|

市場調查報告書

商品編碼

2072703

中東和北非屋頂材料市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East and North Africa Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

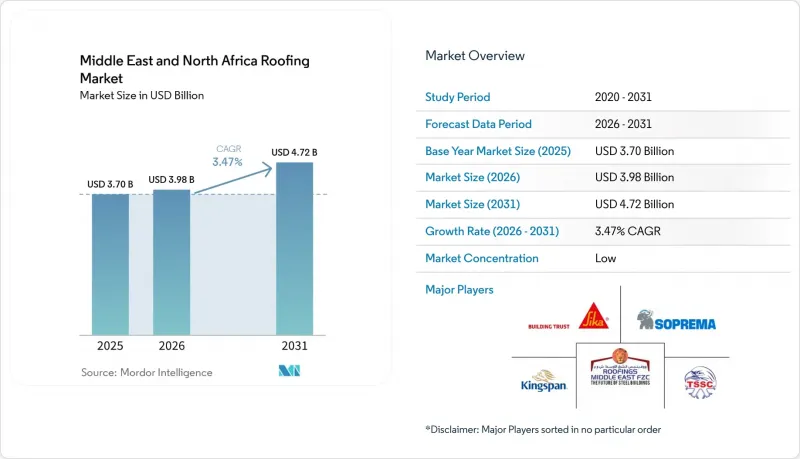

根據 Mordor Intelligence 預測,中東和北非的屋頂材料市場規模將從 2025 年的 37 億美元和 2026 年的 39.8 億美元成長到 2031 年的 47.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 3.47%。

本報告按材料(瀝青瓦、粘土/混凝土瓦、金屬屋頂等)、建築類型(新建、屋頂更換/翻新)、用途(住宅、商業、工業、公共及其他)和地區(沙烏地阿拉伯、阿拉伯聯合大公國、埃及等)進行分類。市場預測以美元計價。

中東及北非車頂材料市場趨勢及洞察

沙烏地阿拉伯的大規模項目、不斷擴大的住宅建設以及旅遊業對屋頂材料的需求主導。

沙烏地阿拉伯仍然是中東和北非屋頂材料市場需求的主要驅動力,這主要得益於不斷擴張的住宅建設和大規模旅遊項目。住宅建設項目推動了基礎屋頂材料的需求成長,而旅遊業和綜合用途開發項目則促使市場轉向對高性能屋頂系統的需求,這些系統對隔熱、隔音和太陽能整合等方面的要求也更加嚴格。這種市場格局的變化正在改變屋頂材料組合的價值結構,越來越多的項目需要的是符合特定主導的系統,而非基礎的通用材料。能夠滿足專案核准標準、保固要求和系統認證要求的供應商,相較於僅以產量取勝的供應商,擁有顯著優勢。因此,中東和北非屋頂材料市場受益於高銷量和先進技術的雙重優勢。

強制性能源法規促使屋頂隔熱材料和反射性屋頂材料得到更廣泛的應用。

在中東和北非的屋頂材料市場,能源法規如今已成為決定產品規格的直接因素。這是因為符合相關法規的要求已納入建築許可和設計核准流程。杜拜市政府已將新建平屋頂和低坡度屋頂的最低太陽反射率指數 (SRI) 設定為 78,阿布達比和卡達也引入了類似的建築性能標準。在沙烏地阿拉伯,《沙烏地阿拉伯建築標準法》對屋頂結構的熱傳導係數進行了限制,已發表的研究表明,在沙烏地阿拉伯所有氣候區,使用隔熱材料可以降低建築物的能耗。事實上,僅使用反射飾面材料正在逐漸失去市場佔有率,取而代之的是兼具膜材性能和隔熱性,且符合長期能源法規要求的屋頂結構。這推高了每個項目的平均材料成本,並推動了中東和北非屋頂材料市場向更高附加價值產品組合的轉變。

與鋼鐵、瀝青、聚合物和進口相關的原料成本波動。

在中東和北非的屋頂材料市場,原物料成本波動仍是限制利潤率擴張的最明顯阻礙因素之一。 2025年發表於《建築》(Buildings)雜誌的一項研究表明,當可靠的本地價格指標不足或延遲時,卡達的建築價格調整機制無法充分保護承包商的利益。即使本地價格短期內有所回落,金屬屋頂材料供應商仍容易受到全球鋼材價格、運費和進口平價波動的影響。這種風險在北非更為突出,因為進口原料會受到外匯波動和商品價格波動的影響。這種成本波動使得提案規格升級方案變得困難,並可能減緩整個中東和北非屋頂材料市場向高附加價值產品轉型的步伐。

細分市場分析

到2025年,瀝青/改質瀝青防水卷材將佔總需求的33.5%,成為中東和北非屋頂材料市場中最大的材料類別。其主導地位得益於其卓越的耐熱性、在承包商中的廣泛認可,以及在沙烏地阿拉伯和埃及等國的在地化供應鏈。這些卷材也已廣泛應用於住宅和標準商業建築,在這些應用中,買家仍然優先考慮初始成本和成熟的安裝方法。儘管具有這些優勢,但隨著專案業主對更強防水性能、更高反射率和更完善的保固服務提出更高的要求,材料結構正逐漸轉向高附加價值系統。這種轉變正在推動中東和北非屋頂材料產業的增值成長,儘管總噸位成長仍然較為溫和。

單層薄膜,包括熱塑性聚烯(TPO)、乙丙橡膠 (EPDM) 和聚氯乙烯(PVC),是成長最快的材料類別,預計到 2031 年將以 5.8% 的複合年成長率成長。它們的吸引力在於與屋頂太陽能發電系統相容,在現有建築中安裝更加清潔,並且符合沿岸地區商業項目的「冷屋頂」法規。根據杜拜水電局 (DEWA) 的一份報告,到 2025 年,杜拜將有 8430 棟建築接入總合725 兆瓦的屋頂太陽能發電系統,這凸顯了市場對與已安裝系統兼容並滿足保固要求的屋頂結構的高需求。金屬屋頂在工業設施中也扮演著重要角色。同時,粘土瓦和混凝土瓦在北非和中東部分地區仍然十分重要,預計屋頂材料市場將繼續保持多元化,而不是由單一材料主導。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場趨勢與分析

- 市場概覽

- 市場促進因素

- 沙烏地阿拉伯的巨型計畫、不斷擴大的住宅建設以及旅遊業主導的屋頂需求

- 強制性能源標準導致屋頂隔熱材料和反射性屋頂材料的使用量增加。

- 採用保溫金屬屋面板的工業、物流和倉儲設施的建設正在不斷擴大。

- 高溫氣候區商業設施平屋頂的防水與維修週期

- 太陽能屋頂的具體要求推動了對太陽能屋頂系統的需求成長。

- 旨在提高房屋抵禦暴雨和洪水能力的維修工程正在加速屋頂的更換,主要集中在防水方面。

- 市場限制因素

- 與鋼鐵、瀝青、聚合物和進口相關的投入成本波動極大。

- 先進屋頂系統認證安裝人員短缺

- 由於夏季高溫和高溫作業限制,安裝工期縮短了。

- 價格主導的規格決策正在減緩高階薄膜的普及速度。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 成本結構分析

- 屋頂材料更換的趨勢和影響

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 瀝青瓦

- 粘土瓦和混凝土瓦

- 金屬屋頂

- 瀝青基/改質瀝青基防水卷材

- 單層薄膜(TPO、EPDM、PVC)

- 樹

- 其他屋頂材料

- 依建築類型

- 新建工程

- 屋頂更換和維修

- 透過使用

- 住宅

- 商業

- 產業

- 公共設施

- 其他用途

- 按地區

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 埃及

- 摩洛哥

- 卡達

- 中東和北非其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sika

- Soprema

- Kingspan

- TSSC Group

- Roofings Middle East

- Emirates Industrial Panel

- Litco Industries

- Compass Waterproofing

- SECC Insulation

- Target Engineering Specialized Works

- Maghreb Steel

- Pyramids Steel

- Al-Majd International for Bituminous Insulation

- SAHARA Insulation Factory

- Saudi Insulation Factory

- BMI Group

- Saint-Gobain

- GAF

- Owens Corning

- Arabian Tiles Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east and north africa roofing market size is projected to expand from USD 3.70 billion in 2025 and USD 3.98 billion in 2026 to USD 4.72 billion by 2031, registering a CAGR of 3.47% between 2026 to 2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, and More), by Construction Type (New Construction and Reroofing and Replacement), by Application (Residential, Commercial, Industrial, Institutional, and Others), and by Geography (Saudi Arabia, United Arab Emirates, Egypt, and More). The Market Forecasts are Provided in Terms of Value (USD).

Middle East and North Africa Roofing Market Trends and Insights

Saudi Giga-Projects, Housing Expansion, and Tourism-Led Roof Demand

Saudi Arabia remains the clearest demand engine for the Middle East and North Africa roofing market, as housing expansion and large destination projects are advancing simultaneously. Housing programs are increasing baseline roof demand, while tourism and mixed-use developments are pushing projects toward higher-performing systems with stronger thermal, acoustic, and solar integration requirements. This mix is changing the value profile of the roof package, as more projects now require specification-led systems rather than basic commodity materials. Suppliers that meet project approval standards, warranty expectations, and system certification requirements are in a stronger position than those that compete only on output volume. As a result, the Middle East and North Africa roofing market is benefiting from both high volume and richer technical content.

Mandatory Energy Codes Increasing Roof Insulation and Reflective Roof Adoption

Energy regulation is now a direct specification force in the Middle East and North Africa roofing market because compliance is built into permit and design approval processes. Dubai Municipality requires a minimum Solar Reflectance Index (SRI) of 78 for flat and low-sloped roofs in new construction, and comparable building performance systems are active in Abu Dhabi and Qatar. In Saudi Arabia, the Saudi Building Code sets limits on roof assembly thermal transmittance, and published research shows that insulation can reduce building energy use across the country's climate zones. The practical effect is that reflective finishes alone are losing ground to roof assemblies that combine membrane performance with insulation and longer-term energy compliance. This is raising the average material bill per project and supporting a higher-value product mix across the roofing market in the Middle East and North Africa.

Volatile Steel, Bitumen, Polymer, and Import-Linked Input Costs

Input cost volatility remains one of the clearest limits on margin expansion in the Middle East and North Africa roofing market. A 2025 study in Buildings found that construction price adjustment mechanisms in Qatar do not fully protect contractors when reliable local pricing benchmarks are weak or delayed. Metal roofing suppliers also remain exposed to movements in global steel pricing, freight, and import parity, even when local prices soften for short periods. The risk is more pronounced in North Africa because imported raw materials can be affected by currency fluctuations and commodity price movements. This cost instability makes specification upgrades harder to sell and can delay the conversion of projects into higher-value products across the Middle East and North Africa roofing market.

Other drivers and restraints analyzed in the detailed report include:

- Industrial, Logistics, and Warehouse Build-Out Supporting Insulated Metal Roof Panels

- Waterproofing Upgrade Cycle for Flat Roofs in Hot-Climate Commercial Assets

- Price-Led Specification Behavior Slowing Premium Membrane Conversion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bituminous / modified bitumen membranes accounted for 33.5% of total demand in 2025, making them the largest material group in the Middle East and North Africa roofing market. Their lead still rests on proven heat resistance, wide contractor familiarity, and localized supply chains in countries such as Saudi Arabia and Egypt. These membranes are also well established across residential and standard commercial applications, where buyers still put strong weight on initial cost and known installation practices. Even with this lead, the material mix is gradually shifting toward higher-value systems as project owners request stronger waterproofing, greater reflectivity, and warranty support. That shift is boosting value growth in the Middle East and North Africa roofing industry, even as total tonnage rises at a more moderate pace.

Single-ply membranes, including thermoplastic polyolefin (TPO), ethylene propylene diene monomer (EPDM), and polyvinyl chloride (PVC), are the fastest-growing material category at a 5.8% CAGR through 2031. Their appeal lies in rooftop solar compatibility, cleaner installation on occupied buildings, and compliance with cool-roof rules in Gulf commercial projects. Dubai Electricity and Water Authority reported that 725 megawatts of rooftop solar had been connected across 8,430 buildings in Dubai by 2025, underscoring demand for roof assemblies compatible with mounting systems and meeting warranty requirements. Metal roofing also plays an important role in industrial facilities. At the same time, clay and concrete tiles remain relevant in parts of North Africa and the Middle East, and the roofing market will remain mixed rather than single-material-led.

Complete Report Scope:

- By Material Type

- Asphalt Shingles

- Clay and Concrete Tiles

- Metal Roofing

- Bituminous / Modified Bitumen Membranes

- Single-Ply Membranes (TPO, EPDM, and PVC)

- Wood

- Other Roofing Materials

- By Construction Type

- New Construction

- Reroofing and Replacement

- By Application

- Residential

- Commercial

- Industrial

- Institutional

- Other Applications

- By Geography

- Saudi Arabia

- United Arab Emirates

- Egypt

- Morocco

- Qatar

- Rest of the Middle East and North Africa

List of Companies Covered in this Report:

- Sika

- Soprema

- Kingspan

- TSSC Group

- Roofings Middle East

- Emirates Industrial Panel

- Litco Industries

- Compass Waterproofing

- SECC Insulation

- Target Engineering Specialized Works

- Maghreb Steel

- Pyramids Steel

- Al-Majd International for Bituminous Insulation

- SAHARA Insulation Factory

- Saudi Insulation Factory

- BMI Group

- Saint-Gobain

- GAF

- Owens Corning

- Arabian Tiles Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Saudi Giga-Projects, Housing Expansion, and Tourism-Led Roof Demand

- 4.2.2 Mandatory Energy Codes Increasing Roof Insulation and Reflective Roof Adoption

- 4.2.3 Industrial, Logistics, and Warehouse Build-Out Supporting Insulated Metal Roof Panels

- 4.2.4 Waterproofing Upgrade Cycle for Flat Roofs in Hot-Climate Commercial Assets

- 4.2.5 Solar-Ready Rooftop Specifications Increasing Demand for PV-Compatible Roofing Systems

- 4.2.6 Extreme Rain and Flood Resilience Retrofits Accelerating Waterproofing-Led Reroofing

- 4.3 Market Restraints

- 4.3.1 Volatile Steel, Bitumen, Polymer, and Import-Linked Input Costs

- 4.3.2 Shortage of Certified Installers for Advanced Roof Systems

- 4.3.3 Summer Heat and Hot-Work Restrictions Narrowing Installation Windows

- 4.3.4 Price-Led Specification Behavior Slowing Premium Membrane Conversion

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Cost Structure Analysis

- 4.8 Trend and Impacts of Roofing on Replacements

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay and Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes (TPO, EPDM, and PVC)

- 5.1.6 Wood

- 5.1.7 Other Roofing Materials

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Egypt

- 5.4.4 Morocco

- 5.4.5 Qatar

- 5.4.6 Rest of the Middle East and North Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sika

- 6.4.2 Soprema

- 6.4.3 Kingspan

- 6.4.4 TSSC Group

- 6.4.5 Roofings Middle East

- 6.4.6 Emirates Industrial Panel

- 6.4.7 Litco Industries

- 6.4.8 Compass Waterproofing

- 6.4.9 SECC Insulation

- 6.4.10 Target Engineering Specialized Works

- 6.4.11 Maghreb Steel

- 6.4.12 Pyramids Steel

- 6.4.13 Al-Majd International for Bituminous Insulation

- 6.4.14 SAHARA Insulation Factory

- 6.4.15 Saudi Insulation Factory

- 6.4.16 BMI Group

- 6.4.17 Saint-Gobain

- 6.4.18 GAF

- 6.4.19 Owens Corning

- 6.4.20 Arabian Tiles Company

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類)

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類) 中東歐屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲屋頂材料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)東協屋頂材料市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東歐屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲屋頂材料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)東協屋頂材料市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告

2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告