 瀝青、樹脂和石油化學產品等原料成本的波動給利潤率帶來了壓力。

- 熟練工人短缺導致建築品質下降,並減緩了專用屋頂材料的採用。

- 來自成本更低的替代材料的競爭正在限制定價權。

- 對進口的依賴和不一致的區域標準使與供應相關的決策變得複雜。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 成本結構分析

- 屋頂更換的趨勢和影響

- 波特五力模型

第5章 市場規模與成長預測

- 依材料類型

- 瀝青瓦

- 粘土磚和水泥瓦

- 金屬屋頂

- 瀝青基/改質瀝青基防水卷材

- 單層薄膜(TPO、EPDM、PVC)

- 樹

- 其他

- 依建築類型

- 新建工程

- 屋頂更換和維修

- 透過使用

- 住宅

- 商業

- 產業

- 公共設施

- 其他

- 按地區

- 印尼

- 越南

- 泰國

- 菲律賓

- 其他東南亞國協

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SCG Roofing

- Swissma Building Technologies

- Thung Hing

- Le Nam Megasheet

- LCP Group

- Kemudi Sempurna

- Asia Jaya Sepadu

- UGI

- PT. Insulated Panel Indonesia

- Subzero

- PT. Mandiri Mulia Makmur Abadi(MMMA)

- ROOFMAXX

- Kingspan

- Sika

- SOPREMA

第7章 市場機會與未來展望

According to Mordor Intelligence, the ASEAN roofing market size is projected to be USD 5.5 billion in 2025, USD 5.78 billion in 2026, and reach USD 7.46 billion by 2031, growing at a CAGR of 5.24% from 2026 to 2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, Single-Ply Membranes, Wood, and Others), Construction Type (New Construction, Reroofing and Replacement), Application (Residential, Commercial, Industrial, and More), and Geography (Indonesia, Vietnam, Thailand, and More). The Market Forecasts are Provided in Terms of Value (USD).

ASEAN Roofing Market Trends and Insights

Government Housing and Infrastructure Pipelines Expanding Roofing Demand

Government-backed housing schemes are providing a reliable support base for the ASEAN roofing market as private construction moves unevenly. In Indonesia, the renovation of 2 million substandard dwellings by the end of 2025, backed by Rp 43.6 trillion (USD 2.65 billion), is directly driving roofing replacement demand in provinces with large housing deficits such as West Java, Banten, and Central Java. In Vietnam, more than 102,600 social housing units were completed in 2025, which exceeded the annual plan, and the 2026 target rises to 158,723 units, with stronger public investment disbursement behind it. These programs matter because they sustain roofing volume even when private housing starts slow, and they create clearer order visibility for manufacturers and contractors. They also encourage the use of certified, standardized materials in mass housing, gradually reducing the role of informal or recycled roofing inputs and broadening the formal, addressable base of the ASEAN roofing market.

Green-Building and Thermal-Performance Regulation Tightening Roof Specifications

Regulations around building envelope performance are steadily changing product choice in the ASEAN roofing market. The International Energy Agency (IEA) roadmap for energy-efficient buildings in ASEAN identifies roofs as the critical thermal boundary in tropical climates. It highlights cool roofs, green roofs, and passive ventilation as practical measures to reduce cooling demand. The Passive Cooling Roadmap launched by the ASEAN Centre for Energy (ACE) and the United Nations Environment Programme (UNEP) in April 2026 goes further by recommending mandatory passive cooling requirements in national building codes and identifying reflective roofs as a leading intervention. Once green certification systems become a practical requirement for project financing or public procurement, buyers tend to purchase compliant roof assemblies rather than isolated low-cost components. That dynamic supports reflective, insulated, and integrated roof systems and moves the ASEAN roofing market away from purely commodity purchasing in institutional and commercial projects.

Raw-Material Cost Volatility Compressing Project Economics and Supplier Margins

Input cost volatility is still one of the clearest brakes on the ASEAN roofing market. Bitumen, Polyvinyl Chloride (PVC) resin, Thermoplastic Polyolefin (TPO) compounds, and steel coil are exposed to global commodity cycles that often move out of step with local construction schedules and tender timelines. According to the Organisation for Economic Co-operation and Development's (OECD) 2025 Steel Outlook, fluctuations in pricing for strip and coil buyers, crucial for metal roofing manufacturers in ASEAN, may arise from capacity additions and inconsistent demand growth. In 2024 and 2025, those swings compressed supplier margins and pushed some contractors toward downgraded material choices when protecting bids became difficult. Manufacturers without hedging capacity, long-term sourcing arrangements, or some level of input integration remain more exposed during long project cycles in the ASEAN roofing market.

Other drivers and restraints analyzed in the detailed report include:

- Industrial, Logistics, and Data Centre Build Out Driving Insulated Metal Panel Demand

- Tropical Climate and Monsoon Exposure Reinforcing Premium Waterproofing Specification

- Skilled Installer Shortages Reducing Execution Quality and Slowing Specialized Roof Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal roofing accounted for 38% of the ASEAN roofing market in 2025, making it the largest material category across the region. Its position is tied to broad use in industrial warehousing, peri-urban housing, and public projects where speed of installation and cost per square meter remain central buying criteria. The category also benefits from the region's manufacturing and logistics build-out, as large-span, low-slope roofs commonly default to profiled metal sheets, sometimes paired with insulated composite layers. The OECD's 2025 steel outlook reinforces this backdrop by identifying ASEAN as one of the few regions where steel demand is expected to grow strongly through 2030. In the ASEAN roofing market, this gives metal roofing manufacturers a material supply base that remains strategically important even when prices are volatile.

Single-ply membranes are projected to grow at a 6.4% CAGR in the ASEAN roofing market through 2031, making them the fastest-growing material group in the forecast period. Their demand is being led by data centers and high-specification commercial roofs in Singapore, Jakarta, and Ho Chi Minh City, where heat-welded systems are chosen for low seam-failure risk and short replacement shutdown windows. Clay and concrete tiles still retain cultural and architectural relevance in Thai and Vietnamese housing. Still, they face pressure to be replaced by lighter fiber-cement and metal options in multi-story applications. Asphalt shingles remain more concentrated in premium residential pockets in Thailand, Malaysia, and the Philippines. At the same time, bituminous membranes continue to serve flat commercial and industrial roofs because they have a familiar installer base and lower equipment needs than welded systems. Wood roofing is declining, while polycarbonate, uPVC, and fiber-cement sheets are gaining traction in affordable housing renovation, especially where certified heat-reflective, low-maintenance products align with state-backed renovation demand.

Complete Report Scope:

- By Material Type

- Asphalt Shingles

- Clay & Concrete Tiles

- Metal Roofing

- Bituminous / Modified Bitumen Membranes

- Single-Ply Membranes (TPO, EPDM, and PVC)

- Wood

- Others

- By Construction Type

- New Construction

- Reroofing and Replacement

- By Application

- Residential

- Commercial

- Industrial

- Institutional

- Others

- By Geography

- Indonesia

- Vietnam

- Thailand

- Philippines

- Rest of ASEAN

List of Companies Covered in this Report:

- SCG Roofing

- Swissma Building Technologies

- Thung Hing

- Le Nam Megasheet

- LCP Group

- Kemudi Sempurna

- Asia Jaya Sepadu

- UGI

- PT. Insulated Panel Indonesia

- Subzero

- PT. Mandiri Mulia Makmur Abadi (MMMA)

- ROOFMAXX

- Kingspan

- Sika

- SOPREMA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Housing and Infrastructure Pipelines Expanding Roofing Demand

- 4.2.2 Green Building and Thermal Performance Rules Supporting Cool and Insulated Roofs

- 4.2.3 Industrial, Logistics, Cold Chain, and Data Center Build Out Increasing Demand for Insulated Panels and Membranes

- 4.2.4 Tropical Humidity, Monsoon Exposure, and Leakage Risk Lifting Waterproofing Intensity

- 4.2.5 Green Roofs, Siphonic Drainage, and Stormwater Features Adding Premium Content

- 4.2.6 Lower Intra-ASEAN Trade Barriers Improving Access to Premium Roofing Inputs

- 4.3 Market Restraints

- 4.3.1 Raw Material Cost Volatility in Bitumen, Resin, and Petrochemical Inputs Pressuring Margins

- 4.3.2 Skilled Installer Shortages Reducing Execution Quality and Slowing Specialized Roof Adoption

- 4.3.3 Competition from Lower Cost Substitute Materials Capping Pricing Power

- 4.3.4 Import Dependence and Uneven Regional Standards Complicating Supply Decisions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Cost Structure Analysis

- 4.8 Trend and Impacts of Roofing Replacements

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay & Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes (TPO, EPDM, and PVC)

- 5.1.6 Wood

- 5.1.7 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 Indonesia

- 5.4.2 Vietnam

- 5.4.3 Thailand

- 5.4.4 Philippines

- 5.4.5 Rest of ASEAN

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 SCG Roofing

- 6.4.2 Swissma Building Technologies

- 6.4.3 Thung Hing

- 6.4.4 Le Nam Megasheet

- 6.4.5 LCP Group

- 6.4.6 Kemudi Sempurna

- 6.4.7 Asia Jaya Sepadu

- 6.4.8 UGI

- 6.4.9 PT. Insulated Panel Indonesia

- 6.4.10 Subzero

- 6.4.11 PT. Mandiri Mulia Makmur Abadi (MMMA)

- 6.4.12 ROOFMAXX

- 6.4.13 Kingspan

- 6.4.14 Sika

- 6.4.15 SOPREMA

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類)

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類) 中東和北非屋頂材料市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東歐屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲屋頂材料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和北非屋頂材料市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東歐屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲屋頂材料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告

2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告