|

市場調查報告書

商品編碼

2072711

亞太地區屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Asia-Pacific Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

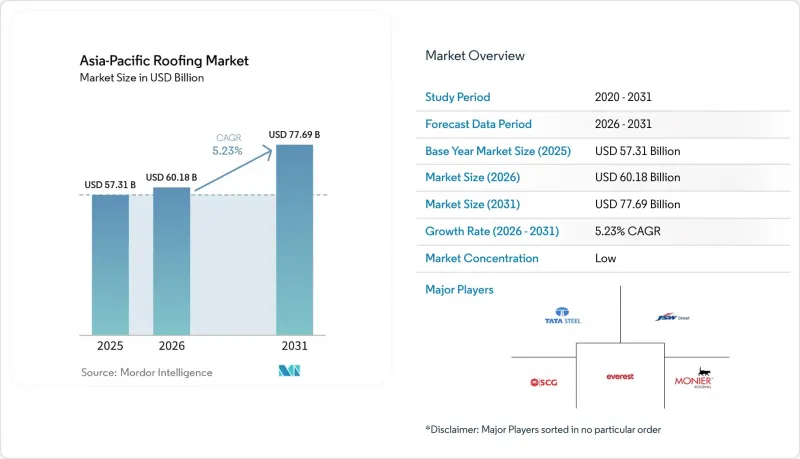

根據 Mordor Intelligence 預測,亞太地區屋頂材料市場規模預計將在 2025 年達到 573.1 億美元,2026 年達到 601.8 億美元,2031 年達到 776.9 億美元,2026 年至 2031 年的複合年成長率為 5.23%。

本報告按材料類型(瀝青瓦、粘土/混凝土瓦、金屬屋頂、瀝青/改性瀝青膜等)、施工類型(新建、屋頂更換/翻新)、應用領域(住宅、商業等)和地區(中國、日本、印度、澳大利亞、韓國以及亞太地區其他國家)進行細分。市場預測以美元計價。

亞太地區屋頂材料市場趨勢及洞察。

建築和基礎設施建設對屋頂材料的需求主導。

在亞太地區,建設活動仍然是屋頂材料市場需求的主要驅動力,因為交通走廊、物流園區、產業叢集和城市住宅都需要大量且持續的屋頂材料。印度和東南亞地區倉儲網路、廠房建設和公共基礎設施項目的擴張進一步推動了這一趨勢,這些項目更傾向於選擇金屬屋頂系統和其他可快速安裝的高擴充性屋頂形式。越南、泰國和印尼的工業園區也在促進這一需求,因為預製結構通常在專案週期的早期階段就對屋頂材料的選擇進行標準化,從而提高了供應商的知名度並帶來了回頭客。住宅主導的需求也進一步支撐了市場,因為大規模住宅項目傾向於購買重複購買的產品類型,而不是零散的一次性訂單。因此,亞太地區的屋頂材料市場不僅與週期性的建築趨勢密切相關,而且與更廣泛的採購體系密切相關,在這個體系中,合規性、安裝速度和生命週期耐久性以及初始成本的經濟性都備受重視。

屋頂更換和維修需求增加

在日本、澳洲和韓國等成熟經濟體中,屋頂更換和維修仍然是亞太地區屋頂市場的核心,因為幾十年前建成的大量建築正在被替換。在這些更換週期中,很少會選擇相同的材料。這是因為業主和承包商擴大利用屋頂更換專案來改善隔熱性能、減輕結構荷載或延長屋頂的使用壽命。這一趨勢支撐了對高階金屬系統、塗料和防水卷材的需求,尤其是在隔熱和防水維修整合到單一項目中時。在澳大利亞,主要製造商增加供應反映出他們對新建和住宅重建需求在當前週期內保持強勁的信心。因此,亞太地區的屋頂市場正受益於維修項目,因為與新建項目相比,翻新項目的需求波動性較小,且單一項目的規格價值更高。

原物料價格波動

原物料價格波動持續限制亞太地區屋頂材料市場的短期阻礙因素。這是因為鋼鐵、鋁和瀝青的成本會影響工廠的利潤率和競標紀律。依賴進口的市場更容易受到原物料成本劇烈波動的影響,因為當地的垂直整合程度有限,難以消化這些波動。更大的問題往往是專案延期而非徹底取消。這是因為屋頂工程定價的不確定性可能導致承包商和開發商推遲開工,直到競標價格穩定下來。瀝青相關產品也面臨類似的問題。這是因為即使終端需求強勁,由於煉油廠的配額和原油價格的波動,供應也可能緊張。雖然這種壓力不太可能消除亞太地區屋頂材料市場的需求,但可能會壓縮季度銷售量,並使產品組合更容易受到採購時機的影響。

細分市場分析

到2025年,瀝青瓦將佔據亞太地區屋頂材料市場31.8%的佔有率,這主要得益於其成本競爭力以及在價格敏感型住宅市場中易於安裝的優勢。在那些初始成本仍然優先於隔熱和使用壽命等性能要求的地區,瀝青瓦的地位將最為穩固。然而,隨著能源效率和反射率標準的不斷提高,瀝青瓦的中期發展受到明顯限制,因為傳統的深色瀝青瓦產品在現有的「冷屋頂」測量框架下表現不佳。在那些仍然重視建築傳統、陡峭屋頂設計和長使用壽命的國家,粘土瓦和混凝土瓦的需求仍然強勁。金屬屋頂材料也是亞太地區屋頂材料市場的主要銷售量類別,廣泛應用於工業建築和高階維修項目。製造商的回饋也印證了這一點,JSW鋼鐵公司報告稱,在2024-2025會計年度,其鍍鋁鋅鋼板和鍍鋅鋼板的銷量同比成長了14%。

單層薄膜,包括熱塑性聚烯(TPO)、乙丙橡膠 (EPDM) 和聚氯乙烯(PVC),預計到 2031 年將以 6.8% 的複合年成長率成長,成為該地區成長最快的材料類別。亞太地區屋頂材料市場規模的成長主要由商業和工業建築驅動,這些建築對低坡度系統、快速安裝和高隔熱性能的需求日益成長。 TPO 在資料中心和物流設施專案中尤其受歡迎,因為業主重視其接縫密封性、安裝速度和便於管理大面積面積的統一細節設計。 EPDM 仍然適用於成熟的維修項目,在這些項目中,耐候性和防水性比美觀更為重要。瀝青卷材繼續用於基礎設施和防水應用,而木材由於防火安全和永續性的考慮,在一些已開發市場的應用受到限制。 「其他」類別包括整合太陽能的屋頂、綠色屋頂和一些小眾的高性能系統。雖然這些產品的規模仍然相對較小,但它們在都市區項目中變得越來越重要。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 建築和基礎設施主導了對屋頂材料的需求。

- 屋頂更換和維修需求增加

- 過渡到節能冷屋頂系統

- 廣泛使用耐候耐用的屋頂材料。

- 地方政府強制使用冷屋頂正在加速高品質屋頂材料的採用。

- 資料中心擴建催生了對高性能屋頂系統的需求。

- 市場限制因素

- 原物料價格波動

- 各國之間監管規定的碎片化

- 屋頂工程勞動力和承包商短缺

- 污染和潮濕地區冷屋頂性能下降

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 成本結構分析

- 屋頂更換的趨勢和影響

- 波特五力模型

第5章 市場規模與成長預測

- 依材料類型

- 瀝青瓦

- 粘土磚和水泥瓦

- 金屬屋頂

- 瀝青基/改質瀝青基防水卷材

- 單層薄膜(TPO、EPDM、PVC)

- 樹

- 其他

- 依建築類型

- 新建工程

- 屋頂更換和維修

- 透過使用

- 住宅

- 商業

- 產業

- 公共設施

- 其他

- 按地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Tata Steel Colors

- JSW Steel Ltd

- Everest Industries Limited

- The Siam Cement Public Company Limited

- CSR Monier Roofing

- Bristile Roofing

- NS BlueScope Lysaght

- BlueScope Steel Pacific

- Dimond Roofing

- Kingspan Group

- Sika AG

- Oriental Yuhong

- KMEW Co., Ltd.

- Gerard Roofs

- Puyat Steel Corporation

- Tatalogam Lestari

- Kanmuri Roof

- Hoa Sen Home

- Nippon Steel(Thailand)Co., Ltd.

- Onduline

- LCP Building Products Pte Ltd

- Taiyo Kogyo Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific roofing market size is projected to be USD 57.31 billion in 2025, USD 60.18 billion in 2026, and reach USD 77.69 billion by 2031, growing at a CAGR of 5.23% from 2026 to 2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, and More), Construction Type (New Construction and Reroofing and Replacement), Application (Residential, Commercial, and More), and Geography (China, Japan, India, Australia, South Korea, and Rest of APAC). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Roofing Market Trends and Insights

Construction and Infrastructure-Led Roofing Demand

Construction activity remains a core demand engine for the Asia-Pacific roofing market, as transport corridors, logistics parks, industrial clusters, and urban housing all require large, recurring roof procurement volumes. India and Southeast Asia continue to support this pattern through expanding warehouse networks, factory shells, and public infrastructure programs that favor fast-installing metal systems and other scalable roofing formats. Industrial parks in Vietnam, Thailand, and Indonesia also strengthen this demand because pre-engineered structures typically standardize roof selection early in the project cycle, which improves supplier visibility and repeat business. Housing-led demand adds another layer of support because large residential programs concentrate purchases into repeatable product categories instead of fragmented one-off orders. This keeps the Asia-Pacific roofing market tied not only to cyclical building starts, but also to a broader procurement system in which compliance, installation speed, and lifecycle durability matter as much as first-cost economics.

Reroofing and Renovation Demand Expansion

Reroofing and renovation remain central to the Asia-Pacific roofing market because mature economies such as Japan, Australia, and South Korea are replacing large portions of building stock that entered service decades ago. These replacement cycles rarely result in like-for-like material selection because owners and contractors increasingly use reroofing projects to improve thermal performance, reduce structural load, or extend service life. That pattern supports premium metal systems, coated products, and membranes, especially when insulation and waterproofing upgrades are bundled into a single project. In Australia, supply additions by major producers reflect confidence that both new and replacement housing demand will remain active through the current cycle. The Asia-Pacific roofing market, therefore, benefits from renovation activity, as replacement work tends to be less volatile than new construction and often carries a higher specification value per project.

Raw-Material Price Volatility

Raw-material volatility remains a near-term constraint for the Asia-Pacific roofing market, as steel, aluminum, and bitumen costs affect both factory margins and tendering discipline. Import-dependent markets are more exposed because sudden swings in feedstock costs are harder to absorb when local backward integration is limited. The bigger issue is often project delay rather than outright cancellation, since uncertain roof package pricing can cause contractors and developers to postpone starts until bids stabilize. Bitumen-linked products face a similar problem because refinery allocation and oil price cycles can tighten supply even when end demand remains intact. This pressure does not eliminate demand from the Asia-Pacific roofing market, but it can compress quarterly volumes and make the product mix more sensitive to procurement timing.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Energy-Efficient and Cool-Roof Systems

- Weather Resilience and Durable-Roof Adoption

- Cross-Country Regulatory Fragmentation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Asphalt shingles held 31.8% of the Asia-Pacific roofing market share in 2025, supported by their cost competitiveness and straightforward installation across price-sensitive residential markets. Their position remains strongest where upfront affordability still outweighs thermal performance or long-life requirements in the purchase decision. At the same time, rising energy and reflectance standards create a clear medium-term limit, as conventional dark asphalt products perform worse under established cool-roof measurement frameworks. Clay and concrete tiles continue to hold meaningful demand in countries where architectural tradition, steep-slope design, and long service life remain important. Metal roofing also remains a major volume category in the Asia-Pacific roofing market, serving both industrial buildings and higher-specification renovation projects. Producer commentary supports that role, with JSW Steel reporting 14% year-on-year growth in galvalume and galvanized sales in FY 2024-25.

Single-ply membranes, including thermoplastic polyolefin (TPO), ethylene propylene diene monomer (EPDM), and polyvinyl chloride (PVC), are forecast to grow at a 6.8% CAGR through 2031, making them the fastest-rising material group in the region. The Asia-Pacific roofing market size for this segment is being lifted by commercial and industrial buildings where low-slope systems, faster installation, and higher thermal performance are increasingly specified. TPO is gaining particular traction in data-center and logistics projects because owners value seam integrity, installation speed, and the ability to manage large roof areas with consistent detailing. EPDM still fits mature renovation settings where weather exposure and waterproofing resilience matter more than aesthetic finish. Bituminous membranes continue to serve infrastructure and waterproofing-heavy applications, while wood remains limited by fire and sustainability concerns in several developed markets. The others category captures early adoption of solar-integrated roofing, green roof assemblies, and niche high-performance systems that are still small in volume but increasingly visible in urban projects.

Complete Report Scope:

- By Material Type

- Asphalt Shingles

- Clay & Concrete Tiles

- Metal Roofing

- Bituminous / Modified Bitumen Membranes

- Single-Ply Membranes (TPO, EPDM, and PVC)

- Wood

- Others

- By Construction Type

- New Construction

- Reroofing and Replacement

- By Application

- Residential

- Commercial

- Industrial

- Institutional

- Others

- By Geography

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Tata Steel Colors

- JSW Steel Ltd

- Everest Industries Limited

- The Siam Cement Public Company Limited

- CSR Monier Roofing

- Bristile Roofing

- NS BlueScope Lysaght

- BlueScope Steel Pacific

- Dimond Roofing

- Kingspan Group

- Sika AG

- Oriental Yuhong

- KMEW Co., Ltd.

- Gerard Roofs

- Puyat Steel Corporation

- Tatalogam Lestari

- Kanmuri Roof

- Hoa Sen Home

- Nippon Steel (Thailand) Co., Ltd.

- Onduline

- LCP Building Products Pte Ltd

- Taiyo Kogyo Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction and Infrastructure-Led Roofing Demand

- 4.2.2 Reroofing and Renovation Demand Expansion

- 4.2.3 Shift Toward Energy-Efficient and Cool-Roof Systems

- 4.2.4 Weather Resilience and Durable-Roof Adoption

- 4.2.5 Subnational Cool-Roof Mandates Accelerating Premium Roof Specifications

- 4.2.6 Data-Center Buildout Creating Demand for High-Performance Roofing Systems

- 4.3 Market Restraints

- 4.3.1 Raw-Material Price Volatility

- 4.3.2 Cross-Country Regulatory Fragmentation

- 4.3.3 Roofing Labor and Installer Shortages

- 4.3.4 Cool-Roof Performance Degradation in Polluted and Humid Zones

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Cost Structure Analysis

- 4.8 Trend and Impacts of Roofing Replacements

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay & Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes (TPO, EPDM, and PVC)

- 5.1.6 Wood

- 5.1.7 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Tata Steel Colors

- 6.4.2 JSW Steel Ltd

- 6.4.3 Everest Industries Limited

- 6.4.4 The Siam Cement Public Company Limited

- 6.4.5 CSR Monier Roofing

- 6.4.6 Bristile Roofing

- 6.4.7 NS BlueScope Lysaght

- 6.4.8 BlueScope Steel Pacific

- 6.4.9 Dimond Roofing

- 6.4.10 Kingspan Group

- 6.4.11 Sika AG

- 6.4.12 Oriental Yuhong

- 6.4.13 KMEW Co., Ltd.

- 6.4.14 Gerard Roofs

- 6.4.15 Puyat Steel Corporation

- 6.4.16 Tatalogam Lestari

- 6.4.17 Kanmuri Roof

- 6.4.18 Hoa Sen Home

- 6.4.19 Nippon Steel (Thailand) Co., Ltd.

- 6.4.20 Onduline

- 6.4.21 LCP Building Products Pte Ltd

- 6.4.22 Taiyo Kogyo Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類)

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類) 中東和北非屋頂材料市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東歐屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲屋頂材料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)東協屋頂材料市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和北非屋頂材料市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東歐屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲屋頂材料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)東協屋頂材料市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告

2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告