|

市場調查報告書

商品編碼

2066752

美國屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)United States Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

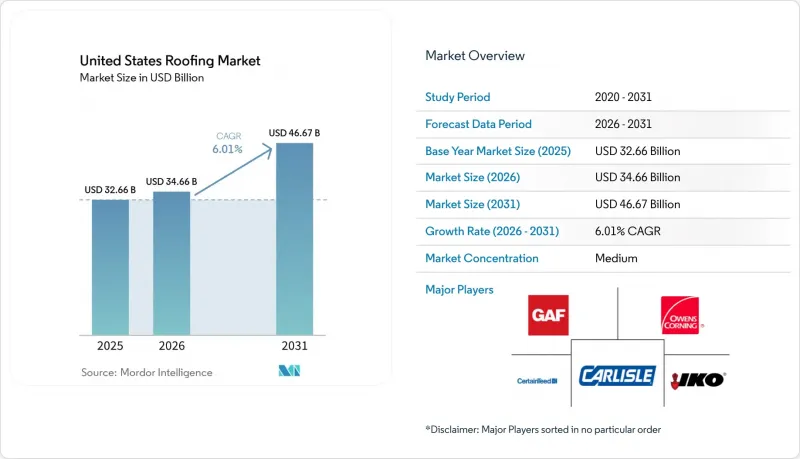

根據 Mordor Intelligence 預測,美國屋頂市場規模將從 2025 年的 326.6 億美元成長到 2026 年的 346.6 億美元,然後在 2031 年達到 466.7 億美元,2026 年至 2031 年的複合年成長率為 6.01%。

本報告按材料類型(瀝青瓦、粘土/混凝土瓦等)、施工類型(新建、屋頂更換、維修)、應用領域(住宅、商業、工業、公共及其他)和地區(東北部、中西部、東南部、西部和西南部)進行細分。市場預測以美元計價。

美國屋頂材料市場趨勢與洞察

屋頂材料庫存老化和更換週期延長,導致屋頂更換需求增加。

美國超過三分之一的自住住宅建於2000年之前,到2025年,屋頂的平均使用壽命將超過17年,這意味著數百萬個屋頂將超過其正常使用壽命。這種人口結構的變化確保了承包商的穩定業務,即使住宅開工量放緩。住宅在拆除現有屋頂時,擴大選擇升級為複合瓦或金屬屋頂,使專案價值實現兩位數的成長。保險公司現在要求在續保房齡超過15年的住宅時進行屋頂檢查,從而縮短了從損壞到維修的時間。因此,穩定的屋頂翻新需求支撐著美國屋頂材料市場的基礎。

由於暴風雨和冰雹造成的損壞,保險公司承擔的屋頂維修費用增加。

2024年至2025年間,德克薩斯州、奧克拉荷馬州和愛荷華州遭遇強烈對流風暴,導致屋頂相關保險理賠金額超過150億美元。為此,保險公司強制要求在高風險地區使用UL 2218 4級認證的抗衝擊屋頂材料。雖然這些優質產品的價格高出約18%,但住宅可獲得大幅保費折扣,促使他們更多地購買利潤更高的材料。此外,颶風伊恩過後,佛羅裡達州修訂了抗風標準,迫使不符合標準的屋頂提前更換。這些因素共同作用,加速了屋頂更換週期,並提高了每平方公尺屋頂的價值。

技術純熟勞工短缺限制了承包商訂單的能力,並推高了成本。

儘管時薪已提高至 28 美元,屋頂公司預計 2025 年的空置率仍將達到 12% 。人手不足在寒冷地區最為嚴重,這些地區老化勞動力難以補充。承包商正在投資機器人施工設備和物料升降機以彌補人手不足,但設備成本的增加推高了營運成本。工期延長 8 至 12 週迫使一些屋主推遲項目,導致短期工作量減少,並減緩了美國屋頂市場的成長。

細分市場分析

到2025年,瀝青瓦將佔據美國屋頂市場58.6%的佔有率,並繼續保持其在所有屋頂材料中的領先地位。這一規模反映了廣泛的承包商網路、成熟的安裝方法、強大的住宅分銷網路以及仍然高度依賴瓦片更換的屋頂更換週期。根據歐文斯科寧公司預測,2024年美國瀝青瓦市場總面積將達1.6億平方米,其中1.35億平方米將用於屋頂更換和維修。這表明,市場規模的很大一部分依賴定期更換工作,而非新建工程。歐文斯科寧公司也指出,到2025年,複合瓦產品將佔瓦片需求的95%,這表明美國屋頂市場已經開始從標準的三片式瓦片轉向更高附加價值的複合瓦系統。這一構成比至關重要,因為複合瓦產品售價更高、抗衝擊性更強,並且更能滿足易受冰雹災害影響的州的保險公司要求。

美國單層膜屋頂市場預計到2031年將以7.69%的複合年成長率成長,成為成長最快的建築材料類別。這一成長反映了低坡度商業建築對建築規範合規性的日益成長的需求,因為與許多傳統替代方案相比,反射性熱塑性聚烯(TPO)、乙丙橡膠(EPDM)和聚氯乙烯(PVC)系統在效率和維護方面更勝一籌。加州目前的建築規範趨勢和聯邦能源效率標準正在推動屋頂規範向這些系統轉變,尤其是在業主希望在同一項目中既滿足法規要求又降低製冷負荷的情況下。 GAF位於喬治亞瓦爾多斯塔的佔地42.5萬平方英尺的熱塑性聚烯(TPO)工廠於2024年9月投產,這表明該製造商為應對這一轉變而大幅提高了產能。金屬、改質瀝青、瓦片、木材和其他材料在某些地區的細分市場仍然佔據重要地位。然而,在美國屋頂材料市場,瀝青瓦在銷售方面仍然佔據主導地位,而防水卷材預計將在未來實現最強勁的成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場洞察與市場動態

- 市場概覽

- 市場促進因素

- 屋頂老化和更換週期延長,推高了屋頂更換的需求。

- 由於暴風雨和冰雹造成的破壞,保險公司承擔的維修和屋頂更換費用增加。

- 能源效率的提高推動了對冷屋頂和高性能隔熱系統需求的成長。

- 物流倉庫和資料中心的增加推動了商業屋頂工程的擴張。

- 採用可安裝太陽能發電系統的屋頂材料和整合式屋頂太陽能發電系統的屋頂材料,導致維修成本增加。

- 市場限制因素

- 技術純熟勞工短缺限制了承包商的能力,並增加了安裝成本。

- 瀝青瓦、金屬和隔熱材料等原料價格的波動給利潤率帶來了壓力。

- 由於授權、保險和擔保要求,專案工期可能會延長。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 材料類型

- 瀝青瓦

- 粘土磚和水泥瓦

- 金屬屋頂

- 瀝青基/改質瀝青基防水卷材

- 單層薄膜(TPO、EPDM、PVC)

- 樹

- 其他

- 依建築類型

- 新建工程

- 屋頂更換和維修

- 透過使用

- 住宅

- 商業

- 產業

- 對於機構投資人而言

- 其他

- 按地區

- 東北

- 中西部

- 東南部

- 西

- 西南

第6章 競爭情勢

- 策略趨勢

- 市佔率分析

- 公司簡介

- GAF Materials Corporation

- Owens Corning

- CertainTeed Corporation

- Carlisle Companies Inc.

- IKO Industries Ltd.

- Tamko Building Products

- Johns Manville

- Firestone Building Products(Holcim)

- Sika AG

- Soprema Group

- Atlas Roofing Corporation

- Beacon Building Products

- CentiMark Corporation

- Tecta America

- Flynn Group of Companies

- Baker Roofing Company

- Nations Roof

- IronHead Roofing

- Malarkey Roofing Products

- Best Contracting Services

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states roofing market size is expected to grow from USD 32.66 billion in 2025 to USD 34.66 billion in 2026 and is forecast to reach USD 46.67 billion by 2031 at 6.01% CAGR over 2026-2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, and More), by Construction Type (New Construction, Reroofing, and Replacement), by Application (Residential, Commercial, Industrial, Institutional, Others), and by Geography (North East, Mid West, South East, West, South West). The Market Forecasts are Provided in Terms of Value (USD).

United States Roofing Market Trends and Insights

Aging Roof Stock and Higher Replacement Cycles Sustaining Reroofing Demand

More than one-third of U.S. owner-occupied homes were built before 2000, and the median roof age exceeded 17 years in 2025, moving millions of coverings beyond their typical service life. This demographic swell assures baseline work for contractors even when housing starts slow. Homeowners often upgrade to laminated shingles or metal during tear-offs, lifting ticket values by double digits. Insurers now request roof inspections when policies renew on homes older than 15 years, shortening the lag between failure and action. As a result, consistent replacement volume underpins the United States roofing market .

Storm and Hail Events Increasing Insurance-Funded Roofing Activity

Severe convective storms generated more than USD 15 billion in roof-related claims across Texas, Oklahoma, and Iowa during 2024-2025. Carriers responded by insisting on impact-resistant shingles certified to UL 2218 Class 4 in high-risk zones. These premium products cost around 18% more but earn homeowners sizable premium credits, directing spend toward higher-margin materials. Florida's revised wind codes after Hurricane Ian are also forcing early replacements of non-compliant roofs. Collectively, these conditions accelerate reroof cycles and elevate value per square.

Skilled Labor Shortages Limiting Contractor Capacity and Raising Costs

Roofing firms recorded vacancy rates of 12% in 2025 despite wage hikes to USD 28 per hour. Scarcity is sharpest in colder regions where an aging workforce lacks replacements. Contractors are buying robotic applicators and material lifts to offset head-count gaps, but equipment costs raise overhead. Extended lead times of eight to twelve weeks push some owners to defer projects, trimming near-term volume and tempering growth for the United States roofing market.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Upgrades Boosting Demand for Cool Roofs and Better Insulation Systems

- Growth in Logistics Warehouses and Data Centers Expanding Commercial Roofing Installations

- Volatility in Asphalt, Metal, and Insulation Input Prices Pressuring Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Asphalt shingles held 58.6% of the United States roofing market share in 2025, keeping them firmly in the lead across materials. Their scale reflects a wide installer network, familiar installation methods, strong residential distribution, and a reroofing cycle that still leans heavily toward shingle replacement. Owens Corning stated that the U.S. asphalt shingle market totaled 160 million squares in 2024, with 135 million squares from reroof and repair activity, indicating how much of the material base is tied to recurring replacement work rather than new construction. Owens Corning also noted in 2025 that laminate products accounted for 95% of shingle demand, indicating that the United States roofing market has already shifted away from standard 3-tab products toward higher-value laminated systems. That mix matters because laminates support better selling prices, stronger impact ratings, and better alignment with insurer preferences in hail-prone states.

The United States roofing market for single-ply membranes is forecast to grow at a 7.69% CAGR through 2031, making that group the fastest-growing material category. This expansion reflects stronger code alignment in low-slope commercial work, where reflective Thermoplastic Polyolefin, Ethylene Propylene Diene Monomer, and Polyvinyl Chloride systems better meet efficiency and maintenance requirements than many legacy alternatives. California's current code direction and federal efficiency standards are helping move reroof specifications toward those systems, especially where owners want compliance and lower cooling loads in the same project. GAF's 425,000-square-foot Thermoplastic Polyolefin plant in Valdosta, Georgia, which began production in September 2024, demonstrates that manufacturers are adding real capacity to this shift. Metal, modified bitumen, tile, wood, and other materials remain important in specific regional niches. However, the United States roofing market still relies on asphalt shingles for volume and on membranes for the strongest forward growth.

List of Companies Covered in this Report:

- GAF Materials Corporation

- Owens Corning

- CertainTeed Corporation

- Carlisle Companies Inc.

- IKO Industries Ltd.

- Tamko Building Products

- Johns Manville

- Firestone Building Products (Holcim)

- Sika AG

- Soprema Group

- Atlas Roofing Corporation

- Beacon Building Products

- CentiMark Corporation

- Tecta America

- Flynn Group of Companies

- Baker Roofing Company

- Nations Roof

- IronHead Roofing

- Malarkey Roofing Products

- Best Contracting Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights & Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging roof stock and higher replacement cycles sustaining reroofing demand

- 4.2.2 Storm and hail events increasing insurance-funded repairs and re-roof activity

- 4.2.3 Energy-efficiency upgrades boosting demand for cool roofs and better insulation systems

- 4.2.4 Growth in logistics warehouses and data centers expanding commercial roofing installations

- 4.2.5 Adoption of solar-ready and rooftop PV-integrated roofing increasing upgrade spending

- 4.3 Market Restraints

- 4.3.1 Skilled labor shortages limiting contractor capacity and raising installation costs

- 4.3.2 Volatility in asphalt shingles, metal, and insulation input prices pressuring margins

- 4.3.3 Permitting, insurance, and warranty requirements extending project timeline

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay & Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes (TPO, EPDM, and PVC)

- 5.1.6 Wood

- 5.1.7 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North East

- 5.4.2 Mid West

- 5.4.3 South East

- 5.4.4 West

- 5.4.5 South West

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 GAF Materials Corporation

- 6.3.2 Owens Corning

- 6.3.3 CertainTeed Corporation

- 6.3.4 Carlisle Companies Inc.

- 6.3.5 IKO Industries Ltd.

- 6.3.6 Tamko Building Products

- 6.3.7 Johns Manville

- 6.3.8 Firestone Building Products (Holcim)

- 6.3.9 Sika AG

- 6.3.10 Soprema Group

- 6.3.11 Atlas Roofing Corporation

- 6.3.12 Beacon Building Products

- 6.3.13 CentiMark Corporation

- 6.3.14 Tecta America

- 6.3.15 Flynn Group of Companies

- 6.3.16 Baker Roofing Company

- 6.3.17 Nations Roof

- 6.3.18 IronHead Roofing

- 6.3.19 Malarkey Roofing Products

- 6.3.20 Best Contracting Services

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類)

屋面材料市場:2026-2032年全球市場預測(按屋頂類型、材料類型、安裝類型、分銷管道和應用分類)水泥屋頂材料市場:2026-2032年全球市場預測(依產品種類、厚度、材質成分、應用、最終用途及通路分類) 中東和北非屋頂材料市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東歐屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲屋頂材料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)東協屋頂材料市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和北非屋頂材料市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東歐屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區屋頂材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲屋頂材料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)東協屋頂材料市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)印度屋頂工程:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告

2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告