|

市場調查報告書

商品編碼

2072710

南美洲屋頂材料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)South America Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

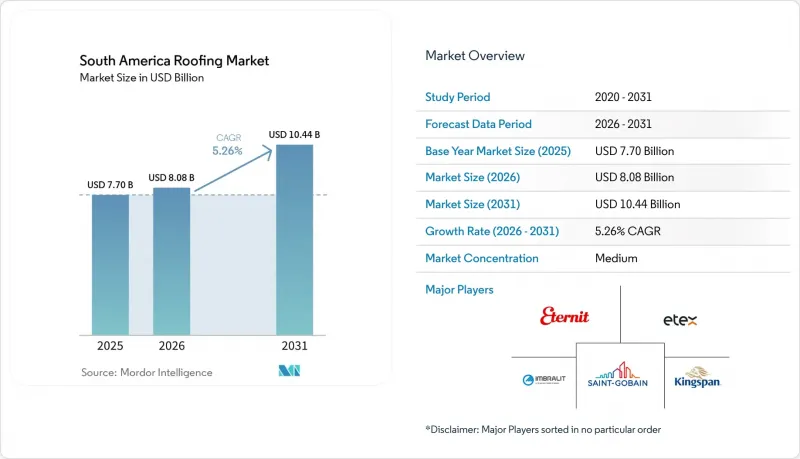

根據 Mordor Intelligence 預測,南美屋頂材料市場規模預計在 2025 年達到 77 億美元,2026 年達到 80.8 億美元,到 2031 年達到 104.4 億美元,2026 年至 2031 年的複合年成長率為 5.26%。

本報告按材料類型(瀝青瓦、粘土/混凝土瓦、金屬屋頂材料、瀝青/改性瀝青膜等)、施工類型(新建、屋頂更換/維修等)、應用領域(住宅、商業等)和地區(巴西、阿根廷、哥倫比亞、智利、秘魯和其他南美國家)進行細分。市場預測以美元計價。

南美洲屋頂材料市場趨勢與洞察

補貼住宅計畫和尚未開工的住宅建設項目。

巴西的「我的家,我的生活」(Minha Casa Minha Vida)計劃於2025年5月選定13萬套住宅,供月收入低於2850雷亞爾(約合502美元)的家庭使用。該計劃將每套住房的補貼上限從14萬雷亞爾(約24,659.6美元)提高至18,05萬雷亞爾(約3,1793.3美元)。這項機制為南美洲屋頂市場維持了需求空間,因為補貼住宅的屋頂需求很大程度上並不依賴標準房屋抵押貸款。哥倫比亞和秘魯類似的低收入住宅市場為南美洲入門級住宅屋頂需求提供了更廣泛的區域基礎。該市場的產品組合也在發生變化,住宅面積的縮小和成本上限的收緊導致人們更傾向於選擇纖維水泥和平面混凝土屋頂,而不是傳統的粘土瓦。已經擴大該領域產能的製造商處於更有利的地位。此外,Eternit 投資 1.87 億雷亞爾(3,290 萬美元)的 Caukaia 工廠於 2024 年完成了其第一年的名義產能運作,進一步鞏固了其供應方面的優勢。

由於老舊瓦屋頂庫存積壓,更換需求增加

南美洲的大多數住宅建築建於2000年之前,當時屋頂的耐久性和隔熱性能並未像今天這樣受到重視。 1980年至2000年間安裝的黏土和陶瓷屋頂如今已超過30年,導致巴西、阿根廷和哥倫比亞的屋頂更換需求呈現系統性成長。這對南美洲的屋頂市場產生了重大影響,因為更換舊屋頂的住宅擴大選擇纖維水泥、塗層金屬或輕質混凝土,而不是直接更換為陶瓷屋頂。這種升級趨勢在巴西已經顯現,Eternit公司2025年第一季的纖維水泥屋面板銷售量達到16.76萬噸,年增15.1%。這一成長部分源於巴西北部和東北部地區需求的增加,這些地區的老舊屋頂更換工作正在穩步推進。此外,由於屋頂更換專案通常不僅包括可見的屋頂材料,還包括底層材料、屋脊防水層和改進的緊固系統,因此這種更換週期也有助於擴大南美洲屋頂材料市場的收入來源。

高利率抑制了私人建築工程的開工。

預計到2026年初,巴西的法定工業利率(selic)將達到15%,為2006年以來的最高水平,這將對私人建設活動構成明顯的限制。根據已提交的草案,到2025年年中,巴西新建工程量將下降6.2%,全國都將出現下滑。這解釋了為何面向中等收入群體的私人項目仍然面臨挑戰。開發商還必須應對比法定工業利率高出3%至3.5%的資金籌措,以及家庭購買力未能跟上建築成本通膨步伐的問題。在南美屋頂市場,這意味著中等收入購屋者的私人住宅訂單成長放緩,專案工期延長。然而,巴西央行在2026年3月發布的「焦點」(Focus)調查預測,到年底法定工業利率將降至12.13%,這意味著後期降息或許能夠緩解部分風險。

細分市場分析

截至2025年,黏土和混凝土屋瓦將佔南美洲屋頂市場以金額為準的34.2%,成為該市場最大的材料類別。其在巴西、阿根廷和哥倫比亞的主導地位尤為突出,這些國家的陶瓷屋頂材料持續符合當地的建築規範和較低的住宅預算。金屬屋頂材料是成長最快的材料類別,預計2026年至2031年的複合年成長率將達到6.4%。這一成長速度與物流倉庫、冷庫、礦業相關設施和農業工業建築密切相關。南美洲黏土和混凝土屋頂市場仍然主要受大眾住宅需求的驅動。同時,在非住宅項目中,成長的主要驅動力正轉向塗層和保溫金屬屋頂系統。智利和哥倫比亞的保溫法規正在推動這一趨勢,工業和公共部門的買家也越來越要求從專案設計的早期階段就獲得更詳細的屋頂性能數據。

在南美洲屋頂市場,纖維水泥仍然是經濟型住宅屋頂的主要選擇,而巴西是該地區規模最大、發展最成熟的纖維水泥屋頂市場之一。領先的製造商之一Eternit報告稱,其2024年纖維水泥年銷售量將達到633,242噸,凸顯了該市場在巴西的規模和滲透率。雖然瀝青和改質瀝青防水卷材在許多商業平屋頂中仍然佔據主導地位,但優先考慮太陽反射率和接縫可靠性的新計畫擴大採用單層系統,特別是熱塑性聚烯(TPO)。乙丙橡膠(EPDM)在高階商業應用中仍然佔據重要地位,而聚氯乙烯(PVC)在需要耐化學腐蝕的環境中繼續發揮關鍵作用。瀝青瓦和木質屋頂材料在南美洲屋頂市場中所佔佔有率相對較小。瀝青瓦的應用僅限於都市區維修等特定領域,而木質屋頂材料由於存在火災風險,其普及程度受到限制。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 補貼住宅項目和住宅供應延誤

- 由於屋頂老化,需要更換屋頂,其中瓦片屋頂是主要類型。

- 工業建築中金屬和保溫屋頂材料的採用

- 更嚴格的屋頂隔熱性能標準

- 極端天氣事件後,更換屋頂以提高應對氣候變遷的能力。

- 在氣候炎熱的城市中,冷屋頂維修的經濟可行性

- 市場限制因素

- 高利率抑制了私人建築工程的開工。

- 鋼材、膜材和瀝青產品的投入成本波動

- 先進屋頂系統承包商的能力差距

- 非官方的自學途徑正在減緩高階系統的普及。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 成本結構分析

- 屋頂更換的趨勢和影響

- 波特五力模型

第5章 市場規模與成長預測

- 材料類型

- 瀝青瓦

- 粘土磚和水泥瓦

- 金屬屋頂

- 瀝青基/改質瀝青基防水卷材

- 單層

- 木頭

- 其他

- 依建築類型

- 新建工程

- 屋頂更換和維修

- 透過使用

- 住宅

- 商業的

- 產業

- 公共設施

- 其他

- 按地區

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Eternit

- Saint-Gobain Brasilit

- Imbralit

- Etex

- Kingspan

- Ternium

- Cintac

- Tupemesa

- Ajover

- Sika

- Viapol

- Danica

- Multilit

- Aceros Arequipa

- Acesco Ecuador

- Onduline

- Hunter Douglas Architectural

- Rooftec Telhas Metalicas

- Thermo-Iso

- Brastetto

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america roofing market size is projected to be USD 7.70 billion in 2025, USD 8.08 billion in 2026, and reach USD 10.44 billion by 2031, growing at a CAGR of 5.26% from 2026 to 2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, and More), Construction Type (New Construction, Reroofing and Replacement), Application (Residential, Commercial, and More), & Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

South America Roofing Market Trends and Insights

Subsidized Housing Pipelines and Housing Backlog

Brazil's Minha Casa Minha Vida program selected 130,000 new housing units in May 2025 for families with a monthly gross income below BRL 2,850 (USD 502). The same announcement set per-unit subsidy ceilings at BRL 140,000 (USD 24,659.6) to BRL 180,500 (USD 31,793.3). This structure keeps a demand corridor open for the South America roofing market because a large share of roofing demand in subsidized housing is not tied to standard mortgage availability. Comparable affordable housing channels in Colombia and Peru create a broader regional base for entry-level residential roofing demand within the South America roofing market. The mix in this channel is also shifting, with tighter unit sizes and cost ceilings favoring fiber-cement and flat concrete systems over traditional ceramic clay tiles. Manufacturers that already expanded capacity for this tier are in a stronger position, and Eternit's BRL 187 million (USD 32.9 million) Caucaia plant completed its first full year of nominal-capacity operation in 2024, reinforcing that supply-side advantage.

Replacement-Led Demand from Aging Tile-Heavy Roof Stock

A large share of South America's residential buildings were erected before 2000, when roofing durability and thermal performance were not consistently addressed as they are today. As clay and ceramic roofs installed during the 1980-2000 building cycle age past 30 years, replacement demand is becoming more systematic across Brazil, Argentina, and Colombia. This matters for the South America roofing market because homeowners replacing old roofs are increasingly choosing fiber cement, coated metal, or lightweight concrete instead of direct ceramic replacements. That trade-up pattern is already visible in Brazil, where Eternit's Q1 2025 fiber-cement roofing panel sales rose 15.1% year on year to 167,600 tonnes, with gains linked in part to North and Northeast Brazil, where older roofs are being replaced. The replacement cycle also expands the revenue pool for the South America roofing market because reroofing projects often include underlayments, ridge capping, and improved fastening systems rather than only the visible roof covering.

High Interest Rates Limiting Private Construction Starts

Brazil's Selic rate stood at 15% in early 2026, which was the highest level since 2006 and a clear constraint on private construction activity. The supplied draft noted that new construction starts declined 6.2% through mid-2025, with weakness seen across all Brazilian regions, which explains why mid-income private projects remain under pressure. Developers are also dealing with financing costs at Selic plus 3% to 3.5% and with household purchasing power that has not kept pace with construction cost inflation. In the South American roofing market, that means slower order conversion in private housing and longer project timelines for developers targeting middle-income buyers. Even so, the Central Bank's Focus survey in March 2026 pointed to a year-end Selic rate of 12.13%, suggesting some easing risk if rate cuts materialize later in the period.

Other drivers and restraints analyzed in the detailed report include:

- Metal and Insulated Roofing Adoption in Industrial Buildings

- Tightening Roof Thermal Efficiency Standards

- Input-Cost Volatility in Steel, Membranes, and Asphaltic Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clay & concrete tiles held a 34.2% value share in 2025, making them the largest material group in the South American roofing market. Their leading position remains strongest in Brazil, Argentina, and Colombia, where ceramic roofing continues to align with local building practices and entry-level residential budgets. Metal roofing is the fastest-growing material segment with a 6.4% CAGR through 2026-2031, and that rate is closely tied to logistics warehouses, cold storage, mining-support assets, and agro-industrial buildings. The South America roofing market size for clay & concrete tiles remained anchored by mass-market residential demand. At the same time, the growth premium shifted toward coated and insulated metal systems in non-residential projects. Thermal regulations in Chile and Colombia are reinforcing this move, as industrial and institutional buyers now need better-documented roof performance from the outset of project design.

Fiber cement remains the main affordable residential roofing alternative in the South America roofing market, with Brazil representing one of the largest and most established fiber-cement roofing markets in the region. As one of the leading manufacturers, Eternit reported full-year fiber-cement sales volume of 633,242 tonnes in 2024, highlighting the significant scale and depth of the segment in Brazil. Bituminous and modified bitumen membranes continue to dominate many flat commercial roofs, while single-ply systems, especially Thermoplastic Polyolefin (TPO), are gaining adoption in newer projects that prioritize solar reflectivity and seam reliability. Ethylene Propylene Diene Monomer (EPDM) remains relevant in premium commercial applications, while Polyvinyl Chloride (PVC) continues to be important in environments where chemical resistance is required. Asphalt shingles and wood roofing keep smaller positions in the South America roofing market, with shingles tied to urban renovation niches and wood limited by fire-risk concerns in broader adoption.

Complete Report Scope:

- By Material Type

- Asphalt Shingles

- Clay & Concrete Tiles

- Metal Roofing

- Bituminous / Modified Bitumen Membranes

- Single-Ply Membranes

- Wood

- Others

- By Construction Type

- New Construction

- Reroofing and Replacement

- By Application

- Residential

- Commercial

- Industrial

- Institutional

- Others

- By Geography

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

List of Companies Covered in this Report:

- Eternit

- Saint-Gobain Brasilit

- Imbralit

- Etex

- Kingspan

- Ternium

- Cintac

- Tupemesa

- Ajover

- Sika

- Viapol

- Danica

- Multilit

- Aceros Arequipa

- Acesco Ecuador

- Onduline

- Hunter Douglas Architectural

- Rooftec Telhas Metalicas

- Thermo-Iso

- Brastetto

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subsidized Housing Pipelines and Housing Backlog

- 4.2.2 Replacement Demand from Aging Tile-Heavy Roof Stock

- 4.2.3 Metal and Insulated Roofing Adoption in Industrial Buildings

- 4.2.4 Tightening Roof Thermal Efficiency Standards

- 4.2.5 Climate-Resilience Reroofing After Extreme Weather Events

- 4.2.6 Cool-Roof Retrofit Economics in Hot-Climate Cities

- 4.3 Market Restraints

- 4.3.1 High Interest Rates Limiting Private Construction Starts

- 4.3.2 Input-Cost Volatility in Steel, Membranes, and Asphaltic Products

- 4.3.3 Installer Capability Gaps for Advanced Roofing Systems

- 4.3.4 Informal Self-Build Channel Slows Premium-System Adoption

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Cost Structure Analysis

- 4.8 Trend and Impacts of Roofing Replacements

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay & Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes

- 5.1.6 Wood

- 5.1.7 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Colombia

- 5.4.4 Chile

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Eternit

- 6.4.2 Saint-Gobain Brasilit

- 6.4.3 Imbralit

- 6.4.4 Etex

- 6.4.5 Kingspan

- 6.4.6 Ternium

- 6.4.7 Cintac

- 6.4.8 Tupemesa

- 6.4.9 Ajover

- 6.4.10 Sika

- 6.4.11 Viapol

- 6.4.12 Danica

- 6.4.13 Multilit

- 6.4.14 Aceros Arequipa

- 6.4.15 Acesco Ecuador

- 6.4.16 Onduline

- 6.4.17 Hunter Douglas Architectural

- 6.4.18 Rooftec Telhas Metalicas

- 6.4.19 Thermo-Iso

- 6.4.20 Brastetto

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類)

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類) 中東和北非屋頂材料市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東歐屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)東協屋頂材料市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和北非屋頂材料市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東歐屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)東協屋頂材料市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告

2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告